Learning Outcomes

This article explains the valuation and analysis of bonds with embedded options, including:

- Identifying key structural features of callable, putable, and convertible bonds and linking these features to investors’ and issuers’ incentives and payoffs.

- Comparing straight, callable, putable, and convertible bonds in terms of price behavior, yield, and sensitivity to changes in interest rates and volatility.

- Applying arbitrage-free binomial interest rate trees to value bonds with embedded options and to isolate the value of call, put, and conversion features.

- Implementing the call rule, put rule, and conversion value floor at each relevant node in a valuation tree to obtain consistent model prices.

- Evaluating how changes in the level, slope, and volatility of the yield curve affect the prices of callable, putable, and convertible bonds and their embedded options.

- Calculating and interpreting option-adjusted spreads (OAS) for bonds with embedded options, and contrasting OAS with Z-spreads in relative value and risk assessment.

- Assessing the risk–return profile of convertible bonds, including equity participation, downside protection from the bond floor, and constraints imposed by issuer call provisions.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are expected to understand the analysis and valuation of fixed-income securities with embedded options, with a focus on the following syllabus points:

- Describe features of callable, putable, and convertible bonds and how they affect pricing.

- Utilize the arbitrage-free valuation framework to value bonds with embedded options using interest rate trees.

- Compare the values of straight, callable, and putable bonds and relate them to option pricing.

- Analyze the impact of interest rate volatility and changes in yield curves on bonds with embedded options.

- Calculate and interpret the option-adjusted spread (OAS) and apply it in relative valuation.

- Evaluate risk, return, and valuation for convertible bonds.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What impact does increasing interest rate volatility have on the price of a callable bond?

- Explain how the price of a putable bond compares to an equivalent straight bond.

- Which bond features give the investor the right to return the bond to the issuer at a specified price before maturity?

- When the yield curve becomes steeper, how is the value of a call option within a callable bond affected?

Introduction

Many fixed-income securities include embedded options that significantly affect their valuation and risk-return characteristics. These embedded options, such as call and put features or conversion rights, allow issuers or investors to alter the bond's expected cash flows under certain conditions. Callable bonds allow issuers to redeem bonds prior to maturity, putable bonds grant investors the right to sell back bonds at specified terms, and convertible bonds permit holders to exchange bonds for shares. Understanding how these options alter bond valuation, and how to use interest rate trees and option-adjusted spreads (OAS) in analysis, is essential for CFA candidates.

Key Term: embedded option

An option feature built into a fixed-income security, such as a call, put, or convertibility provision, which alters the bond's cash flows under certain circumstances. Key Term: callable bond

A bond that grants the issuer the right, but not the obligation, to redeem the bond before maturity at a predetermined price. Key Term: putable bond

A bond that gives the investor the right, but not the obligation, to sell the bond back to the issuer at a specified price before maturity. Key Term: convertible bond

A hybrid security allowing the bondholder to exchange the bond for a fixed number of the issuer’s common shares during a certain period.Test Tip: When revising Callable putable and convertible bond valuation, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Valuing Bonds with Embedded Options

Option-adjusted spread estimation for callable, putable, and convertible bonds applies tree-based discounting, node-specific exercise constraints, and repeated market-price matching.

Option-Adjusted Valuation Approach

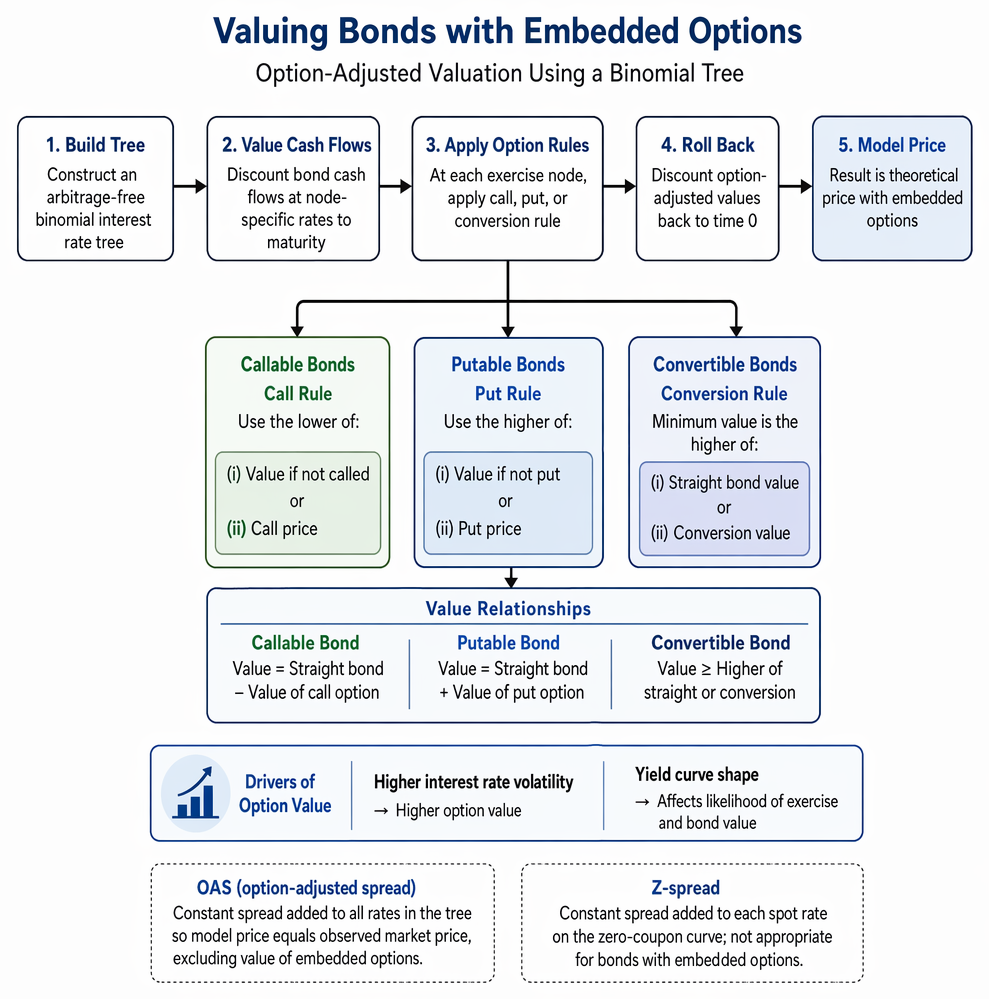

When valuing bonds with embedded options, each possible future cash flow depends on the likelihood of the option being exercised. An arbitrage-free binomial interest rate tree is used to simulate multiple interest rate scenarios and determine bond value under different paths.

For an option-free (straight) bond, each cash flow is discounted at the corresponding spot or forward rate. With embedded options, you must apply option exercise rules at each relevant node in the tree.

Key Term: option-adjusted spread (OAS)

The constant spread added to all rates in a valuation tree such that the model price equals the observed market price, excluding the value of embedded options.

Callable Bonds

The value of a callable bond equals the value of an otherwise identical straight bond minus the value of the embedded call option:

At any node where a call is allowed, use the lesser of (i) the value if not called, or (ii) the call price. This is known as the "call rule."

Putable Bonds

The value of a putable bond is the value of the straight bond plus the value of the put option:

Where a put is permitted, use the greater of (i) the value if not put, or (ii) the put price ("put rule").

Convertible Bonds

Convertible bonds combine straight debt with a long position in a call option on the issuer’s equity. The minimum value is the higher of the straight bond or the bond's conversion value:

The value increases with the probability of conversion being optimal, and is capped by the call feature if present.

Worked Example 1.1

A two-year, 5% $100 par bond is callable at par in one year. One-year forward rates are 4% and 7% in year 1, 5% and 9% in year 2. Calculate the value of the callable bond if the issuer can call at $100 after year 1.

Answer:

Build a binomial tree: Value in year 2 nodes is $105. Discount these back to year 1 nodes at the relevant rates. At the call date (year 1), use the lower of the non-called value and $100 (call price). Discount the year 1 values to time 0. The callable bond will be valued lower than an otherwise identical straight bond, reflecting the value of the issuer’s call option.

Effects of Interest Rate Volatility and Yield Curve Shape

The value of embedded options rises as interest rate volatility increases. For callable bonds, the call option becomes more valuable to the issuer, decreasing the bond’s price for the investor. Putable bonds behave oppositely: the put option gains value for the investor, raising the price compared to a straight bond.

Key Term: interest rate volatility

The expected magnitude of future changes in interest rates; its increase raises option values embedded in bonds.

Worked Example 1.2

Explain what happens to the price of a putable bond when interest rate volatility rises.

Answer:

As volatility rises, the value of the investor’s put option increases. This increases the price of the putable bond relative to an identical straight bond.

Option-Adjusted Spread and Valuation

The OAS is used to measure the spread relative to risk-free rates after removing the effect of the embedded option. For comparison among riskier bonds or relative value analysis, OAS is a more appropriate spread than the Z-spread for bonds with embedded options.

Key Term: Z-spread

The constant spread added to each spot rate on the zero-coupon curve so the theoretical price equals the bond’s market price; not appropriate for bonds with embedded options.Exam Warning: When valuing bonds with embedded options, always apply the option exercise (call/put/conversion) logic at each relevant node of the valuation tree. Failing to do this produces incorrect bond values and may lead to substantial errors on the exam.

Convertible Bond Risk and Return

Convertible bonds allow the investor to participate in equity upside while providing bond floor protection. Downside risk is limited by the straight bond value while upside is capped by the conversion ratio and issuer call rights. Convertible bond value depends on volatility of the issuer’s equity as well as prevailing rates.

Worked Example 1.3

A $1,000 par convertible bond can be converted into 20 shares. The stock price is $45. The convertible trades at $1,080. What is the minimum value of the convertible?

Answer:

Conversion value = 20 x $45 = $900. The straight (option-free) value must be given or can be calculated; assuming straight value = $950, the minimum is $950, as it is higher than conversion value.

Summary

Valuing bonds with embedded options requires understanding how callable, putable, and convertible features affect price and risk. Callable bond prices are capped by the call price and decline as volatility increases. Putable bonds are more valuable than straight bonds, especially when volatility rises. Convertible bonds combine features of debt and equity, granting investors participation in equity appreciation with protection from significant downside. Option-adjusted valuation using interest rate trees is essential, and the OAS is the standard spread measure for comparison.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain and distinguish callable, putable, and convertible bonds and their valuation.

- Apply binomial interest rate trees and option exercise rules in valuation.

- Understand the impact of interest rate volatility and yield curve changes on embedded option values.

- Calculate and interpret the option-adjusted spread (OAS).

- Assess risk and return characteristics of convertible bonds.

Key Terms and Concepts

- embedded option

- callable bond

- putable bond

- convertible bond

- option-adjusted spread (OAS)

- interest rate volatility

- Z-spread