Learning Outcomes

This article explains dividend policy theories, payout mechanisms, and their implications for valuation, including:

- distinguishing among regular, special, liquidating, and stock dividends, as well as share repurchases, and linking each method to typical corporate objectives;

- comparing dividend irrelevance, bird-in-the-hand, and tax preference theories, and evaluating how each predicts the relationship between payout choices and firm value;

- analyzing how dividend changes and share repurchase announcements act as signals about management’s expectations for future earnings, risk, and investment opportunities;

- assessing the effects of dividends and buybacks on key exam-relevant metrics such as earnings per share (EPS), book value per share (BVPS), payout ratios, and dividend coverage;

- evaluating the conditions under which firms are likely to favor stable dividends, constant payout ratios, or residual payout policies, and the implications for dividend sustainability;

- interpreting market reactions to payout policy changes and repurchases, and applying this understanding to typical CFA Level 2 item-set and calculation-style questions.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are required to understand how payout policy and capital structure decisions influence firm value, investor signals, and market price, with a focus on the following syllabus points:

- Defining and distinguishing between regular, special, stock, and liquidating dividends

- Comparing stable dividend, constant payout, and residual dividend policies

- Explaining dividend irrelevance, bird-in-hand, and tax preference theories

- Analyzing share repurchase methods and their effects on financial metrics

- Interpreting dividend and repurchase actions as signals to the market

- Calculating the impact of payout decisions on earnings per share (EPS), book value per share (BVPS), and coverage ratios

- Evaluating dividend sustainability and factors that influence payout policies

- Comparing paying cash dividends to repurchasing shares, including tax, flexibility, and signaling considerations

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

Background vignette (use for Questions 1–5):

Omega Tools has the following data (before any payout decision):

- Net income: $120 million

- Shares outstanding: 40 million

- Share price: $30

- Book value of equity: $400 million

- Cash balance in excess of operating needs: $60 million (earning essentially zero)

- Cost of new debt (after tax): 4%

- Book value per share (BVPS): $400 / 40 = $10

Management is considering three alternative actions:

- Plan A: Initiate a regular cash dividend of $1.00 per share.

- Plan B: Make a one‑time special cash dividend of $1.50 per share but no ongoing regular dividend.

- Plan C: Use the entire $60 million excess cash to repurchase shares at the current market price.

Assume no taxes and no market imperfections unless otherwise stated.

-

Under dividend irrelevance theory, which statement best describes the impact of choosing Plan A versus Plan C on Omega’s value?

- a) Plan A will increase firm value because cash dividends are preferred to capital gains.

- b) Plan C will increase firm value because repurchases improve EPS.

- c) Firm value will be the same under Plans A and C, ignoring taxes and transaction costs.

- d) Firm value will be higher under the plan that produces the higher BVPS.

-

Under Plan C, approximately how many shares will Omega repurchase, and what happens to EPS (ignoring interest income on cash)?

- a) 1 million shares; EPS rises because shares decline while income is unchanged.

- b) 2 million shares; EPS rises because shares decline while income is unchanged.

- c) 2 million shares; EPS falls because equity decreases.

- d) 1 million shares; EPS is unchanged because total equity is unchanged.

-

If Omega’s announcement is an unexpected and credible move from “no dividend” to Plan A (a stable $1.00 regular dividend), how is the market most likely to interpret this?

- a) As a positive signal that management expects stronger and more stable future earnings.

- b) As a negative signal that Omega has run out of positive‑NPV projects.

- c) As neutral, because in efficient markets payout decisions contain no information.

- d) As negative, because it will increase Omega’s tax burden relative to investors.

-

Which payout theory best supports a client preference for Plan C (repurchase) over Plan A (regular dividend) if the client faces a higher tax rate on dividends than on capital gains?

- a) Dividend irrelevance theory

- b) Bird‑in‑the‑hand theory

- c) Tax preference theory

- d) Signaling theory

-

If instead Omega borrows $60 million at an after‑tax cost of 4% to fund the repurchase (and leaves its cash intact), which condition must hold for EPS to increase after the repurchase?

- a) The firm’s earnings yield exceeds 4%.

- b) The firm’s P/E ratio exceeds the market P/E.

- c) The firm’s BVPS exceeds the repurchase price.

- d) The firm’s dividend payout ratio is less than 50%.

Introduction

Capital structure and payout policy decisions shape how a company returns value to shareholders and send signals to the market. Payout policy covers not only cash dividends (both regular and irregular) but also share repurchases, as companies increasingly use buybacks alongside dividends. Understanding the theories and practical effects of these decisions is essential for both valuation and interpreting signals for the CFA Level 2 exam.

Key Term: payout policy

The firm’s approach to distributing earnings to shareholders through cash dividends, special dividends, share repurchases (buybacks), or a combination.

Dividend and repurchase choices affect:

- the pattern, level, and stability of cash flows to equity holders,

- perceived risk and growth opportunities,

- capital structure (through changes in equity and sometimes debt),

- valuation metrics such as P/E, BVPS, and justified multiples in dividend discount and free cash flow models.

At Level 2, you must move beyond definitions and analyze how a specific payout action affects both numbers (EPS, BVPS, coverage ratios) and investor interpretation (signaling).

Test Tip: When revising Dividends share repurchases and signaling, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Exam Warning: Do not rely on keyword recognition alone; check the precise condition, exception, calculation step, or evidence the question requires.

Types of Dividends and Payout Methods

Companies can return cash to shareholders through several methods: regular cash dividends, special (or extra) dividends, liquidating dividends, stock dividends, and share repurchases.

Key Term: regular cash dividend

A recurring cash payment to shareholders, usually quarterly or annually, representing a portion of earnings that management expects to sustain. Key Term: special (extra) dividend

A non‑recurring cash dividend, typically larger than the regular dividend, paid under unusual or highly profitable circumstances and not expected to be maintained. Key Term: liquidating dividend

A cash distribution that exceeds cumulative retained earnings and represents a return of shareholders’ invested capital, often associated with selling all or part of the firm. Key Term: stock dividend

A non‑cash dividend in which a company distributes additional shares to existing shareholders in proportion to their holdings, leaving proportional ownership unchanged. Key Term: stock split

A corporate action that increases the number of shares and proportionally reduces the price per share (for example, a 2‑for‑1 split), without changing total equity value. Key Term: reverse stock split

The opposite of a stock split; it reduces the number of shares and increases the price per share (for example, a 1‑for‑5 reverse split), often to move the price into a higher trading range. Key Term: share repurchase

When a company buys back its own shares from the market or shareholders, reducing the number of shares outstanding and returning cash to shareholders.

Cash dividends: regular, special, and liquidating

Regular cash dividends communicate stable, ongoing profitability. Many firms target a pattern of stable or slowly increasing regular dividends and are very reluctant to cut them, precisely because the market treats cuts as negative signals.

Special (extra) dividends allow management to distribute temporary excess cash (for example, from an unusually profitable year or the sale of a non‑core division) without committing to a permanently higher regular dividend. The market typically views a special dividend as largely non‑recurring and does not project it into future expected cash flows.

Liquidating dividends occur when the firm winds down operations or sells a major portion of its assets and distributes the proceeds. Economically, these cash flows are partly or wholly a return of capital rather than a return on capital. The shareholder’s wealth increases only if the distribution exceeds what the assets were previously valued at.

From an accounting and ratio standpoint:

- Declaring a cash dividend reduces retained earnings and creates a dividend payable (a current liability).

- On the payment date, cash and the liability both decrease.

- As a result, liquidity ratios (current and quick ratios) and equity decline, while leverage ratios (debt‑to‑equity, debt‑to‑assets) increase.

Stock dividends, stock splits, and reverse splits

Stock dividends and stock splits do not involve cash and do not change total shareholders’ equity. They simply reclassify equity and change the number of shares outstanding and the par value per share.

After a small stock dividend:

- each shareholder holds more shares,

- the share price falls in inverse proportion (ignoring signaling effects),

- the total value of the holding is unchanged.

The same logic applies to stock splits. A 2‑for‑1 split doubles the number of shares and halves the share price. A reverse stock split does the opposite. Firms use splits and reverse splits to move the share price into a “desirable” trading range (for example, to improve liquidity or meet minimum listing thresholds).

Key Term: book value per share (BVPS)

Common shareholders’ equity divided by the number of common shares outstanding.

Stock dividends and splits change the denominator in BVPS and EPS but also adjust the numerator in a way that leaves per‑share and ownership economics unchanged. In exam questions, you will often be required to restate prior‑period EPS for stock splits and stock dividends to maintain comparability.

Dividend payment chronology (brief recap)

Although emphasized at Level I, you may still see questions that rely on the timing of dividend dates:

- Declaration date: board announces the dividend; a liability is recorded.

- Ex‑dividend date: shares begin trading without the right to the upcoming dividend; price typically falls by approximately the dividend amount (ignoring taxes and frictions).

- Holder‑of‑record date: company determines which shareholders are entitled to receive the dividend.

- Payment date: cash is disbursed.

On an exam, if you are told the trade occurs on or after the ex‑dividend date, the buyer does not receive the declared dividend.

Theories of Dividend Policy

Dividend policy has been extensively studied. Three primary theories are tested at Level 2.

Key Term: dividend irrelevance theory

The proposition that, in a world with no taxes, transaction costs, or information asymmetries, a firm’s value is unaffected by its dividend payout policy. Key Term: bird‑in‑the‑hand theory

The view that investors prefer certain current dividends to uncertain future capital gains, so higher payout reduces perceived risk and may increase firm value. Key Term: tax preference theory

The view that, when dividends are taxed more heavily than capital gains, investors prefer low‑payout firms that retain earnings or repurchase shares.

Dividend irrelevance (Modigliani–Miller)

Under Modigliani–Miller’s assumptions (no taxes, no transaction costs, fixed investment policy, perfect information), payout policy does not affect intrinsic value:

- If the firm pays a dividend, the share price falls by the dividend amount; investors receive cash plus a lower‑priced share.

- If the firm does not pay a dividend, the share price is higher, but investors can create “homemade dividends” by selling a small portion of their holdings.

This theory underpins the idea that, in perfect markets, a $1 of dividend and a $1 of repurchase are equivalent distributions of cash.

Bird‑in‑the‑hand (dividend preference) theory

This theory argues that:

- dividends are certain cash flows received now,

- capital gains are uncertain and depend on future earnings and investment decisions.

Because risk‑averse investors discount uncertain future gains more heavily, they may require a lower rate of return for high‑dividend stocks, which in a Gordon growth model framework implies a higher value:

If a higher payout reduces perceived risk (lowers ), holding growth constant, rises. This theory predicts that, all else equal, high‑dividend firms trade at higher valuations.

Tax preference theory

When dividends face higher tax rates or are taxed earlier than capital gains, investors may prefer:

- low dividend payout,

- higher retention of earnings,

- share repurchases (which are taxed as capital gains when investors sell).

In this framework, a higher payout implies a higher effective tax burden on investors, who then require a higher pre‑tax return to compensate, increasing and reducing . The theory predicts that firms facing a shareholder base in high tax brackets may favor low‑dividend policies and repurchases.

In practice, no single theory perfectly explains behavior. Payout policy reflects a mix of tax, signaling, agency, and client‑base considerations.

Signaling Effects of Dividend and Repurchase Decisions

Management’s payout decisions convey information about profitability and future prospects, especially when information asymmetry exists.

Key Term: signaling

The concept that corporate actions (like dividend changes or share repurchases) communicate information about management’s private assessment of the firm’s future.

Key ideas:

- Managers are reluctant to increase regular dividends unless they believe higher cash flows are sustainable; they know that a future cut would be punished by the market.

- Unexpected dividend increases and the initiation of a stable dividend often signal confidence in future earnings and cash flows.

- Dividend cuts, omissions, or sharp reductions in payout usually signal financial weakness, deteriorating prospects, or a shift to fund large investment needs.

- Share repurchases can signal that management believes the shares are undervalued, especially when accompanied by statements to that effect and when funded from excess cash rather than necessary operating liquidity.

Worked Example 1.1

A company has paid a stable dividend of $1.00 per share for five years. This year, it announces an increase to $1.30 per share. What signal does this send, and what might you expect for the share price if investors believe management has private information about future earnings?

Answer:

The dividend increase signals that management expects higher or more stable earnings going forward and is confident it can sustain the higher payout. If the market trusts management’s assessment, the required return may fall or expected cash flows may be revised upward, so the share price is likely to rise in response to the perceived improvement in outlook.

Additional signaling points

- A shift from dividends toward repurchases may signal a desire for flexibility (management is unsure about the permanence of excess cash flows) or to convey undervaluation without committing to higher ongoing dividends.

- Conversely, substituting a regular dividend for frequent ad‑hoc repurchases may signal that cash flows have become more predictable.

Understanding whether a payout change is permanent (affecting long‑term expectations) or temporary (seen as a one‑off) is central to interpreting the market reaction in exam vignettes.

Share Repurchases: Methods and Effects

Common methods of share repurchase include:

Key Term: open‑market share repurchase

A flexible method in which the firm buys its shares in the secondary market over time, much like any other investor, often up to an announced limit. Key Term: fixed‑price tender offer

A repurchase in which the firm offers to buy a specified number of shares at a fixed price, usually at a premium to the current market price. Key Term: Dutch auction tender

A repurchase in which the firm specifies a price range and shareholders tender shares at different prices; the firm pays a single “clearing price” that repurchases the desired quantity. Key Term: direct negotiation repurchase

A repurchase in which the firm buys shares directly from a large shareholder, sometimes at a premium or discount, to remove an overhang or in a greenmail situation.

- Open‑market transactions are the most common and most flexible. The firm is not obligated to complete the announced program.

- Fixed‑price tenders and Dutch auctions allow the firm to buy back a relatively large block quickly but at a premium.

- Direct negotiation may be used to remove a large shareholder who wants to exit or in takeover defense.

Share repurchases reduce shares outstanding and may increase metrics like EPS and return on equity (ROE), even if total earnings remain unchanged.

Key Term: EPS (Earnings per Share)

A measure of profit allocated to each outstanding share, calculated as net income divided by the number of common shares outstanding. Key Term: dividend coverage ratio

A measure of the sustainability of dividends, typically net income divided by total dividends (or by total cash distributions in a broader “payout coverage” measure).

Worked Example 1.2

ABC Corp. has net income of $10 million, 5 million shares outstanding, and declares a $2 million dividend. What is the dividend coverage ratio?

Answer:

Dividend coverage ratio = Net income / Total dividends = $10 million / $2 million = 5. ABC can pay its dividend five times from current earnings; a higher ratio generally suggests a more sustainable dividend, assuming cash flows and investment needs are consistent.

EPS impact of repurchases: cash vs debt financing

Repurchases made using surplus cash:

- reduce cash and shareholders’ equity,

- increase financial leverage,

- reduce shares outstanding,

- leave net income unchanged (ignoring lost interest income).

EPS will increase because the denominator (shares) falls while the numerator (net income) is unchanged.

If the repurchase is financed with new debt:

- cash may remain unchanged or even increase,

- debt and interest expense increase,

- net income falls by the after‑tax interest cost,

- shares outstanding fall.

EPS will increase only if the earnings yield before the repurchase exceeds the after‑tax cost of debt. Using notation:

- Earnings yield before repurchase:

- After‑tax cost of debt:

EPS increases if:

Worked Example 1.3

JetFun, Inc., has 10 million shares outstanding and has just reported net income of $50 million. It is considering repurchasing 2 million shares at $50 per share (a 25% premium over the current $40 price), using either $100 million of excess cash or $100 million of new debt at a 3% after‑tax cost. What is the effect on EPS under each financing method?

Answer:

- Current EPS = $50 million / 10 million = $5.00

- After repurchase, shares outstanding = 8 million

Using surplus cash:

- Net income unchanged at $50 million (ignoring interest income)

- New EPS = $50 million / 8 million = $6.25 (25% increase)

Using new debt:

- After‑tax interest expense = 3% × $100 million = $3 million

- New net income = $50 – $3 = $47 million

- New EPS = $47 million / 8 million = $5.875 (17.5% increase)

In both cases EPS increases because the earnings yield, $5/50 = 10%, exceeds the after‑tax cost of debt (3%). However, leverage increases, so a higher EPS does not automatically imply higher firm value.

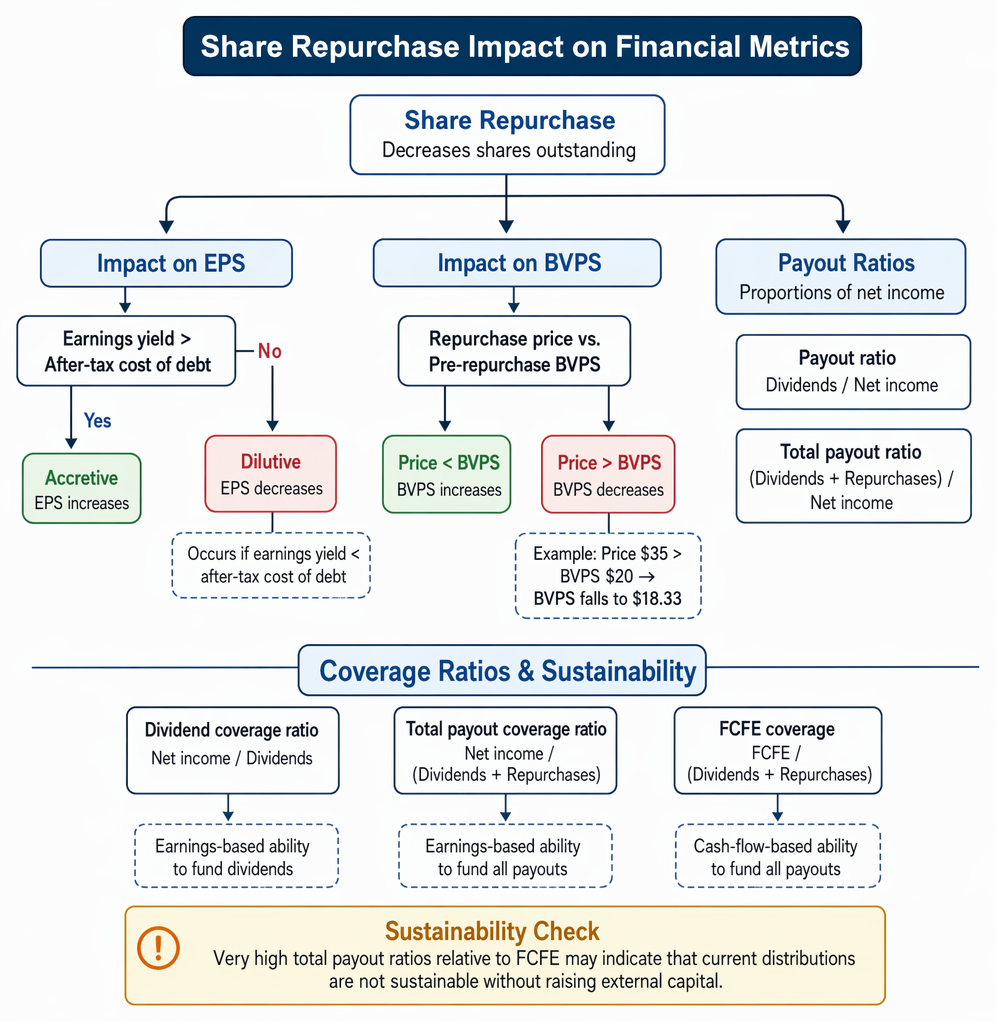

Impact on Financial Metrics: EPS, BVPS, and Coverage

Share repurchases decrease the number of shares outstanding and may:

Dividend payout frameworks distinguish stable, constant-ratio, and residual policies and relate each approach to earnings stability, payout variability, and investment priority.

- increase EPS (accretive) when funded at a price where earnings yield exceeds after‑tax debt cost (for debt‑funded) or when funded with idle cash;

- decrease EPS (dilutive) if the firm’s earnings yield is less than the after‑tax cost of debt.

BVPS behavior depends on the relationship between the repurchase price and pre‑repurchase BVPS.

Key Term: payout ratio (dividend payout ratio)

The proportion of net income paid out as cash dividends: dividends / net income. Key Term: total payout ratio

The proportion of net income paid out through both dividends and share repurchases: (dividends + repurchases) / net income.

Worked Example 1.4

XYZ Inc. has 1,000,000 shares, each with a book value of $20 and market price of $35. If the firm repurchases 100,000 shares at market price using cash, what is the effect on BVPS?

Answer:

Initial equity (book value) = $20 million. Repurchase amount = 100,000 × $35 = $3.5 million. New equity = $20 – $3.5 = $16.5 million. New shares outstanding = 1,000,000 – 100,000 = 900,000. New BVPS = $16.5 million / 900,000 = $18.33. BVPS decreases because the repurchase price ($35) exceeds the pre‑repurchase BVPS ($20). Repurchasing above BVPS transfers book value from remaining shareholders to those selling into the repurchase.

Coverage ratios and sustainability

Analysts assess payout sustainability using both earnings‑based and cash‑flow‑based measures:

- Dividend coverage ratio = Net income / Dividends

- Total payout coverage ratio = Net income / (Dividends + Repurchases)

- Free cash flow to equity (FCFE) coverage = FCFE / (Dividends + Repurchases)

From a free‑cash‑flow standpoint, dividends and repurchases are uses of FCFE, not determinants of it. FCFF and FCFE reflect cash flows available before payout; payout decisions allocate those flows between retained cash and distributions. Very high total payout ratios relative to FCFE may indicate that current distributions are not sustainable without raising external capital.

Exam warning

Misunderstanding the effect of share repurchases on EPS and BVPS is common:

- BVPS increases only if shares are repurchased below pre‑repurchase BVPS.

- EPS increases with a debt‑financed repurchase only if earnings yield exceeds the after‑tax cost of debt.

- A higher EPS does not guarantee a higher share price; you must consider risk, leverage, and the required return.

Choosing Between Dividends and Repurchases

Key Term: stable dividend policy

A dividend policy in which the firm targets a relatively fixed dividend per share and adjusts it infrequently, often with a long‑term target payout ratio in mind. Key Term: constant payout ratio

A dividend policy in which a fixed percentage of net income is paid as dividends each period, causing the dividend amount to vary directly with earnings. Key Term: residual dividend policy

A policy in which dividends equal earnings minus the equity portion of capital expenditures needed for positive‑NPV projects; dividends fluctuate with investment opportunities.

Firms may prefer buybacks to regular dividends for several reasons:

- Potential tax advantages where capital gains are taxed more favorably than dividends.

- Greater flexibility: repurchases are discretionary and do not create expectations of continuation in the same way that regular dividends do.

- Signaling and price support: announcing a buyback can signal perceived undervaluation and help support the share price during periods of weakness.

- Offsetting dilution from stock‑based compensation: firms frequently repurchase shares to offset option exercises and maintain EPS.

- Adjusting capital structure: debt‑financed repurchases can increase leverage toward a target capital structure.

Key Term: residual dividend policy

(re‑emphasized) Under this approach, the firm funds all positive‑NPV projects at its target capital structure and pays out any residual earnings as dividends.

In practice, many firms:

- Maintain a relatively stable regular dividend per share (stable dividend policy),

- Supplement it with either occasional special dividends or share repurchases when cash flows are temporarily high,

- Use repurchases to fine‑tune leverage and offset dilution.

Analysts must read vignettes carefully to determine whether a payout change is:

- a shift in policy (for example, adopting a stable dividend),

- or a one‑off tactical move (for example, a single, opportunistic repurchase).

Worked Example 1.5

Spencer Pharmaceuticals (SPI) has 20 million shares at $50 each. It has $100 million of profits this quarter and plans to reinvest 70%, leaving $30 million to distribute. The board is debating:

- Option 1: pay a $1.50 per‑share dividend;

- Option 2: repurchase $30 million of stock at $50 per share.

Assume no taxes.

Answer:

Option 1: Dividend

- Dividend per share = $30 million / 20 million = $1.50

- Ex‑dividend price approximately = $50 – $1.50 = $48.50

- A shareholder with 1 share holds $48.50 in stock + $1.50 in cash = $50 total wealth.

Option 2: Repurchase

- Shares repurchased = $30 million / $50 = 600,000

- Shares outstanding after = 19.4 million

- Equity value after = $1,000 million – $30 million = $970 million

- Price per share after = $970 million / 19.4 million = $50

- A shareholder with 1 share holds 1 share at $50 = $50 total wealth.

Under perfect‑market assumptions and no tax differences, a $30 million dividend and a $30 million repurchase are economically equivalent for shareholders. This illustrates dividend irrelevance.

Sustainability of Dividends

A high or rising dividend payout ratio may be unsustainable if:

- earnings are volatile or declining,

- free cash flow to equity is weak (for example, due to high capital expenditures or working capital needs),

- leverage and interest obligations are rising.

Dividend policies include:

- Stable dividend per share (favored for signaling stability and reducing investor uncertainty),

- Constant payout ratio (dividends fluctuate directly with earnings, which can create volatility in investor income),

- Residual payout (dividends paid after profitable investments are funded, leading to highly variable payouts).

Key Term: stable dividend policy

(re‑emphasized) Firms with this policy tend to increase dividends gradually as earnings grow, smoothing through short‑term earnings volatility.

When assessing sustainability in an exam setting, look for:

- Dividend coverage ratios significantly above 1 (for both dividends alone and total payout),

- Positive and stable FCFE after capital expenditures and working capital needs,

- Reasonable leverage ratios and interest coverage,

- Management statements about maintaining or growing the dividend.

A sudden cut to a long‑standing stable dividend is a strong negative signal and often coincides with liquidity stress, covenant breaches, or a major shift in strategy requiring large investment.

Summary

Capital structure and payout policy decisions affect both valuation metrics and investor perceptions. Dividends and share repurchases are the primary methods to return cash to shareholders, each with unique signaling, tax, and financial effects.

You should be able to:

- classify payouts as regular, special, stock, or liquidating dividends or as repurchases,

- apply dividend policy theories (irrelevance, bird‑in‑the‑hand, tax preference) to predict how changes in payout might affect value under different assumptions,

- quantify the effects of different payout choices on EPS, BVPS, and coverage ratios,

- interpret dividend and repurchase announcements as signals about earnings, risk, and investment opportunities,

- assess whether a given dividend level or buyback program is sustainable in light of FCFE, leverage, and investment needs.

Key Point Checklist

This article has covered the following key knowledge points:

- Main dividend types: regular, special, stock, and liquidating

- Stock splits and reverse splits and their effect on price and ratios

- Dividend policy theories: irrelevance, bird‑in‑hand, tax preference

- Signaling role of dividend changes and repurchase announcements

- Share repurchase methods and their qualitative differences

- Effects of repurchases on EPS, BVPS, leverage, and coverage ratios

- Dividend, total payout, and FCFE coverage ratios for sustainability analysis

- Comparison of stable, constant payout, and residual payout policies

- Economic equivalence of dividends and repurchases under perfect‑market assumptions

- How payout choices influence market perception, required return, and firm value

Key Terms and Concepts

- payout policy

- regular cash dividend

- special (extra) dividend

- liquidating dividend

- stock dividend

- stock split

- reverse stock split

- share repurchase

- book value per share (BVPS)

- dividend irrelevance theory

- bird‑in‑the‑hand theory

- tax preference theory

- signaling

- open‑market share repurchase

- fixed‑price tender offer

- Dutch auction tender

- direct negotiation repurchase

- EPS (Earnings per Share)

- dividend coverage ratio

- payout ratio (dividend payout ratio)

- total payout ratio

- stable dividend policy

- constant payout ratio

- residual dividend policy