Learning Outcomes

This article explains how fiscal, monetary, and exchange rate policies interact across the business cycle, including:

- distinguishing between expansionary and contractionary fiscal and monetary stances and linking them to aggregate demand, output, and inflation;

- evaluating how different exchange rate regimes (floating, fixed, and managed) modify the transmission of policy actions to growth, prices, and employment;

- assessing how capital mobility and openness of the economy affect the relative power of fiscal versus monetary policy;

- analyzing standard policy combinations (e.g., loose–loose, tight–tight, fiscal–monetary mix) and predicting their likely effects on GDP, inflation, and the external balance;

- explaining the policy trilemma and its implications for a country’s ability to pursue exchange rate targets, free capital flows, and independent monetary policy simultaneously;

- identifying conditions under which expansionary policies may backfire through currency depreciation, imported inflation, or crowding out of private activity;

- recognizing the risks of policy misalignment, such as currency crises, loss of credibility, and destabilizing capital flows;

- applying these frameworks to interpret scenario-based questions, including those with shifting global interest rates or sudden stops in capital flows;

- interpreting CFA-style vignettes that describe policy decisions and determining the most consistent macroeconomic outcomes for output, inflation, and exchange rates;

- contrasting short-run (Mundell–Fleming) and longer-run (monetary and portfolio-balance) approaches on how fiscal and monetary stances influence exchange rates.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are required to understand the relationships between policy actions and macroeconomic growth, with a focus on the following syllabus points:

- Describing how fiscal, monetary, and exchange rate policies interact to affect growth, inflation, and the business cycle

- Explaining the effect of different policy combinations (e.g., expansionary fiscal/monetary, floating/fixed exchange rates)

- Assessing policy limitations and trade-offs, especially in open economies

- Identifying risks of policy misalignment (e.g., currency crises, inflation, recession)

- Evaluating policy influences on exchange rates and capital flows

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

Vignette: Country A is a small open economy with a freely floating exchange rate and highly mobile capital. Growth is weak, inflation is below target, and unemployment is high. The government announces a temporary fiscal stimulus financed by borrowing, while the central bank cuts its policy rate and signals that rates will stay low. International investors view Country A as politically stable with credible institutions.

-

Under the Mundell–Fleming framework, what is the most likely combination of short-run outcomes for Country A?

- a) Higher GDP, lower inflation, and currency appreciation

- b) Higher GDP, higher inflation risk, and currency depreciation

- c) Lower GDP, lower inflation, and currency depreciation

- d) Higher GDP, lower inflation, and an unchanged exchange rate

-

Still in Country A, which of the following channels is most likely to offset part of the fiscal stimulus under high capital mobility?

- a) Higher domestic interest rates causing capital outflows and currency depreciation

- b) Lower domestic interest rates causing capital inflows and currency appreciation

- c) Higher domestic interest rates causing capital inflows and currency appreciation

- d) Lower domestic interest rates causing capital outflows and currency appreciation

Vignette: Country B pegs its currency to the US dollar, has an open capital account, and is running a large fiscal deficit financed by issuing local-currency debt. Growth is above trend and inflation is rising. The central bank keeps its policy rate below US rates to support government borrowing costs and employment.

-

In the short run, Country B’s policy mix is most likely to lead to:

- a) Capital inflows and increasing foreign reserves

- b) Capital outflows and pressure to devalue the currency

- c) A stronger current account surplus and currency appreciation

- d) Reduced domestic credit growth and falling asset prices

-

Which development would be the clearest sign that Country B’s policies are becoming unsustainable and a currency crisis risk is rising?

- a) Persistent current account surplus and rising foreign exchange reserves

- b) Falling domestic interest rates and lower government bond yields

- c) Rapid loss of foreign exchange reserves and rising external interest spreads

- d) Increasing foreign direct investment in export sectors

Vignette: Country C has low capital mobility due to capital controls and operates a managed float regime. It implements a large, long-lived fiscal expansion, while monetary policy remains neutral. The economy was initially at potential output.

-

In Country C, which combination is most consistent with the likely medium-run effects of the sustained fiscal expansion according to the portfolio-balance approach?

- a) Higher interest rates, persistent capital inflows, and long-run currency appreciation

- b) Lower interest rates, capital outflows, and long-run currency appreciation

- c) Higher risk premium on government debt, concerns about debt sustainability, and eventual currency depreciation

- d) Lower risk premium, improved sovereign credit rating, and currency appreciation

-

Across the three countries, which statement about policy coordination is most accurate?

- a) In Country A, monetary easing is likely to fully neutralize the inflationary effects of fiscal stimulus

- b) In Country B, independent monetary policy, a hard peg, and free capital mobility can be sustained simultaneously with credible policies

- c) In Country C, capital controls relax the trade-off between fiscal expansion and external balance pressures

- d) In all three countries, fiscal policy is always more effective than monetary policy for influencing output

Introduction

Economic growth is shaped by the interaction of fiscal, monetary, and exchange rate policies. Each policy tool can influence key outcomes such as GDP, employment, inflation, external balances, and currency value. However, the effectiveness and consequences of each policy depend on how they are implemented—individually and together—especially across different exchange rate regimes and degrees of capital mobility. A clear understanding of policy interactions is essential for investors, policymakers, and CFA exam candidates because Level II item sets frequently embed multiple policy changes in a single vignette.

Key Term: fiscal policy

Government decisions on spending and taxation aimed at influencing economic activity. Key Term: monetary policy

Central bank actions that affect the money supply and interest rates to steer inflation, output, or employment. Key Term: exchange rate regime

The system adopted by a country to determine its currency’s value relative to others, such as floating, fixed (pegged), or managed float. Key Term: capital mobility

The ease with which financial capital can move in and out of a country. High capital mobility increases sensitivity to interest rate differentials and policy credibility. Key Term: floating exchange rate

A regime in which the exchange rate is determined mainly by market forces, with no pre-announced target and usually only limited intervention. Key Term: fixed exchange rate

A regime where the domestic currency is pegged at a set rate to another currency or basket, and the central bank intervenes as needed to maintain the peg. Key Term: managed float

A regime where the authority does not commit to a strict peg but intervenes to smooth excessive volatility or lean against undesired exchange rate movements.

Open-economy macroeconomics at Level II is framed largely by the Mundell–Fleming model in the short run and by monetary and portfolio-balance approaches in the longer run. These frameworks link policy choices to interest rates, capital flows, and exchange rates, which in turn affect aggregate demand and the business cycle.

Key Term: Mundell–Fleming model

A short-run open-economy framework that analyzes how fiscal and monetary policy affect output and the exchange rate under different exchange rate regimes and degrees of capital mobility, assuming spare capacity and relatively stable inflation.

At a high level:

- Mundell–Fleming focuses on the short-run effect of policy on interest rates, capital flows, and the nominal exchange rate, holding prices and inflation roughly constant.

- Monetary models treat output as fixed in the long run and emphasize how money growth affects inflation and, via purchasing power parity, the trend exchange rate.

- Portfolio-balance models analyze how sustained fiscal deficits and rising public debt alter risk premia, portfolio allocations, and long-run currency values.

Level II questions often require you to:

- Identify which framework is implicitly being used in a vignette.

- Distinguish between short-run cyclical effects on output and the longer-run implications for inflation, debt sustainability, and currency trends.

- Recognize that policy choices today can have opposite effects on the exchange rate in the short run versus the long run.

Key Term: balance of payments (BOP)

The accounting framework summarizing all economic transactions between residents of a country and the rest of the world, including the current account and the capital/financial account.

Understanding how the BOP must balance is important: a current account deficit must be financed by capital inflows (a financial account surplus) or a weakening of the currency that improves competitiveness. Policy choices affect both sides of the BOP and thus the exchange rate.

The rest of this article develops these ideas systematically, focusing on the policy mix, the exchange rate regime, and capital mobility.

Test Tip: When revising Policy interactions fiscal monetary and exchange rate, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Exam Warning: Do not rely on keyword recognition alone; check the precise condition, exception, calculation step, or evidence the question requires.

The Policy Mix: Coordinated and Conflicting Actions

Economic outcomes depend not just on individual policy choices but on how policies affect each other and the wider economy. The “policy mix” refers to the combination of fiscal and monetary stances, implemented within a given exchange rate and capital-flow environment.

Common combinations include:

- Expansionary fiscal with expansionary monetary (loose–loose)

- Contractionary fiscal with contractionary monetary (tight–tight)

- Expansionary fiscal with tight monetary

- Tight fiscal with easy monetary

Their impact differs markedly under floating versus fixed exchange rates and under high versus low capital mobility.

Fiscal and Monetary Policy in Tandem

Fiscal and monetary authorities may aim for similar objectives—stimulating growth, limiting inflation, or supporting employment—but their tools act via different transmission channels and time horizons.

- Expansionary fiscal policy (increased government spending, lower taxes) aims to boost aggregate demand directly through higher public demand and higher disposable income for households.

- Expansionary monetary policy (lower policy rates, asset purchases, liquidity injections) works by reducing borrowing costs and easing financial conditions, encouraging consumption, investment, and often asset-price appreciation.

When both policies are expansionary:

- Aggregate demand typically rises strongly.

- Output and employment tend to increase, especially if there is slack in the economy.

- Inflationary pressures build as the economy approaches or exceeds potential output.

- Interest rates are pushed down by monetary policy but up by higher government borrowing; the net effect depends on the relative strength of each.

In a closed economy, the loose–loose mix is usually very powerful for short-run growth but risks overheating and higher inflation expectations. In an open economy, the exchange rate and capital flows can either strengthen or offset domestic effects.

Conversely, when both policies are restrictive (tight–tight), aggregate demand falls, helping to control inflation or correct external imbalances but at the cost of slower growth or recession.

In practice, fiscal and monetary authorities may pursue:

- A stabilizing mix, where one policy leans against the other (tight fiscal with easy monetary or vice versa) to achieve both internal balance (full employment with low inflation) and external balance (sustainable current account).

- A pro-cyclical mix, where both policies move in the same direction as the cycle (looser in booms, tighter in recessions), often due to political constraints, which can intensify business cycles and raise crisis risk.

Exam vignettes often describe a policy mix without spelling out whether it is pro- or counter-cyclical. You must infer that from the output gap, inflation, and external position.

Within the Mundell–Fleming framework:

- Under floating rates with high capital mobility, monetary policy is the dominant tool for managing output, while fiscal policy becomes less effective due to offsetting exchange rate movements.

- Under fixed rates with high capital mobility, fiscal policy is powerful, and independent monetary policy is largely lost because it must support the peg.

Contrasting Policy Mixes Across the Cycle

To apply this on the exam, it is useful to mentally benchmark the four main combinations:

-

Loose fiscal + loose monetary

- Strong demand stimulus.

- Under floating rates and high capital mobility, the interest-rate impact is ambiguous, but if markets expect low real rates, the currency tends to depreciate, adding net-export support and imported inflation.

- Under a fixed rate with open capital, the mix is usually inconsistent with the peg unless the anchor country is also very loose.

-

Tight fiscal + tight monetary

- Strong demand contraction.

- Under floating rates, higher real rates attract capital and appreciate the currency, hurting net exports but reinforcing disinflation.

- Under fixed rates, this mix is often used as a crisis response to defend the currency and restore external balance, at the cost of recession.

-

Loose fiscal + tight monetary

- Often deployed when government wants to support aggregate demand but the central bank is focused on inflation.

- Under floating rates and high mobility, higher interest rates attract inflows and appreciate the currency, crowding out net exports. Domestic demand may be little changed, but the composition of demand shifts from traded to non-traded sectors.

- This mix is consistent with disinflation and sometimes describes early stages of “austerity” plus monetary tightening.

-

Tight fiscal + loose monetary

- Used, for example, when governments consolidate debt while central banks support activity.

- Under floating rates and high mobility, lower rates tend to weaken the currency, boosting net exports and partially offsetting the fiscal drag.

- This is broadly the “expansionary monetary, restrictive fiscal” combination that Mundell–Fleming associates with depreciation.

A common Level II task is to take such a mix, combine it with a specified regime and capital mobility, and deduce:

- The direction of GDP and unemployment.

- The likely change in inflation pressure.

- The direction of the exchange rate.

- The effect on the current and capital accounts.

Exchange Rate Considerations

The ability of monetary and fiscal policies to achieve growth or stabilization targets depends heavily on the exchange rate regime and capital mobility.

-

Floating exchange rate

- Currency value is determined by market forces.

- Monetary policy is most effective: changes in interest rates drive capital flows and exchange rate movements that adjust net exports.

- Fiscal policy may be partly neutralized by induced currency appreciation or depreciation.

-

Fixed exchange rate

- Currency is pegged to another major currency or basket.

- Monetary independence is restricted; the central bank must adjust its balance sheet to maintain the peg, often aligning domestic rates with those of the anchor currency.

- Fiscal policy changes can be amplified or constrained by the need to defend the peg.

-

Managed float

- Authorities have some room to use both monetary and fiscal tools while smoothing exchange rate extremes.

- Persistent policy–exchange-rate inconsistencies will still generate pressure, forcing either a policy shift or a regime change.

Exchange rate responses are closely linked to capital-flow behavior. With high capital mobility, interest rate differentials quickly trigger cross-border flows that move the exchange rate and the balance of payments.

Key Term: uncovered interest rate parity (UIP)

A condition stating that the expected percentage change in the exchange rate between two currencies equals the interest rate differential between them; it is not enforced by arbitrage and typically holds, if at all, only in the long run.

Under UIP, if is the interest rate in country A and in country B, the expected percentage change in the rate is approximately:

By contrast, in Mundell–Fleming:

- Real interest rates can differ across countries.

- Higher domestic interest rates (relative to foreign) attract capital and appreciate the the currency in the short run.

- Uncovered interest parity does not have to hold; the interest differential may reflect both expected depreciation and a risk premium.

The curriculum explicitly warns that candidates are often confused by these conflicting implications. The key is:

- UIP assumes equal real rates and that nominal differences stem from expected inflation (so high nominal rates signal expected depreciation).

- Mundell–Fleming ignores inflation and treats higher domestic real rates as attracting capital and causing appreciation.

You must infer, from context, whether higher interest rates are due primarily to a monetary tightening (Mundell–Fleming, short run) or to higher inflation expectations (UIP/monetary approach, long run).

Policy Interactions in Open and Closed Economies

The Mundell–Fleming model highlights the role of capital mobility. Two polar cases are especially relevant for exam questions.

Open economy, high capital mobility, floating exchange rate

-

Expansionary monetary policy

- Lowers domestic interest rates.

- Triggers capital outflows as investors seek higher returns abroad.

- Domestic currency depreciates.

- Net exports rise, reinforcing the monetary stimulus.

-

Expansionary fiscal policy

- Raises aggregate demand and often pushes interest rates higher.

- Higher rates attract capital inflows.

- Currency appreciates.

- Net exports fall, partially offsetting the fiscal stimulus.

In this environment, monetary policy is powerful for output stabilization; fiscal policy is weaker because exchange rate appreciation crowds out net exports.

Key Term: current account

Part of the balance of payments that records trade in goods and services, net investment income, and unilateral transfers between a country and the rest of the world. Key Term: capital (financial) account

Part of the balance of payments that records cross-border flows of financial capital, including portfolio investment and foreign direct investment.

From a balance-of-payments view:

- Monetary easing tends to worsen the financial account (capital outflows) but improve the current account (via depreciation).

- Fiscal expansion tends to improve the financial account (capital inflows) but worsen the current account (via appreciation and higher imports).

A useful way to think about this in an exam scenario is:

- Ask: “Which account (current vs capital) is the main channel?” With high capital mobility, capital flows dominate.

- Determine the direction of the policy-induced interest rate change.

- Infer the direction of capital flows and the exchange rate.

- Then infer the impact on net exports and aggregate demand.

Open economy, high capital mobility, fixed exchange rate

Under a credible peg:

- The central bank must buy or sell its currency to keep the exchange rate at the target.

- Expansionary monetary policy that pushes domestic rates below foreign rates would cause capital outflows and depreciation pressure. To maintain the peg, the central bank must sell foreign reserves and contract the money supply, undoing the initial easing. Independent monetary policy is effectively impossible.

- Expansionary fiscal policy that raises domestic interest rates attracts capital inflows and puts upward pressure on the currency. To defend the peg, the central bank must buy foreign assets and expand the money supply, reinforcing the fiscal expansion.

Thus, with a fixed rate and high capital mobility, fiscal policy is potent, and monetary policy becomes endogenous to the peg.

Exam-style implications:

- If a vignette describes a country with a hard peg and open capital account, and shows the central bank cutting rates below the anchor’s rate without large capital controls or reserve changes, you should question the sustainability of that stance.

- A “conflict” between the peg and domestic monetary goals is a classic setup for a currency crisis question.

Low capital mobility or more closed economy

Where capital flows are restricted or small relative to trade:

- Interest rate differentials matter less for capital movements.

- Trade (goods and services) flows become the main driver of exchange rate changes.

- Both expansionary fiscal and monetary policies tend to increase imports and widen the current account deficit, putting downward pressure on the currency.

- Restrictive policies reduce imports and may support currency appreciation.

The textbook summary (for exchange rate direction) is:

-

High capital mobility:

- Expansionary monetary, restrictive fiscal → depreciation

- Restrictive monetary, expansionary fiscal → appreciation

- Loose–loose or tight–tight → ambiguous currency effect

-

Low capital mobility:

- Loose–loose → depreciation

- Tight–tight → appreciation

- Mixed stances → ambiguous

This summary corresponds to the qualitative version of the Mundell–Fleming “policy matrix” you see in the curriculum. In a vignette, once you identify the appropriate box in this matrix, the currency direction usually follows.

Worked Example 1.1

A country runs an expansionary fiscal policy and a simultaneous easy monetary policy, while maintaining a floating exchange rate and high capital mobility. What is the likely effect on GDP, inflation, and the exchange rate?

Answer:

The dual stimulus boosts aggregate demand, so GDP rises and unemployment falls. If spare capacity is limited, inflation pressures increase. The monetary easing tends to lower interest rates and weaken the currency via capital outflows, while fiscal expansion tends to raise rates and strengthen the currency. With high capital mobility, these interest rate effects can offset each other, making the net exchange rate impact uncertain. If markets believe the central bank will prioritize growth and keep rates low, depreciation is more likely, adding imported inflation but supporting net exports.

Policy Dilemmas: The Trilemma

Key Term: policy trilemma (impossible trinity)

The principle that a country cannot simultaneously maintain a fixed exchange rate, free capital movement, and an independent monetary policy. Only two of the three are feasible in the long run.

Governments must choose two out of three:

- Full capital mobility

- Fixed exchange rate

- Independent monetary policy

Attempting all three creates arbitrage opportunities and credibility problems. For example:

- A country with a hard peg and open capital account must align its interest rates with the anchor currency; otherwise, capital flows will force either reserve losses or currency appreciation.

- A country wanting independent monetary policy and free capital flows must allow its exchange rate to float.

- A country that wants both a peg and monetary independence must impose capital controls.

You can think of three “corner solutions” corresponding to real-world regimes:

- Monetary union or currency board: fixed exchange rate and free capital mobility, but no independent monetary policy (e.g., euro area members relative to the ECB, or Hong Kong’s currency board relative to the US dollar).

- Inflation-targeting float: free capital mobility and independent monetary policy, but no fixed exchange rate (e.g., UK, Canada).

- Peg with capital controls: fixed or tightly managed exchange rate and some domestic monetary autonomy, but restrictions on capital flows (e.g., several emerging markets during transition periods).

Worked Example 1.2

A central bank keeps its interest rates low to stimulate domestic growth under a fixed exchange rate and open capital account. Foreign interest rates rise. What is the likely outcome?

Answer:

Higher foreign rates widen the interest differential. Investors shift funds abroad for higher returns, creating capital outflows and downward pressure on the domestic currency. To defend the peg, the central bank must sell foreign reserves and raise domestic interest rates toward foreign levels, directly conflicting with its domestic growth objective. If reserves are insufficient or markets doubt the commitment to the peg, the country may be forced into devaluation or a regime change. This is a classic example of the policy trilemma.

Exchange Rate Policy and Policy Effectiveness

The exchange rate regime shapes the effectiveness and side effects of policy actions.

-

Expansionary monetary policy

-

Under floating rates:

- Tends to depreciate the currency.

- Boosts net exports and growth but can generate imported inflation (via higher import prices) and potentially unanchor inflation expectations.

-

Under fixed rates with open capital:

- Not sustainable as an independent tool; defending the peg forces the central bank to reverse the expansion.

- The only way to maintain a looser stance is to restrict capital mobility.

-

-

Contractionary monetary policy

-

Under floating rates:

- Raises interest rates, attracting capital inflows and appreciating the currency.

- Lowers inflation but can worsen the trade balance and reduce output in export sectors.

-

Under a peg:

- Often used precisely to defend the currency in the face of outflow pressure.

- If rates must rise sharply, recession and financial stress may follow.

-

-

Expansionary fiscal policy

-

Under floating rates and high capital mobility:

- Can raise interest rates and appreciate the currency, crowding out net exports.

- Output gains are smaller than in a closed economy.

-

Under fixed rates and high capital mobility:

- Attracts inflows, forcing monetary expansion to maintain the peg.

- Yields a strong short-run boost to output, but at the cost of higher inflation and often rising external imbalances.

-

Key Term: monetary approach to exchange rates

A long-run framework where output is assumed fixed and monetary policy mainly affects price levels; under purchasing power parity, faster money growth leads to higher inflation and proportional currency depreciation. Key Term: portfolio-balance approach

A long-run framework emphasizing how sustained fiscal deficits and rising public debt affect investor portfolios, risk premia, and, ultimately, the currency’s value.

In more detail:

- Monetary models come in two main versions:

- Under a “pure” monetary model, purchasing power parity (PPP) is assumed to hold continuously, and any permanent increase in the money supply leads to an equiproportionate increase in the price level and a proportional currency depreciation.

- Under the Dornbusch overshooting model, prices are sticky in the short run, so an expansionary monetary shock causes the currency to depreciate more than its eventual PPP-consistent level. Over time, as prices rise, the currency gradually re-appreciates toward its long-run equilibrium.

Key Term: Dornbusch overshooting

A dynamic adjustment process in which a monetary expansion causes the exchange rate to depreciate more than its long-run PPP level in the short run, followed by gradual appreciation back toward equilibrium as prices adjust.

- Portfolio-balance models analyze how changes in the stock of government debt and its perceived risk alter required yields and the currency. A persistent fiscal deficit can:

- Initially attract inflows and support the currency due to higher yields.

- Later weaken the currency if investors become concerned about debt sustainability and demand a higher risk premium.

Short run (Mundell–Fleming):

- Focuses on how fiscal and monetary policy affect interest rates, capital flows, and the exchange rate, assuming spare capacity and relatively stable prices.

Long run (monetary and portfolio-balance approaches):

- Emphasize that:

- Excessive monetary expansion raises inflation and leads to trend currency depreciation.

- Sustained fiscal deficits may initially support the currency (via higher yields and inflows) but eventually raise default and inflation risk, leading to a higher risk premium and potential depreciation.

This short-run versus long-run contrast is frequently tested: the same policy (e.g., fiscal expansion) can have opposite implications for the exchange rate across horizons.

Worked Example 1.3

A country with a floating exchange rate and high capital mobility embarks on a long-lasting, debt-financed fiscal expansion. Initially, monetary policy is neutral and inflation is low. Over several years, investors become increasingly concerned about rising public debt. How do short-run and long-run models interpret the currency impact?

Answer:

In the short run, Mundell–Fleming suggests that higher deficits raise domestic interest rates, attract capital inflows, and appreciate the currency, partially crowding out net exports. However, in the longer run, the portfolio-balance approach highlights that rising public debt increases perceived sovereign risk. Investors eventually demand a higher risk premium or reduce exposure, prompting capital outflows and currency depreciation. Thus, fiscal expansion may appreciate the currency in the short run but weaken it in the long run if debt becomes unsustainable.

Balance of Payments Channels and Capital Flows

The balance of payments (BOP) records all transactions between residents and the rest of the world. Its main components are:

- The current account (trade in goods and services, factor income, transfers)

- The capital/financial account (cross-border financial flows)

BOP accounting implies that a current account deficit must be financed by a capital account surplus (net capital inflows), or, if flows are insufficient, by a currency depreciation that improves competitiveness.

Current account deficits can weaken the currency through several mechanisms:

- Flow supply–demand mechanism: Imports exceeding exports increase supply of domestic currency in FX markets, putting downward pressure on its value. A weaker currency can, over time, restore balance by making exports more competitive and imports more expensive, subject to demand elasticities.

- Portfolio-balance mechanism: Surplus countries accumulate claims on deficit countries. If they later rebalance portfolios (e.g., reduce holdings of deficit-country assets), they may sell the currency, further depressing it.

- Debt sustainability mechanism: If current account deficits are financed by borrowing, rising external debt relative to GDP can eventually trigger concerns about sustainability, leading to sharper depreciation.

Key Term: current account deficit

A situation where a country’s imports of goods, services, and income exceed its exports, requiring net capital inflows or currency depreciation to finance the gap.

Capital account flows:

- Higher relative real interest rates or growth prospects attract capital inflows and support the currency.

- Excessive inflows, especially into emerging markets, can create problems:

- Overvalued real exchange rate

- Asset-price bubbles and credit booms

- Vulnerability to sudden stops in capital flows

Key Term: sudden stop

An abrupt reversal of capital inflows into a country, often triggered by a loss of investor confidence, global risk aversion, or policy misalignment, typically accompanied by sharp currency depreciation and output contraction.

Governments often respond with capital controls or central bank intervention to manage these risks.

Key Term: capital controls

Regulatory measures that limit or tax cross-border capital movements, used to influence capital flows, protect the financial system, or preserve monetary autonomy.

Capital controls can:

- Reduce the sensitivity of capital flows to interest differentials.

- Give policymakers more room to pursue an independent monetary stance under a managed or fixed exchange rate.

- However, they can also:

- Distort investment decisions.

- Encourage circumvention through offshore or derivative channels.

- Lose effectiveness over time if not supported by credible macro policies.

Worked Example 1.4

An emerging market with a floating currency, high domestic real interest rates, and strong growth attracts large short-term portfolio inflows. Fiscal policy is somewhat expansionary, and monetary policy is only mildly restrictive. What are the likely macro and currency implications?

Answer:

High real yields and favorable growth prospects attract capital, causing currency appreciation. The stronger currency worsens the current account by making exports less competitive and imports cheaper, while capital inflows fuel domestic credit growth and asset prices. In the short run, GDP may remain strong, but the economy becomes vulnerable to a reversal in sentiment. If global risk appetite falls or domestic imbalances build (credit boom, asset bubbles), a sudden stop in inflows can trigger sharp depreciation, higher inflation, and a growth downturn.

Interest Parity, Inflation, and Policy

Although the main focus in this reading is on policy mixes and the Mundell–Fleming model, Level II candidates are also expected to be familiar with the parity conditions that link interest rates, inflation, and expected exchange rate changes. These conditions provide a bridge to the monetary and portfolio-balance approaches.

Key Term: purchasing power parity (PPP)

A theory stating that exchange rates adjust over time so that identical goods cost the same in different countries when priced in a common currency; in relative form, it links expected exchange rate changes to inflation differentials.

In relative PPP, the expected percentage change in the exchange rate is approximately:

where and are the inflation rates in countries A and B.

Key Term: real interest rate parity

The condition that, with free capital mobility, real interest rates across countries tend to equalize, as capital flows toward higher real returns. Key Term: international Fisher relation

A relationship stating that the difference between two countries’ nominal interest rates equals the expected inflation differential between them.

Formally, if real interest rate parity and the Fisher relation hold, then:

where and are nominal rates and denotes expected inflation.

Combining PPP, real interest parity, and the Fisher relation gives a chain linking:

- Monetary policy (which affects nominal interest rates and, in the long run, inflation)

- Expected inflation differentials

- Expected exchange rate changes

Exam applications:

- If the vignette is clearly long-run in nature (e.g., 5–10 years out, fully flexible prices), PPP and the monetary approach give you the sign of long-run currency trends.

- If it is short-run and about cyclical stabilization, Mundell–Fleming dominates, and interest differentials mainly drive capital flows and current exchange rate moves.

Being able to switch mental models depending on the horizon is an important Level II skill.

Carry Trades, Volatility, and Policy Regimes

Key Term: FX carry trade

A strategy in which an investor borrows in a low-yielding currency (funding currency) and invests in a higher-yielding currency, profiting if the high-yield currency does not depreciate by the interest rate differential.

In a carry trade, the expected excess return (ignoring transaction costs) is:

where is the realized percentage change in the investment currency against the funding currency.

Carry trades are profitable only when uncovered interest parity fails over the horizon considered. They:

- Tend to perform well in periods of low volatility and strong risk appetite (“search for yield”).

- Can intensify the effects of monetary policy:

- Very low policy rates in advanced economies encourage borrowing in those currencies and investment into higher-yielding emerging-market currencies.

- This can drive large capital inflows, appreciations, and credit booms in recipient countries.

However, carry trades are subject to crash risk:

- When risk sentiment turns, many investors try to unwind simultaneously.

- High-yielding currencies can experience sharp depreciation.

- Central banks in recipient countries may respond with:

- Higher interest rates to stem depreciation, tightening domestic conditions.

- Capital controls or macroprudential measures to reduce inflow volatility.

Vignettes may indirectly allude to carry-trade dynamics by describing:

- Wide interest differentials.

- Large speculative inflows into local bond markets.

- Vulnerability to global “risk-off” episodes.

You should be able to link this back to the policy mix (e.g., sustained loose monetary policy in reserve-currency countries) and to the risks of sudden stops for high-yield emerging markets.

Policy Misalignment and Associated Risks

When fiscal and monetary policies work against each other, or run counter to exchange rate commitments, several risks arise:

- Currency crises

- Occur when defending a peg or a target band becomes untenable.

- Often preceded by:

- Overvalued real exchange rate

- Rapid loss of foreign exchange reserves

- Rising inflation and excessive credit growth

- Large current account deficits and short-term external debt

- A fixed or tightly managed nominal exchange rate that is not adjusted despite changing fundamentals

Key Term: currency crisis

A situation where a currency experiences a sharp depreciation or a forced devaluation, often after speculative attacks and loss of foreign reserves, usually linked to inconsistent policies or weak fundamentals.

-

Loss of credibility

- Inconsistent or opportunistic policy mixes can unanchor inflation expectations and increase risk premia.

- Once credibility is damaged, larger policy moves are needed to regain control (e.g., very high interest rates to defend the currency).

- Risk premia show up as widening sovereign spreads, falling demand for domestic-currency debt, and downward pressure on the currency.

-

Inflation spikes or recessions

- Excessive expansionary policies may trigger inflation surges and abrupt tightening later.

- Aggressive defense of a peg (through high rates and fiscal tightening) can cause deep recessions, banking stress, and political backlash.

-

Distorted capital flows and asset bubbles

- Prolonged negative real rates or implicit FX guarantees can encourage leverage and speculative carry trades.

- The unwind of such positions can be disorderly, with sharp exchange rate moves and asset-price falls.

Key Term: overvalued real exchange rate

A situation where a country’s price level (adjusted for the nominal exchange rate) is high relative to trading partners, often reflected in sustained current account deficits and loss of competitiveness.

From an exam standpoint, always assess:

- Whether fiscal, monetary, and exchange rate policies are mutually consistent.

- Whether the policy mix is sustainable given capital mobility, external balances, and institutional credibility.

- How a change in global conditions (e.g., higher US rates) would transmit through capital flows and exchange rates.

Worked Example 1.5

A country maintains a fixed exchange rate, has open capital markets, and runs a large, persistent fiscal deficit during a credit boom. Inflation rises above that of the anchor currency, and the real exchange rate becomes increasingly overvalued. The central bank keeps rates low to support growth. Which outcome is most consistent with this policy misalignment?

Answer:

The combination of a fiscal deficit, low interest rates, rising inflation, and an overvalued real exchange rate is inconsistent with a fixed nominal peg and open capital account. Investors recognize that the currency is overvalued and that real returns are deteriorating. Capital outflows begin, reserves fall, and the central bank faces a choice between sharply higher interest rates (to defend the peg) or abandoning the peg. If reserves are insufficient or political willingness to tighten is low, a currency crisis with forced devaluation is likely.

Worked Example 1.6

Country D operates a managed float with moderate capital controls. It has been running a tight fiscal policy to reduce debt, while the central bank has cut policy rates aggressively to support growth. The current account is in small deficit, and reserves are stable. How does this policy mix affect macro outcomes and crisis risk?

Answer:

Tight fiscal policy reduces domestic demand and debt accumulation, while loose monetary policy supports private spending and lowers borrowing costs. Under a managed float with capital controls, interest-rate differentials generate some capital flows but less than under full mobility. The easier monetary stance tends to weaken the currency, improving net exports and partially offsetting fiscal drag. Stable reserves and only a small current account deficit suggest that the exchange rate is broadly consistent with fundamentals. Overall, this mix supports internal balance (moderate growth, controlled debt) and external balance, with relatively low crisis risk, provided inflation remains anchored.

Worked Example 1.7

Country E has a floating exchange rate and high capital mobility. Inflation has been persistently above target, but the output gap is small. The central bank unexpectedly hikes its policy rate sharply and signals a strong anti-inflation stance. According to:

- (i) Mundell–Fleming, and

- (ii) uncovered interest rate parity and the monetary approach

what are the likely short-run and long-run directions of the currency?

Answer:

(i) In the short run under Mundell–Fleming, the higher domestic interest rate attracts capital inflows. With high capital mobility and a floating rate, this leads to an appreciation of the currency. Output may weaken, especially in interest-sensitive and export sectors, but the stronger currency helps reduce inflation via cheaper imports. (ii) In the longer run, if the tighter monetary stance credibly lowers expected inflation, the monetary approach implies that the domestic price level grows more slowly than foreign prices. Under PPP, this supports a stronger long-run currency level (less trend depreciation, possibly slight appreciation) than under the previous, more inflationary regime. Thus, both frameworks point in the same direction in this case: tightening that reduces inflation pressure supports the currency in both the short and long run.

Worked Example 1.8

Country F has low capital mobility due to strict controls and a crawling-peg exchange rate that depreciates gradually against a basket. It implements a large, permanent increase in government spending, financed by domestic borrowing, while monetary policy remains neutral. Initially, the economy is at potential output. Using the Mundell–Fleming and portfolio-balance approaches, what are the likely medium-run outcomes?

Answer:

With low capital mobility, the main channel is trade rather than capital flows. The fiscal expansion raises domestic demand and imports, widening the current account deficit and putting pressure for a faster depreciation under the crawling peg. If the central bank accommodates the fiscal expansion over time (for example, to keep interest rates stable), the money supply and inflation tend to increase. From the portfolio-balance approach, a sustained higher deficit raises the stock of government debt and, eventually, investors may demand a higher risk premium or reach exposure limits, especially if domestic savings are insufficient. Over the medium run, the likely outcomes are:

- Higher real interest rates and some crowding out of private investment.

- A weaker currency path than previously planned under the crawl, possibly requiring step devaluations.

- Rising concerns about debt sustainability if growth does not keep up with debt accumulation.

Currency depreciation thus eventually reflects both flow imbalances (current account deficit) and stock concerns (higher public debt).

Capital Controls and Central Bank Intervention

Policy makers sometimes try to smooth or offset market-driven exchange rate moves through:

- Direct intervention in FX markets: buying or selling foreign currency against domestic currency.

- Sterilization: conducting offsetting open-market operations to neutralize the impact of FX intervention on the domestic money supply.

- Capital controls: taxes, quantity limits, or prudential regulations that deter certain types of flows (e.g., short-term debt inflows).

The curriculum emphasizes that:

- In large, liquid FX markets (major currencies), central bank reserves are often too small relative to daily turnover to resist market forces for long.

- In smaller or emerging markets, especially those with large reserves relative to turnover, intervention can have a more persistent impact—provided it is consistent with fundamentals.

- Capital controls can temporarily relieve pressure on the exchange rate and give policymakers more room to reconcile domestic and external objectives, but they are not a substitute for sound macro policies.

From a Level II exam standpoint, when you read about intervention and controls, ask:

- Are they being used to complement needed fiscal/monetary adjustment (e.g., smoothing a necessary depreciation), or to avoid it (e.g., defending an unrealistic peg)?

- Is the fundamental policy mix consistent with the exchange rate target, or are controls and intervention simply delaying a necessary adjustment?

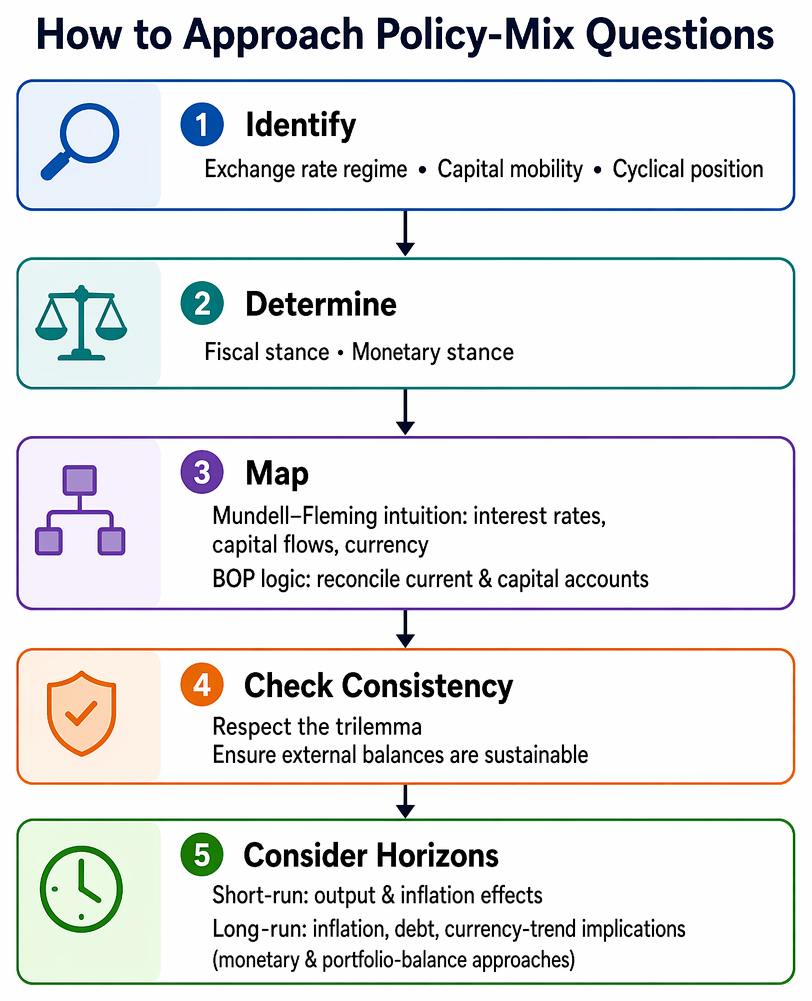

Revision Tip: How to Approach Policy-Mix Questions

A disciplined approach can help in complex vignettes:

Alternative policy mixes map joint fiscal-monetary stances to expected macroeconomic outcomes, including growth, disinflation, inflation risk, and external-balance support.

-

Identify:

- The exchange rate regime (floating, fixed, managed float, crawling peg).

- The degree of capital mobility (high, moderate, low).

- The cyclical position (output gap, inflation relative to target).

-

Determine:

- Fiscal stance (expansionary, neutral, contractionary).

- Monetary stance (relative to neutral rate, direction of recent changes).

-

Map:

- Use the Mundell–Fleming intuition to infer short-run effects on interest rates, capital flows, and the currency.

- Use BOP logic to reconcile current and capital account movements.

-

Check consistency:

- Does the policy mix respect the trilemma?

- Are external balances sustainable?

-

Consider horizons:

- Short-run output and inflation effects.

- Long-run inflation, debt, and currency-trend implications (monetary and portfolio-balance approaches).

Key Point Checklist

This article has covered the following key knowledge points:

- Fiscal, monetary, and exchange rate policies interact, and outcomes depend on the exchange rate regime and capital mobility.

- Under floating rates with high capital mobility, monetary policy is powerful for output stabilization; fiscal policy is partly offset by exchange rate movements.

- Under fixed rates with high capital mobility, fiscal policy is potent, and independent monetary policy is constrained by the need to defend the peg.

- The relative effectiveness of fiscal and monetary policy reverses when moving from floating to fixed regimes under high capital mobility.

- The policy trilemma implies that a country cannot simultaneously have a fixed exchange rate, free capital flows, and independent monetary policy.

- Short-run (Mundell–Fleming) and long-run (monetary and portfolio-balance) approaches can imply different currency responses to the same policy in different horizons.

- Uncovered interest rate parity, purchasing power parity, and the international Fisher relation link interest rate differentials, inflation expectations, and expected exchange rate changes.

- Balance of payments dynamics link current account imbalances, capital flows, and exchange rates through flow, portfolio-balance, and debt sustainability mechanisms.

- Capital controls and FX intervention can temporarily influence exchange rates, especially in smaller markets, but cannot offset fundamentally inconsistent policy mixes over time.

- Expansionary policy mixes can backfire via crowding out, currency depreciation, imported inflation, or eventual loss of confidence.

- Policy misalignment can trigger currency crises, reserve losses, sudden stops in capital flows, and abrupt shifts in growth and inflation.

- Exam-type scenarios often hinge on correctly identifying the regime, capital mobility, and likely direction of capital flows and currency movements in response to policy changes, as well as distinguishing short- from long-run effects.

Key Terms and Concepts

- fiscal policy

- monetary policy

- exchange rate regime

- capital mobility

- floating exchange rate

- fixed exchange rate

- managed float

- Mundell–Fleming model

- balance of payments (BOP)

- uncovered interest rate parity (UIP)

- current account

- capital (financial) account

- policy trilemma (impossible trinity)

- monetary approach to exchange rates

- portfolio-balance approach

- Dornbusch overshooting

- current account deficit

- sudden stop

- capital controls

- purchasing power parity (PPP)

- real interest rate parity

- international Fisher relation

- FX carry trade

- currency crisis

- overvalued real exchange rate