Learning Outcomes

This article explains valuation and term structure concepts for credit spreads and option-adjusted spreads (OAS) in CFA Level 1 fixed income, including:

- Defining credit spreads and identifying their main components (default and liquidity premia) and key drivers.

- Describing the term structure of credit spreads, typical curve shapes, and what steepening or flattening indicates about near‑ versus long‑term credit risk.

- Distinguishing nominal spreads, Z‑spreads, and OAS, and explaining how embedded options and option cost affect these measures.

- Applying OAS as the preferred spread measure for bonds with embedded options and computing simple OAS–option cost relationships for callable and putable bonds.

- Comparing bonds with and without embedded options on a like‑for‑like basis and using spreads, OAS, and spread duration to assess creditworthiness, price sensitivity, and relative value.

- Identifying macroeconomic, market, and issuer‑specific factors that cause spreads to widen or tighten and linking these moves to the credit cycle.

- Relating spreads to credit ratings, seniority, security, expected recovery, and key financial ratios such as leverage, coverage, and profitability.

- Interpreting benchmark‑based measures (G‑spreads and I‑spreads) and linking them conceptually to credit spreads, Z‑spreads, and OAS for exam-style fixed‑income problems.

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are required to understand credit spreads and OAS as key components of fixed income valuation, with a focus on the following syllabus points:

- Explain what a credit spread is, what it measures, and why it changes.

- Relate the term structure of credit spreads to bond maturity, default risk, and liquidity.

- Define and interpret option-adjusted spread (OAS) and explain its relevance for bonds with embedded options.

- Distinguish between nominal spread, Z-spread, and OAS, and explain conceptually how option cost affects these measures.

- Calculate and interpret the relationship between nominal spread, OAS, and option cost for simple callable and putable bonds.

- Assess how changes in credit spreads affect bond yields, prices, and relative value across different fixed income securities.

- Describe how macroeconomic, market, and issuer‑specific factors affect credit spreads, especially across different stages of the credit cycle.

- Compare spread measures across rating categories and explain why credit ratings and spreads can send different signals about credit risk.

- Explain basic spread measures over benchmark curves, including government spreads (G‑spreads and I‑spreads) and how they relate to credit spreads and OAS.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

A 5‑year corporate bond’s yield increases from 4.5% to 5.1% while the 5‑year government yield stays at 2.0%. What does this most likely indicate?

- a) Lower default risk and improved liquidity

- b) Higher credit and/or liquidity risk for the issuer

- c) A parallel upward shift in the risk-free yield curve

- d) Lower required compensation for bearing credit risk

-

For a callable corporate bond and a similar non-callable corporate bond with the same maturity and issuer, which statement about nominal spread and OAS is most accurate?

- a) Nominal spreads and OAS will always be identical

- b) The callable bond’s nominal spread is smaller because of call risk

- c) The callable bond’s nominal spread is larger, but its OAS may be similar

- d) The callable bond’s OAS includes only the value of the call option

-

Two 7‑year bonds have the same credit rating and issuer, but Bond X trades with a wider credit spread than Bond Y. Which explanation is most consistent with this information?

- a) Bond X is likely more liquid than Bond Y

- b) Bond X likely has worse recovery prospects than Bond Y

- c) Bond Y must have an embedded call option

- d) Bond X is likely less liquid or has less favorable issue features

-

The term structure of credit spreads for an investment‑grade industrial issuer shifts from 60 bps (2‑year) and 110 bps (10‑year) to 95 bps (2‑year) and 125 bps (10‑year). Which description is most accurate?

- a) Curve has flattened; near‑term credit risk has increased more than long‑term risk

- b) Curve has steepened; investors demand much more compensation for long‑term risk

- c) Curve is unchanged; spreads have moved in parallel

- d) Curve has inverted; investors expect default only in the distant future

-

A 10‑year callable bond has a nominal spread of 220 bps. The estimated value of the embedded call is 70 bps in spread terms. Assuming no other options, which of the following is closest to the bond’s OAS, and how does it compare to an otherwise similar non‑callable bond with a 180 bp nominal spread?

- a) OAS 290 bps; callable bond offers more pure credit compensation

- b) OAS 150 bps; callable bond offers less pure credit compensation

- c) OAS 150 bps; callable bond offers similar pure credit compensation

- d) OAS 220 bps; callable and non‑callable bonds cannot be compared

Introduction

Credit spreads and option-adjusted spreads (OAS) are central to fixed income valuation and term structure analysis. Spreads quantify the extra yield investors demand, over a default risk–free benchmark, for bearing credit and liquidity risk and, when relevant, the risk from embedded options. Understanding what these spreads measure, how they behave across maturities, and how to adjust them for options is essential when valuing corporate bonds, securitized products, and other risky fixed income instruments.

Key Term: credit spread

The yield difference between a non-government (risky) bond and a comparable-maturity benchmark risk-free bond, typically used to quantify compensation for default risk, liquidity risk, and other non–interest-rate risks. Key Term: yield spread

The yield difference between two bonds or bond indices. A credit spread is a specific type of yield spread: risky bond yield minus risk-free (or near risk-free) benchmark yield of similar maturity.

In many markets, the benchmark is a government bond curve, but in others (for example, markets where government issuance is limited or not considered default‑risk free) swap rates are used as the reference.

Key Term: G-spread (government spread)

The yield spread of a bond over a government bond of similar maturity: bond yield minus same‑maturity government yield. If there is no government bond with exactly the same maturity, the government yield is often linearly interpolated between two surrounding maturities. Key Term: I-spread (interpolated spread)

The yield spread of a bond over the swap curve, calculated as bond yield minus the swap rate of the same maturity (often obtained by interpolating between two swap maturities). It is widely used when the swap curve is viewed as the main benchmark. Key Term: term structure of credit spreads

The pattern of credit spreads across different maturities for the same issuer or rating category, reflecting how credit and liquidity risk (and investor risk premiums) change with the time horizon. Key Term: option-adjusted spread (OAS)

The constant spread over the benchmark yield curve that, when added to each benchmark rate in an interest rate tree and applied to the bond’s option-adjusted cash flows, makes the model price equal to the market price. It is interpreted as the spread that compensates only for credit and liquidity risk, after removing the value of embedded options. Key Term: benchmark yield curve

The term structure of yields on high-quality, default risk–free (or nearly risk-free) securities, such as government bonds or interest rate swaps, used as a basis for measuring spreads.

At the simplest level, a fixed‑rate bond’s yield to maturity can be decomposed into two main components:

- The yield on the appropriate point of the benchmark yield curve (reflecting time value of money and interest rate expectations).

- A credit spread (reflecting compensation for default risk, expected loss, liquidity, and other credit-related risks).

Symbolically, for a corporate bond:

For bonds with embedded options, a third component—the option cost—affects the observed yield. In that case you can think of:

with the sign depending on whether the investor is effectively short (callable) or long (putable) the option. Option-adjusted spread techniques allow the analyst to isolate the compensation for credit and liquidity from the effect of the option so that bonds with and without options can be compared on a like‑for‑like basis.

From a valuation standpoint, the spread can also be viewed in present value terms. Conceptually, an analyst could:

- Discount each promised cash flow at the appropriate risk‑free spot rate plus a constant spread (the Z‑spread or OAS, depending on whether there is an option).

- Adjust the spread until the discounted cash flows equal the bond’s market price.

The resulting spread is a compact way to summarize all non–interest‑rate risks in a single number.

In the CFA curriculum, spreads are studied alongside the term structure of interest rates. The benchmark yield curve itself reflects:

- Expected future short‑term risk‑free rates.

- A term premium for locking in a long‑term risk‑free rate.

- Expected inflation (in nominal curves).

Credit spreads sit on top of this curve and change with both issuer‑specific credit factors and broader macroeconomic conditions. Separating “pure interest rate moves” (changes in the benchmark curve) from “spread moves” (changes in credit and liquidity compensation) is a core exam skill.

Key Term: investment-grade bond

A bond rated BBB−/Baa3 or higher by major rating agencies. These bonds are considered to have relatively low credit risk and generally trade at tighter (smaller) spreads. Key Term: high-yield (speculative-grade) bond

A bond rated below investment grade (BB+/Ba1 or lower). These bonds carry higher credit risk and typically trade at wider (larger) credit spreads that are more sensitive to the economic cycle.

Investment-grade and high-yield spreads behave differently over the credit cycle.

Key Term: credit cycle

The recurring pattern over time in credit availability, default rates, rating migrations, and credit spreads, typically linked to the broader business cycle (expansion, slowdown, recession, recovery).

- In expansions, when default rates are low and funding is easily available, spreads tend to be tight.

- In recessions or periods of stress, default risk and risk aversion increase, causing spreads—especially high‑yield spreads—to widen sharply.

Historical risk–return evidence shows that higher-risk assets (such as high-yield bonds and equities) have earned higher average returns over long periods but with greater volatility. The credit spread is one observable market measure of the extra compensation (risk premium) investors require for bearing that additional risk.

Test Tip: When revising Credit spreads and OAS basics, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Exam Warning: Do not rely on keyword recognition alone; check the precise condition, exception, calculation step, or evidence the question requires.

Credit Spreads: Definition and Key Drivers

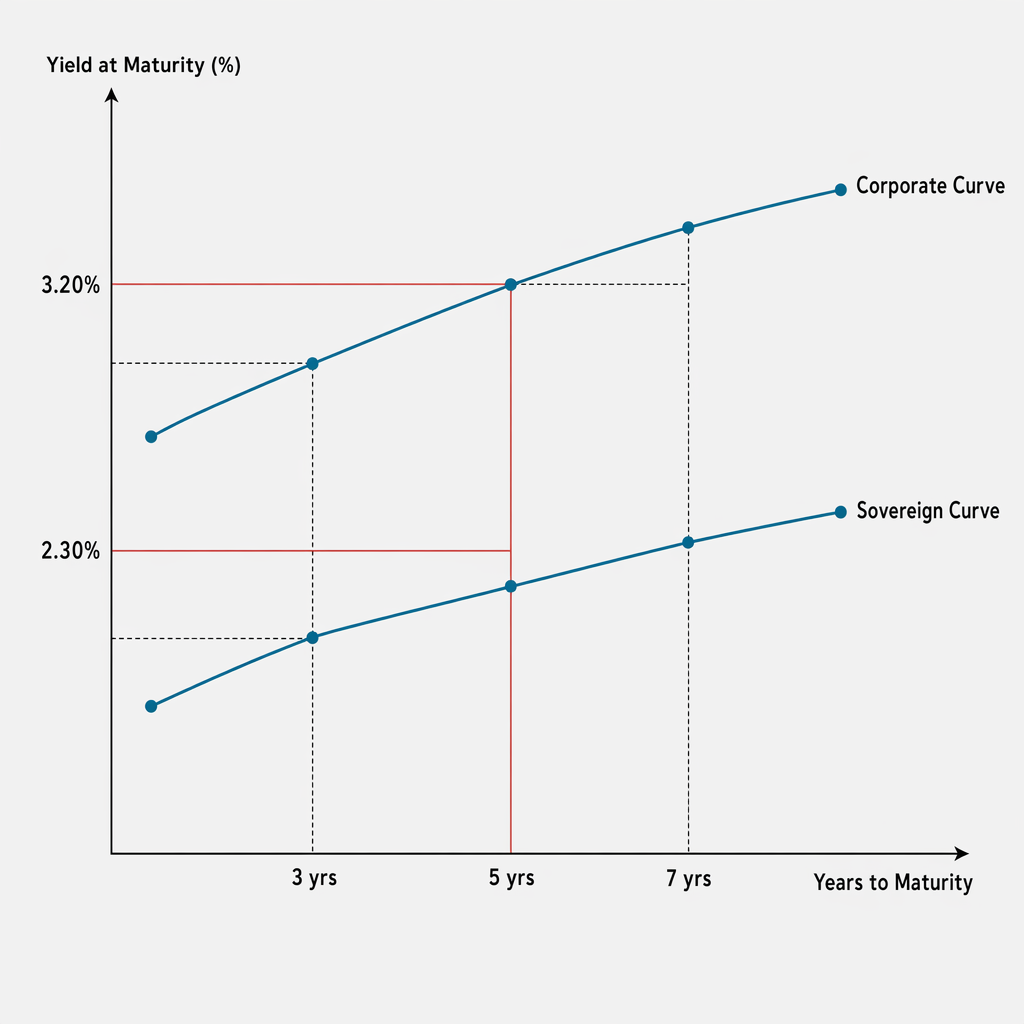

A credit spread reflects the additional yield, usually expressed in basis points (1 bp = 0.01%), that investors require for holding a bond with credit risk or reduced liquidity compared with a default risk–free government bond of similar maturity.

Single-panel yield curve chart compares a higher corporate curve with a lower sovereign curve across maturities, with guides emphasizing spreads at 3, 5, and 7 years. It illustrates the credit spread concept that underlies valuation and the option-adjusted spread (OAS) discussion in the article.

At Level 1, it is helpful to think of the credit spread as consisting of:

- A default risk premium (for the chance of non-payment and expected loss if default occurs).

- A liquidity premium (for the difficulty of trading the bond quickly at fair value).

- Other minor components, such as compensation for tax differences, complexity, or structural features (for example, subordination or weak covenants).

Key Term: default risk premium

The component of the credit spread that compensates investors for the probability of issuer default and the expected loss given default. Key Term: liquidity premium

The component of the credit spread that compensates investors for the risk of not being able to trade the bond quickly at a reasonable price, especially in stressed markets.

From a risk-management standpoint, thinking explicitly about expected loss is useful.

Key Term: probability of default (PD)

The likelihood, over a specified time horizon, that an issuer will fail to meet its debt obligations as promised. Key Term: loss given default (LGD)

The proportion of exposure that is lost if default occurs, equal to 1 minus the recovery rate. Key Term: recovery rate

The proportion of par value (or exposure) that investors are expected to recover in the event of default, usually expressed as a percentage of par.

Although Level 1 does not require formulas, conceptually:

Investors then require a spread that covers:

- This expected loss, plus

- An additional risk premium for uncertainty in PD and LGD, correlation with the business cycle, and tail risks.

The quoted credit spread incorporates both components.

In practice, the market does not separately quote each component; you observe only the overall spread. However, keeping these building blocks in mind helps explain why spreads differ across issuers and change over time.

Credit spreads are typically quoted relative to a standard benchmark:

- For domestic corporate bonds, the reference is often the government bond curve (G‑spread).

- For some corporate, supranational, or covered bonds, the swap curve may be the reference (I‑spread).

- For securitized products and indices, analysts frequently quote OAS relative to a fitted government or swap curve.

Main drivers of credit spreads

Key factors that influence credit spreads include the following.

Default (credit) risk

- Lower-rated or financially weaker issuers have a higher probability of missed payments or restructuring.

- As credit quality deteriorates, spreads widen to provide higher compensation.

- Spreads by rating category reflect this: historically, AAA or AA bonds trade with tight spreads, while BB or B (high yield) bonds trade with much wider spreads.

- Within a rating category, spreads also vary with issue‑specific factors such as seniority, security, and expected recovery.

Key Term: credit rating

A letter-grade assessment of an issuer’s or issue’s relative credit risk, assigned by a credit rating agency, based mainly on default probability and expected loss severity. Key Term: seniority

The ranking of a debt claim in the capital structure, determining the order in which creditors are paid in bankruptcy or liquidation. Key Term: secured debt

Debt backed by specific collateral (for example, property or receivables). Secured creditors have a claim on the pledged assets. Key Term: subordinated debt

Debt that ranks below senior obligations in the capital structure. Subordinated creditors are paid only after more senior creditors are fully satisfied.

More senior and/or secured issues typically have higher expected recovery and therefore trade at tighter spreads than subordinated and unsecured issues from the same issuer.

Credit ratings are useful summary indicators, but they are not sufficient on their own. Ratings tend to be “sticky” and are updated much less frequently than market prices. Bond prices and spreads often move significantly before a rating upgrade or downgrade is announced.

Key Term: downgrade risk

The risk that a rating agency will lower the credit rating of an issuer or issue, typically resulting in wider spreads and lower bond prices. Key Term: upgrade risk

The (usually favorable) risk that a rating agency will raise the credit rating, often leading to tighter spreads and higher bond prices.

Within speculative‑grade bonds, two subcategories are often mentioned:

Key Term: fallen angel

A bond that was originally issued with an investment‑grade rating but has subsequently been downgraded to high-yield status. Key Term: crossover bond

A bond rated near the boundary between investment grade and high yield (for example, BBB−/BB+), which may be attractive to both investment‑grade and high‑yield investors.

Fallen angels and crossover bonds often experience large spread changes around rating migration events because of changes in the eligible investor base or forced selling from investment‑grade mandates.

The 2024 curriculum also highlights that spreads can move substantially while the rating is unchanged. For example:

- A bond may still be rated investment grade, but if its spread widens to levels typical of high-yield bonds, the market is already pricing in substantial credit deterioration.

- Historical cases such as Wirecard AG, Enron, or WorldCom demonstrate that spreads can signal rising risk well before formal rating downgrades.

This is why Level 1 emphasises: use ratings as one input, but rely on spreads and fundamental analysis to get a timely view of credit risk.

Liquidity conditions

- Bonds that trade infrequently, in small sizes, or in less developed markets tend to have wider spreads.

- New, large benchmark issues (“on‑the‑run” issues) often trade at tighter spreads than small, older “off‑the‑run" issues of the same issuer.

- During periods of market stress, liquidity can dry up and liquidity premiums can rise sharply even for fundamentally sound issuers.

Two behaviours often observed in stressed markets are:

Key Term: flight-to-quality

A shift by investors from riskier assets (such as high-yield bonds or equities) into safer assets (such as government bonds), resulting in wider credit spreads and lower government yields. Key Term: flight-to-liquidity

A shift by investors into the most liquid securities (often recently issued government bonds), which can widen spreads on less liquid bonds even if credit fundamentals are unchanged.

In both cases, spreads may widen even without large changes in expected default losses, simply because investors increasingly value safety and liquidity.

At Level 1, it is important to recognise that:

- Liquidity-driven spread moves can reverse quickly once risk appetite returns.

- Fundamental deterioration (weakening leverage or coverage ratios) usually results in more persistent spread widening.

Maturity and term structure

- For many investment-grade issuers, spreads increase with maturity, reflecting greater uncertainty about long-term creditworthiness and a longer exposure to business cycles.

- For distressed or very low-rated issuers, near-term default risk may be high, leading to relatively large short-maturity spreads and even inverted spread curves (higher spreads at short maturities than at long maturities).

- The pattern of spreads across maturities (the credit spread curve) is discussed in detail later.

Macroeconomic environment

Spreads are strongly influenced by macro conditions and policy. The curriculum’s credit risk readings summarise key macro drivers as:

- Economic growth (GDP, industrial production, employment).

- Inflation and inflation uncertainty.

- Monetary policy stance and interest rate levels.

- Fiscal policy and overall debt burdens.

- Global economic conditions and trade.

In broad terms:

- In economic expansions with strong growth and low default rates, credit spreads generally narrow as investors are more willing to bear credit risk.

- In recessions or periods of financial stress, spreads widen sharply as default expectations and risk aversion increase.

- High-yield (speculative‑grade) spreads tend to be more cyclical than investment‑grade spreads, as weaker issuers are more sensitive to downturns in earnings and cash flow.

Monetary and fiscal policies matter as well:

-

Expansionary monetary policy (for example, lowering policy rates or implementing asset purchases) tends to:

- Reduce funding costs and ease refinancing pressure.

- Improve banking system liquidity.

- Support asset prices and credit availability.

- Contribute to spread tightening.

-

Restrictive monetary policy (rising real interest rates, reduced central bank balance sheets) often:

- Increases financing costs.

- Tightens credit conditions.

- Leads to spread widening, especially for weaker issuers and long-maturity bonds.

-

Fiscal stimulus (higher government spending or lower taxes) can:

- Support growth and reduce default risk, especially in the short to medium term.

-

Fiscal tightening in an already weak economy can:

- Depress activity further and increase credit risk.

You are not expected to forecast specific macro data in the exam, but you should be able to interpret scenarios such as “recession with tight credit conditions” versus “early recovery with accommodative monetary policy” and explain likely spread behaviour.

Market (technical) factors

Market factors (often called “technical” factors) can cause spreads to move independently of fundamentals:

- Imbalances between supply and demand for corporate bonds versus government bonds.

- Heavy new issuance in a particular sector or maturity bucket.

- Index rebalancing, benchmark changes, or rating changes that trigger forced buying or selling.

- Fund flows into or out of credit funds, ETFs, or high-yield mandates.

These “technical” factors can cause short-term spread moves not fully justified by fundamentals, creating potential relative‑value opportunities.

Issuer-specific factors

Issuer-specific drivers reflect bottom‑up credit analysis:

- Changes in leverage (debt relative to cash flow or capital), profitability, cash flow stability, and asset quality.

- Event risk, such as acquisitions financed with new debt, large share buybacks, or regulatory changes affecting the issuer’s business model.

- Corporate governance, management quality, and financial policy (for example, willingness to maintain conservative leverage) also matter.

Important fundamental metrics include:

- Profitability and cash flow metrics: EBITDA, EBIT, free cash flow (FCF).

- Leverage metrics: debt/capital, debt/EBITDA, funds‑from‑operations (FFO)/debt.

- Coverage metrics: EBITDA/interest expense, EBIT/interest expense.

Improving profitability, lower leverage, stronger coverage, and better liquidity are typically associated with tighter spreads, whereas deteriorating metrics coincide with wider spreads.

The 2024 readings on corporate credit analysis group these into:

- Profitability and cash flow metrics (for example, EBITDA, FCF).

- Leverage metrics (for example, debt/EBITDA, FFO/debt, debt/capital).

- Coverage metrics (for example, EBITDA/interest, EBIT/interest).

Higher leverage and weaker coverage imply a lower capacity to absorb earnings shocks and therefore higher spreads.

Key Term: credit spread risk

The risk that a bond’s credit spread will widen (increase), causing its price to fall, even if the benchmark yield curve is unchanged.

Textbooks often distinguish three related credit risks:

- Default risk (the risk of actual non-payment).

- Downgrade risk (the risk that the rating agency will lower the issuer’s rating).

- Credit spread risk (the risk that spreads widen for any reason, including changing risk appetite, even if default expectations do not change).

Credit spread risk directly affects bond prices through spread duration, discussed next.

Spread tightening versus spread widening

Analysts often describe spread moves using two standard terms:

Key Term: spread tightening

A decrease in the credit spread (for example, from 250 bps to 200 bps), which, all else equal, increases the bond’s price. Key Term: spread widening

An increase in the credit spread (for example, from 150 bps to 220 bps), which, all else equal, decreases the bond’s price.

Interpreting spread moves:

- Spread tightening typically reflects improving credit fundamentals, better liquidity, or increased risk appetite.

- Spread widening usually signals deteriorating fundamentals, reduced liquidity, or higher risk aversion.

When interpreting moves, always separate:

- Changes in absolute yields (bond yield to maturity).

- Changes in risk-free benchmark yields.

- Changes in credit spreads (the difference between the two).

On exam questions, you may see situations where:

- The corporate bond’s yield rises because government yields have risen more than spreads have tightened.

- The corporate bond’s yield falls even though government yields rise, because spreads tighten by a larger amount.

You must be able to isolate the spread component and interpret what it implies about credit conditions.

A useful qualitative checklist when spreads tighten is:

- Are macro conditions improving (growth, employment, corporate earnings)?

- Are central banks easing and adding liquidity?

- Are rating upgrades increasing, or are default rates falling?

When spreads widen sharply, especially relative to history, analysts often ask:

- Is this mainly a liquidity shock (flight‑to‑quality or flight‑to‑liquidity)?

- Or are fundamentals deteriorating (earnings disappointments, rising leverage, weakening coverage)?

Measuring the price impact of spread changes

Credit risk is often summarised by a measure called spread duration.

Key Term: spread duration

A measure of the sensitivity of a bond’s price to changes in its credit spread, usually expressed as the approximate percentage price change for a 100 bp (1%) change in the spread, assuming the benchmark yield curve is unchanged.

Spread duration is conceptually similar to interest rate duration, but instead of measuring sensitivity to changes in the overall yield, it measures sensitivity specifically to changes in the spread component. A simple approximation used in practice is:

where is the change in spread expressed in decimal form (for example, 0.005 for 50 bps).

For a given issuer, spread duration tends to be:

- Larger for longer-maturity bonds.

- Larger for bonds with lower coupons (all else equal).

- An important input when managing portfolio exposure to the credit cycle.

If spreads widen, the negative sign in the formula indicates that the bond’s price falls; if spreads tighten, the bond’s price rises.

In practice:

- For many investment-grade bonds, spread duration and interest rate duration are of similar magnitudes.

- For high-yield bonds, interest rate duration is often shorter (their high coupons and yields frontload cash flows), but spread changes tend to be larger and more volatile, making spread duration a dominant risk.

Spread duration can be estimated from price changes when spreads move historically, or approximated from interest rate duration when spreads are moderate. Many portfolio reports show both interest rate duration and spread duration separately so that managers can see how much of total risk comes from rates versus credit.

Worked Example 1.1

A 2‑year BBB-rated corporate bond has a spread of 70 bps over the risk-free yield. The 10‑year BBB-rated bond from the same issuer trades at a spread of 120 bps. What does this shape of the term structure suggest about investor perceptions? How might your interpretation change if the 10‑year spread were instead 80 bps?

Answer:

With 2‑year spreads at 70 bps and 10‑year spreads at 120 bps, the term structure is clearly upward sloping. This suggests: -Investors see relatively low near-term default risk but increasing uncertainty about the issuer’s ability to meet obligations over a 10‑year horizon. -They may also require more compensation for long-term exposure to macroeconomic and industry cycles and for the lower liquidity of long-dated bonds. If the 10‑year spread were 80 bps instead (only slightly above the 2‑year spread), the spread curve would be almost flat. This would suggest: -Investors perceive similar credit risk per year across horizons, or -Factors such as strong demand for longer-dated bonds are compressing long-term spreads, offsetting higher long-run uncertainty.

Worked Example 1.2

A 6‑year corporate bond has a spread duration of 4.8. If its credit spread widens from 150 bps to 210 bps, approximately what percentage price change would you expect, assuming the benchmark yield curve is unchanged?

Answer:

The spread change is 60 bps, or 0.60%.

Using the approximation:

gives:

So the bond’s price is expected to fall by about 2.9% due to the spread widening, even though risk‑free rates have not changed.

Additional detail: spread duration versus interest rate duration

For many corporate bonds, both spread duration and interest rate duration matter:

-

An investment-grade corporate bond might have:

- Interest rate duration ≈ 7.

- Spread duration ≈ 6.

-

A high-yield bond of the same maturity might have:

- Interest rate duration ≈ 3–4 (because its cash flows are more heavily discounted by the larger yield).

- Spread duration ≈ similar magnitude (3–4), but credit spread changes tend to be larger and more volatile.

This means:

- Investment-grade bonds are more sensitive to moves in the risk-free curve.

- High-yield bonds are more sensitive to spread moves; “credit events” and the business cycle dominate returns.

From a portfolio standpoint, combining bonds with different spread durations (across issuers, sectors, and ratings) allows diversification of credit spread risk in the same way that combining assets with imperfectly correlated returns reduces overall portfolio variance.

The Term Structure of Credit Spreads

The term structure of credit spreads describes how spreads vary with maturity for a given issuer, sector, or rating category. For example, you can plot the spreads of a BBB-rated issuer’s 2‑, 5‑, 10‑, and 20‑year bonds over the benchmark curve to obtain a credit spread curve (often called a “credit curve”).

Key Term: credit spread curve (credit curve)

The graph of credit spreads versus maturities for a single issuer, sector, or rating category, constructed by plotting spreads at different maturities over the benchmark yield curve.

When analysing credit curves, it is useful to distinguish:

- The level of the curve (how wide spreads are overall).

- The slope (how spreads change with maturity).

- Any humps or local irregularities (often driven by supply, demand, or specific refinancing events).

You should also remember that the credit curve is separate from the risk-free yield curve. An issuer can have an upward-sloping government curve but a flat or even inverted credit curve, depending on how its spread behaves with maturity.

Typical shapes and interpretations

Common shapes and their interpretations include:

-

Upward sloping (most common for investment grade):

- Short-term spreads are relatively low, and spreads increase with maturity.

- This reflects low near-term default risk but increasing uncertainty over longer horizons.

- It can also reflect lower liquidity and higher risk premiums for long-dated bonds.

- For high‑quality issuers, this is the “normal” shape: investors demand more spread to lend for longer.

-

Flat term structure:

- Similar spread levels across maturities.

- May indicate fairly constant perceived credit risk over time, or offsetting effects (for example, higher long-term uncertainty but better liquidity in the 5–10‑year “benchmark” sector).

- A flattening curve can arise when near‑term risk rises while long‑term risk expectations change little.

-

Downward sloping (inverted):

- Short-term spreads are higher than long-term spreads.

- Often associated with issuers facing near-term distress: investors require a high premium for short maturities where default risk is concentrated but expect that, conditional on survival, risk falls at longer horizons.

- Common in speculative-grade or distressed credits, especially when a large debt maturity or refinancing is due soon.

-

Hump-shaped (bell-shaped):

- Spreads rise from short to intermediate maturities, then fall for very long maturities.

- Can occur when medium-term uncertainty (for example, a large debt “maturity wall” or an expected industry downturn) is greater than either near-term or very long-term uncertainty.

- Sometimes reflects technical factors, such as heavy issuance in the 5–7‑year part of the curve.

In exam questions, you may be given a table of spreads at different maturities and asked to identify the curve shape or to interpret how perceived risk has shifted when the curve steepens or flattens.

Investment-grade versus high-yield credit curves

The term structure of spreads often differs systematically between investment-grade and high-yield issuers:

-

Investment-grade issuers:

- Credit curves are usually gently upward sloping.

- Spread differences between 2‑ and 10‑year maturities might be modest (for example, 30–70 bps).

- Spread levels are influenced by interest rate expectations and macroeconomic conditions, but default risk over the next few years is generally perceived as low.

- In stressed macro conditions, curves may steepen as investors demand more premium for long-term uncertainty.

-

High-yield issuers:

- Credit curves can be steep, flat, or inverted, and shapes can change rapidly.

- Near-term spreads may jump sharply if a particular maturity is seen as difficult to refinance or if insolvency risk rises.

- Longer-dated bonds may trade at lower spreads (conditional on survival) or may not exist if the issuer cannot issue at very long maturities.

- Distressed issuers often show very high short-dated spreads and lower long-dated spreads, reflecting “default or recovery” scenarios in the near term.

Because high-yield cash flows are discounted at high yields, long-maturity high-yield bonds may have relatively low price sensitivity to further spread changes compared with similar-maturity investment-grade bonds.

Factors affecting the shape of the spread curve

Several factors influence the shape of the term structure:

-

Cumulative default risk:

- The probability that an issuer defaults generally increases with time, which tends to make spread curves upward sloping, especially for higher-quality issuers.

- For very weak issuers, however, default risk may be heavily concentrated in the near term. If investors expect that the issuer either defaults soon or survives and improves, the curve can invert.

-

Economic and industry cycles:

- If investors expect economic conditions to deteriorate several years ahead, spreads may widen more at intermediate maturities, steepening the spread curve in the “belly.”

- If a current downturn is expected to be short-lived, short-term spreads may be high, but longer-term spreads may be relatively lower (downward sloping).

- For cyclical industries (such as autos, airlines, or commodity producers), credit curves can change shape quickly as the economic outlook changes.

-

Liquidity at different maturities:

- In many markets, bonds around 5–10 years may be most liquid, while very short- or very long-dated bonds can be less liquid.

- Liquidity differences can cause local humps or dips in the spread curve. For example, a highly liquid 5‑year benchmark issue may trade at a tighter spread than a less liquid 6‑year bond from the same issuer.

-

Refinancing and event risk:

- If a large bond maturity or bank facility comes due in a particular year, spreads at that horizon may be elevated.

- Anticipated mergers, regulatory changes, or patent expirations can also affect spreads at specific maturities.

-

Technical supply–demand factors:

- Heavy issuance in certain maturities can localise spread widening.

- Regulatory or investor preferences for particular maturities (for example, insurers preferring long-dated bonds to match liabilities) can compress spreads at those points.

- Index inclusion rules (for example, only including bonds with 1–10 years to maturity) can also affect demand and thus spreads along the curve.

Interpreting steepening and flattening of credit curves

Interpreting changes in the term structure is an important part of spread analysis:

-

Steepening spread curve: spreads increase more at long maturities than at short maturities.

- Often signals rising concern about long-term credit risk or more compensation demanded for long-term illiquidity.

- Can also indicate growing uncertainty about long-run economic conditions, even if near‑term conditions are stable.

- For a high-quality issuer, a steepening curve sometimes reflects investors’ desire to move into shorter maturities to reduce overall portfolio duration, leaving long-dated bonds cheaper.

-

Flattening spread curve: long-maturity spreads rise less than, or even fall relative to, short-maturity spreads.

- Can indicate reduced long-term uncertainty or increased near-term risk.

- A sharp jump in short‑maturity spreads, with long-dated spreads little changed, often reflects concerns about immediate refinancing risk, covenant breaches, or other near-term events.

- For an issuer emerging from distress, near-term spreads may tighten significantly as default is avoided, flattening a previously inverted curve.

It is important to distinguish changes in the credit curve from changes in the risk-free yield curve. A flattening government yield curve might be driven by monetary policy expectations, while a steepening credit curve at the same time can still signal rising long-term credit risk.

Analysts also pay attention to roll-down along the credit curve: if the credit curve is upward sloping, a bond purchased at, say, 7 years to maturity will “roll down” to the lower-spread 6‑year and 5‑year points over time, potentially generating spread-related price gains, provided issuer credit quality remains stable.

Worked Example 1.3

A 3‑year bond from Issuer A trades at a 90 bp spread over the benchmark, while its 10‑year bond trades at 150 bps. Three months later, the 3‑year spread has widened to 140 bps, and the 10‑year spread has moved to 160 bps. How has the shape of the spread curve changed, and what does this most likely imply about perceived credit risk?

Answer:

Initially, the curve is upward sloping: -3‑year spread: 90 bps -10‑year spread: 150 bps -Difference: 60 bps (steep curve) After three months: -3‑year spread: 140 bps -10‑year spread: 160 bps -Difference: 20 bps (much flatter curve) The spread curve has flattened, mainly because short‑term spreads increased much more than long‑term spreads. This pattern is consistent with:

- Rising concerns about near‑term risk (for example, upcoming debt maturity, weaker recent earnings, increased event risk), while

- Long-run views on the issuer’s credit quality have changed less.

Worked Example 1.4

A distressed high-yield issuer has the following observed credit spreads over the government curve: 2‑year bond 900 bps, 5‑year bond 650 bps, and 8‑year bond 600 bps. Describe the shape of the issuer’s credit curve and provide a plausible interpretation.

Answer:

The spreads decline as maturity increases: -2‑year: 900 bps -5‑year: 650 bps -8‑year: 600 bps This is a downward sloping (inverted) credit curve. A plausible interpretation is:

- The market believes there is a high probability of default in the near term (next two years), so investors demand extremely high spreads on short-dated debt.

- Conditional on survival and successful refinancing in the near term, investors may expect that the issuer’s financial condition to improve, so spreads required for longer maturities are lower.

This pattern is typical of distressed or very low-rated issuers where default risk is heavily front-loaded.

Option-Adjusted Spread (OAS): Basics

For bonds with embedded options—such as callable, putable, or many mortgage-backed securities—the quoted yield and nominal spread reflect not only credit and liquidity risk but also the value of these options. To compare such bonds fairly with option-free bonds, the effect of the option must be removed.

Key Term: embedded option

A contractual feature in a bond that gives the issuer or investor the right, but not the obligation, to take an action such as calling, putting, or converting the bond under specified conditions. Key Term: option-free bond

A plain-vanilla bond with no embedded options; its promised cash flows depend only on the issuer not defaulting and are not subject to early redemption or investor exercise rights. Key Term: nominal spread

The simple difference between the bond’s yield-to-maturity and the yield of a comparable-maturity government (or other benchmark) bond. It does not account for the term structure of interest rates or the presence of embedded options. Key Term: Z-spread (zero-volatility spread)

The constant spread that, when added to each spot rate on the benchmark zero-coupon yield curve and used to discount the bond’s promised cash flows, makes the present value of those cash flows equal to the bond’s market price. For bonds with embedded options, the Z-spread still includes the effect of the option. Key Term: option cost

The value of the embedded option, expressed in yield or spread terms. For a callable bond, investors are effectively short a call option to the issuer (option cost is a positive yield component). For a putable bond, investors are long a put option (option benefit reduces required yield).

Comparing spread measures

For bonds without embedded options:

-

The nominal spread and Z-spread are often similar, especially when:

- The benchmark yield curve is relatively flat, and

- The bond is not very long-dated.

-

Both measures are intended to capture compensation for credit and liquidity risk.

-

The Z-spread is conceptually more precise because it uses the full term structure of benchmark spot rates: each cash flow is discounted at the corresponding risk‑free spot rate plus a constant spread .

When the benchmark curve is not flat (for example, an upward-sloping government curve), the nominal spread can be a noisy measure because it compresses the entire term structure into a single yield number. The Z-spread avoids this by working directly with spot rates.

For bonds with embedded options, however:

-

The nominal spread and Z-spread include both:

- Compensation for credit and liquidity risk, and

- Compensation for option risk (short or long position).

-

They are therefore not “pure” measures of credit and liquidity compensation.

The OAS removes the option effect by:

- Building an interest rate tree or performing a Monte Carlo simulation that is consistent with the benchmark yield curve and an assumed volatility of interest rates.

- Adding a trial constant spread to each rate in the tree.

- Valuing the bond’s cash flows along each path, recognising that the embedded option may be exercised depending on how rates change.

- Adjusting the spread until the model price equals the observed market price.

The resulting OAS is interpreted as the spread that would be required on an otherwise similar option-free bond to make its price equal to the observed price of the bond with the embedded option.

Conceptually:

-

For callable bonds:

- Investors are short a call option (the issuer can redeem the bond when rates fall).

- The option is a cost to the investor, so the observed spread must compensate for both credit/liquidity risk and this option cost.

- Z‑spread ≈ OAS + option cost.

-

For putable bonds:

- Investors are long a put option (they can sell the bond back when spreads widen or rates rise).

- The option is a benefit to the investor, reducing the yield required for a given OAS.

- Z‑spread ≈ OAS − option cost.

At Level 1, a simplified relationship is often presented using nominal spreads instead of Z-spreads:

-

For a callable bond: Nominal spread ≈ OAS + option cost

-

For a putable bond: Nominal spread ≈ OAS − option cost

The key idea is the same: the observed spread includes both pure credit/liquidity compensation (OAS) and the value of any embedded options.

In practice, OAS is particularly important for:

- Callable and putable corporate bonds.

- Mortgage-backed securities (MBS), where homeowners’ prepayment options resemble a call option on the pooled mortgages.

- Other asset-backed securities with prepayment or extension options.

Analysts use OAS to:

- Compare option‑embedded bonds with option‑free bonds on a consistent basis.

- Separate option risk from credit and liquidity risk.

- Detect relative mispricing within sectors after controlling for option features.

Illustration: G-spread, I-spread, Z-spread, and OAS

Consider a 7‑year corporate bond:

- Yield to maturity: 4.2%

- 7‑year government yield: 2.6%

- 7‑year swap rate: 2.8%

Then:

- G‑spread ≈ 4.2% − 2.6% = 1.6% = 160 bps

- I‑spread ≈ 4.2% − 2.8% = 1.4% = 140 bps

If we discount its cash flows using the full government spot curve and find that a spread of 150 bps over every spot rate makes PV equal to price, then:

- Z‑spread = 150 bps

For an option‑free bond, this Z‑spread is effectively its OAS and represents pure credit and liquidity compensation. For a callable version of the same bond priced at the same yield, the nominal spread and Z‑spread would be higher than the OAS because they incorporate the call option’s value.

Worked Example 1.5

A callable bond has a nominal spread of 200 bps over the benchmark. The estimated value of the embedded call option is 40 bps (in yield terms). What is the bond’s OAS, and how should you use it in relative-value analysis?

Answer:

For a callable bond, the option cost is added to the OAS to obtain the nominal spread. Rearranging: -OAS = Nominal spread − Option cost -OAS = 200 bps − 40 bps = 160 bps The 160 bps OAS represents the compensation for credit and liquidity risk only, after stripping out the effect of call risk. It is appropriate to compare this 160 bps spread with: -The OAS of other callable bonds, and -The spreads (Z‑spreads or OAS) of similar option-free bonds with the same issuer, rating, and maturity. This allows a fair assessment of whether the bond offers attractive compensation for credit and liquidity risk, after adjusting for the embedded call.

OAS for putable bonds

For putable bonds, investors benefit from the option: if credit quality deteriorates or interest rates rise, they can sell the bond back to the issuer at the put price. This makes the bond less risky and lowers the required yield, all else equal.

Consequently, the nominal spread of a putable bond is smaller than its OAS:

- Nominal spread = OAS − option benefit (option cost is effectively negative).

- Therefore, OAS = Nominal spread + option benefit.

Worked Example 1.6

A 7‑year putable corporate bond has a nominal spread of 150 bps over the benchmark. The estimated value of the embedded put option is 25 bps in spread terms. What is its OAS? How does this compare with a similar non-putable bond’s spread of 160 bps?

Answer:

For a putable bond: -OAS = Nominal spread + Option benefit -OAS = 150 bps + 25 bps = 175 bps Interpretation: -The putable bond’s investors receive 175 bps of compensation for credit and liquidity risk (OAS), but its quoted nominal spread is only 150 bps because the put option reduces required yield. -Compared to a similar non-putable bond with a 160 bps spread, the putable bond actually offers more credit and liquidity compensation (175 bps) despite its lower nominal spread. This illustrates why nominal spreads across bonds with different option features can be misleading. OAS allows a fairer comparison.

Interest rate volatility and OAS

In valuing bonds with embedded options, the assumed volatility of interest rates matters because it affects the value of the option:

-

For a callable bond (investor short a call):

- Higher interest rate volatility increases the probability that rates fall sharply, making it more likely the issuer will call the bond.

- This increases the value of the call option to the issuer (and its cost to the investor).

- Holding the bond’s market price and the benchmark yield curve constant, a higher option cost means the OAS (pure credit/liquidity spread) must be lower.

-

For a putable bond (investor long a put):

- Higher volatility increases the probability that rates rise or spreads widen sharply, making it more likely the investor will exercise the put.

- This increases the value of the put option (a benefit to the investor).

- Holding price and benchmark curve constant, the OAS will be higher.

-

By contrast, for an option-free bond, the calculated OAS (which in this case is essentially the same as the Z-spread) is independent of interest rate volatility assumptions because there is no option whose value depends on volatility.

This dependence on volatility is frequently tested conceptually in exam questions.

Worked Example 1.7

A 10‑year callable bond has a nominal spread of 210 bps. Under a low interest rate volatility assumption, the option cost is estimated at 50 bps in spread terms. Under a higher volatility assumption, the option cost rises to 80 bps, with the bond’s price and benchmark curve unchanged. What are the OAS values under the two volatility assumptions, and what does the change imply?

Answer:

Under the low volatility assumption: -OAS = Nominal spread − Option cost = 210 − 50 = 160 bps Under the high volatility assumption: -OAS = 210 − 80 = 130 bps Interpretation: -As interest rate volatility increases, the call option becomes more valuable to the issuer (more costly to the investor), so the option cost rises. -With the market price unchanged, the model assigns a smaller portion of the total spread to pure credit and liquidity compensation (OAS falls from 160 bps to 130 bps). -This behaviour—OAS decreasing with higher volatility—is characteristic of callable bonds. For putable bonds, the opposite holds: OAS would increase as volatility rises.

OAS, effective duration, and embedded options

In later fixed-income readings, OAS is closely linked to duration measures for bonds with embedded options.

Key Term: effective duration

A duration measure that estimates the sensitivity of a bond’s price to small parallel shifts in the benchmark yield curve, taking into account that embedded options may change expected cash flows when yields change.

For option-free bonds, effective duration and modified duration are very similar. For callable or putable bonds:

- Effective duration is calculated using a pricing model that incorporates option exercise behaviour and often uses OAS to align the model with the observed market price.

- Callable bonds usually have lower effective duration than an otherwise similar option-free bond because the call option limits price appreciation when yields fall (“negative convexity”). As yields decline, the likelihood of a call increases, capping further price gains and causing effective duration to shorten.

- Putable bonds often have effective duration that is shorter when yields rise, as the put sets a floor on price declines. When yields increase significantly, the bond’s price tends toward the put price, and further yield increases have smaller incremental effects.

The combination of OAS and effective duration allows analysts to:

- Separate pure credit/liquidity compensation (OAS) from interest rate and option risk.

- Measure how sensitive price is to changes in the benchmark curve, controlling for option exercise.

- Compare interest rate risk across bonds with different embedded options on a consistent basis.

Exam warning on comparing spreads

A common mistake is to compare nominal spreads for bonds with different option features (for example, callable versus non-callable versus putable). Because nominal spreads for callable bonds are inflated by call risk and those for putable bonds are depressed by the put option, they are not directly comparable.

For relative-value analysis across bonds with different embedded options, use OAS (or OAS-based measures) whenever it is available. For option-free bonds, the OAS and Z‑spread will be very similar and both represent compensation for credit and liquidity risk.

In some markets, analysts also look at an “OAS-to-Treasury” or “OAS-to-swap” measure (OAS over the government or swap curve) when comparing bonds across sectors. The key idea remains: adjust for options before comparing credit compensation.

Credit Spread Analysis in Practice

Credit spreads and OAS are used in several ways in fixed income analysis.

Assessing credit quality and market-implied risk

- Widening spreads for an issuer or sector typically indicate rising perceived credit risk, reduced liquidity, or both.

- Tightening spreads often reflect improving fundamentals, lower expected default rates, or stronger demand for credit.

- Because rating changes can lag market developments, spread behaviour often provides earlier signals than credit rating actions. For example, spreads on a company’s bonds may widen significantly months before a formal downgrade.

Credit spread levels across rating categories provide a quick “market view” of relative credit risk. For instance:

- AAA spreads might be in the tens of basis points.

- BBB spreads could be 100–200 bps.

- Single‑B and CCC spreads can be several hundred basis points or more, particularly in stressed markets.

These differences reflect both higher expected default losses and higher required risk premiums for bearing more uncertain and cyclical cash flows.

Relative-value analysis across issuers or sectors

Analysts compare spreads across bonds with similar maturities and ratings to identify mispriced securities:

- If Bond A and Bond B have similar ratings, maturities, and structures but Bond A trades at a meaningfully wider OAS, analysts investigate why:

- Is there a genuine difference in fundamentals (higher leverage, lower coverage, weaker industry position)?

- Or is the spread difference mainly due to technical factors (lower liquidity, non‑index issue, recent forced selling)?

For bonds with embedded options, OAS is used to ensure comparisons focus on credit and liquidity compensation, not option features:

- A callable bond and a non‑callable bond with similar OAS but different nominal spreads may offer similar risk‑adjusted value once option risk is considered.

- A putable bond with a lower nominal spread than a non‑putable bond may still have a higher OAS if the put is valuable.

Monitoring the term structure of spreads

The credit curve shows how the market views the timing of credit risk:

- A steepening spread curve might lead a portfolio manager to reduce long-maturity exposure to vulnerable issuers or sectors.

- A flattening curve for high-quality issuers might suggest opportunities to extend duration without taking much additional credit risk.

- For high‑yield issuers, a sharply inverted credit curve may signal severe near‑term distress and potential default.

Managers may also look at how spreads at different maturities move relative to each other:

- Parallel shifts (similar changes at all maturities).

- Rotations around an intermediate point (belly of the curve).

- Localised moves around known event dates (for example, large maturities or regulatory decisions).

Pricing new issues

When a company issues a new bond:

- Underwriters reference current secondary-market spreads for similar issuers and maturities to set the new issue spread.

- They adjust for any embedded options by estimating OAS and option cost.

- New issues often come at a small concession (slightly wider spread) to attract investors; this concession can be evaluated using spread or OAS comparisons.

If a new issue offers a materially wider OAS than comparable existing bonds, it may be considered attractively priced (cheap) relative to the market; if its OAS is materially tighter, it may be rich.

Managing portfolio risk

Spread duration (the sensitivity of price to changes in credit spreads) is used alongside interest rate duration to measure total risk:

- Managers may reduce spread duration before a forecasted recession, when spreads are likely to widen.

- Conversely, when spreads appear unusually wide relative to history and fundamentals (for example, after a sharp market sell‑off), managers may increase spread exposure to capture potential tightening.

Portfolio-level spread duration can be decomposed by rating, sector, or issuer, allowing targeted risk management. For example:

- Reduce high-yield spread duration while maintaining investment-grade exposure.

- Tilt towards defensive sectors (utilities, consumer staples) and away from cyclical sectors (autos, airlines) when recession risk rises.

Spreads, credit ratings, and the credit cycle

As discussed earlier, credit spreads, ratings, and the stage of the credit cycle are closely linked:

-

Early in an expansion:

- Spreads are still relatively wide following a recession, but fundamentals are improving.

- Default rates are falling, and upgrades may begin to outnumber downgrades.

- This can be an attractive time to add credit risk, especially in intermediate maturities.

-

Mid to late expansion:

- Spreads gradually tighten, particularly for high-yield issuers.

- Issuers may increase leverage using cheap funding (for example, to finance acquisitions or buybacks).

- The risk–reward trade-off becomes less favourable as spreads approach historically tight levels.

-

Downturn or recession:

- Spreads widen sharply, especially in high yield and cyclical sectors.

- Downgrades and defaults increase, and liquidity may deteriorate.

- Investors become more selective, favouring higher-quality issuers.

Because ratings update infrequently, spreads are often a better real-time indicator of where an issuer sits in the credit cycle. A sudden spread widening for a single issuer, compared with peers, often precedes a rating downgrade.

There have been cases where bonds initially rated investment grade traded at spreads typical of high-yield issues well before ratings agencies downgraded them, illustrating that market‑implied credit views can move much faster than formal ratings.

Linking spreads to fundamental credit analysis

Spread and OAS analysis complements, but does not replace, fundamental credit analysis based on financial statements and ratios. Some key ideas:

- Profitability and cash flow metrics (for example, EBITDA, free cash flow) inform the issuer’s ability to generate cash.

- Leverage metrics (for example, debt/EBITDA, debt/capital, FFO/debt) capture how much debt is outstanding relative to earnings or cash flow.

- Coverage metrics (for example, EBITDA/interest expense, EBIT/interest expense) measure the ability to cover interest payments from operating profits.

- Liquidity metrics (for example, cash balances, committed credit lines) indicate the capacity to handle temporary shocks.

Higher leverage and weaker coverage ratios generally result in wider spreads. For example:

- A company with debt/EBITDA of 1.5× and EBITDA/interest of 8× will normally trade at tighter spreads than a peer with debt/EBITDA of 4× and EBITDA/interest of 2×, all else equal.

Analysts may also look at trends:

- Are leverage and coverage ratios improving or deteriorating?

- Is free cash flow positive and sufficient to reduce debt over time, or is the company consistently borrowing to fund operations?

Research in the curriculum also emphasises that:

- Profitability and free cash flow are the starting point: if a business is structurally unprofitable, even low leverage may not be sufficient to ensure timely debt service.

- Leverage metrics (like debt/EBITDA) should be interpreted in the context of business volatility. The same leverage may be acceptable for a stable utility but risky for a cyclical commodity producer.

- Coverage ratios provide a more direct test of capacity to service interest.

Key Term: recovery rate

(Reiterated) Because structural features affect recovery, spreads for secured, senior bonds typically embed higher expected recovery and thus a smaller loss given default than subordinated or unsecured issues. This is reflected in spread differences across an issuer’s capital structure.

Rating agencies use these metrics, together with qualitative factors (management quality, industry position, regulatory environment), to assign ratings. Investors then analyse whether observed spreads are consistent with these fundamentals. If a bond trades at a spread much wider than peers with similar fundamentals, it may be “cheap” unless there is hidden risk.

Seniority, security, and spreads

Within a single issuer’s capital structure, different bonds can have different seniority and security features:

- Secured bonds (backed by specific collateral) usually trade at tighter spreads than unsecured bonds.

- Senior bonds rank ahead of subordinated or junior bonds in bankruptcy and therefore have lower expected loss and tighter spreads.

- Subordinated and hybrid instruments (for example, deeply subordinated bank capital securities) have higher spreads to reflect their lower recovery in default and greater likelihood of coupon deferral or loss absorption.

These structural features influence spreads even when the issuer’s rating is the same. For exam purposes, remember: higher expected recovery → lower spread, holding everything else constant.

Worked Example 1.8

Bond A (non-callable) and Bond B (callable) both have AA ratings and 7‑year maturities. Bond A yields 3.2%, the benchmark yield is 2.5%, and Bond B yields 3.5% with an estimated option cost of 0.3%. What are the credit spreads and OAS, and which bond offers greater pure credit compensation?

Answer:

For Bond A (non-callable): -Credit spread = Yield − Benchmark yield -Credit spread = 3.2% − 2.5% = 0.7% = 70 bps For Bond B (callable): -Nominal spread = 3.5% − 2.5% = 1.0% = 100 bps -Option cost (call option) = 0.3% = 30 bps -OAS = Nominal spread − Option cost = 100 bps − 30 bps = 70 bps Interpretation: -Both bonds have an OAS of 70 bps. -Bond B’s higher nominal spread (100 bps versus 70 bps) is fully explained by the embedded call option; once the option cost is stripped out, the two bonds provide the same compensation for credit and liquidity risk. -From a pure credit view, neither bond is superior; the choice will depend on the investor’s views on interest rates and call risk.

Worked Example 1.9

A 5‑year corporate bond’s yield decreases from 4.0% to 3.7%. Over the same period, the 5‑year government yield increases from 2.0% to 2.2%. What has happened to the bond’s credit spread, and what might this suggest about credit conditions?

Answer:

Initial credit spread: -4.0% − 2.0% = 2.0% = 200 bps New credit spread: -3.7% − 2.2% = 1.5% = 150 bps The credit spread has narrowed by 50 bps (from 200 to 150 bps), even though the bond’s yield fell only 30 bps and government yields rose 20 bps. This suggests: -Market participants now view the issuer as less risky (improved credit outlook), and/or -There is stronger demand or better liquidity in the corporate bond market. Spread tightening is typically associated with improving credit conditions or higher risk appetite.

Worked Example 1.10

A 10‑year callable bond and a 10‑year option-free bond from the same issuer both trade at par. The government yield at 10 years is 2.8%. The callable bond’s yield is 4.2%, and the option-free bond’s yield is 3.6%. If the option cost for the callable bond is estimated to be 50 bps in spread terms, compare the OAS of the two bonds and comment on relative value.

Answer:

For the option-free bond: -Nominal spread = 3.6% − 2.8% = 0.8% = 80 bps -With no embedded options, OAS ≈ nominal spread = 80 bps For the callable bond: -Nominal spread = 4.2% − 2.8% = 1.4% = 140 bps -Option cost = 50 bps -OAS = Nominal spread − option cost = 140 − 50 = 90 bps Interpretation: -The callable bond offers an OAS of 90 bps, 10 bps higher than the 80 bps OAS of the option-free bond. -After adjusting for option risk, the callable bond provides slightly more compensation for credit and liquidity risk. -All else equal (including liquidity and tax treatment), the callable bond appears marginally more attractive on a pure credit basis, but the investor must also be comfortable bearing call risk and potential price appreciation caps if yields fall.

Revision tip on OAS interpretation

When interpreting OAS, always remember what it includes and excludes:

- Includes: compensation for credit and liquidity risk.

- Excludes: value of embedded options and pure interest rate risk (captured by the benchmark yield curve).

OAS is the appropriate measure to compare:

- Callable versus putable versus option-free bonds, and

- Corporate and structured products that differ in option structure.

Nominal spreads alone can be very misleading when option features differ.

Summary

Credit spreads quantify the additional yield investors demand over a risk-free benchmark for taking on credit and liquidity risk. The term structure of credit spreads—the pattern of spreads across maturities—reveals how investors perceive the timing and magnitude of credit risk. Upward-sloping, flat, downward-sloping, or hump-shaped spread curves each carry distinct implications about expected default risk, liquidity, and macroeconomic conditions, and changes in curve shape (steepening or flattening) provide signals about shifts in perceived near‑term versus long‑term risk.

For bonds with embedded options, nominal spreads and Z-spreads are not sufficient for comparison because they combine credit and liquidity compensation with the value of the options. The option-adjusted spread (OAS) removes the option value, isolating the spread attributable to credit and liquidity risk. For callable bonds, the nominal spread or Z-spread exceeds the OAS by the option cost; for putable bonds, the OAS exceeds the nominal spread by the option benefit. OAS is also sensitive to interest rate volatility for bonds with options, while it is essentially unaffected by volatility assumptions for option-free bonds.

Using credit spreads, OAS, and spread duration together allows analysts to:

- Decompose bond yields into benchmark and credit components.

- Assess how spread changes (independent of interest rates) affect prices and total returns.

- Compare bonds with and without embedded options on a consistent basis.

- Interpret market signals about creditworthiness, liquidity, and the stage of the credit cycle.

- Link market‑implied credit views (through spreads and OAS) to fundamental analysis (through financial ratios, business risk, and capital structure).

Understanding how to interpret spread levels, spread changes, OAS, and the term structure of credit spreads is fundamental for pricing bonds, assessing credit risk, and positioning fixed income portfolios in line with views on issuers and macroeconomic conditions.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain what a credit spread is and identify its main components (default risk premium and liquidity premium).

- Describe how credit spreads respond to changes in issuer fundamentals, macroeconomic conditions, and market liquidity.

- Distinguish spread tightening from spread widening and relate each to bond price movements and credit conditions.

- Describe the term structure of credit spreads, typical shapes, and what steepening or flattening spread curves indicate.

- Recognise the differences in credit curve behaviour between investment-grade and high-yield issuers.

- Define nominal spread, Z-spread, and option-adjusted spread (OAS), and explain their relationships.

- Calculate simple OAS values from nominal spreads and option costs for callable and putable bonds.

- Interpret OAS as a measure of compensation for credit and liquidity risk, excluding embedded option value.

- Explain how interest rate volatility affects the OAS of callable and putable bonds but not option-free bonds.

- Use spread duration to approximate the price impact of changes in credit spreads, holding benchmark yields constant.

- Recognise why nominal spreads for bonds with different embedded options should not be compared directly.

- Use credit spread and OAS analysis to infer market-implied credit risk and to identify relative-value opportunities.

- Link spread movements to the credit cycle and distinguish between fundamental and technical drivers of spread changes.

- Relate spread differentials to seniority, security, and expected recovery rates within an issuer’s capital structure.

- Connect credit spreads with key financial ratios (leverage, coverage, profitability) used in corporate credit analysis.

- Understand basic benchmark-based spread measures (G-spread and I-spread) and how they relate to credit spreads, Z‑spreads, and OAS.

Key Terms and Concepts

- credit spread

- yield spread

- G-spread (government spread)

- I-spread (interpolated spread)

- term structure of credit spreads

- option-adjusted spread (OAS)

- benchmark yield curve

- investment-grade bond

- high-yield (speculative-grade) bond

- credit cycle

- default risk premium

- liquidity premium

- probability of default (PD)

- loss given default (LGD)

- recovery rate

- credit rating

- seniority

- secured debt

- subordinated debt

- downgrade risk

- upgrade risk

- fallen angel

- crossover bond

- flight-to-quality

- flight-to-liquidity

- credit spread risk

- spread tightening

- spread widening

- spread duration

- credit spread curve (credit curve)

- embedded option

- option-free bond

- nominal spread

- Z-spread (zero-volatility spread)

- option cost

- effective duration