Learning Outcomes

This article explains the fundamental law of active management and the information ratio in the context of CFA Level 2 portfolio management. It clarifies how active return and active risk are defined, measured, and combined to quantify value added by an active manager relative to a benchmark. It explains how the information ratio is calculated, interpreted, and distinguished from the Sharpe ratio when comparing managers or constructing benchmark-plus portfolios. It analyzes how factor models are used to separate manager skill from factor exposures and to estimate risk-adjusted performance. It details each component of the fundamental law—information coefficient, breadth, and transfer coefficient—and shows how these elements interact to determine the maximum achievable information ratio under both unconstrained and constrained implementations. It examines how changes in breadth, skill, or implementation efficiency affect optimal active risk allocation and expected active return. It reviews the main limitations and practical considerations when applying the fundamental law in manager evaluation, including estimation error, correlations among active bets, and institutional constraints, preparing you for both conceptual and calculation-based exam questions.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are expected to understand the evaluation of active portfolio managers using factor-based performance assessment methods and key risk-adjusted metrics, with a focus on the following syllabus points:

- Describe how value added by active management is measured using active return and active risk.

- Calculate and interpret the information ratio and distinguish it from the Sharpe ratio.

- Explain and interpret the fundamental law of active management: transfer coefficient, information coefficient, breadth, and active risk.

- Contrast ex-ante (expected) and ex-post (realized) uses of these performance measures.

- Evaluate the strengths and limitations of the fundamental law of active management.

- Apply these principles to investment manager selection and the determination of appropriate portfolio risk.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which ratio is best used to evaluate an active manager's consistency in outperforming a benchmark: the information ratio or the Sharpe ratio?

- What does the transfer coefficient measure in the context of active management?

- What is breadth in the fundamental law of active management, and how does it affect potential value added by a portfolio manager?

- If a fund has an information coefficient of 0.10 and undertakes 25 fully independent active decisions per year, what is its optimal ex-ante information ratio (assuming no constraints)?

Introduction

Selecting and assessing active managers requires a systematic approach to understanding value added, risk, and skill. Modern portfolio theory extends far beyond basic risk-return figures, placing importance on risk-adjusted measures that evaluate both returns and the consistency of those returns relative to benchmarks. For CFA Level 2, you must be fluent in using factor models for performance measurement, understanding the information ratio, and applying the fundamental law of active management. These concepts provide a robust framework for comparing, selecting, and constructing actively managed portfolios.

Key Term: active return

The difference between the return of an actively managed portfolio and its designated benchmark, representing the contribution of active decisions. Key Term: active risk (tracking error)

The standard deviation of the difference between the returns of an active portfolio and its benchmark over time, measuring volatility due to active management. Key Term: information ratio

The ratio of a portfolio’s active return to its active risk (tracking error), indicating how much active return is earned per unit of active risk. Key Term: information coefficient (IC)

A measure of a manager’s skill, defined as the expected correlation between forecasted active returns and actual active returns, risk-adjusted where applicable. Key Term: transfer coefficient (TC)

The correlation between the actual active weights applied and the optimal active weights that a manager would choose without constraints. Key Term: breadth (BR)

The number of independent active investment decisions made by a manager during a given period, usually per year. Key Term: fundamental law of active management

A framework expressing the maximum expected information ratio for an active manager as a function of skill (IC), breadth, and the manager's ability to implement active bets (TC).

Active Return, Active Risk, and Value Added

Active management aims to outperform a benchmark portfolio by making specific investment choices (active bets). The outcome is measured as active return and the volatility of those active returns is active risk.

Key Term: active return

The return in excess of the benchmark arising from overweighting or underweighting assets relative to the benchmark. Key Term: active risk (tracking error)

The standard deviation of the active return series, showing the unpredictability of manager outperformance or underperformance.

Calculation:

-

Active Return (RA): Where is the portfolio return and is the benchmark return.

-

Active Risk (σA): standard deviation of over time.

The Information Ratio: Assessment of Active Skill

The information ratio (IR) is the central tool for measuring how efficiently active return has been delivered, per unit of risk taken by deviating from a benchmark.

Key Term: information ratio

Active return divided by active risk (tracking error); a key figure for comparing managers’ risk-adjusted value-add versus a passive benchmark.

-

Formula:

-

Applications:

- Used to compare the consistency of value added by different managers.

- Useful for determining the optimal level of active risk to combine with a benchmark for maximum overall Sharpe ratio.

Worked Example 1.1

A portfolio outperformed its benchmark by 2% over the past year and had a tracking error (standard deviation of ) of 8%. What is its ex-post information ratio?

Answer:

IR = 2% / 8% = 0.25. This means the manager added 25 basis points of active return per 1% unit of active risk.Exam Warning: A common error is to confuse the information ratio with the Sharpe ratio. The Sharpe ratio considers return above the risk-free rate divided by total risk; the information ratio considers return relative to the benchmark per unit of active risk. Do not interchange these metrics when evaluating active managers.

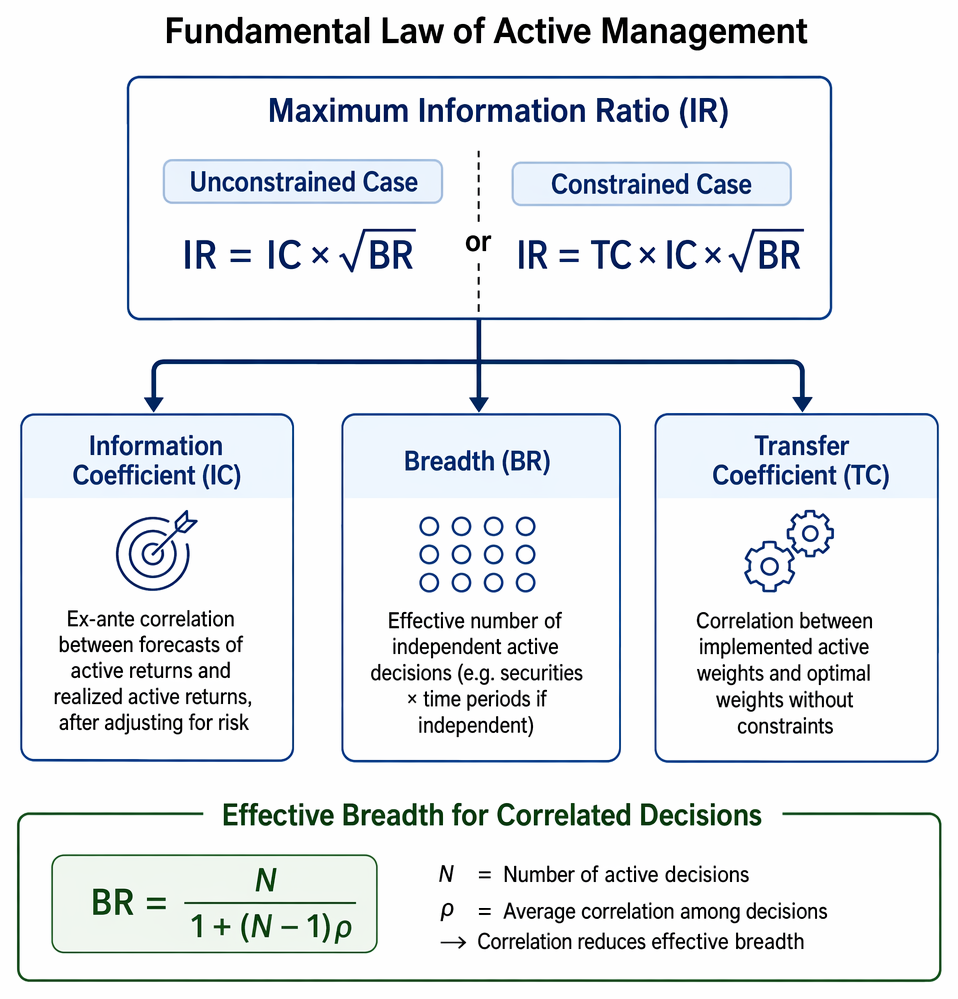

The Fundamental Law of Active Management

The fundamental law of active management expresses the expected value a manager can add as a function of their skill, the number of independent bets (breadth), and their ability to implement these bets optimally.

Fundamental law of active management equations present unconstrained and constrained information ratio expressions as functions of forecast skill, breadth, and implementation efficiency.

Key Term: fundamental law of active management

A model stating that the maximum information ratio achievable by an active manager equals the information coefficient (skill) times the square root of breadth, adjusted by the transfer coefficient (implementation quality).

-

Formula (unconstrained case):

Where:

- = Information coefficient (skill)

- = Breadth (number of independent bets per year)

-

Constrained portfolios:

Key Term: information coefficient (IC)

The ex-ante correlation between manager forecasts of active returns and the realized active returns, after adjusting for risk. Key Term: transfer coefficient (TC)

The correlation between the implemented active weights and the optimal weights the manager would select without constraints. Key Term: breadth (BR)

The effective number of independent active decisions (e.g., securities × time periods if independent).

Worked Example 1.2

Suppose a manager has IC = 0.08 and makes 100 independent active decisions per year (BR = 100). There are no implementation constraints (TC = 1). What is the manager's optimal information ratio?

Answer:

The manager could, in theory, achieve an IR of 0.80, assuming independent decisions and perfect implementation.

Revision Tip: In practice, decisions are often less than fully independent. If there is correlation among active decisions, effective breadth is reduced. For correlated decisions, use

where ρ is the average correlation among decisions.

Practical Use: Manager Selection and Portfolio Construction

When selecting managers or constructing active portfolios, focus on maximizing the information ratio. Investors can choose a combination of active manager and benchmark to achieve an optimal trade-off between active return and active risk.

- The optimal active risk allocation maximizes the overall Sharpe ratio.

- The expected active return for a given level of active risk is: .

- Adding cash or borrowing does not change the information ratio for an unconstrained portfolio.

Worked Example 1.3

A manager has an IR of 0.3. If an investor requires a maximum active risk of 5%, what is the expected active return from this manager at optimal allocation?

Answer:

Limitations of the Fundamental Law

While the framework is powerful, its practical use is limited by:

- Difficulty in accurately estimating manager skill (IC).

- Breadth (BR) may be significantly overstated if active decisions are correlated.

- Constraints (e.g., long-only, regulatory, liquidity) reduce the transfer coefficient (TC) below 1.

Summary

Factor models and risk-adjusted metrics such as the information ratio allow for objective assessment and comparison of active management performance. The fundamental law of active management expresses the link between skill, breadth, and implementation constraints in determining potential value added. For exam success, you must be able to apply these measures to evaluate managers and to construct risk-efficient portfolios.

Key Point Checklist

This article has covered the following key knowledge points:

- Measurement of value added by active management using active return and active risk

- Calculation and interpretation of the information ratio for active managers

- Formula and practical meaning of the fundamental law of active management

- Definitions and roles of the information coefficient, transfer coefficient, and breadth

- Application of these concepts to selecting managers and setting portfolio risk

- Real-world limitations such as estimation error and correlated decisions

Key Terms and Concepts

- active return

- active risk (tracking error)

- information ratio

- information coefficient (IC)

- transfer coefficient (TC)

- breadth (BR)

- fundamental law of active management