Learning Outcomes

This article explains multi-stage dividend discount and H-model valuation for equities with non-constant dividend growth, including:

- identifying when multi-stage DDMs or the H-model are appropriate based on a firm’s life-cycle stage and dividend pattern;

- structuring two-stage and three-stage DDMs, specifying explicit high-growth and transition periods, and defining the start of the mature phase;

- calculating forecast dividends, terminal value using the Gordon growth formula, and present value of all cash flows under exam conditions;

- applying the H-model formula, interpreting the role of H, and contrasting linear-growth decline assumptions with stepwise changes;

- reconciling values produced by alternative models and explaining differences arising from growth-rate and horizon assumptions;

- spotting and correcting common computational mistakes, such as misaligning time indices, misusing , or over-extending high growth;

- linking model outputs to CFA Level 2 item-set questions that test valuation, reasonableness of assumptions, and sensitivity to key inputs;

- summarizing the strengths, limitations, and typical exam traps associated with each model to support efficient problem‑solving.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are expected to understand discounted cash flow valuation techniques for equities where dividend growth is non-constant, with a focus on the following syllabus points:

- Recognizing when to use multi-stage dividend discount models (DDMs) or the H-model for a given growth scenario

- Calculating equity value using two-stage, three-stage, or H-model DDMs, including all necessary dividend and terminal value projections

- Explaining growth, transition, and maturity stages, and aligning the correct model to each phase

- Computing and interpreting terminal value in multi-stage models using the Gordon growth approach

- Evaluating the assumptions and potential limitations of each model, especially regarding growth trajectories and transition patterns

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- In which company life-cycle situations is it most appropriate to use the H-model instead of a simple two-stage DDM?

- What does the “H” represent in the H-model, and how does it affect the calculation?

- How is terminal value calculated in a multi-stage DDM, and when should it be used?

- True or false? The H-model assumes a stepwise change from high to low dividend growth at the end of the transition period.

Introduction

Real-world companies rarely experience steady, perpetual dividend growth. Instead, growth typically occurs in distinct phases: an initial period of rapid expansion, a more gradual slowdown, and eventually a stable mature phase. Discounted cash flow valuation models must reflect this reality for accurate share valuation. Multi-stage dividend discount models (DDMs) and the H-model are the principal tools CFA Level 2 candidates use to account for these changing patterns of dividend growth.

Key Term: multi-stage dividend discount model (multi-stage DDM)

A present value model that projects different dividend growth rates over multiple periods to reflect high, declining, and stable growth, discounting all projected cash flows to today.Test Tip: When revising Multi-stage dividend discount and h-model, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

GROWTH PHASES AND APPROPRIATE VALUATION MODELS

Dividend growth models accommodate typical firm life cycles:

- Growth phase: Above-average, often double-digit dividend growth due to competitive advantages, innovation, or market expansion.

- Transition phase: Growth slows as market competition rises, advantages erode, and the firm matures.

- Maturity phase: Growth stabilizes at a rate close to that of the broad economy or industry.

The valuation model selected must match the firm's anticipated growth trajectory:

- Two-stage DDM: Dividends grow at an initial, higher rate for N years, then revert to a lower, sustainable rate forever.

- Three-stage DDM: Dividends grow at a high rate, followed by a period of moderate or slowing growth, then mature at a stable rate.

- H-model: Dividend growth declines linearly from a high starting rate to a stable long-term rate over a defined period.

Key Term: terminal value

The present value, at the end of the explicit forecast period, of all future dividends assuming perpetual stable growth—normally estimated using the Gordon growth formula.

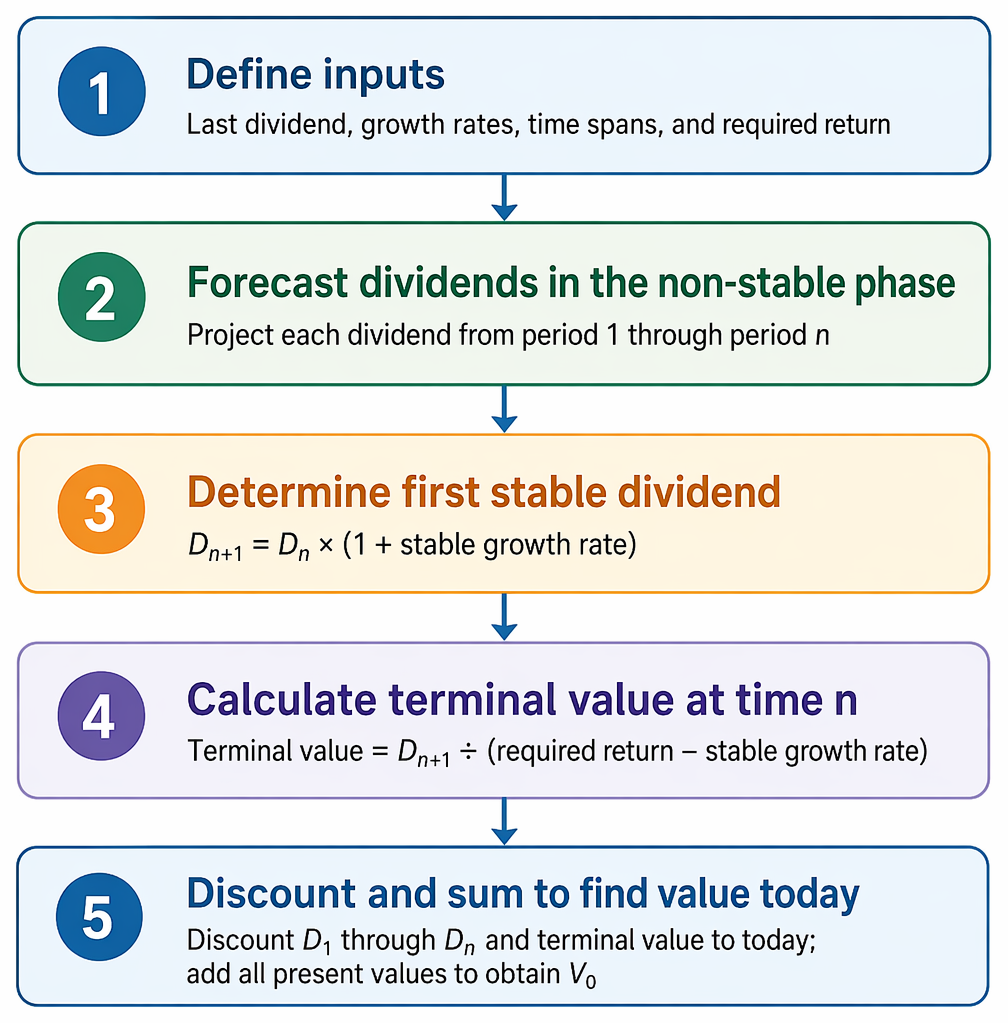

MULTI-STAGE DDM: STRUCTURE AND USE

The two-stage and three-stage DDMs require explicit projection of dividends for each period of non-constant growth, then the present value of all future stable-growth dividends is captured via a terminal value.

Worked Example 1.1

A company just paid a $2.50 dividend. Dividends are expected to grow at 10% for four years, then at 4% indefinitely. The required return is 8%. What is the fair value per share?

Answer:

D_1 &= 2.50 \times 1.10 = 2.75 \\ D_2 &= 2.75 \times 1.10 = 3.03 \\ D_3 &= 3.03 \times 1.10 = 3.34 \\ D_4 &= 3.34 \times 1.10 = 3.67 \end{aligned}$$ Step 2: Terminal value at t=4 $$> \begin{aligned} D_5 &= 3.67 \times 1.04 = 3.82 \\ TV_4 &= 3.82 / (0.08 - 0.04) = 95.50 \end{aligned}$$ Step 3: Discount all cash flows to present $$> V_0 = \frac{2.75}{1.08} + \frac{3.03}{1.08^2} + \frac{3.34}{1.08^3} + \frac{3.67 + 95.50}{1.08^4}$$ $$= 2.55 + 2.61 + 2.65 + 73.54 = \$81.35$$ **Key Term: two-stage dividend discount model** A valuation model projecting one period of above-normal growth, then a perpetual mature-growth phase with a different rate.

Step 1: Forecast dividends

THE H-MODEL

The H-model provides a shortcut to estimate value when dividend growth is expected to decline at a constant, steady rate rather than abruptly. It avoids the need to project each dividend individually during the transition.

Two-stage and three-stage DDM workflow projects nonconstant dividends, estimates terminal value at stable growth, and discounts cash flows to V0.

Key Term: H-model

A DDM assuming dividend growth declines linearly from a high initial rate to a stable rate over a transition period, allowing a single formula valuation. Key Term: H (in H-model)

Half the length (in years) of the transition from high growth to stable growth (H = N/2 if the transition period is N years).

The H-model formula is:

Where:

- = value today

- = most recent dividend

- = initial short-term (high) dividend growth

- = long-term stable growth

- = required return

- = half the transition period (years)

The first term is the present value of a stable-growth stock (as in the Gordon model), and the second term adjusts for value created during the period when growth is above the long-term rate.

Worked Example 1.2

A firm has just paid a $1.20 dividend. Dividends are expected to grow at 12% initially, falling linearly to a stable 5% growth over the next 6 years, then grow at 5% perpetually. The required return is 9%. What is the value per share using the H-model?

Answer:

g_S = 12%, g_L = 5%, H = 6/2 = 3

TERMINAL VALUE IN MULTI-STAGE DDM

Terminal value is used when, after a period of forecasted (usually non-constant) growth, dividends are assumed to settle into stable growth. The terminal value at the end of the high-growth period is:

Where = first dividend in the stable-growth phase.

Worked Example 1.3

You forecast dividends for eight years. The final forecasted dividend, , is $4.00. After year 8, dividends grow at 4%; the cost of equity is 10%. What is the terminal value at ?

Answer:

Key Term: terminal value

The present value of all future dividends from a specified future date onward, assuming perpetual stable growth. Usually estimated via Gordon's model.

COMPARISON OF MULTI-STAGE DDM AND H-MODEL

- Multi-stage DDMs accommodate detailed, uneven dividend growth assumptions but require explicit forecasting for each year of non-stable growth.

- The H-model offers a practical alternative for gradual, linear declines in growth. It is a shortcut—not a substitute when complex, non-linear, or stepwise transitions are expected.

- Model choice should mirror the realistic dividend growth expectations for the company and the information available.

Exam Warning: A frequent exam pitfall in the H-model is mis-calculating H (it is always half the transition period). Also, avoid applying the starting (high) growth rate to the entire terminal value—only use the stable rate once the transition is complete. Carefully check all denominator expressions: r - g_L.

Summary

Understanding growth phases and the right model choice is essential. Multi-stage DDMs require clear explicit projections when growth patterns are complicated. The H-model offers a simplified approach for scenarios with steadily decaying growth. Terminal value calculations are essential and always use the long-term stable rate. The chosen model should faithfully represent the company's dividend trajectory and simplify calculations where appropriate.

Key Point Checklist

This article has covered the following key knowledge points:

- The multi-stage DDM and the H-model estimate equity value for non-constant dividend growth.

- Identify the firm growth stage (growth, transition, maturity) to select the correct model.

- Two-stage and three-stage DDMs require explicit dividend and terminal value projections.

- The H-model applies linear transition from high to stable growth without year-by-year forecasting.

- Terminal value is found using the Gordon growth formula at the start of the mature-growth phase.

- The H in H-model is always half the length of the decline period.

- Carefully match the model used to the actual expected dividend behavior of the stock.

Key Terms and Concepts

- multi-stage dividend discount model (multi-stage DDM)

- terminal value

- two-stage dividend discount model

- H-model

- H (in H-model)