Learning Outcomes

This article explains how benchmarks and return measures are used in CFA Level 1 performance evaluation, focusing on the precise knowledge and calculations tested in the exam. It clarifies the role of benchmarks in portfolio appraisal and distinguishes absolute, relative, peer group, and custom or strategy-specific benchmarks. It describes the MIRRAT benchmark selection criteria and applies them to typical exam-style scenarios involving mandate and index choice. It details how to compute and interpret single-period total return, multi-period and annualized returns, and relative (active) return versus a stated benchmark. It discusses the use of information ratio, tracking error, and other risk-adjusted performance measures in assessing manager skill versus luck. It examines common benchmarking pitfalls, including non-investable or mismatched benchmarks, survivorship bias in peer groups, and post-hoc benchmark design, and explains why these practices lead to misleading conclusions. It prepares you to analyze CFA-style questions that require selecting an appropriate benchmark, diagnosing benchmark problems, performing basic return calculations, and interpreting numerical performance results in the context of a clearly specified investment objective.

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are expected to understand the construction, selection, and limitations of performance benchmarks and return measures, with a focus on the following syllabus points:

- Identify and describe different types of performance benchmarks (absolute and relative)

- Evaluate the appropriateness of benchmarks for a strategy or manager

- Calculate total, annual, and relative returns for a portfolio or investment

- Explain the importance of benchmark characteristics: relevance, investability, and transparency

- Describe common problems with performance benchmarking

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What are the key features of an effective benchmark for portfolio evaluation?

- True or false? "A market index is always an appropriate performance benchmark for any equity fund."

- Explain the difference between absolute and relative return benchmarks.

- If a portfolio earns 12% in a year and the chosen market index returns 10%, what is the portfolio's relative performance?

Introduction

Benchmarking and return measurement are fundamental for evaluating investment strategies and portfolio managers. Reliable benchmarks offer a reference for comparing investment outcomes, while clear return measures provide the basis for consistent performance calculation and attribution. Proper benchmarks and return analytics are core requirements for CFA candidates and critical for investment decision-making and client reporting.

Test Tip: When revising Benchmarks and return measures, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Types of Benchmarks

A benchmark is a standard or point of reference against which investment performance is compared. Benchmarks can be broadly grouped as absolute or relative.

Key Term: Benchmark

A quantitative or qualitative reference point used to measure portfolio performance, return, or risk. Key Term: Absolute Benchmark

A fixed or predetermined return value, such as a 5% annual target, against which performance is judged. Key Term: Relative Benchmark

An index or peer group return representing actual or theoretical results of a well-defined strategy or universe.

Absolute Benchmarks

Absolute benchmarks are based on non-comparative references such as a required yield, inflation plus a spread, or a fixed percentage. For example, a mandate requiring "return over 6% per annum" is based on an absolute benchmark. Common examples include treasury bill returns, inflation rates, or contractual return thresholds.

Absolute benchmarks are easy to understand but often lack investability and may not reflect the opportunity set or market risk.

Relative Benchmarks

Most performance evaluation is relative: a portfolio's return is compared to a relevant, investable standard, usually a market index or a peer group.

Key Term: Market Index Benchmark

An investable portfolio representing a broad market segment or asset class, widely regarded as a proxy for systematic market exposure.

Relative benchmarks are widely used for equities, fixed income, and other asset classes. For example, large-cap US equity managers might be compared to the S&P 500 Total Return Index.

Peer Group Benchmarks

Peer group benchmarks evaluate performance against the results of similar investment strategies or products.

Key Term: Peer Group Benchmark

The composite return of a group of portfolios or funds sharing similar investment objectives and constraints.

Peer group benchmarks are sensitive to group selection and may be prone to survivorship bias.

Custom or Strategy-Specific Benchmarks

Some strategies, such as factor or quantitative approaches, require a custom combination of asset classes, indexes, factor portfolios, or even a notional “normal” portfolio reflecting the manager's risk and opportunity set.

Benchmark Selection Criteria

For a benchmark to be fit for purpose, it should meet the following six criteria (often summarized by the CFA Institute acronym "MIRRAT"):

- Measurable: Its return and risk statistics must be calculable regularly and objectively.

- Investable: It must be possible, at reasonable cost, to actually hold the benchmark.

- Relevant: It aligns with the strategy’s risk, style, and constraints.

- Representative: The constituents match the manager's universe or mandate.

- Appropriate: It reflects the opportunity set and constraints of the portfolio.

- Transparent: Its construction rules are clear, rules-based, and available.

Failure to satisfy these can lead to misleading assessments or misaligned incentives.

Worked Example 1.1

Question: A UK pension fund invests only in domestic investment-grade bonds. Should a global bond index or a UK government bond index serve as the benchmark?

Answer:

The UK government bond index is more appropriate: it is relevant, investable for the client, and reflects the manager’s constraints. A global bond index, while broad, is not investable by the fund due to issuer, currency, and risk restrictions.

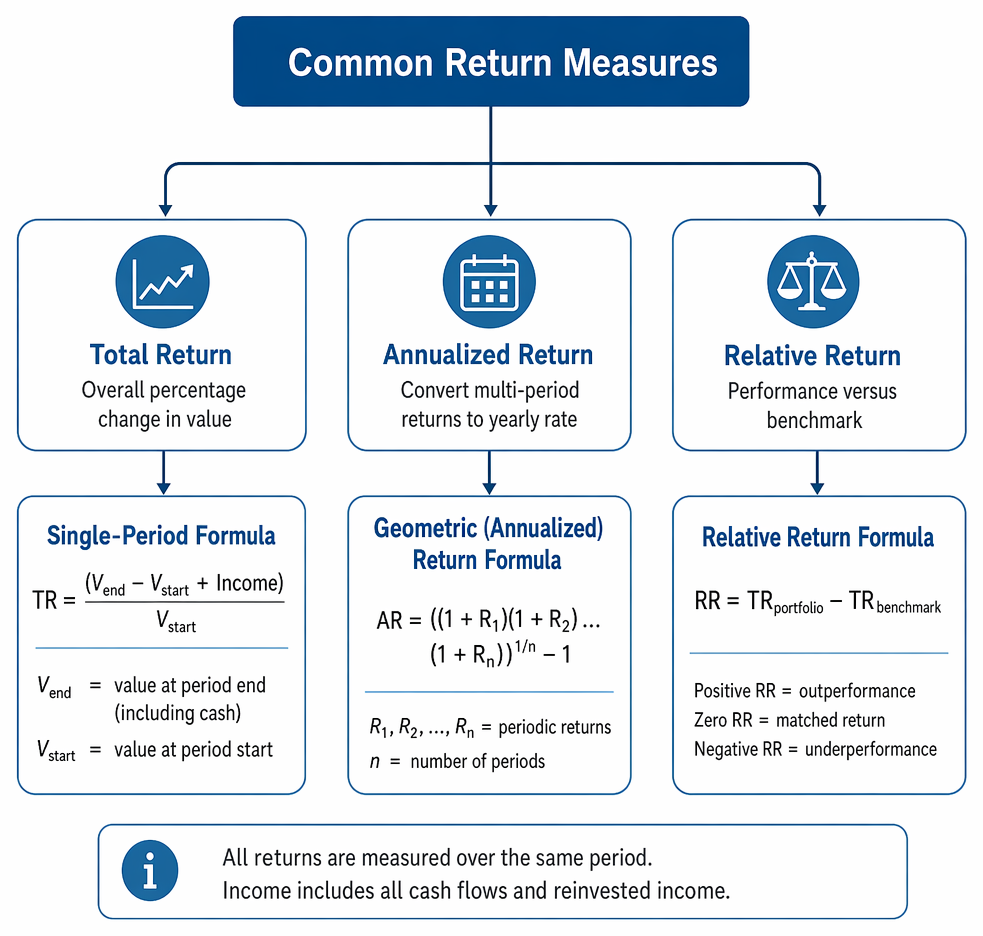

Common Return Measures

Comparing performance requires clear return formulas:

MIRRAT organizes benchmark evaluation into data, strategy-fit, and construction criteria used to assess portfolio performance benchmarks.

Key Term: Total Return

The overall percentage change in portfolio value, including all cash flows and reinvested income, over a stated period.

Single-Period Total Return

- = value at period end (including remaining cash)

- = value at period start

Annualized Return

For multi-period returns:

- If returns are expressed as arithmetical averages but periods are not all one year, convert to annualized (geometric) return:

Key Term: Relative Return

The difference between the portfolio's total return and its benchmark's return over the same period.

Performance Attribution and Appraisal

Attributing performance involves splitting excess return into sources such as asset allocation, security selection, and interaction effects. Manager appraisal relies on measuring skill versus luck, using metrics like Information Ratio, Sharpe Ratio, and comparison to the benchmark.

Key Term: Information Ratio

The ratio of portfolio active return to active risk (tracking error), used to assess consistency of outperformance relative to a benchmark. Key Term: Tracking Error

The standard deviation of the difference between a portfolio’s return and its benchmark’s return.

Worked Example 1.2

A portfolio earns 9% and its benchmark earns 7%. The portfolio's tracking error is 2.5%. What is its information ratio?

Answer:

Information Ratio = (9% - 7%) / 2.5% = 0.8. This indicates strong consistency in excess return per unit of risk versus the benchmark.

Problems in Benchmarking and Return Measurement

Incorrect benchmarks can give a false sense of performance and distort incentives. Watch for:

- Mismatched Benchmarks: An index that does not reflect the actual opportunity set.

- Non-Investable Benchmarks: Return targets or peer averages not available in practice.

- Survivorship Bias: Peer groups omit underperforming funds that have closed.

- Benchmark Overfitting: Custom indexes designed post-hoc to look similar to recent results.

Exam Warning: Benchmarks must be set before the performance period begins. Do not select or modify a benchmark after results are known—this practice results in biased assessments and is not accepted for CFA exam answers.

Summary

Selecting relevant, investable benchmarks and applying consistent return measures are foundational for manager appraisal, product due diligence, and investment monitoring. Benchmarks should closely match the strategy's mandate, constraints, and risk profile. Total, annualized, and relative return calculations are exam staples and must be mastered.

Key Point Checklist

This article has covered the following key knowledge points:

- Differentiate between absolute, relative, peer, and custom benchmarks

- Benchmark selection criteria: Measurability, investability, relevancy, transparency

- Correctly compute single-period and annualized total returns

- Calculate and interpret relative return, information ratio, and tracking error

- Recognize common errors and risks with benchmark use and performance appraisal

- Avoid post-hoc benchmark selection for exams—choose the benchmark first

Key Terms and Concepts

- Benchmark

- Absolute Benchmark

- Relative Benchmark

- Market Index Benchmark

- Peer Group Benchmark

- Total Return

- Relative Return

- Information Ratio

- Tracking Error