Learning Outcomes

This article explains cash versus accrual accounting, including:

- Distinguishing how each method recognizes revenues and expenses

- Linking recognition timing to the income statement, balance sheet, and cash flow statement

- Applying the matching principle and period cut-off under accrual accounting

- Identifying how credit sales and payables affect profit and liquidity under each method

- Interpreting exam-style data that mix cash-based and accrual-based information

This article explains the mechanics, recognition principles, and analytical implications of cash and accrual accounting for CFA Level 1 candidates. It clarifies how each method records revenues and expenses, distinguishes timing based on cash movements versus economic activity, and links these differences to reported profit and financial position. The article explains core concepts such as revenue recognition under both bases, the matching principle for expenses, and the role of period cut‑off in ensuring that transactions are assigned to the correct reporting period. It emphasizes how cash accounting can distort performance for firms with significant credit sales or payables, contrasted with the more decision‑useful but judgment‑dependent information produced under accrual accounting. The discussion prepares candidates to compare methods in exam questions, adjust for recognition differences when interpreting ratios, and identify when an item in a vignette refers to cash flows versus accrual-based income or expense. It also supports the ability to evaluate strengths, weaknesses, and exam-relevant risks of each approach.

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are required to understand how accounting methods affect reported financial results and the interpretation of financial statements, with a focus on the following syllabus points:

- The distinction between cash and accrual accounting methods for recognizing income and expenses

- Implications of each method for reported performance and position

- The effect of recognition timing and measurement on financial analysis

- Comparing limitations and benefits for exam scenarios

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which statement best describes revenue recognition under cash accounting?

- a) Revenue is recognized when goods are shipped to the customer.

- b) Revenue is recognized when the customer accepts delivery.

- c) Revenue is recognized when cash is received from the customer.

- d) Revenue is recognized when an invoice is issued.

-

Under accrual accounting, when is an expense normally recognized?

- a) When the supplier is selected.

- b) When cash is paid to the supplier.

- c) When the related revenue is earned or the obligation is incurred.

- d) When the purchase order is approved.

-

Which of the following is a key weakness of pure cash-basis accounting for a company with extensive credit sales and purchases?

- a) It overstates total assets.

- b) It ignores non-cash expenses such as depreciation.

- c) It can seriously misrepresent profitability across periods.

- d) It cannot be used to produce a statement of cash flows.

-

A rapidly growing company switches from cash accounting to accrual accounting. If it has substantial receivables and payables, its reported profit in the transition year is most likely to:

- a) Decrease because expenses will be recognized earlier.

- b) Increase because credit sales will be recognized before cash is received.

- c) Stay the same because total cash collected is unchanged.

- d) Become negative because non-cash items are excluded.

Introduction

A clear understanding of the difference between cash and accrual accounting is fundamental for financial reporting and analysis. The method chosen for revenue and expense recognition can have a significant impact on a company's reported profits, financial position, and comparability across reporting periods. The CFA curriculum requires you to not only identify the mechanics of each approach but also to appreciate their implications for interpreting financial statements and making investment decisions.

Modern financial reporting standards (IFRS and US GAAP) are built on the accrual basis of accounting. This means that income statements and balance sheets for listed companies are prepared using accrual accounting, with a separate statement of cash flows to show cash receipts and payments. The use of accruals and estimates introduces judgment, but it also allows the financial statements to reflect the true economic activity more faithfully than cash accounting alone.

Key Term: Cash Accounting

Cash accounting is an accounting method that records revenues and expenses only when cash is received or paid, regardless of when the transaction occurs. Key Term: Accrual Accounting

Accrual accounting is an accounting method that records revenues when earned and expenses when incurred, irrespective of when cash is exchanged.

Understanding how and why these methods differ will help in:

- Interpreting the relationship between net income (accrual-based) and cash from operations (cash-based)

- Assessing earnings quality (the extent to which earnings are supported by cash flows)

- Answering exam questions that mix invoiced amounts, cash receipts, and changes in working capital.

Cash Accounting

Cash accounting is a straightforward system where transactions are recorded only when cash changes hands. Revenue is recognized when payments are received, and expenses are recorded when cash is paid out. This approach matches closely with cash flows but can provide a misleading picture of profitability and financial position if substantial sales or purchases occur on credit.

Key Term: Revenue Recognition (Cash Basis)

Revenue recognition (cash basis) means recognizing revenue only when payment is actually received from the customer.

Under cash accounting:

- Credit sales are ignored until customers pay

- Purchases on credit are ignored until suppliers are paid

- There are no accounts receivable, accounts payable, or other accruals on the balance sheet

- Reported profit is effectively “cash in minus cash out” for the period.

Cash accounting can be useful for very small or cash-only businesses, where credit transactions are minimal and the key focus is on cash management. However, two issues are critical for exam purposes:

-

Timing distortions: A business may carry out most of its work in one period but collect cash in another. Profit will be reported in the period of cash collection, not the period of economic activity. This can make performance look volatile and can be easily “managed” by accelerating or delaying payments.

-

Incomplete financial position: Because receivables, payables, and other obligations are not recorded until cash moves, the balance sheet under pure cash accounting understates both assets and liabilities. It may appear that the business has fewer obligations or less value than in reality.

For these reasons, cash-basis financial statements are not permitted for public companies under IFRS and US GAAP. However, the statement of cash flows for those companies is always prepared on a cash basis, so understanding cash accounting remains important.

Accrual Accounting

Accrual accounting, required by IFRS and US GAAP for public companies, recognizes income when it is earned and expenses when obligations are incurred, regardless of the timing of actual cash flows. This method is designed to present a more accurate, period-based view of a company's performance and obligations. It relies on applying specific recognition and matching principles.

Key Term: Revenue Recognition (Accrual Basis)

Revenue recognition (accrual basis) means recognizing revenue when goods or services are delivered and the earnings process is substantially complete, provided it is probable that economic benefits will flow to the entity and the amount can be reliably measured, even if cash has not yet been received. Key Term: Expense Recognition (Matching Principle)

Expense recognition under the matching principle means recording expenses in the period in which the related revenues are earned, not necessarily when cash is paid.

Within the accrual framework:

- Revenues are recognized when control of goods or services passes to the customer (e.g., on delivery or completion), not when cash is collected.

- Expenses are recognized when they help generate revenue or when the entity becomes obliged to pay them, not when cash leaves the bank.

Accrual accounting leads to several key balance sheet items:

Key Term: Accounts Receivable

Accounts receivable are amounts owed by customers for goods or services already delivered on credit but not yet paid for in cash. Key Term: Accounts Payable

Accounts payable are amounts owed to suppliers for goods or services already received where payment is deferred. Key Term: Prepaid Expense

A prepaid expense is an amount paid in advance for a good or service to be consumed in future periods (e.g., prepaid rent or insurance). Key Term: Unearned Revenue (Deferred Revenue)

Unearned revenue is cash received before goods or services are delivered; it is recorded as a liability until the revenue is earned. Key Term: Accrued Expense

An accrued expense is an expense that has been incurred but not yet paid in cash (e.g., wages earned by employees but not yet paid at year-end).

These items allow the financial statements to capture the timing differences between economic events and their related cash flows.

For CFA purposes, accrual accounting:

- Improves period-to-period comparability of performance

- Provides a more complete picture of financial position

- Requires judgment and estimation (e.g., allowance for doubtful accounts, useful lives for depreciation), which can affect earnings quality.

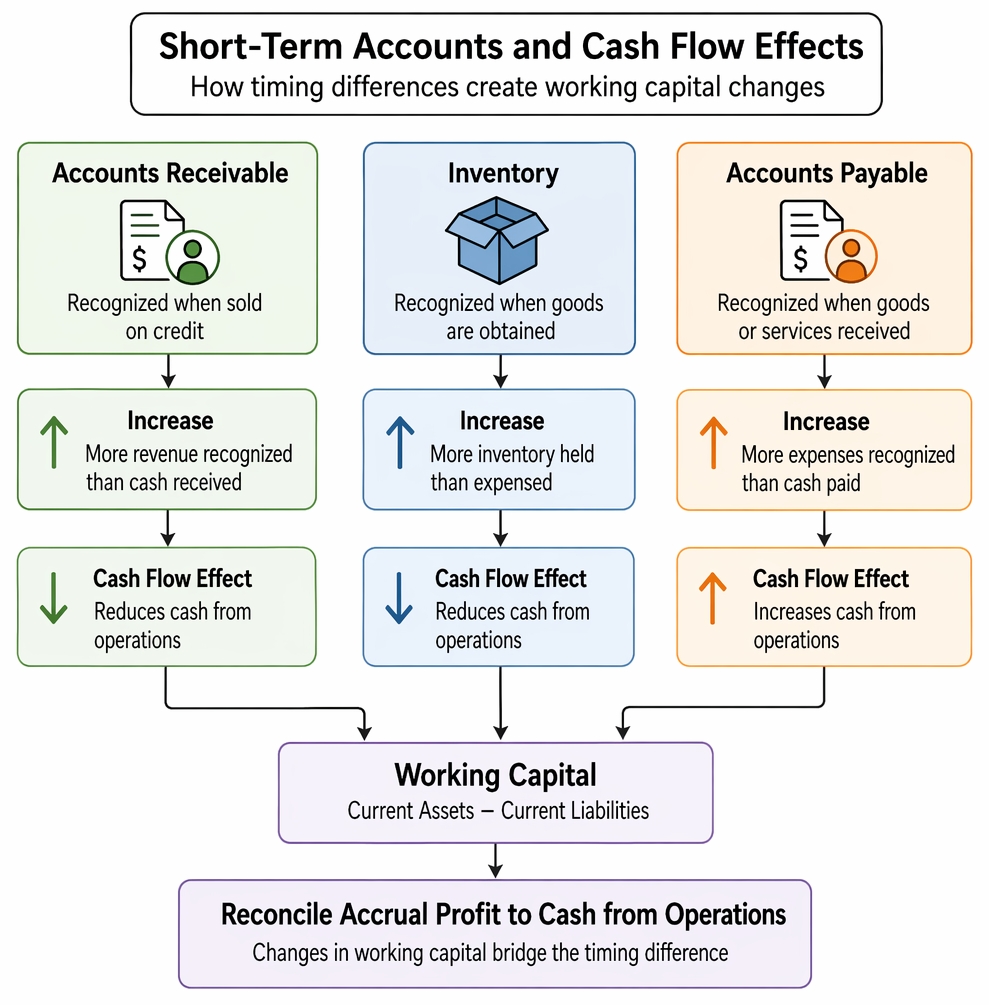

Accrual Adjustments and Short-Term Accounts

Short-term assets and liabilities are central to understanding the link between accrual profit and cash flows.

Accrual accounting records a credit sale as revenue and accounts receivable before subsequent customer payment converts receivables into cash.

Under accrual accounting:

- Accounts receivable are recognized when the product or service is sold on credit and derecognized when cash is received.

- Inventory is recognized when ownership of goods is obtained and derecognized when goods are sold (through cost of goods sold).

- Accounts payable are recognized when goods or services are received and derecognized when cash is paid to suppliers.

These timing differences create working capital (current assets minus current liabilities), and changes in working capital reconcile accrual-based net income to cash from operations.

For example:

- If accounts receivable increase, the company has recognized more revenue on an accrual basis than cash received from customers.

- If accounts payable increase, the company has recognized more expenses than cash actually paid to suppliers, improving cash flows relative to accrual expenses.

Understanding these relationships is critical when interpreting the statement of cash flows and when converting between cash and accrual information in exam questions.

Comparison: Key Mechanics

| Cash Accounting | Accrual Accounting | |

|---|---|---|

| Revenue | When cash is received | When earned (goods/services delivered; performance obligations satisfied) |

| Expense | When cash is paid | When incurred or matched to revenue |

| Timing | Follows cash flows | Follows economic activity (period-based) |

| GAAP/IFRS | Not permitted for public companies | Required for public companies |

Additional Mechanics

Under accrual accounting, each revenue or expense has two aspects:

- An income statement effect (revenue or expense recognized)

- A balance sheet effect (change in an asset or liability such as cash, receivables, inventory, payables, or equity)

Under cash accounting, the balance sheet effects are largely limited to cash and owner’s equity, resulting in a much simpler but less informative financial position.

Worked Example 1.1

A consulting firm completes a project on 20 December. The client pays on 15 January. When is the revenue recognized under each method?

Answer:

- Under cash accounting: Revenue is recognized in January, when payment is received.

- Under accrual accounting: Revenue is recognized in December, when the work was completed and the earnings process was substantially complete.

Worked Example 1.2

A company buys raw materials worth $50,000 on credit on 28 February and pays the invoice in March. Under each method, when is the expense recorded?

Answer:

- Under cash accounting: Expense is recorded in March, when cash is paid.

- Under accrual accounting: Expense is recorded in February, when the obligation to pay is incurred and the materials are used in production in that period.

Worked Example 1.3 – Credit Sales and Profit Timing

A retailer sells goods that cost $60,000 on credit for $100,000 on 30 November. Customers pay in cash on 15 January. There are no other transactions.

What is the profit in the year ended 31 December under each method?

Answer:

- Under cash accounting:

- No cash has been received or paid by 31 December, so revenue and expense are both zero.

- Profit for the year ended 31 December = 0.

- Under accrual accounting:

- Revenue recognized in November = $100,000 (goods delivered).

- Cost of goods sold = $60,000.

- Profit for the year ended 31 December = $40,000. Accrual accounting shows the economic profit in the correct period, even though cash will be received in the next year.

Worked Example 1.4 – Prepaid Expense

On 1 October, a company pays $12,000 for a 12‑month insurance policy covering 1 October to 30 September next year.

What expense is recognized in the current year (ending 31 December) under accrual accounting, and what is the cash outflow?

Answer:

- Cash outflow in October: $12,000 (cash accounting would treat this as a $12,000 expense in October).

- Under accrual accounting:

- Insurance expense for current year = 3 months (October–December) × $1,000 per month = $3,000.

- Prepaid insurance (asset) at year-end = remaining 9 months × $1,000 = $9,000. Accrual accounting spreads the cost over the periods that benefit from the insurance coverage.

Implications for Financial Analysis

Cash accounting may misstate performance—particularly for businesses with significant receivables or payables—since profits can be “managed” by timing payments. For example:

- Delaying payment to suppliers can make a cash‑basis profit look higher in the current period.

- Collecting receivables aggressively before year-end can inflate current-period cash-basis revenue.

Accrual accounting offers a more accurate measure of performance in each period but requires greater judgment and introduces estimation risk (e.g., in doubtful debts, warranty provisions, depreciation). Analysts must therefore evaluate both:

- The quality of earnings (the degree to which earnings are backed by cash flows)

- The reasonableness of accruals and estimates.

Key Term: Matching Principle

The matching principle requires that expenses be recorded in the same period as the revenues they help to generate, so that reported profit reflects true performance for that period. Key Term: Period Cut-off

Period cut-off is the process ensuring that income and expenditures are recognized in the correct accounting period, as required by accrual accounting.

Accrual Accounting and the Statement of Cash Flows

While the income statement is accrual-based, the statement of cash flows reports:

- Cash from operating activities (CFO)

- Cash from investing activities

- Cash from financing activities.

Under the indirect method (common in practice), CFO starts with net income and adjusts for:

- Non‑cash items (e.g., depreciation, amortization)

- Changes in working capital (receivables, inventory, payables, and other accruals).

From the source material, analysts are expected to compare:

- Net income (accrual measure of performance), and

- Cash from operations (cash measure of performance),

to assess earnings quality. For mature companies, operating cash flow is usually expected to exceed net income over time because net income includes non‑cash charges such as depreciation.

Converting Between Accrual and Cash for Operating Items

The Level 1 curriculum shows how to move from accrual figures to cash figures using changes in related balance sheet accounts. For example, cash paid to suppliers can be approximated as:

-

Purchases from suppliers = Cost of goods sold

- Increase in inventory (or − decrease in inventory)

-

Cash paid to suppliers = Purchases from suppliers − Increase in accounts payable (or + decrease in accounts payable)

This logic reflects that:

- If inventory increases, the company purchased more goods than it sold, increasing cash outflow relative to cost of goods sold.

- If accounts payable increase, the company has not yet paid for some purchases, so cash outflow is lower than accrual purchases.

Being able to apply this type of reasoning helps in exam questions where you must derive a cash‑flow figure from accrual data (or vice versa).

Cash vs. Accrual—Strengths, Weaknesses, and CFA Relevance

-

Cash accounting:

-

Strengths:

- Tracks liquidity directly by focusing only on cash movements.

- Simple to apply and understand, with minimal estimates.

- Useful for very small or cash‑based businesses and for personal cash budgeting.

-

Weaknesses:

- Poor measure of profitability when there are significant credit sales, credit purchases, or prepayments.

- Omits key assets and liabilities (receivables, payables, accrued expenses, unearned revenue).

- Earnings easily influenced by timing of payments and collections.

-

-

Accrual accounting:

-

Strengths:

- Better reflects economic performance by matching revenues and expenses to the correct period.

- Produces a more complete balance sheet, including receivables, payables, and other obligations.

- Forms the basis of IFRS and US GAAP financial reporting and is central to valuation analysis.

-

Weaknesses:

- Requires estimates and judgment, introducing subjectivity (e.g., provisions, depreciation, impairment).

- Complex to apply and interpret; misapplication can reduce comparability and reliability.

- Creates a gap between net income and cash flows that must be understood and analyzed.

-

For exam purposes:

- Almost all financial statement analysis is based on accrual accounting.

- Many questions require distinguishing whether a number is cash-based (e.g., “cash received from customers”) or accrual-based (e.g., “sales revenue” or “cost of goods sold”).

- Candidates must be able to interpret adjustments involving receivables, inventory, and payables to move between accrual and cash amounts.

Exam Warning: Cash-based numbers (like timing of receipts and payments) can deviate significantly from reported accrual-based net income, especially for growing companies or where significant credit terms are offered. For CFA questions, always check whether the figure needed is cash-based or accrual-based.

Revision Tip: If you are given both a cash receipts/payments schedule and invoice-based (accrual) sales/purchases table, pause to note which method the question is really asking about, and double-check the period being used.

Summary Table: Cash vs. Accrual Accounting—Quick Reference

| Feature | Cash Basis | Accrual Basis |

|---|---|---|

| Recognition Timing | When cash changes hands | When earned/incurred |

| Revenues | On cash receipt | On delivery of goods/services or completion of service |

| Expenses | On cash payment | When obligation incurred or matched to related revenue |

| Financial Position | Understates payables/receivables and other accruals | More complete, includes receivables, payables, accruals |

| CFA Focus | Not permitted under GAAP/IFRS for listed companies | Required by standards; core for valuation and analysis |

Key Point Checklist

This article has covered the following key knowledge points:

- Explain the difference between cash and accrual accounting

- Identify when revenues and expenses are recognized under each method

- Understand the matching principle and its relevance under accrual accounting

- Recognize the role of receivables, payables, prepaid expenses, unearned revenue, and accrued expenses

- Understand how changes in working capital link accrual profit to cash flows

- Recognize the implications of recognition method for performance analysis and exam questions

- List strengths and weaknesses of cash and accrual accounting

Key Terms and Concepts

- Cash Accounting

- Accrual Accounting

- Revenue Recognition (Cash Basis)

- Revenue Recognition (Accrual Basis)

- Expense Recognition (Matching Principle)

- Accounts Receivable

- Accounts Payable

- Prepaid Expense

- Unearned Revenue (Deferred Revenue)

- Accrued Expense

- Matching Principle

- Period Cut-off