Learning Outcomes

This article explains the mechanics, valuation, and risk management uses of interest rate and currency swaps in a CFA Level 1 context. It clarifies the structure of plain vanilla interest rate swaps and cross-currency swaps, the role of the notional principal, and how fixed and floating legs are determined and settled. It distinguishes cash-flow patterns in interest rate versus currency swaps, including when principal is exchanged and how net versus gross interest payments are calculated. It examines how swaps are used to hedge interest rate and foreign exchange risk, to transform the characteristics of existing assets or liabilities, and to align asset–liability profiles with risk management objectives. It analyzes the main sources of swap risk—market, counterparty, and operational—and how these risks differ between cleared and OTC transactions. It highlights typical CFA Level 1 exam traps, such as confusing notional exchanges, misidentifying the payer and receiver in a swap, and assuming swaps eliminate all risk, and reinforces learning with testable numerical-style applications.

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are expected to understand the function and construction of swaps in financial risk management, with a focus on the following syllabus points:

- Define and describe interest rate swaps and currency swaps

- Identify cash flow structures of fixed-for-floating and cross-currency swaps

- Explain how swaps are used to hedge interest rate and currency risk

- Recognize the risks—market, credit, operational—associated with swaps

- Apply swap payoffs to simple numerical examples

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What cash flows are exchanged in a plain vanilla interest rate swap?

- How can a company use a currency swap to hedge against foreign currency exposure?

- Name one key risk that both counterparties in a swap transaction face.

Introduction

Swaps are fundamental financial derivatives used by institutions, corporations, and investors to manage exposures to interest rate and currency fluctuations. Swaps transform the nature of cash flows, allowing parties to exchange one set of obligations for another. In both exam and practice, candidates must know how swaps function, how they are used to mitigate risk, and the main risks swaps introduce.

Key Term: swap

A contractual agreement between two parties to exchange future cash flows, based on pre-arranged terms, over a set period.

Types of Swaps

Interest rate swaps and currency swaps are the most common swaps tested at CFA Level 1.

Key Term: interest rate swap

An agreement where two parties exchange future interest payments, typically one fixed-rate for one floating-rate, on a notional principal. Key Term: currency swap

An agreement where two parties exchange principal and future interest payments in different currencies, usually both at fixed or both at floating rates.

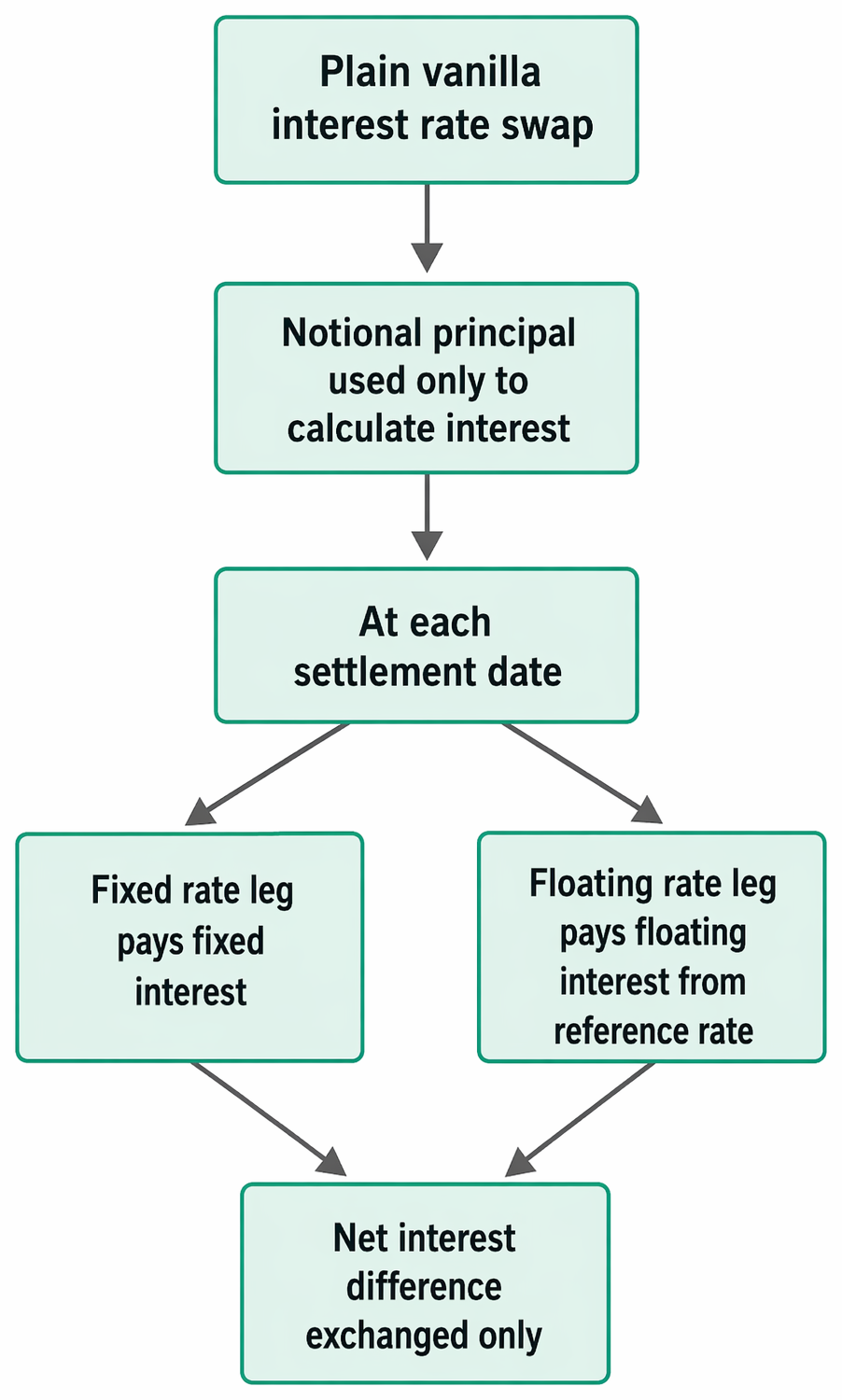

Interest Rate Swaps

In a plain vanilla interest rate swap, one party pays a fixed interest rate and receives a floating rate, or vice versa, on a notional amount. The notional amount is not exchanged; it simply serves as the basis for the interest calculations.

Plain vanilla interest rate swaps calculate fixed and reference-rate floating coupons on notional principal and settle only the net interest differential.

The floating rate is usually referenced to an index such as LIBOR. Settlement occurs periodically (commonly semiannually), with only the net difference between fixed and floating interest payments exchanged.

Key Term: plain vanilla interest rate swap

A fixed-for-floating interest rate swap, using a notional principal, where only interest differentials are exchanged.

Currency Swaps

A currency swap involves initial and final exchanges of principal in two currencies, along with periodic interest payments. Each party effectively diverts exposure to a different currency. Currency swaps may involve fixed-for-fixed, floating-for-fixed, or floating-for-floating arrangements.

The most common use is to convert a liability or asset in one currency into another without closing out the original position.

Worked Example 1.1

Scenario: A US company needs to finance €5 million for a European project. It has good credit in the US and can borrow $ at a lower rate but faces unfavorable euro borrowing rates. A European company has access to better EUR rates but wants $ exposure. They enter a currency swap: the US firm borrows $, the European firm borrows EUR; they exchange principals at spot and swap their interest payments. At maturity, the principal amounts are swapped back at the original rate.

Answer:

The US firm obtains effective euro financing at a lower cost, hedging its EUR exposure. The European firm does the same for USD. Both hedge currency risk and gain more favorable borrowing costs.

Swap Cash Flows

For both types of swaps:

- Interest rate swaps: No exchange of principal; periodic net interest exchanged.

- Currency swaps: Both principal and interest are exchanged in different currencies; principal typically exchanged at inception and maturity.

Worked Example 1.2

Question: In a 3-year USD/EUR fixed-for-fixed currency swap (principal $10 million/€8 million), with annual payments, what flows occur at initiation and at the first payment date?

Answer:

At initiation: The parties exchange $10m for €8m at spot. At year 1: Each pays interest on the currency received—US party pays € interest on €8m, EU party pays USD interest on $10m.

Swap Applications in Risk Management

Swaps are mainly used to:

- Hedge interest rate exposure (e.g., convert fixed-rate debt to floating to benefit if rates decline, or vice versa).

- Hedge currency risk (e.g., convert USD cash flows into local currency to avoid FX fluctuations).

Institutions may also use swaps to match asset and liability profiles or restructure portfolios without transacting in the reference securities.

Worked Example 1.3

Question: How can a company with a floating-rate loan use a swap to convert it into a synthetic fixed-rate loan?

Answer:

It enters into a pay-fixed, receive-floating interest rate swap on the same notional as its loan. The swap fixed payment plus the floating-rate loan net to a synthetic fixed-rate obligation.

Swap Risks

Swaps create exposures that must be understood for both exam and practice.

Key Term: counterparty risk

The risk that one party in a swap defaults and does not fulfill contractual obligations. Key Term: market risk

The risk of loss from adverse movements in interest rates or FX rates affecting swap value. Key Term: operational risk

Risk of loss from process failures or errors in documenting, managing, or settling swap transactions.

Credit risk in swaps is bilateral: each party faces the risk that the other could default, especially if the swap is in their favor ("in the money"). Swaps are usually traded over-the-counter (OTC); central clearing has become more prominent to reduce this risk.

Exam Warning: A common exam error is assuming that swaps eliminate all risk. Swaps can hedge market risk but may introduce or concentrate credit and operational risks. Also, swaps usually do not hedge principal risk in an interest rate swap, as the notional is never exchanged.

Revision Tip: Always distinguish between an interest rate swap (only interest flows, no principal exchanged) and a currency swap (principal and interest both exchanged in two currencies).

Summary

Swaps are fundamental instruments for transforming exposures between interest rates and currencies. Interest rate swaps exchange fixed and floating interest obligations; currency swaps exchange both principal and interest in two currencies. Swaps can efficiently hedge risk but also introduce credit and operational risks. Proficiency involves knowing swap structures, applications, and key definitions.

Key Point Checklist

This article has covered the following key knowledge points:

- Define and describe plain vanilla interest rate and currency swaps

- Identify and explain swap cash flows for both types

- Explain how swaps can hedge interest rate and currency risks

- Recognize the main risks in swap transactions, including counterparty risk

- Apply swap applications using illustrative numerical examples

Key Terms and Concepts

- swap

- interest rate swap

- currency swap

- plain vanilla interest rate swap

- counterparty risk

- market risk

- operational risk