Learning Outcomes

This article explains cost-of-carry pricing and convexity effects for forwards, futures, and swaps, including:

- Valuing forward and futures contracts using the cost-of-carry framework under discrete and continuous compounding, and interpreting each parameter in exam-style calculations.

- Adjusting spot prices for dividends, coupons, foreign interest rates, storage, insurance, and convenience yields, and distinguishing between discrete cash flows and continuous yields.

- Translating qualitative descriptions of carry benefits and costs into the correct pricing inputs, net cost-of-carry rate, and sign conventions tested in CFA Level 2 item sets.

- Comparing theoretical (no-arbitrage) forward and futures prices with quoted market prices, identifying mispricing, and quantifying the magnitude of the deviation.

- Structuring cash-and-carry and reverse cash-and-carry arbitrage strategies, detailing trade setup, financing, and payoff cash-flows, and computing risk-free profit when implementation is feasible.

- Explaining swap valuation by viewing interest rate, equity, and commodity swaps as portfolios of forward contracts and linking the par swap rate to forward prices.

- Analyzing convexity effects that cause futures and forwards on the same reference asset to differ in value when interest rates are stochastic and correlated with the asset price.

- Recognizing common Level 2 traps such as double-counting carry components, mixing compounding conventions, or misinterpreting dividend, yield, and convenience yield information in vignette data.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are required to understand forwards, futures, and swaps valuation using cost-of-carry pricing and convexity concepts, with a focus on the following syllabus points:

- Explain and apply the cost-of-carry pricing model for forwards, futures, and swaps.

- Calculate forward and futures prices for assets with or without income, storage, or other carrying costs.

- Adjust forward pricing for known cash flows, income yields, and foreign interest rates.

- Identify and exploit (or explain why you cannot exploit) arbitrage opportunities when traded prices deviate from theoretical values.

- Describe and analyze convexity effects in derivative pricing, particularly the difference between futures and forward prices.

- Understand how non-linear payoffs and daily marking-to-market affect futures and swap valuations.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

Use the following information for Questions 1–4.

An analyst at Delta Capital is reviewing several derivative positions:

- Stock X trades at $80. It is expected to pay a single dividend of $1.20 in three months. The 6‑month risk‑free rate is 4% (simple annual, actual/365). A 6‑month forward on Stock X is quoted at $82.20.

- A broad equity index is at 3,000 with a continuous dividend yield of 2% and a continuous risk‑free rate of 3%. The 1‑year futures price is 3,080.

- A 2‑year fixed‑for‑floating interest rate swap on notional $10 million is priced at par at inception, with annual payments.

- A 5‑year Treasury bond and a 5‑year Treasury bond futures contract on the same bond are both quoted, and interest rates are expected to be volatile.

-

Based on the stock forward information, what is the theoretical no‑arbitrage 6‑month forward price for Stock X (using simple compounding), and is there an arbitrage opportunity?

- a) $81.11; forward is overpriced and a cash‑and‑carry arbitrage is possible.

- b) $81.11; forward is underpriced and a reverse cash‑and‑carry arbitrage is possible.

- c) $82.20; the forward is fairly priced and no arbitrage exists.

- d) $83.31; the forward is underpriced and a reverse cash‑and‑carry arbitrage is possible.

-

For the 1‑year equity index futures, which statement best describes the impact of a higher continuous dividend yield (with all else constant)?

- a) The theoretical futures price falls because the index’s carry benefit has increased.

- b) The theoretical futures price rises because the index’s carry benefit has increased.

- c) The theoretical futures price is unchanged because dividends do not affect index futures.

- d) The theoretical futures price may rise or fall depending on the sign of the basis.

-

Regarding the 2‑year interest rate swap priced at par at inception, which statement is most accurate?

- a) The fixed rate is set so that the present value of fixed payments equals zero.

- b) The fixed rate is set so that the present values of fixed and expected floating payments are equal.

- c) The swap fixed rate equals the current 2‑year spot rate.

- d) The swap fixed rate equals the average of 1‑ and 2‑year spot rates.

-

For the 5‑year Treasury bond futures and forward with the same maturity and reference asset, when are you most likely to observe a higher futures price than forward price, assuming identical cost‑of‑carry inputs?

- a) When interest rates are constant and non‑stochastic.

- b) When interest rates are volatile and negatively correlated with the bond price.

- c) When interest rates are volatile and positively correlated with the bond price.

- d) When there is no marking‑to‑market on the futures contract.

Introduction

Derivative contracts such as forwards, futures, and swaps are priced to rule out arbitrage by linking their values to the cost of holding (carrying) the reference asset until the contract’s maturity. The cost-of-carry model brings together financing costs, any income generated by the asset (such as dividends, coupons, or foreign interest), and any storage or insurance costs.

Key Term: cost-of-carry

The total net cost of holding an asset until a future date, including financing, storage, and insurance costs, minus any income or benefits generated by the asset over that period.

Futures contracts add one important feature relative to forwards: they are marked to market daily through a clearinghouse. This daily settlement gives futures a non‑linear dependence on interest rate movements because gains and losses are realized and reinvested (or financed) over time, instead of only at maturity.

Key Term: convexity

The curvature in the relationship between a derivative’s value and movements in relevant risk factors such as prices or interest rates; for futures, convexity arises because daily marking‑to‑market alters cash‑flow timing and reinvestment opportunities.

Pricing must also consider arbitrage relationships between the derivative and the reference asset. When the market forward or futures price diverges from theoretical no‑arbitrage value, a well‑constructed trading strategy can lock in a risk‑free profit—provided practical constraints do not prevent implementation.

Key Term: arbitrage

A trading strategy that requires no net investment, has negligible risk, and is expected to generate a risk‑free profit by exploiting mispricing among related instruments.

These ideas extend directly to swaps. Many swaps can be decomposed into portfolios of forward contracts, so understanding forward pricing is a key prerequisite for swap valuation at Level 2.

Test Tip: When revising Cost-of-carry pricing and convexity effects, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Exam Warning: Do not rely on keyword recognition alone; check the precise condition, exception, calculation step, or evidence the question requires.

COST-OF-CARRY PRICING OF FORWARDS, FUTURES, AND SWAPS

The cost-of-carry model provides the no-arbitrage price for forward and futures contracts under the assumption that investors can borrow and lend at the risk-free rate and can buy or short the reference asset without restriction.

Key Term: forward price

The agreed price today for future delivery of an asset, set so that the contract has zero value at initiation under no-arbitrage conditions.

General cost-of-carry relationship

For an asset with a spot price , known cash flows during the life of the contract, and a simple annual risk‑free rate , the basic discrete‑compounding forward pricing formula is:

where:

- = no‑arbitrage forward (or futures) price for maturity (in years)

- = present value of known income (dividends, coupons, lease payments received) over

- = present value of known carrying costs (storage, insurance, etc.) over

- = financing rate (often the risk‑free rate consistent with the currency and maturity)

- = time to forward delivery in years

A very common Level 2 variant uses continuous compounding and expresses net carry as a rate:

where:

- = continuously compounded proportional storage or other cost rate

- = continuously compounded income or yield benefit rate (e.g., dividend yield, foreign risk‑free rate, or convenience yield for commodities)

The combination is the net cost of carry: a positive value pushes the forward above spot; a negative value pulls it below.

Key Term: income yield

A continuously compounded rate representing income (such as dividend or foreign interest) expressed as a percentage of the asset’s price, used as:

in cost-of-carry models.

Applying cost-of-carry to different assets

1. Individual stocks with discrete dividends

For a stock paying known cash dividends at times , each dividend is discounted at the appropriate risk‑free rate:

Then:

Key Term: futures price

The quoted price for a standardized futures contract. Under deterministic interest rates and identical carry assumptions, the theoretical futures price equals the forward price for the same reference asset and maturity.

This reflects that an investor who buys the stock today benefits from dividends, so a buyer of the forward should effectively pay less than .

2. Bonds with coupons

For coupon‑paying bonds, the same logic applies. The present value of any coupons to be received before maturity of the forward is subtracted from the spot price.

- Identify coupon dates within .

- Discount each coupon at the appropriate risk‑free rate to obtain .

- Compute:

Exam item sets frequently combine bond mathematics with forward pricing, so be careful not to double‑discount coupons (once for the bond price and again for the forward).

3. Stock index and other assets with a known yield

When the asset provides a known proportional income yield (e.g., a broad equity index with dividend yield), a continuous‑compounding formulation is convenient:

Here, plays the role of a negative carry cost. For , the theoretical forward can be below the spot price—that is, the market can be in backwardation even in the absence of storage or convenience yield.

4. Foreign currency forwards

Foreign currency can be treated as an asset that provides a “dividend” equal to the foreign risk‑free rate while costing the domestic risk‑free rate to finance. With continuous compounding:

This is simply covered interest parity expressed in forward pricing form.

5. Commodity forwards and convenience yield

For commodities, we must incorporate storage costs and the idea that holding the physical asset can provide non‑monetary benefits known as convenience yield.

Key Term: convenience yield

A non‑cash benefit (such as assured availability or production continuity) from physically holding a commodity inventory, modeled as a yield that effectively reduces the net cost of carry.

Let:

- = proportional storage and insurance cost rate

- = sum of all yield‑like benefits (e.g., convenience yield, lease rate)

Then:

Because is not directly observable and reflects market conditions (inventory levels, demand uncertainty), commodities often trade within a no‑arbitrage band rather than at a single precise theoretical price.

Key Term: basis

The difference between the spot price and the futures (or forward) price for a given maturity:

When (positive net cost of carry), the market is in contango. When (negative net cost of carry, often due to high convenience yield), the market is in backwardation.

Key Term: contango

A term structure state where futures (or forward) prices are above the current spot price, often associated with positive net carry costs. Key Term: backwardation

A term structure state where futures (or forward) prices are below the current spot price, often associated with strong carry benefits such as high convenience yield.

Swaps as portfolios of forwards

Many swaps can be decomposed into a series of forward contracts, so cost-of-carry logic carries over directly.

Key Term: swap fixed rate

The fixed rate on a swap chosen at initiation so that the present value of fixed‑leg cash flows equals the present value of expected floating‑leg cash flows, giving the swap zero value initially.

- Interest rate swaps: A fixed‑for‑floating interest rate swap with annual payments over years is equivalent to a portfolio of forward rate agreements (FRAs), each setting a forward interest rate for a future period. The par swap fixed rate is the weighted average of these forward rates, discounted with the appropriate zero‑coupon rates.

- Equity swaps: A total‑return equity swap exchanging equity index returns for a fixed rate can be replicated by a sequence of equity index forwards priced via the cost‑of‑carry formula for indices.

- Commodity swaps: A fixed‑for‑floating commodity swap can be valued as a strip of commodity forwards using the commodity cost‑of‑carry relationship (including storage and convenience yield).

In all cases, at inception the swap is priced so that the initial value is approximately zero to both counterparties, mirroring the zero value of a fairly priced forward.

Worked Example 1.1

A 180‑day forward contract is written on a share trading at $50. The annual risk‑free rate is 6% (simple annual), and a $0.80 dividend is expected in 90 days. Calculate the no-arbitrage forward price.

Answer:

First compute the present value of the dividend using the 6% annual rate for 0.25 years:

Adjust the spot price for the dividend:

Now compound this net amount for 0.5 years at 6%:

The no-arbitrage 180-day forward price is approximately $50.68.

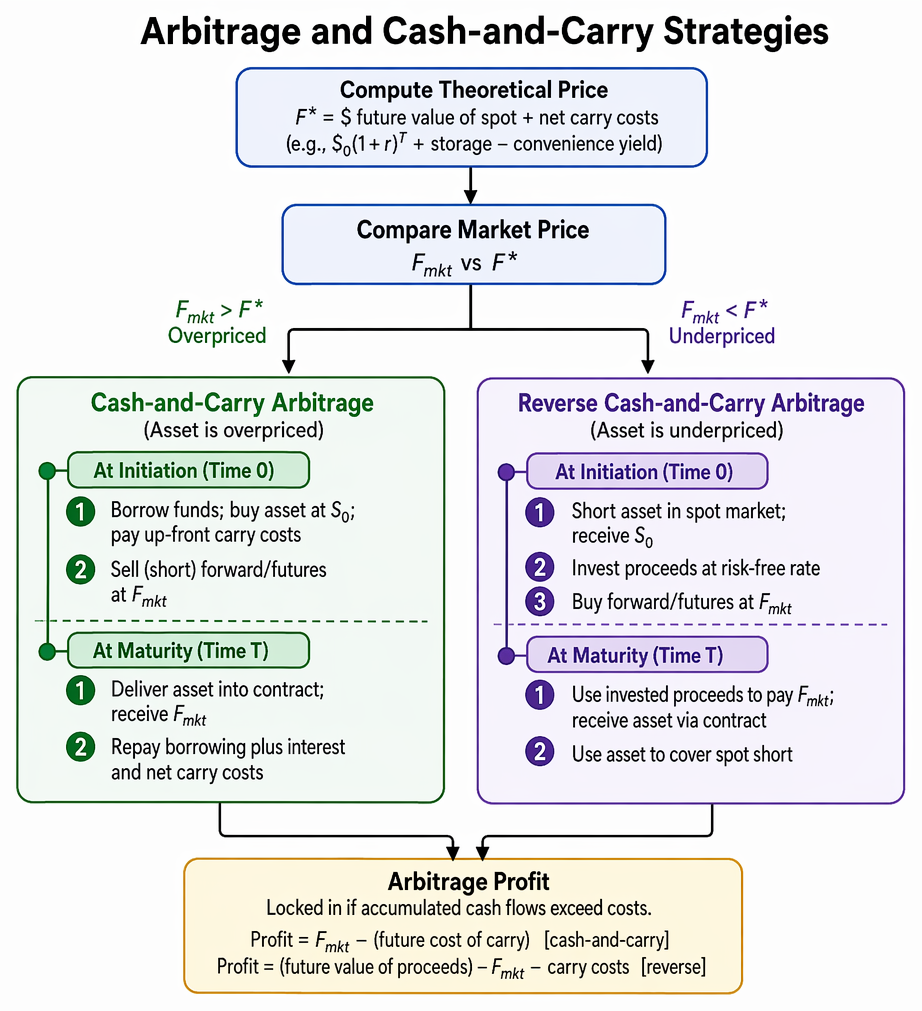

ARBITRAGE AND CASH-AND-CARRY STRATEGIES

When the actual forward or futures price deviates from the no‑arbitrage price implied by cost‑of‑carry, arbitrage may be possible. You must be able to:

Cost-of-carry relationships for major asset classes are summarized using discrete cash-flow adjustments and continuous net carry formulations.

- Decide whether the contract is overpriced or underpriced.

- Specify whether to use a cash‑and‑carry or reverse cash‑and‑carry arbitrage.

- Lay out the trades at initiation and at maturity, and compute risk‑free profit.

Key Term: cash-and-carry arbitrage

An arbitrage strategy used when the forward or futures price is too high: buy (carry) the asset in the spot market, finance it, and sell the overpriced forward or futures. Key Term: reverse cash-and-carry arbitrage

An arbitrage strategy used when the forward or futures price is too low: short the asset in the spot market, invest the proceeds, and buy the underpriced forward or futures.

Overpriced forward or futures (cash-and-carry)

If the quoted price is above theoretical :

-

At initiation:

- Borrow funds at rate to buy the reference asset at and pay any up‑front carry costs.

- Sell (short) the forward or futures at .

-

At maturity:

- Deliver the asset into the contract and receive .

- Repay the borrowing plus interest and any net carry costs.

A positive difference between and the accumulated cost of carrying the asset generates a risk‑free profit.

Underpriced forward or futures (reverse cash-and-carry)

If :

-

At initiation:

- Short the asset in the spot market and receive .

- Invest the proceeds at the risk‑free rate.

- Buy the forward or futures at .

-

At maturity:

- Use proceeds from the invested cash to pay and receive the asset via the forward.

- Use the asset to cover the spot short sale.

If the accumulated invested proceeds exceed plus any borrowing of carry costs (e.g., dividends, coupons you must pay to the lender of the security), you lock in arbitrage profit.

Worked Example 1.2

Suppose crude oil trades at a spot price of $70 per barrel. The annual risk‑free rate is 5% (simple annual), and storage costs are $1 per barrel, payable at the end of the year. A one‑year oil futures contract is quoted at $78. Assume no convenience yield and that the contract size is one barrel. Determine whether an arbitrage exists and, if so, construct it and compute the profit per barrel.

Answer:

First compute the theoretical no-arbitrage futures price. The future value of the spot purchase plus storage cost is:

- Spot purchase financed for one year:

- Storage cost at maturity: $1.

- Total cost of carry at maturity:

Thus the theoretical futures price is:

The quoted futures price is $78, so the futures is overpriced. A cash-and-carry arbitrage is appropriate. At initiation (time 0):

- Borrow $71 at 5% and buy one barrel of oil for $70; hold $1 aside to pay storage at year-end.

- Enter a short futures position at $78.

At maturity (time 1):

- Pay $1 storage cost.

- Deliver the barrel into the futures contract and receive $78.

- Repay the loan: $71 x 1.05 = $74.55.

Profit per barrel at maturity:

A risk-free arbitrage profit of $2.45 per barrel can be locked in, ignoring transaction costs and margins.

In item sets, you are often asked not only for the strategy direction (long/short asset and forward) but also for the exact cash‑flow amounts at each date.

Practical limits to arbitrage

In reality—and in some exam vignettes—arbitrage may not be feasible even when theoretical mispricing exists. Constraints include:

- Short‑selling restrictions or high stock‑loan fees (for reverse cash‑and‑carry).

- Limited or costly storage capacity for commodities.

- Bid‑ask spreads, commissions, and margin requirements.

- Credit risk and capital constraints.

- Model risk (e.g., uncertainty about true convenience yield).

You must be able to recognize such situations in item sets and justify why an apparent mispricing may persist without true arbitrage.

CONVEXITY EFFECTS IN FORWARD AND FUTURES PRICING

Convexity reflects non‑linear relationships between derivative values and key risk factors. Forwards and futures with the same reference asset and maturity, cost‑of‑carry alone would imply they should have the same theoretical price when interest rates are known with certainty. However, when interest rates are stochastic, daily marking-to-market makes the futures contract’s payoff path‑dependent and introduces convexity.

Key Term: marking-to-market

The daily settlement process for futures contracts whereby gains and losses are realized each day as prices change, with variation margin flows between counterparties.

Because futures gains and losses are realized over time, the timing of these cash flows interacts with interest rate movements:

- When the asset price and interest rates are positively correlated, gains on a long futures position tend to occur when rates are high (allowing gains to be reinvested at higher rates), and losses occur when rates are low (and are financed at lower rates). This favors the long futures holder.

- When they are negatively correlated, gains occur when rates are low and losses when rates are high, which is disadvantageous for the long futures holder.

This asymmetry, analogous to convexity in bond pricing or gamma in option pricing, causes the fair futures price to differ from the forward price even when all carry inputs are identical.

Key Term: convexity (futures vs forwards)

The effect whereby daily marking‑to‑market causes futures contract value to respond non‑linearly to changes in interest rates and the asset price, leading to systematic differences between futures and forward prices when rates are volatile.

The rule of thumb is:

- If the asset price and interest rates are positively correlated (e.g., many commodities and equities), the futures price tends to be higher than the forward price.

- If the asset price and interest rates are negatively correlated (e.g., long‑duration government bonds), the futures price tends to be lower than the forward price.

Worked Example 1.3

A 5‑year government bond and its corresponding 5‑year futures contract are both priced using the same spot price, coupon schedule, and risk‑free yield curve. Interest rates are volatile and tend to fall when bond prices rise (i.e., bond prices and interest rates are negatively correlated). Explain why the futures price may be lower than the forward price, even though the cost‑of‑carry inputs are identical.

Answer:

With negative correlation between bond prices and interest rates, a long futures position tends to earn gains when interest rates are low and incur losses when interest rates are high:

- When bond prices rise (rates fall), the long futures position gains. These gains are received through daily marking‑to‑market, but must be reinvested at the new, lower interest rates.

- When bond prices fall (rates rise), the long futures position loses, and these losses are financed at higher interest rates.

This timing asymmetry hurts the long futures holder relative to a forward contract, where the entire payoff is realized only at maturity and effectively discounted at an average interest rate over the life of the contract. To compensate for this disadvantage, the fair futures price must be set below the corresponding forward price. This difference is the convexity effect arising from the interaction of interest rate volatility, negative correlation with bond prices, and daily marking‑to‑market.

Conceptually, this is similar to bond convexity: ignoring convexity (using only duration) misstates the true sensitivity of bond prices to interest rates; ignoring futures convexity misstates the relation between futures and forward prices when rates are stochastic.

Exam warning on carry inputs

It is a common Level 2 error to mishandle income and carry components:

- Forgetting to subtract the present value of dividends or coupons.

- Treating a yield (e.g., dividend yield ) as a discrete amount and also subtracting individual cash flows (double‑counting).

- Ignoring storage or convenience yield in commodity questions.

- Mixing simple and continuous compounding within the same calculation.

Always read carefully whether the question states discrete cash flows or continuous yields, and whether carrying costs are quoted as dollar amounts or percentage rates. Align the compounding method for spot adjustment, cost-of-carry, and discounting.

Summary

Cost-of-carry pricing links forward, futures, and swap values to the economics of holding the reference asset: financing costs, income, and storage or convenience yields. The general framework can be adapted to equities, bonds, currencies, commodities, and swaps by appropriately adjusting for cash flows and yields. When market prices deviate from theoretical values, cash‑and‑carry or reverse cash‑and‑carry arbitrage strategies may exist, although real‑world constraints can prevent their execution. Futures differ from forwards because daily marking‑to‑market introduces convexity: under volatile and stochastic interest rates, the correlation between the asset price and interest rates drives systematic differences between futures and forward prices.

Key Point Checklist

This article has covered the following key knowledge points:

- The general cost-of-carry model for pricing forwards and futures under discrete and continuous compounding.

- Adjusting forward prices for dividends, coupons, foreign interest rates, storage costs, and convenience yields.

- Viewing and valuing swaps as portfolios of forward contracts with zero value at inception.

- Identifying when a forward or futures is overpriced or underpriced and constructing cash‑and‑carry or reverse cash‑and‑carry arbitrage strategies.

- Recognizing practical constraints that can limit arbitrage, such as short‑selling restrictions and storage constraints.

- Understanding how daily marking‑to‑market and interest rate volatility create convexity effects, leading to differences between futures and forward prices.

- Applying these concepts in CFA Level 2 item sets without double‑counting carry components or misinterpreting yield information.

Key Terms and Concepts

- cost-of-carry

- convexity

- arbitrage

- forward price

- income yield

- futures price

- convenience yield

- basis

- contango

- backwardation

- swap fixed rate

- cash-and-carry arbitrage

- reverse cash-and-carry arbitrage

- marking-to-market

- convexity (futures vs forwards)