Learning Outcomes

This article explains loan amortization and cash flow timelines, including:

- calculating periodic loan payments for fully amortizing loans using standard time value of money formulas and financial calculators;

- constructing complete amortization schedules that show interest, principal repayment, and remaining balance for each period;

- interpreting amortization tables to evaluate the cost of borrowing, track outstanding principal, and identify patterns in interest and principal shares over time;

- analyzing cash flow timelines for loans and investment projects to ensure correct timing, sign convention, and matching of interest rates with compounding periods;

- distinguishing between level-payment amortization, interest-heavy early periods, and principal-heavy later periods, and explaining how these features appear in schedules and timelines;

- relating amortization and timeline concepts to typical CFA Level 1 question formats, such as mortgages, car loans, and capital budgeting cash flow sets, to improve speed and accuracy;

- applying these techniques efficiently under exam conditions to check reasonableness of answers and avoid common TVM and loan-setup mistakes.

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are expected to understand the time value of money and its application to loans and investment cash flows, with a focus on the following syllabus points:

- Calculating periodic loan payments for loans with level payments

- Constructing and interpreting loan amortization tables

- Applying timeline diagrams to visualize and solve time value of money problems

- Calculating the outstanding loan principal and interest portions for any period

- Analyzing cash flows for loan and project timelines using annuities and single sums

- Understanding the effect of payment timing and compounding frequency on loan costs

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- A client takes out a $250,000, 20-year mortgage loan with monthly payments and a fixed annual rate of 6%. How do you calculate the required monthly payment?

- Given a loan amortization table, how would you determine the interest and principal components of the 5th payment?

- What does a cash flow timeline represent, and why is it important for analyzing loan and investment projects?

- True or false? For most standard amortizing loans, early payments are composed mainly of interest.

Introduction

Loans and investment projects often involve a series of future cash flows occurring at regular intervals. To analyze, compare, and manage these, students must understand both the time value of money (TVM) and the way payments are structured over time. This article focuses on how to calculate loan payments, construct amortization schedules, and use cash flow timelines for solving investment problems—essential basics for CFA candidates.

Key Term: loan amortization

The process of repaying a loan in equal periodic payments, where each payment covers both interest charged and part of the principal amount. Key Term: cash flow timeline

A graphical representation that shows the size and timing of all relevant cash flows for a loan, investment, or project, indexed by time period. Key Term: amortization schedule

A table or statement showing the allocation of each loan payment between interest and principal across all payment periods.

Loan Amortization Basics

Most personal and business loans are structured as annuities—regular, fixed payments are made over the loan's life. Each payment has two parts:

- Interest – Covers the cost of borrowing for the period (typically based on the remaining outstanding principal).

- Principal repayment – Reduces the outstanding balance.

Over time, as the principal is paid down, the portion of each payment that goes toward interest declines and the principal portion increases.

Key Term: annuity

A series of equal payments made at regular time intervals (e.g., monthly, annually).

The Loan Payment Formula

For a loan of amount (present value), with periodic interest rate , and payment periods, the required equal payment (assuming payments at the end of each period) is:

Where:

- = initial loan principal

- = periodic interest rate (e.g., annual rate divided by number of periods per year)

- = total number of payments

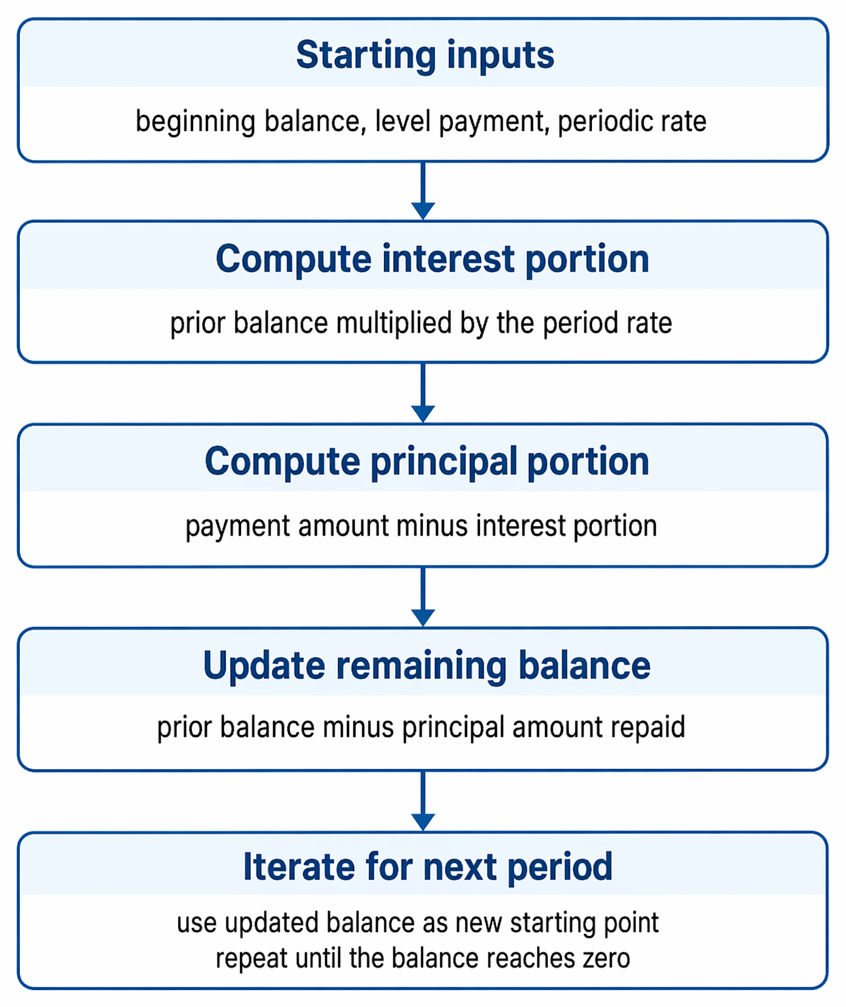

Amortization Schedules

An amortization schedule is a table showing the breakdown of each periodic payment between:

Level-payment amortization is presented as a recursive process linking prior balance, interest expense, principal reduction, and the next period's opening balance.

- Interest paid that period

- Principal repaid that period

- Remaining loan balance after each payment

In the early years, most of each payment is interest. Over time, the principal component becomes larger.

Worked Example 1.1

A borrower takes out a $120,000 loan for 10 years at a fixed annual rate of 5%, compounded monthly. What is the required monthly payment, and what are the principal and interest amounts in the first payment?

Answer:

- Periodic rate: 5%/12 = 0.4167% per month.

- Total payments: 10 x 12 = 120.

- Payment:

- First payment interest:

- Principal:

- New principal after 1st payment:

Worked Example 1.2

After 24 payments, how much of a 25th monthly payment will be interest and how much principal? Continuing from Example 1.1.

Answer:

To find the balance after 24 payments, calculate either by creating an amortization table or by using the loan balance formula: Outstanding principal after k payments:

For month 25's interest:

The rest of the payment is principal.

Cash Flow Timelines

Cash flow timelines are graphical tools that help visualize the pattern and timing of cash flows for loan repayments, investments, or projects.

Timelines always start at time 0 (today). Each “tick mark” to the right represents subsequent periods. Timelines are essential for:

- Keeping track of payment schedules and interest accrual

- Correctly matching interest rates and periods when solving TVM problems

- Preventing errors in payment timing or cash flow sign convention

Key Term: cash flow sign convention

The rule that cash inflows are shown as positive numbers and cash outflows as negative numbers on timelines and in TVM calculations.

Worked Example 1.3

Draw a timeline and explain the cash flows for a 5-year, $25,000 car loan with annual payments of $5,883.70 at 8% interest, paid at year-end.

Answer:

Timeline: t=0 t=1 t=2 t=3 t=4 t=5 [–25k] 5,883.70 5,883.70 5,883.70 5,883.70 5,883.70 At t=0: borrower receives $25,000 (inflow). At each t=1 to 5: pays $5,883.70 (outflows). Interest is being paid each period, principal is shrinking, and at t=5, the loan is fully paid off.

Amortization, Prepayments, and Partial Periods

Amortization schedules may be affected if the borrower makes extra (pre-)payments, pays off the loan early, or misses a scheduled payment. Analysts should be aware of:

- Some contracts allow prepayment without penalty, reducing the interest owed.

- Partial payments require recalculation of the outstanding balance and remaining schedule.

Exam Warning: Do not confuse the payment number with the period referenced in a timeline. The first payment is at the end of period 1, not at time 0.

Revision Tip: On the exam, always draw a timeline for loan and investment cash flow problems. Mark all receipts and payments, including their timing and sign.

Summary

- Amortizing loans require regular fixed payments. Each payment is divided into interest (on outstanding balance) and principal.

- An amortization table shows for each payment the interest, principal, and remaining loan balance.

- Timelines are essential TVM tools—use them to visualize and analyze loan and investment projects.

- Early payments are mainly interest; late payments are mostly principal.

- Prepayments change amortization patterns and remaining loan schedules.

Key Point Checklist

This article has covered the following key knowledge points:

- Calculate the required payment for a fully amortizing loan using the TVM annuity formula.

- Construct (and interpret) an amortization table for a fixed-rate loan.

- Break down any payment into its interest and principal components.

- Use cash flow timelines to analyze TVM problems involving loans and investments.

- Recognize the effect of extra payments or prepayments on remaining loan balances.

Key Terms and Concepts

- loan amortization

- cash flow timeline

- amortization schedule

- annuity

- cash flow sign convention