Learning Outcomes

This article explains covariance, correlation, and portfolio variance in the context of CFA Level 1 portfolio management, including:

- How to calculate and interpret covariance between two return series, and what positive, negative, and zero values imply about co-movement.

- How to compute and interpret the correlation coefficient, recognize its −1 to +1 range, and compare the diversification potential of different correlation levels.

- How to calculate portfolio variance and standard deviation for two-asset and simple multi-asset portfolios using covariances or correlations and asset weights.

- How correlation and covariance jointly determine portfolio risk, and why portfolio volatility is not merely a weighted average of individual asset risks.

- How combining assets with low or negative correlation reduces overall portfolio risk, and the conditions under which diversification benefits are maximized.

- How to contrast portfolios with perfectly positive, imperfect, and perfectly negative correlation to identify which offers greater risk reduction.

- How CFA exam questions typically test these concepts through numerical problems, conceptual scenarios, and interpretation of co-movement measures.

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are expected to understand core statistical measures relevant for portfolio returns, with a focus on the following syllabus points:

- Calculate and interpret covariance and correlation between two return series.

- Calculate portfolio variance and standard deviation for two-asset and multi-asset portfolios.

- Explain the diversification effect of combining assets that are not perfectly correlated.

- Describe how covariance and correlation drive portfolio risk, not just individual asset risk.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- How does correlation between two assets influence risk reduction when they are combined in a portfolio?

- What does a covariance of zero between two returns indicate?

- Portfolio A contains two stocks with a correlation of +1.0. Portfolio B contains two stocks with a correlation of –0.5. Which portfolio will offer greater risk reduction, and why?

- If you add more assets with correlations below 1 to your portfolio, what happens to total portfolio risk, holding other things constant?

Introduction

Statistical concepts are central to understanding how asset returns interact, particularly in portfolio management. Examining not only the individual risk and return of each investment but also how they move together is essential for effective diversification—one of the core principles of modern portfolio theory.

Key Term: covariance

Covariance measures how two random variables (such as asset returns) vary together. Positive covariance means they tend to move in the same direction; negative indicates opposite movement. Key Term: correlation

Correlation is a standardized measure of the linear relationship between two variables, ranging from –1 (perfectly opposite) to +1 (perfectly aligned). It is the covariance divided by the product of their standard deviations.

Covariance: Measuring Co-Movement

Covariance quantifies the tendency of two assets’ returns to move together. If Asset X and Asset Y have positive covariance, when Asset X has a return above its mean, Asset Y likely does too. Negative covariance means when one asset is above its average, the other is below.

The formula for sample covariance is:

where and are paired observations and , their means.

Covariance is reported in units squared and is not bounded, making direct interpretation challenging.

Key Term: portfolio variance

The measure of how spread out portfolio returns are, determined by both individual asset risk and the relationships (covariances) between each pair of assets.

Correlation: Comparing Risk Reduction Potential

Correlation solves the comparability problem of covariance by dividing it by the product of each asset’s standard deviation, yielding a measure between –1 and +1. It informs you how reliably one asset moves in tandem with another:

Correlation interprets as follows:

- 0: No linear relationship.

- +1: Always move together.

- –1: Always move in opposite directions.

Low or negative correlation is desired for diversification.

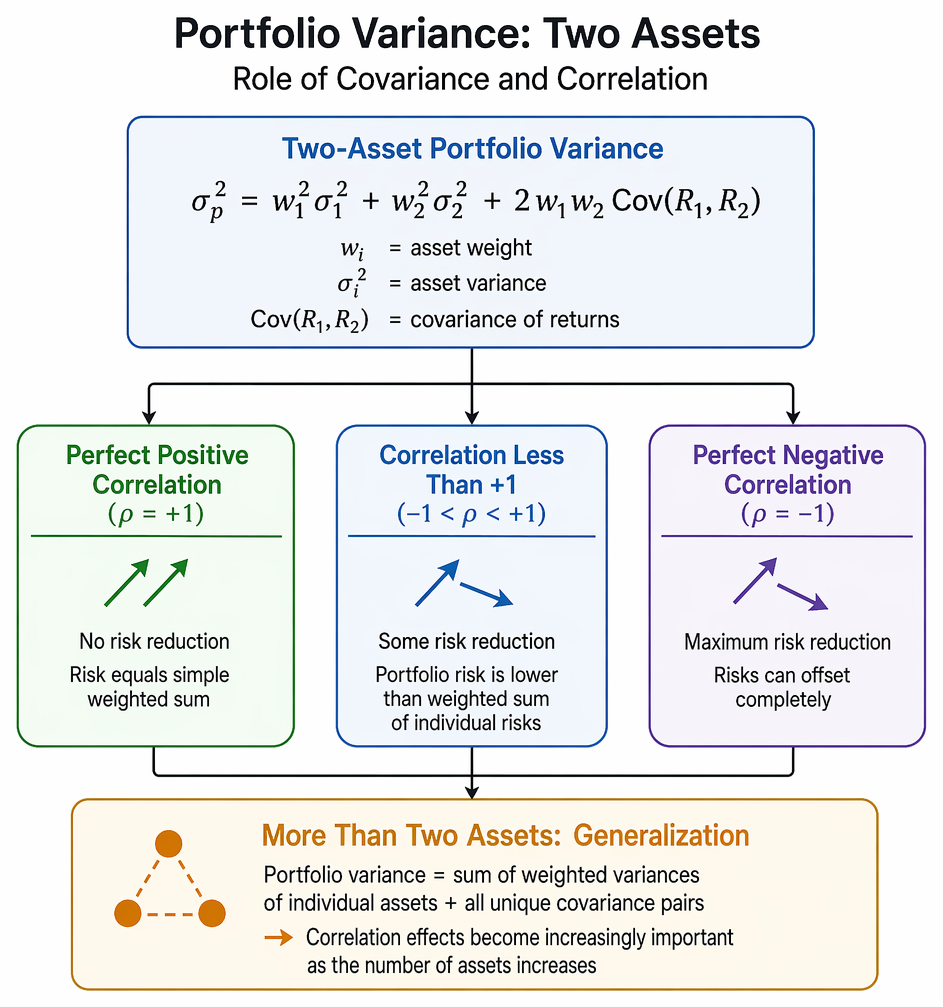

Portfolio Variance: The Role of Covariance and Correlation

The variance of a portfolio containing two assets depends on how their returns interact:

Portfolio risk for two assets is derived from weighted variances and co-movement, with lower correlation reducing volatility below the weighted average.

Where are asset weights, asset variances, and their covariance.

If assets have perfect positive correlation (), portfolio risk is a simple weighted sum—no risk reduction. If correlation is less than +1, portfolio risk is lower than the weighted sum of individual risks.

When combining more than two assets, the formula generalizes: portfolio variance equals the sum of weighted variances of individual assets plus all the unique covariance pairs, emphasizing the growing importance of correlation as the number of assets increases.

Benefits of Diversification

Combining assets with low or negative correlation reduces overall portfolio volatility. The lower the correlation between assets, the greater the diversification benefit. A perfectly negative correlation () allows a portfolio to be constructed with zero risk if individual weights are set appropriately.

Key Term: diversification

The risk reduction strategy achieved by combining assets with less-than-perfectly correlated returns; optimal when correlations are low or negative.

Worked Example 1.1

Portfolio Variance with Two Assets

Suppose Asset A and Asset B both have a standard deviation of 12%. The correlation between their returns is 0.5. You invest 60% in A and 40% in B.

Answer:

Portfolio SD =

A correlation under 1.0 provides significant risk reduction compared to taking a simple weighted average of risks.

Worked Example 1.2

Effects of Correlation

You hold two stocks, each with 10% expected return and 20% standard deviation. Consider three cases:

a) Correlation +1.0 b) Correlation 0 c) Correlation –1.0 Suppose you invest 50% in each.

Answer:

a) Portfolio SD = 20% (no reduction; moves in lockstep). b) Portfolio SD = 14.1% (risk reduced). c) Portfolio SD = 0% (perfect hedging).Exam Warning: Be alert for CFA questions using the formula for portfolio variance. Carefully check the correlation coefficient and asset weights before plugging values into the formula. Many students lose marks by failing to convert percentages to decimals or by misapplying the formula for more than two assets.

Revision Tip: When reviewing for the CFA exam, focus your calculation practice on scenarios where assets have correlations less than 1.0, as these yield maximum diversification benefits.

Summary

Understanding covariance, correlation, and portfolio variance is fundamental for CFA candidates and investment professionals. Portfolio risk is not simply the sum of individual asset risks—it is shaped by how assets move together. Combining assets with less-than-perfect correlation reduces risk, and well-diversified portfolios rely heavily on this effect. Proficiency in these calculations and conceptual relationships equips you to tackle CFA exam portfolio management questions and apply effective diversification in practice.

Key Point Checklist

This article has covered the following key knowledge points:

- Calculate and interpret covariance and correlation between return series.

- Compute portfolio variance and standard deviation using these measures.

- Explain how correlation less than +1.0 allows for risk reduction via diversification.

- Identify why portfolio risk is not simply a weighted average of individual risks.

- Recognize the importance of covariance and correlation in constructing diversified portfolios.

Key Terms and Concepts

- covariance

- correlation

- portfolio variance

- diversification