Learning Outcomes

This article explains how private assets are valued and how their performance is assessed in an exam context. It enables candidates to identify and describe the three principal valuation approaches—income, market, and cost—and to distinguish between the common methods used within each approach, such as discounted cash flow, capitalization, comparable multiples, and replacement-cost techniques. The article explains when each approach is most appropriate, the data it requires, and the typical sources of model risk and estimation error. It also explains how illiquidity, asset heterogeneity, and infrequent transactions complicate fair value estimation for private real estate, infrastructure, and private equity holdings. In addition, the article explains the main challenges in measuring and comparing private asset performance, including appraisal-based return smoothing, reporting lags, and the practical differences between internal rate of return (IRR) and time-weighted return (TWR). Finally, it links these concepts to typical CFA Level 1 question formats so candidates can recognize how exam items test valuation choices, fair value judgments, and performance evaluation for private assets.

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are expected to understand the primary valuation approaches for private assets and the complexities of measuring performance in these markets, with a focus on the following syllabus points:

- The three main approaches to private asset valuation: income, market, and cost methods

- Typical techniques within each valuation approach

- Issues and limitations in fair value estimation for illiquid and unique private assets

- Difficulties and considerations in measuring and comparing performance for private assets versus public assets

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which valuation approach is most commonly used for stabilized income-generating private real estate and why?

- Describe a primary challenge in applying market-based valuation methods to unique private equity investments.

- In private markets, why can performance measurement periods distort true skill or value creation?

- What is an example of a situation where the cost approach may be preferred for a private asset?

Introduction

Private assets—such as private real estate, infrastructure, and private equity—are infrequently traded and often heterogeneous. Their valuation differs from listed assets due to transaction illiquidity, non-uniformity, and limited observable price data. Several valuation approaches are used, each with particular strengths, weaknesses, and conditions for application. Understanding how these approaches work, and the issues that arise in measuring private asset returns, is essential for CFA candidates.

Test Tip: When revising Private asset valuation approaches, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

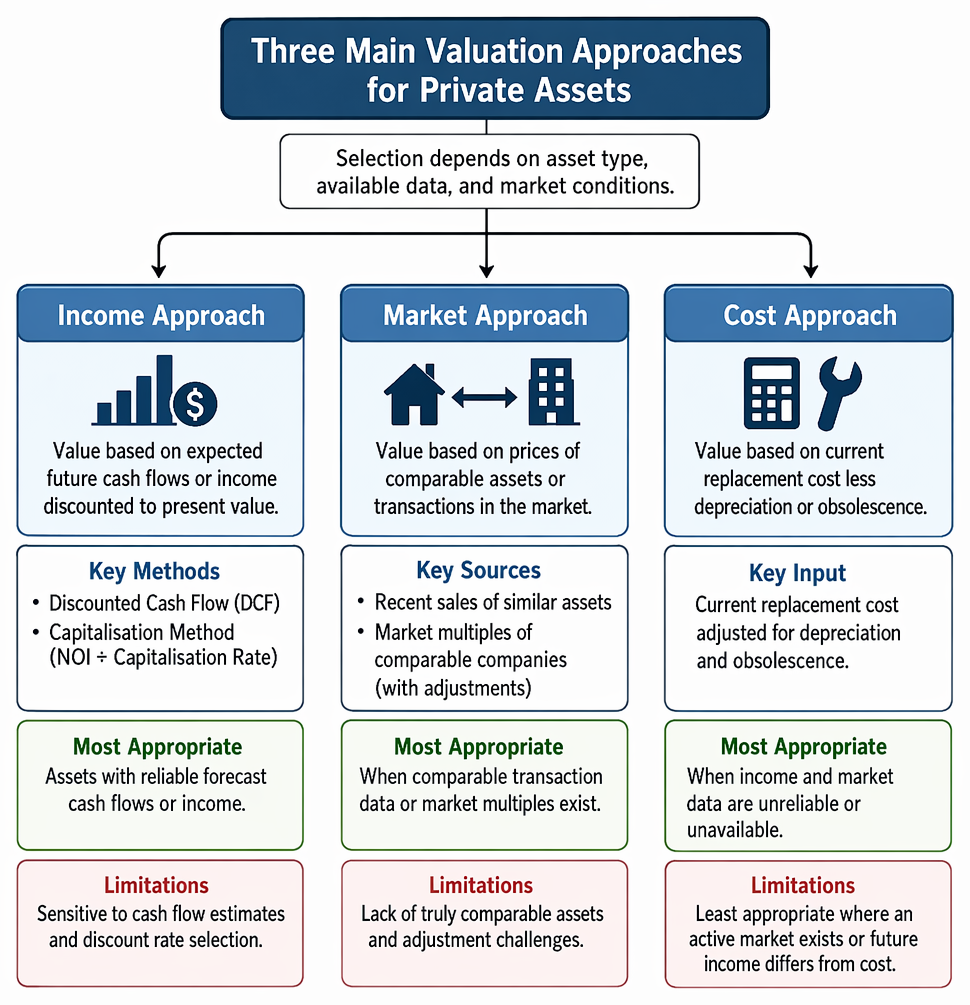

THE MAIN PRIVATE ASSET VALUATION APPROACHES

There are three principal approaches for valuing private assets: the income approach, the market approach, and the cost approach. The selection of approach depends on asset type, available data, and market conditions.

Private asset valuation methods are matched to income, market, or cost approaches according to data availability and comparability conditions.

Key Term: private asset

An asset—such as real estate, infrastructure, or private company equity—not regularly traded on public markets, typically illiquid and unique. Key Term: income approach

A valuation method that estimates value by discounting expected future cash flows or income to present value using a chosen discount rate. Key Term: market approach

A valuation method that estimates value based on observed prices of comparable assets or transactions in the market. Key Term: cost approach

A method that estimates value by determining the current cost to replace the asset, less appropriate adjustments for depreciation or obsolescence.

The Income Approach

Valuation under the income approach calculates the present value of forecast future cash flows from the asset. This is typically implemented using the discounted cash flow (DCF) method, which discounts the cash flows at a rate reflecting risk and time value of money.

For example, stabilized real estate is often valued using a capitalisation method, dividing net operating income (NOI) by a capitalisation (cap) rate. For assets with fixed future cash flows—such as infrastructure or some debt—the DCF is particularly suitable. The biggest challenge is selecting appropriate cash flow estimates and discount rates.

The Market Approach

The market approach estimates asset value by reference to transactions in similar or comparable assets. In private markets, this may include prices of recent sales for similar properties or businesses, or market multiples for comparable public companies, with relevant adjustments.

Practical limitations include a lack of truly comparable assets—especially for unique properties or companies—and difficulties in adjusting for idiosyncratic features, illiquidity, or differences in control.

The Cost Approach

The cost approach uses the current replacement cost of the asset, adjusted for depreciation and obsolescence, to estimate value. This approach is more commonly applied when income and market data are unreliable or unavailable. Unique, specialized, or recently constructed assets are often valued using this method.

It is least appropriate where an active market exists or where future income expectations differ significantly from the cost to replace the asset.

Worked Example 1.1

Question: A warehouse is leased at below-market rent to a long-term tenant and is of a standard, easily replaced design. Which valuation approach is most suitable?

Answer:

In this scenario, both income and cost approaches may be relevant. The income approach would produce a low value due to the below-market rent, while the cost approach would estimate value based on the replacement cost less depreciation. If market rents (and thus asset value) are expected to rise after the lease expires, the income approach using stabilized cash flows may be more appropriate long term. For current valuation, both methods may be presented to highlight conservative and optimistic views.

FAIR VALUE CONSIDERATIONS IN PRIVATE ASSET VALUATION

Estimating the fair value of private assets is more complex than for liquid, exchange-traded securities. Key challenges include:

- Illiquidity and limited observable transactions

- Asset heterogeneity or uniqueness

- Stale or infrequent appraisals

- Reporting lags

Valuation models for private assets rely more on judgment than on automated market pricing, increasing subjectivity and the potential for estimation error.

Key Term: fair value

The price that would be received to sell an asset in an orderly transaction between market participants at the measurement date.

Worked Example 1.2

Why is applying a recent transaction price to value a private equity holding potentially misleading?

Answer:

Private equity transactions can be highly negotiated, reflect control premiums or discounts, and often occur under specific conditions that are not representative of ongoing market value. Additionally, if market conditions change rapidly, a stale transaction price may not reflect fair value at the current valuation date.

PERFORMANCE MEASUREMENT CHALLENGES IN PRIVATE ASSETS

Assessing investment performance in private assets presents unique obstacles:

- Valuations are typically updated less frequently than listed securities (e.g., quarterly appraisals)

- Smoothing of reported returns due to infrequent revaluation

- Backward-looking performance measures may understate volatility and overstate Sharpe ratios

- Timing of cash flows and use of internal rate of return (IRR) as a performance metric instead of time-weighted return (TWR)

- Difficulties in benchmarking due to lack of suitable public market comparables

Key Term: internal rate of return (IRR)

The discount rate that sets the present value of all cash flows (inflows and outflows) from an investment to zero; used as a performance metric in private asset investments. Key Term: time-weighted return (TWR)

A method of performance measurement that eliminates the impact of cash flow timing, allowing comparison with listed benchmarks.

Worked Example 1.3

Question: An infrastructure fund reports an IRR of 15%, but the fund’s largest asset was recently reappraised much higher. Why should an analyst be cautious about using this IRR to judge fund manager skill?

Answer:

The IRR reflects interim valuations based on appraisals, not realized market prices. If the reappraisal is aggressive, the IRR may be artificially inflated. Additionally, IRR can be sensitive to the timing of cash flows and appraisals, making it a less reliable comparator across funds or to public benchmarks. Time-weighted returns should be examined if available.Exam Warning: A common error is to compare IRRs of private equity or real asset investments directly with time-weighted returns (such as public equity indices). IRR is affected by the size and timing of cash flows and may not reflect true manager skill or asset performance in the way required for like-for-like comparison.

Summary

Valuing private assets relies mainly on the income, market, or cost approach, chosen according to asset type and data availability. All methods have strengths and limitations in the context of illiquidity, uniqueness, and low transaction frequency. Fair value estimation is more judgmental than for public assets. Performance measurement for private assets is complicated by appraisal frequency, value smoothing, and the distinct properties of IRR compared with public market time-weighted returns.

Key Point Checklist

This article has covered the following key knowledge points:

- The principal private asset valuation approaches: income, market, and cost methods

- Typical application scenarios and main challenges for each approach

- Limitations in fair value estimation for private, illiquid, or unique assets

- Important performance measurement difficulties in private assets, such as IRR vs TWR and appraisal smoothing

- Benchmarking considerations and analytical risks in comparing private and public asset returns

Key Terms and Concepts

- private asset

- income approach

- market approach

- cost approach

- fair value

- internal rate of return (IRR)

- time-weighted return (TWR)