Learning Outcomes

This article explains the construction and application of macroeconomic, fundamental, and statistical factor models in the context of CFA Level 2 portfolio management. It clarifies how factor sensitivities are estimated, how factor surprises translate into asset returns, and how to distinguish economic shocks from firm-level characteristics and purely statistical dimensions. The discussion develops the multifactor return structure, showing how expected returns, factor exposures, and idiosyncratic components combine to generate realized performance. The article also explains how factor models are used for return attribution, separating active return into contributions from deliberate factor tilts and security selection effects, and for risk attribution, decomposing active risk into systematic and specific components. In addition, it covers the construction and interpretation of factor-mimicking and tracking portfolios, highlighting how managers adjust exposures to size, value, growth, and other style factors while controlling unintended bets. Finally, the article examines typical exam-style calculations, such as computing standardized factor sensitivities, factor premiums, and the factor contribution to active return, and emphasizes the interpretation of regression output and model assumptions that are frequently tested in the CFA Level 2 examinations.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are expected to understand the theory and practical application of multifactor models within the context of active portfolio management, with a focus on the following syllabus points:

- Outlining arbitrage pricing theory (APT) and its relationships to multifactor return models.

- Explaining the construction, use, and interpretation of macroeconomic, fundamental, and statistical factor models.

- Applying multifactor models to return decomposition and risk attribution for portfolios and benchmarks.

- Calculating factor exposures and using models to construct factor and tracking portfolios.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- In a macroeconomic factor model, what does a positive factor sensitivity to unexpected GDP growth imply about a stock’s performance when GDP growth is higher than forecast?

- What distinguishes a fundamental factor model from a macroeconomic factor model?

- What is meant by a "factor mimicking portfolio" and how can it be used by an active manager?

- Why is standardization of factor sensitivities important in constructing a fundamental factor model?

Introduction

Factor models provide the core analytical framework for understanding systematic sources of return and risk in asset pricing and portfolio management. Unlike single-factor models such as the CAPM, multifactor models allow investors to assess exposures to multiple driver variables. These variables can represent shocks to macroeconomic data, firm-specific characteristics, or even purely statistical dimensions. For CFA Level 2, you need to be able to differentiate these models, interpret regression results, and understand their implications for active management.

Key Term: factor model

A linear model where asset returns are explained as a sensitivity-weighted sum of one or more systematic risk factors plus an asset-specific component.Test Tip: When revising Macroeconomic fundamental and statistical factor models, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

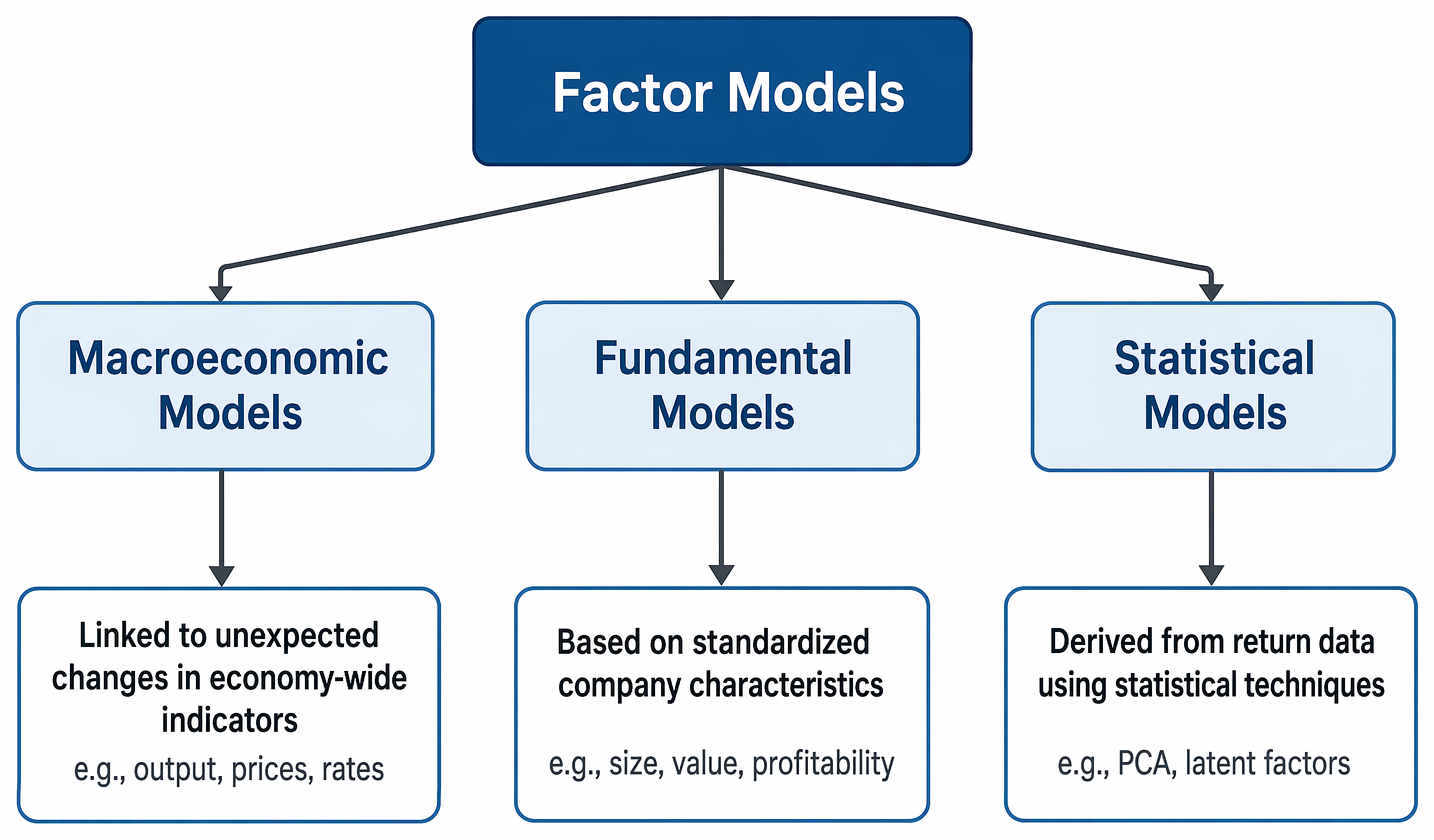

Macroeconomic Factor Models

Macroeconomic factor models explain asset returns by relating them to surprises in economic or financial variables, such as unexpected changes in GDP or inflation. Only unanticipated components (surprises relative to consensus forecasts) influence prices, as expected values are already discounted by the market.

Key Term: systematic risk factor

A variable that affects large numbers of assets and cannot be diversified away in portfolio construction.

The general structure of a macroeconomic factor model is:

Where:

- is the expected return for asset i,

- is the sensitivity of asset i to factor k,

- is the surprise in factor k,

- is asset-specific surprise (idiosyncratic component).

Key Term: factor sensitivity

A measure of how much an asset’s return changes in response to a unit change in a given factor, holding other factors constant.

Typical macro factors include:

- Surprises in real GDP growth,

- Unanticipated inflation,

- Unexpected changes to credit spreads,

- Commodity price shocks.

Worked Example 1.1

A firm’s return is modelled as . If GDP growth is 1% above forecast and credit spread is 0.5% below expectations, what is the total contribution from factor shocks (ignoring )?

Answer:

GDP shock:

Credit spread shock:

Total factor contribution:

or +2.35% Key Term: factor surprise

The difference between the realized value of a macroeconomic factor and its market-expected value.

Fundamental Factor Models

Fundamental factor models link asset returns to firm-specific characteristics, such as size, value, gearing, or profitability. Unlike macro models, the factors here are not economic shocks but attributes calculated from firm data.

Factor model categories are organized by whether factors represent economic shocks, firm characteristics, or latent dimensions estimated from returns.

Sensitivities in fundamental factor models are typically standardized, showing how many standard deviations a company’s characteristic is from the mean. For example, a stock with a P/E 1.5 standard deviations above the average has a standardized factor sensitivity of +1.5.

Key Term: standardized factor sensitivity

The number of standard deviations a firm’s characteristic is from the cross-sectional mean for that attribute.

Statistical regression is used to estimate the return premium (factor return) for each attribute. The model structure is:

Worked Example 1.2

A stock has sales growth 12%, while the market average is 7% with a standard deviation of 2%. What is its standardized sales growth sensitivity?

Answer:

The stock's sales growth is 2.5 standard deviations above average.

Statistical Factor Models

Statistical factor models use mathematical techniques (like principal component analysis) to extract factors that best explain observed covariances or variances in returns—without economic or fundamental interpretation.

Key Term: statistical factor model

A model that identifies factors explaining return behaviour solely through statistical analysis, without reference to identifiable real-world variables.

Such models can reveal hidden commonalities within large universes but may be difficult to interpret or use for strategy construction.

Applications in Active Management

Factor models support portfolio construction, performance attribution, and risk management:

- Return attribution: Breaking down active returns into allocation to specific risk factors (factor return) and security selection.

- Risk attribution: Decomposing active risk into risk from factor tilts (systematic) and risk from selection of individual securities (specific risk).

- Portfolio construction: Designing portfolios targeting desired factor exposures, often for speculation or hedging.

Worked Example 1.3

A manager’s fundamental factor model finds the portfolio’s size exposure is +0.9 relative to the benchmark and the size factor premium is +2%. What is the factor return attributable to size?

Answer:

The size factor adds +1.8% relative to the benchmark.

Exam Warning: When constructing tracking portfolios using factor models, ensure that estimated factor sensitivities match the benchmark. Failing to align exposures results in active risk from unintended sources.

Summary

Macroeconomic, fundamental, and statistical factor models offer frameworks for quantifying sources of return and risk. Macroeconomic models capture reactions to unexpected economic variables. Fundamental models use firm attributes, typically standardized. Statistical models extract factors mathematically, often without economic meaning. All have critical roles in portfolio construction and active management.

Key Point Checklist

This article has covered the following key knowledge points:

- The structure and purpose of macroeconomic, fundamental, and statistical factor models.

- How to interpret factor sensitivities and surprises in macroeconomic models.

- The distinction between regression-based and standardized-factor sensitivities.

- The concept and use of factor mimicking portfolios in active management.

- Applications of factor models for portfolio return attribution and risk management.

Key Terms and Concepts

- factor model

- systematic risk factor

- factor sensitivity

- factor surprise

- standardized factor sensitivity

- statistical factor model