Learning Outcomes

This article explains how to identify, distinguish, and quantify the main forms of currency risk—transaction, translation, and economic exposure—and how each affects the valuation of cross‑border assets, liabilities, cash flows, and reported earnings in typical CFA Level II exam scenarios. It explains how to link specific exposures to appropriate hedging tools, including forward contracts, currency options, money‑market hedges, swaps, and operational (natural) hedges, and how to compare their mechanics, payoff profiles, and practical implementation issues. It discusses how to evaluate hedge effectiveness using scenario analysis, and how to weigh hedging benefits against costs, basis risk, accounting implications, and strategic considerations. It also examines how different measurement approaches capture transaction, translation, and economic exposure, and how exam questions may frame these exposures in balance sheet, cash flow, or valuation contexts. Finally, it outlines how to interpret qualitative vignettes describing multinational firms and infer the most suitable hedging approach, or justify leaving positions partially or fully unhedged.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are expected to understand the various dimensions of currency risk that international firms and investors face, with a focus on the following syllabus points:

- Recognize and distinguish the main types of currency risk: transaction, translation, and economic (operating) exposure

- Analyze how currency fluctuations can impact reported financial statements and the true economic value of assets and liabilities

- Evaluate the principal hedging instruments and strategies available for currency risk management

- Assess the costs, limitations, and effectiveness of common hedging approaches

- Determine when and how to apply hedging or leave positions unhedged, based on scenario requirements

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which type of currency exposure is directly linked to cash flows arising from invoiced transactions denominated in a foreign currency?

- a) Transaction exposure

- b) Translation exposure

- c) Economic exposure

- d) Operating exposure

-

True or False? Hedging translation exposure using forward contracts will always eliminate the effect of exchange rate changes on consolidated financial statements.

-

What is a natural hedge in currency risk management and when is it typically appropriate?

-

What are the main costs and limitations associated with currency option hedges?

Introduction

Companies and investors conducting cross-border operations must consider how fluctuations in exchange rates affect the value of their assets, liabilities, revenues, and expenses. Unmanaged currency risk can lead to unpredictable earnings, distorted performance, and valuation errors. This article explains the key sources of currency exposure, the mechanisms through which these exposures influence financial outcomes, and the hedging strategies most frequently encountered on the CFA exam.

Key Term: currency exposure

The sensitivity of a firm's or investor's cash flows, assets, or liabilities to unexpected exchange rate movements.Test Tip: When revising Currency risk exposures and hedging approaches, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

TYPES OF CURRENCY EXPOSURE

Global businesses and investors commonly face three forms of currency risk:

Transaction Exposure

Transaction exposure arises from contractual commitments—such as payables or receivables—in foreign currencies. The risk is that exchange rate movements between contract initiation and settlement date will change the domestic-currency value of future cash flows.

Key Term: transaction exposure

The risk that exchange rate changes between transaction and settlement date will alter the home-currency value of contractually fixed cash flows.

Translation Exposure

Translation exposure, also known as accounting or balance sheet exposure, concerns the impact of currency fluctuations on the reported value of assets, liabilities, revenues, and expenses when consolidating financial statements across currencies.

Key Term: translation exposure

The effect of exchange rate changes on the reported values of foreign-currency-denominated assets, liabilities, and earnings in consolidated financial statements.

Economic Exposure

Economic exposure refers to the effect of exchange rate changes on an entity's expected future cash flows and overall market value, extending beyond direct contractual commitments to capture the sensitivity of operating income and competitive position.

Key Term: economic exposure

The risk that exchange rate movements will impact the present value of future cash flows by altering sales, costs, or competitive conditions.

MEASURING CURRENCY RISK

Assessing currency risk involves identifying the magnitude and timing of exposure:

- For transaction exposure, sum all pending foreign-currency transactions and revalue them at prevailing forward rates.

- For translation exposure, determine the net foreign assets and liabilities subject to remeasurement in consolidation, considering the appropriate accounting method (temporal or current rate).

- For economic exposure, forecast the effect of currency changes on future sales, costs, market share, and ongoing profitability.

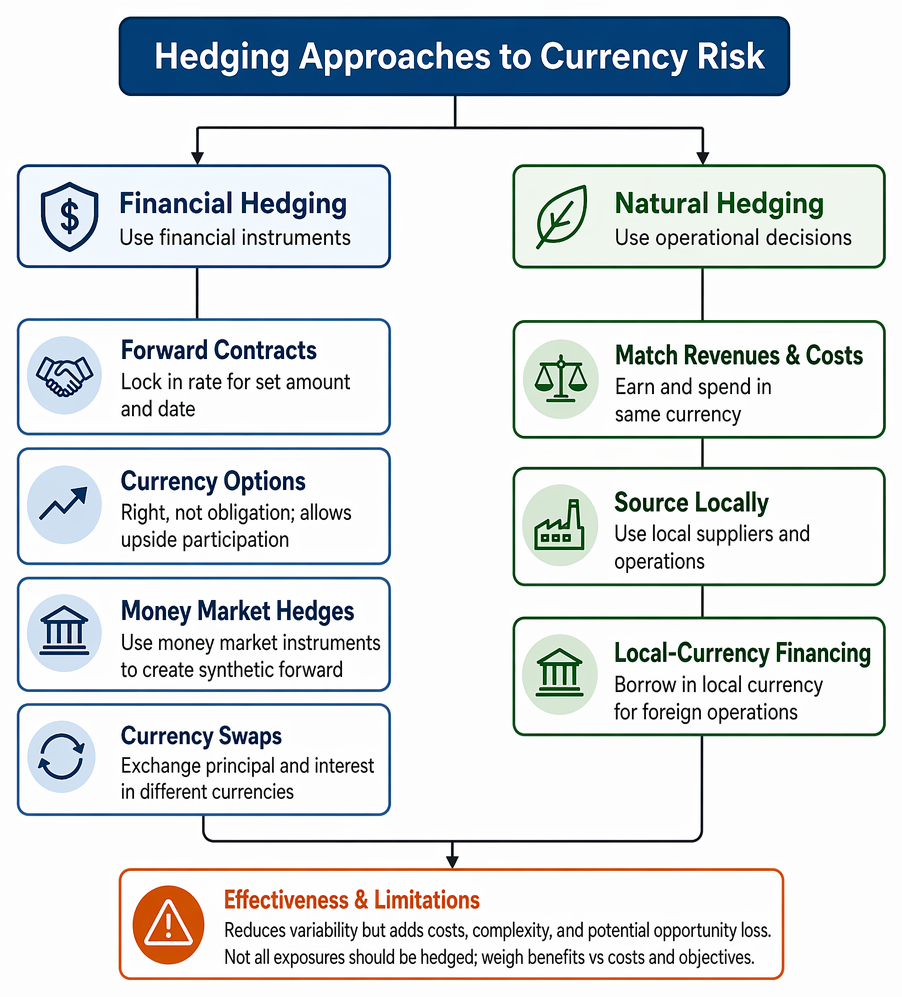

HEDGING APPROACHES TO CURRENCY RISK

A hedge is any action that reduces the variability of value or cash flows due to currency movements.

Measurement approaches for currency exposure distinguish contractual cash flows, translated net assets, and exchange-rate effects on future operating performance.

Financial Hedging Instruments

-

Forward contracts: Lock in the exchange rate for a set amount and date, eliminating transaction risk for committed foreign currency cash flows.

-

Currency options: Provide the right, but not the obligation, to exchange currency at a pre-agreed strike, allowing upside participation if rates move favorably.

-

Money market hedges: Use domestic and foreign money market instruments to synthetically create a forward hedge.

-

Currency swaps: Facilitate exchange of principal and interest in different currencies, often for recurring payments or long-term exposures.

Key Term: forward contract

An agreement obligating the exchange of a specified amount of currency at a fixed rate on a future date. Key Term: currency option

A contract giving the buyer the right, but not the obligation, to exchange a specified amount of currency at a predetermined rate (the strike) within a set period.

Natural Hedging

Operational decisions can offset exposures without derivative use. For example, matching revenues and costs in the same currency, sourcing locally, or financing foreign operations with local-currency debt naturally reduce net exposure.

Key Term: natural hedge

Offsetting currency exposures through operational or balance sheet management decisions rather than financial derivatives.

Hedge Effectiveness and Limitations

Hedging eliminates some risks but introduces others—costs, complexity, or potential opportunity loss (if rates move in a favorable direction). Not all exposures can or should be hedged; judgment is needed to weigh the benefit of reduced volatility against cost, basis risk, or strategic objectives.

Worked Example 1.1

A UK-based exporter agrees to deliver €500,000 of goods to a French customer, with payment due in 90 days. Spot EUR/GBP is 0.8600. Management is concerned about a weaker euro.

Question: How can the exporter hedge this transaction exposure, and what is the effect if the euro depreciates to EUR/GBP 0.8200 at settlement but the hedge was in place?

Answer:

The exporter can enter into a 90-day forward contract to sell €500,000 at the forward rate. If the euro depreciates to 0.8200, the spot value of receivables falls, but the forward contract offsets this loss, locking in the original rate. Cash flows are stabilized.

Worked Example 1.2

A US company has a subsidiary in Japan with net yen assets. How does a stronger yen during the reporting period affect consolidated US financial statements under the current rate method?

Answer:

The increased yen value of net assets, when translated at the stronger yen rate, raises the group’s consolidated equity (via the cumulative translation adjustment in OCI). Translation exposure results in higher group-reported net assets.Exam Warning: Attempting to hedge translation or economic exposures with short-term forwards designed for transaction exposures can produce misleading results and may not be effective in offsetting fundamental value changes in future cash flows.

Summary

Currency fluctuations can materially impact the value of international operations and investments. Effective risk management requires identifying which exposures are most significant and selecting appropriate hedging tools. Transaction exposures are best managed with forwards, options, or natural hedges for committed cash flows. Translation exposures are accounting in nature; the value of hedging them is debatable and depends on financial reporting objectives. Economic exposure is broader, requiring long-term structural approaches and cannot be perfectly hedged through financial instruments alone.

Key Point Checklist

This article has covered the following key knowledge points:

- Define and distinguish transaction, translation, and economic exposures

- Understand implications of each type of exposure for valuation and risk

- Evaluate the use, mechanics, and limitations of forward contracts, currency options, and natural hedges

- Assess when hedging is appropriate, and recognize the residual risks/costs involved

Key Terms and Concepts

- currency exposure

- transaction exposure

- translation exposure

- economic exposure

- forward contract

- currency option

- natural hedge