Learning Outcomes

This article explains FRA valuation and applications, including:

- Pricing FRAs at initiation from money market reference rates, deriving forward rates, and interpreting each term in the standard FRA pricing and payoff formulas.

- Computing FRA settlement amounts when reference rates reset, correctly applying day-count conventions and discounting payoffs to the settlement date.

- Marking FRAs to market before settlement using updated forward curves, valuing early close-outs, and linking changes in value to movements in interest rates.

- Determining appropriate long or short FRA positions to hedge future borrowing or investing, and identifying which side benefits from rate increases or decreases.

- Comparing FRAs with standard forwards, interest rate futures, and plain-vanilla fixed-for-floating swaps, including viewing a swap as a strip of FRAs.

- Diagnosing typical exam errors such as sign, timing, or units mistakes, mixing up reference and FRA rates, omitting discounting, or misreading the FRA notation.

- Interpreting FRA valuation results in the context of term-structure information (spot rates, discount factors, money market reference rates) and relating FRA values to changes in the yield curve.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are required to understand how forward rate agreements (FRAs), forwards, and swaps are valued and applied in practice, with a focus on the following syllabus points:

- Pricing and valuing FRAs at and after contract initiation.

- Calculating the mark-to-market value of FRAs and identifying settlement payments.

- Comparing FRA, forward, futures, and swap structures and their mechanics.

- Applying FRAs for interest rate risk management and hedging strategies.

- Recognizing potential valuation and calculation errors in exam scenarios.

- Relating FRAs to interest rate futures and understanding the swap–FRA equivalence.

- Integrating FRA valuation with broader yield-curve and term-structure analysis.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

Vega Components is a USD-based manufacturer. Its treasurer expects several future money-market transactions and is considering FRAs to hedge rate risk. Unless otherwise stated, assume an actual/360 day-count basis and simple interest.

Three-month and nine-month money market reference rates (MRR) are:

- 3‑month (90 days): 4.0%

- 9‑month (270 days): 5.2%

The firm expects to borrow $20 million for six months, starting in three months. The bank also quotes a 3×9 FRA at 5.0% on a 180‑day reference period.

-

To hedge the planned six‑month borrowing from months 3 to 9, which FRA position and contract rate best implements the hedge for Vega Components?

- a) Short 3×9 FRA at 4.0%

- b) Long 3×9 FRA at 4.0%

- c) Long 3×9 FRA at the fair forward rate implied by 3‑ and 9‑month MRRs

- d) Short 3×9 FRA at the fair forward rate implied by 3‑ and 9‑month MRRs

-

Vega enters a 3×9 FRA at a contract rate of 5.0% on a $20 million notional with a 180‑day reference loan period. At FRA settlement in three months, the 6‑month reference rate (for months 3–9) fixes at 6.2%. Ignoring credit risk, the settlement payment to the long FRA position is closest to:

- a) $0.24 million paid by the long

- b) $0.24 million received by the long

- c) $0.23 million received by the long

- d) $0.23 million paid by the long

-

Ten days after initiating the FRA in Question 2, the term structure shifts and the fair 3×9 FRA rate for a new trade is 4.6%, while Vega’s existing FRA rate is 5.0%. All else equal, the mark‑to‑market value of the original FRA to the long position (ignoring any day-count precision between today and settlement) is:

- a) Negative, because current forward rates are now below the FRA rate

- b) Positive, because current forward rates are now below the FRA rate

- c) Zero, because FRAs always have zero value until settlement

- d) Indeterminate without knowing the notional

-

The bank that sold the FRA to Vega also wants to synthetically convert a separate 2‑year fixed‑rate loan asset into a floating‑rate exposure by using either a plain‑vanilla interest rate swap or a strip of FRAs. Which statement best describes the relation between the swap and an equivalent strip of FRAs?

- a) A swap differs because notional principal is exchanged, whereas FRAs never reference a notional

- b) A swap is economically equivalent to a strip of FRAs with identical fixed rates and reset dates

- c) A swap has a single payment at maturity, whereas a strip of FRAs requires periodic payments

- d) A swap has uncertain cash flows, whereas a strip of FRAs has fixed payments

Introduction

Forward rate agreements (FRAs), forwards, futures, and swaps are core instruments for managing and transferring interest rate risk. For Level 2, FRAs sit at an important crossroads:

- They are priced and valued using the same no‑arbitrage logic as other forwards.

- They embed money market conventions (simple interest, day-count) that must be handled precisely.

- They are the building blocks of plain‑vanilla interest rate swaps and closely related to interest rate futures.

Level 2 questions are vignette‑based. FRAs often appear embedded in:

- Bank asset–liability management problems (hedging repricing gaps).

- Corporate treasury cases (locking in future borrowing or investing rates).

- Swap valuation item sets (using the “strip of FRAs” interpretation).

You are expected not only to remember formulas, but to:

- Place FRA cash flows correctly on a timeline.

- Distinguish clearly between price (the FRA rate) and value (currency amount).

- Interpret how changes in the yield curve affect FRA values and hedge effectiveness.

In practice, FRAs are written on interbank money market reference rates (MRR) such as LIBOR historically and now its replacements (SOFR-based term rates, Euribor, etc.). For exam problems, the reference is often a generic “money market reference rate (MRR)” with:

- Simple interest (no compounding over the period).

- A specified day-count convention (most often actual/360, occasionally 30/360 or actual/365).

Key Term: forward rate agreement (FRA)

A contract where parties agree today on an interest rate to apply to a notional loan or deposit over a future period. At settlement, a single cash payment reflects the present value of the difference between the agreed FRA rate and the actual reference rate, applied to the notional. Key Term: FRA rate

The fixed annualized interest rate specified in the FRA contract. It is set at initiation so that, under no-arbitrage, the FRA has zero value to both parties (ignoring bid–ask spreads and credit effects). Key Term: money market reference rate (MRR)

The annualized benchmark rate (for example, SOFR-based term rates, Euribor) used as the reference for the FRA and for deriving forward rates. Exam questions typically assume an actual/360 day-count unless stated otherwise. Key Term: settlement date (FRA)

The date when the FRA payoff is exchanged, based on the difference between the reference rate and the FRA rate. This is the start date of the underlying notional loan or deposit period. Key Term: notional principal

The face amount on which FRA interest differences are calculated. The notional itself is not exchanged; only interest differentials on the notional are. Key Term: day-count fraction

The ratio of the number of days in the relevant interest period to the day-count basis (for example, ), used to convert annualized rates into period rates. Key Term: reference rate (FRA)

The market interest rate observed at the FRA’s settlement, for the specific loan period referenced by the FRA. It determines the size and direction of the settlement payment. Key Term: forward rate (FRA context)

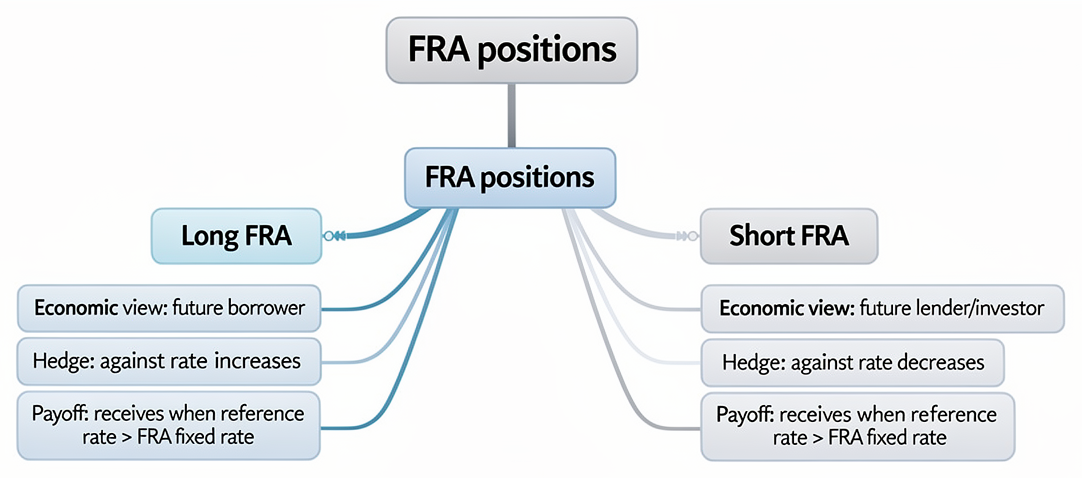

The no-arbitrage annualized rate for a future loan/deposit period implied by today’s term structure. For an FRA, it is the rate for the period from to months. Key Term: long FRA position

The party that benefits when the future reference rate rises above the FRA rate. Economically similar to a future borrower who wants to lock in a borrowing rate (benefits from higher rates). Key Term: short FRA position

The party that benefits when the future reference rate falls below the FRA rate. Economically similar to a future lender who wants to lock in an investment rate (benefits from lower rates).

In market notation, an FRA is described as an contract:

- = months until the start of the reference loan/deposit.

- = months until the end of the reference period.

- Loan/deposit tenor = months.

So a 2×8 FRA references a 6‑month (8 − 2) notional loan that starts in 2 months and ends in 8 months.

Exam questions sometimes mix month notation with day-based money market quotes. A quick way to organize is:

- Convert months into days (treat each month as 30 days unless the vignette specifies actual calendar days).

- Compute the day-count fraction or consistently.

A timeline helps organize the cash flows:

-

Today ():

- FRA is initiated.

- FRA rate is set so that the value is zero to both long and short.

-

Settlement date (, in months):

- Market observes the reference rate for the loan period.

- A single FRA cash flow is exchanged at (present value of the interest differential).

-

Loan maturity date (, in months):

- Any actual loan or deposit in the cash market settles interest.

A subtle but exam-relevant point is that:

- The underlying loan interest is paid at .

- The FRA payoff is paid at and equals the present value (at ) of that interest difference.

This mismatch in timing is exactly why discounting appears in the payoff formula.

FRAs are over-the-counter (OTC), bespoke contracts. There is no exchange of notional; instead, the parties cash-settle the present value of the interest difference. This is why FRAs are sometimes described as “forwards on interest” rather than forwards on principal.

For exam purposes, the essential skills are:

- Using no-arbitrage arguments to link FRA rates to the money market term structure.

- Translating notation into actual days and day-count fractions.

- Applying the correct payoff formula, including discounting to settlement.

- Marking FRAs to market using updated forward curves.

- Seeing FRAs as components of swaps and close substitutes for interest rate futures.

- Interpreting FRA values in light of yield curve shifts (steepening, flattening, inversion).

The following sections move from pricing and payoff logic to mark‑to‑market valuation and hedging applications, always with Level 2 exam mechanics in mind.

Test Tip: When revising FRA valuation and applications, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Exam Warning: Do not rely on keyword recognition alone; check the precise condition, exception, calculation step, or evidence the question requires.

FRA Pricing and Payoff Logic

An FRA fixes an interest rate today for a future short‑term loan or deposit. Instead of actually entering the future loan, the parties settle the present value of the interest differential at the start of the period.

At initiation, the FRA’s value is set to zero for both parties by choosing the FRA rate equal to the arbitrage‑free forward rate implied by the current term structure.

FRA notation and economic interpretation

Consider an FRA on notional :

- Loan/deposit period starts in months and ends in months.

- Loan period length in days: (for example, for about 3 months).

- FRA rate (fixed, annualized on a 360‑day basis): .

- Reference rate at settlement, for the ‑day period: .

Economic interpretation:

- A future borrower wants to hedge against rising rates, so takes the long FRA.

- A future lender (investor) wants to hedge against falling rates, so takes the short FRA.

If at settlement:

- Actual market borrowing is more expensive than the locked FRA rate.

- Long FRA receives a positive settlement amount that offsets the higher interest.

- Short FRA pays that amount.

If , the roles reverse.

You can think of an FRA as a forward contract on a single interest payment:

- Underlying “asset”: the interest payment at the end of the period.

- Forward “price”: .

- Realized “spot”: observed at settlement.

This is conceptually closer to a forward on a bond coupon than a forward on principal.

A critical exam distinction:

- FRA price: the rate (percentage per year).

- FRA value: the present value in currency terms, which is zero at initiation and then moves with the term structure.

Candidates often confuse “price” and “value”; always clarify which the question is asking for.

Pricing an FRA at initiation: deriving the forward rate

The FRA rate is chosen so that the contract has zero value at initiation. Under no-arbitrage, borrowing or lending via the FRA should be equivalent to replicating the same future loan using spot money market instruments.

Suppose the market provides annualized money market reference rates (actual/360):

- for days.

- for days, with .

Convert these quoted annualized rates to period yields (simple interest):

R_N = r_N \times \frac{N}{360}$$ The no-arbitrage simple forward rate over days $M$–$N$ is: $$R_{(M,N)} = \frac{1 + R_N}{1 + R_M} - 1$$ This is the non‑annualized rate over the $N - M$ day interval. Annualize it on a 360‑day basis to obtain the FRA rate: $$R_{\text{FRA}} = R_{(M,N)} \times \frac{360}{N - M}$$ This $R_{\text{FRA}}$ is the contract rate that makes the FRA’s initial value zero. #### Replicating-strategy intuition The no-arbitrage relationship is equivalent to equating two strategies: - Strategy A (synthetic loan from $M$ to $N$): - Lend \$1 today for $N$ days at rate $r_N$. - Borrow \$1 today for $M$ days at rate $r_M$. - Strategy B: - Commit today (via an FRA) to lend/borrow between $M$ and $N$ days at forward rate $R_{\text{FRA}}$. At $M$ days, the short-term borrowing matures; the long-term lending continues. The net result of Strategy A is a synthetic loan from $M$ to $N$ days. If $R_{\text{FRA}}$ differed from $R_{(M,N)}$, you could lock in an arbitrage profit by going long one strategy and short the other. Link to yield curve shape: - If the term structure is upward sloping ($r_N > r_M$), the annualized $R_{\text{FRA}}$ will typically lie between $r_M$ and $r_N$. - If the curve segment is inverted, $R_{\text{FRA}}$ will still be between the two spot rates, but with reversed ordering. This provides a quick reasonableness check on your computed FRA rate. > **Key Term: arbitrage-free forward rate (FRA context)** > The forward interest rate implied by current spot or discount rates that eliminates arbitrage opportunities. In an FRA, the arbitrage-free FRA rate set at initiation is this implied forward rate. ### Worked Example 1.1 – Pricing a 1×4 FRA A dealer quotes the following annualized MRRs (actual/360): - 30‑day MRR: 4.0% - 120‑day MRR: 5.0% Calculate the fair contract rate on a 1×4 FRA on a 90‑day reference loan (days 30–120). > **Answer:** > First compute period yields (simple interest): > > - 30‑day yield: > > $$> R_{30} = 0.04 \times \frac{30}{360} = 0.00333$$ > > - 120‑day yield: > > $$> R_{120} = 0.05 \times \frac{120}{360} = 0.01667$$ > > Next, derive the 90‑day forward yield from day 30 to day 120: > > $$> R_{(30,120)} = \frac{1 + R_{120}}{1 + R_{30}} - 1 > = \frac{1.01667}{1.00333} - 1 > \approx 0.0133$$ > > Annualize this 90‑day rate: > > $$> R_{\text{FRA}} = 0.0133 \times \frac{360}{90} > \approx 0.0532 = 5.32\%$$ > > A 1×4 FRA at 5.32% is fairly priced; its value to both long and short is zero, ignoring bid–ask spreads. From a process standpoint: - Convert quoted annual rates to period yields. - Use the forward-rate identity to extract $R_{(M,N)}$. - Re-annualize to a consistent quoting convention. Exam tip: If months (1×4) rather than days are given, treat each month as 30 days unless the question specifies actual day counts. #### Quick check: 3×5 FRA style problem The same logic applies when more than two spot rates are given. For example, a 3×5 FRA might be implied by: - 60‑day rate (2 months), 90‑day rate (3 months), and 150‑day rate (5 months). You must be careful to: - Use the correct pair of spot rates (start and end of the FRA period). - Ensure the day counts in the period yield calculations match the quoted tenors. Candidates often mistakenly use the 90‑day rate instead of the 150‑day rate when pricing a 3×5 FRA, which leads to a forward rate on the wrong segment of the curve. #### Alternative discount-factor formulation Sometimes the term structure is given via discount factors $P(0,T)$ rather than simple MRRs. The logic is identical. If: - $P(0,M)$ = discount factor to $M$ days. - $P(0,N)$ = discount factor to $N$ days. Then the simple forward rate for $M$–$N$ is: $$R_{(M,N)} = \frac{P(0,M)}{P(0,N)} - 1$$ The corresponding FRA rate (annualized on 360‑day basis) is: $$R_{\text{FRA}} = \left(\frac{P(0,M)}{P(0,N)} - 1\right) \times \frac{360}{N - M}$$ This discount-factor view is especially useful when linking FRAs to swap fixed rates, which are also derived from discount factors. ### FRA payoff at settlement At the settlement date ($T_s$), the reference rate $R_{\text{ref}}$ for the FRA’s loan period is observed. The FRA is then settled as a single payment at $T_s$. For a **long** FRA, the standard settlement payoff at $T_s$ is: $$\text{Payoff}_{\text{long}} = \frac{L \times (R_{\text{ref}} - R_{\text{FRA}}) \times \frac{D}{360}}{1 + R_{\text{ref}} \times \frac{D}{360}}$$ Interpretation of each element: - Numerator: undiscounted interest differential over the loan period: $$ L \times (R_{\text{ref}} - R_{\text{FRA}}) \times \frac{D}{360}.$$ This is how much more interest would be owed at the end of the period if the loan were at $R_{\text{ref}}$ instead of $R_{\text{FRA}}$ (positive when rates rise). - Denominator: discount factor from the end of the loan back to $T_s$, using the market rate $R_{\text{ref}}$ for that period. The **short** FRA payoff is just the negative: $$\text{Payoff}_{\text{short}} = -\text{Payoff}_{\text{long}}$$ #### Derivation of the payoff formula It is worth understanding the derivation so you can reconstruct the formula under pressure. - Suppose the firm borrows $L$ at $R_{\text{ref}}$ for $D$ days. Interest due at the end of the period is: $$ \text{Interest}_{\text{market}} = L \times R_{\text{ref}} \times \frac{D}{360}.$$ - If instead the firm could have borrowed at the FRA rate $R_{\text{FRA}}$, interest would be: $$ \text{Interest}_{\text{fixed}} = L \times R_{\text{FRA}} \times \frac{D}{360}.$$ - The difference at the end of the period is: $$ \Delta \text{Interest} = L \times (R_{\text{ref}} - R_{\text{FRA}}) \times \frac{D}{360}.$$ - FRA convention: this difference is settled at the **beginning** of the loan period ($T_s$). Call $X$ the settlement payment at $T_s$ to the long FRA. Growing $X$ at the market rate $R_{\text{ref}}$ over the period must equal $\Delta \text{Interest}$: $$ X \left(1 + R_{\text{ref}} \times \frac{D}{360} \right) = \Delta \text{Interest}.$$ Solving for $X$ yields: $$ X = \frac{L \times (R_{\text{ref}} - R_{\text{FRA}}) \times \frac{D}{360}} {1 + R_{\text{ref}} \times \frac{D}{360}}.$$ Why discount at $R_{\text{ref}}$? Because this is the prevailing market rate for the cash flows over the loan period at the time the payoff is determined. Conceptually, the FRA is paying/receiving the **present value** of a future interest differential. > **Exam warning on discounting:** A common mistake is to use only the interest difference (numerator) and forget the denominator. That overstates the payoff. If your calculated FRA payoff equals the undiscounted interest differential, you have not discounted correctly. If the question uses a different day-count basis (for example, actual/365), replace $D/360$ with $D/365$ accordingly. ### Worked Example 1.2 – FRA settlement payoff when rates rise A company enters a \$10 million 2×8 FRA at 4.2% (a 6‑month loan starting in 2 months). At settlement, the 6‑month reference rate is 5.0%. Assume 180 days in the accrual period on an actual/360 basis. Compute the settlement value to the FRA long. > **Answer:** > Inputs: > > - $L = 10{,}000{,}000$ > - $R_{\text{FRA}} = 4.2\% = 0.042$ > - $R_{\text{ref}} = 5.0\% = 0.050$ > - $D = 180$, so $D/360 = 0.5$ > > Compute the payoff: > > $$> \text{Payoff}_{\text{long}} = > \frac{10{,}000{,}000 \times (0.050 - 0.042) \times 0.5} > {1 + 0.050 \times 0.5} > = \frac{10{,}000{,}000 \times 0.008 \times 0.5}{1.025}$$ > > $$> = \frac{40{,}000}{1.025} > \approx 39{,}024$$ > > The long FRA receives about \$39,024 at settlement. You can sanity-check: - Rate differential = 0.8% per year. - On \$10 million for half a year, undiscounted difference ≈ \$40,000. - Discounting reduces this slightly, so a payoff just below \$40,000 is reasonable. ### Worked Example 1.3 – FRA settlement payoff when rates fall A bank is short a \$5 million 3×6 FRA at 3.5% on a 90‑day reference period. At settlement, the 3‑month reference rate is 2.8%. Assume 90 days on an actual/360 basis. Compute the settlement amount to the short position. > **Answer:** > The short FRA benefits when $R*{\text{ref}} < R*{\text{FRA}}$. > Inputs: > > - $L = 5{,}000{,}000$ > - $R_{\text{FRA}} = 3.5\% = 0.035$ > - $R_{\text{ref}} = 2.8\% = 0.028$ > - $D = 90$, so $D/360 = 0.25$ > > Compute the long payoff first: > > $$> \text{Payoff}_{\text{long}} = > \frac{5{,}000{,}000 \times (0.028 - 0.035) \times 0.25} > {1 + 0.028 \times 0.25}$$ > > $$> = \frac{5{,}000{,}000 \times (-0.007) \times 0.25}{1.007} > = \frac{-8{,}750}{1.007} \approx -8{,}689$$ > > Therefore: > > $$> \text{Payoff}_{\text{short}} = +8{,}689$$ > > The short FRA receives about \$8,689. ### Long vs short FRA: economic intuition Candidates often flip the signs under time pressure. Anchor your understanding in economic intuition: - Long FRA: - Equivalent to being a **future borrower** who wants to lock in a borrowing rate. - Gains when $R_{\text{ref}} > R_{\text{FRA}}$ (rates rise). - Receives a payoff that offsets higher market borrowing costs. - Short FRA: - Equivalent to being a **future lender/investor** who wants to lock in a lending rate. - Gains when $R_{\text{ref}} < R_{\text{FRA}}$ (rates fall). - Receives a payoff that compensates for lower market investment returns. A useful memory aid: - Long FRA ≈ long the rate (benefits when rates go up). - Short FRA ≈ short the rate (benefits when rates go down). If your computed payoff sign contradicts this intuition, recheck the algebra and which side of the contract you are valuing. ### Approximate vs exact settlement formulas Sometimes an approximate payoff formula that ignores discounting is shown: $$\text{Approximate payoff} \approx L \times (R_{\text{ref}} - R_{\text{FRA}}) \times \frac{D}{360}.$$ This is just the numerator of the exact formula. For short periods and moderate rates the error is small, but the curriculum emphasizes the exact discounted formula. Unless a question explicitly tells you to ignore discounting, use the exact version. Rule of thumb: - For a 90‑day FRA at about 5%, the discount factor is roughly $1/(1 + 0.05 \times 0.25) \approx 0.988$. - Ignoring discounting overstates the payoff by about 1–1.5%. In a tight multiple-choice setting, that difference can separate two plausible answer options. ### Mark-to-Market Valuation of FRAs After initiation and before settlement, the FRA’s value may move away from zero as interest rate expectations change. Conceptually, an outstanding FRA is like holding a “locked-in” forward rate $R_{\text{FRA}}$ while the market’s current forward rate for the same period, $R^{\text{new}}_F$, drifts up and down.  _Long and short FRA exposures are mapped to future borrowing or lending needs and the corresponding payoff direction from rate changes._ > **Key Term: mark-to-market value (of an FRA)** > The current value of an existing FRA, calculated as the present value of the expected settlement payment based on current forward rates and discount factors. Key Level 2 capabilities: - Value an FRA **at settlement** using the realized reference rate. - Value an FRA **prior to settlement** by: - Computing a **new** FRA rate from current money market rates. - Using that rate as the best estimate of the future reference rate. - Discounting the implied settlement payoff back to today. ### General mark-to-market valuation framework Notation: - $t$ = valuation date (between initiation and settlement). - $T_s$ = settlement date (start of loan). - $T_e$ = loan maturity date (end of loan). - $D$ = days from $T_s$ to $T_e$ (loan length). - $\tau$ = days from $t$ to $T_s$. - $L$ = notional principal. - $R_{\text{FRA}}$ = original FRA rate. - $R^{\text{new}}_{F}$ = current fair forward rate for $T_s$–$T_e$. - $r_\tau$ = appropriate money market rate from $t$ to $T_s$. Under risk‑neutral pricing, $R^{\text{new}}_F$ is the market’s best estimate of the rate that will fix at $T_s$. Two-step valuation for the **long** FRA: - Step 1 – Expected payoff at $T_s$ (using $R^{\text{new}}_F$ in place of the unknown $R_{\text{ref}}$): $$ \text{Expected payoff at }T_s \approx \frac{L \times (R^{\text{new}}_{F} - R_{\text{FRA}}) \times \frac{D}{360}} {1 + R^{\text{new}}_{F} \times \frac{D}{360}}.$$ - Step 2 – Discount this payoff back from $T_s$ to today: $$ V_t \approx \frac{L \times (R^{\text{new}}_{F} - R_{\text{FRA}}) \times \frac{D}{360}} {\left(1 + R^{\text{new}}_{F} \times \frac{D}{360}\right) \left(1 + r_{\tau} \times \frac{\tau}{360}\right)}.$$ Sign interpretation: - If $R^{\text{new}}_{F} > R_{\text{FRA}}$, the long has locked in a borrowing rate below the current forward rate → the FRA is an asset to the long ($V_t > 0$). - If $R^{\text{new}}_{F} < R_{\text{FRA}}$, the long is stuck with a relatively high locked-in rate → the FRA is a liability to the long ($V_t < 0$). The short’s mark‑to‑market value is $-V_t$. In exam problems, you often see a simplification where the same rate is used to discount from $T_e$ to $T_s$ and from $T_s$ to $t$, or where discounting is done over $D + \tau$ days in one step. #### Discount-factor view of FRA mark-to-market You can also think in terms of discount factors $P(t,T)$ at time $t$: - $P(t,T)$ = price of a zero-coupon bond paying 1 at time $T$. - The no-arbitrage forward rate for $T_s$–$T_e$ at time $t$ is: $$ R^{\text{new}}_F = \left(\frac{P(t,T_s)}{P(t,T_e)} - 1\right) \times \frac{360}{D}.$$ The value of an existing FRA that locks $R_{\text{FRA}}$ is equal to the difference between: - The PV of paying floating (with expected rate $R^{\text{new}}_F$) over $T_s$–$T_e$, and - The PV of paying fixed $R_{\text{FRA}}$ over that same period, multiplied by $L$. This is exactly analogous to valuing one period of a swap and provides an intuitive bridge to swap valuation. ### Worked Example 1.4 – Simple mark-to-market valuation Revisit the FRA in Example 1.2 (\$10 million notional, 2×8 FRA at 4.2% on a 180‑day period). Thirty days after initiation: - There are 60 days to settlement ($\tau = 60$). - The fair 6‑month forward rate for months 2–8 is now 4.6%. - Assume 180 days in the loan period ($D = 180$) and use 4.6% as both the expected reference rate and the discount rate for simplicity. What is the approximate value of the FRA to the long? > **Answer:** > Use the new forward rate as the expected reference rate. > Step 1 – Expected payoff at settlement: > > $$> \text{Payoff at }T_s \approx > \frac{10{,}000{,}000 \times (0.046 - 0.042) \times 0.5} > {1 + 0.046 \times 0.5}$$ > > $$> = \frac{10{,}000{,}000 \times 0.004 \times 0.5}{1.023} > = \frac{20{,}000}{1.023} \approx 19{,}551$$ > > Step 2 – Discount 60 days back to today: > > $$> V_t \approx \frac{19{,}551} > {1 + 0.046 \times \frac{60}{360}} > = \frac{19{,}551}{1.00767} > \approx 19{,}401$$ > > The FRA is now worth about \$19,400 to the long. Originally, the FRA rate was 4.2%. With the forward rate having risen to 4.6%, the long has locked in a favorable borrowing rate below market, so the FRA has positive value to the long. ### More rigorous valuation before settlement In a more realistic setting, the term structure between today and $T_s$ is non‑flat, and you are given several money market rates. A typical procedure: - Use current short- and longer-dated MRRs to derive a **new** forward rate for the FRA period (for a loan starting at $T_s$ and ending at $T_e$). - Use that new forward rate as $R^{\text{new}}_F$ in the payoff formula. - Discount the payoff from $T_e$ back to $t$, potentially in two steps (via $T_s$). This is exactly the logic implemented in the official curriculum example, and it is heavily tested. ### Worked Example 1.5 – Valuing a 1×4 FRA before settlement Revisit the fairly priced 1×4 FRA of Example 1.1: contract rate 5.32% on a \$1,000,000 notional. Ten days after initiation: - The FRA will now start in 20 days and still cover a 90‑day loan (days 20–110). - Annualized MRRs (actual/360) are: - 20‑day MRR: 5.7% - 110‑day MRR: 5.9% Find the value of the FRA to the long 10 days after initiation. > **Answer:** > Step 1 – Compute the new fair FRA rate for a 90‑day loan starting in 20 days. > Convert to period yields: > > $$> R_{20} = 0.057 \times \frac{20}{360} = 0.00317$$ > > $$> R_{110} = 0.059 \times \frac{110}{360} \approx 0.01803$$ > > Forward yield for days 20–110: > > $$> R_{(20,110)} = \frac{1 + R_{110}}{1 + R_{20}} - 1 > = \frac{1.01803}{1.00317} - 1 \approx 0.01481$$ > > Annualized forward rate: > > $$> R^{\text{new}}_{\text{FRA}} = 0.01481 \times \frac{360}{90} > \approx 0.0592 = 5.92\%$$ > > Step 2 – Interest differential at loan maturity (day 110): > > $$> \Delta \text{Interest} > = (0.0592 - 0.0532) \times \frac{90}{360} \times 1{,}000{,}000 > \approx 0.0060 \times 0.25 \times 1{,}000{,}000 > = 1{,}500$$ > > Step 3 – Discount this \$1,500 back 110 days at 5.9%: > > $$> V_t \approx > \frac{1{,}500}{1 + 0.059 \times \frac{110}{360}} > \approx \frac{1{,}500}{1.0180} > \approx 1{,}473$$ > > The FRA has a positive value of about \$1,470 to the long. Note that rising forward rates (5.92% vs the locked 5.32%) make the FRA valuable to a long (future borrower). ### Worked Example 1.6 – FRA value when forward rates fall A firm is long a \$2 million 2×5 FRA at 4.0% on a 90‑day reference period. Forty days after initiation: - 20 days remain to settlement ($\tau = 20$). - The 90‑day forward rate for the period starting in 20 days is 3.2%. - Assume this 3.2% rate is used for both expected reference rate and discounting. Compute the approximate mark‑to‑market value of the FRA to the long. > **Answer:** > Lower current forward rates relative to the FRA rate hurt the long. > Inputs: > > - $L = 2{,}000{,}000$ > - $R_{\text{FRA}} = 4.0\% = 0.040$ > - $R^{\text{new}}_F = 3.2\% = 0.032$ > - $D = 90$, so $D/360 = 0.25$ > > Step 1 – Expected payoff at settlement: > > $$> \text{Payoff at }T_s \approx > \frac{2{,}000{,}000 \times (0.032 - 0.040) \times 0.25} > {1 + 0.032 \times 0.25}$$ > > $$> = \frac{2{,}000{,}000 \times (-0.008) \times 0.25}{1.008} > = \frac{-4{,}000}{1.008} \approx -3{,}968$$ > > Step 2 – Discount back 20 days: > > $$> V_t \approx > \frac{-3{,}968}{1 + 0.032 \times \frac{20}{360}} > \approx \frac{-3{,}968}{1.00178} > \approx -3{,}961$$ > > The FRA is worth roughly –\$4,000 to the long (and +\$4,000 to the short). ### FRA valuation at settlement vs before settlement Do not confuse two distinct situations: - At settlement ($t = T_s$): - Use the observed reference rate $R_{\text{ref}}$. - Compute $\text{Payoff}_{\text{long}}$ using the settlement payoff formula. - Only one discounting step—from end of loan ($T_e$) back to settlement ($T_s$). - Before settlement ($t < T_s$): - Compute a **new** forward rate $R^{\text{new}}_F$ for the $T_s$–$T_e$ period. - Plug $R^{\text{new}}_F$ into the payoff formula as a proxy for the unknown $R_{\text{ref}}$. - Discount resulting payoff back from $T_e$ to $T_s$ and then from $T_s$ to $t$ (often combined into a single factor). Question wording often signals which case applies: - “At settlement,” “at expiration of the FRA,” or “at contract maturity” → use $R_{\text{ref}}$ and the settlement formula. - “X days after initiation” or “value the FRA today” → do a mark‑to‑market valuation using a new forward rate. A very common exam trap is to use $R_{\text{ref}}$ when the question is clearly about valuation **before** settlement, or to skip the forward-rate recomputation step. ### FRA sensitivity to yield-curve shifts Because the FRA payoff depends on $R_{\text{ref}}$ (or $R^{\text{new}}_F$ before settlement), FRA value is highly sensitive to changes in the relevant segment of the yield curve: - A **parallel upward shift** in the curve typically increases the value of a long FRA (future borrower) and decreases the value of a short FRA, for FRAs referencing that segment. - A **non-parallel move** (steepening or flattening) matters only for the specific start/end of the FRA period. A steepening driven by higher long-term rates might have little effect on a near-term 1×4 FRA. Conceptually, one can think of an FRA as having a “DV01” (dollar value of a one basis point change) similar to a short-duration interest rate swaplet. Although you are not required to compute DV01 for FRAs in the exam, understanding that FRA values change approximately linearly with small rate moves helps interpret mark-to-market results. ### Revision tip: decoding the question When you see an FRA in the item set, quickly ask: - What is the timeline? Am I at $t = 0$, $t = T_s$, or some $t$ in between? - Which rate is which? - FRA rate $R_{\text{FRA}}$ (contract rate). - Reference rate $R_{\text{ref}}$ (observed at settlement). - New forward rate $R^{\text{new}}_F$ (used for early valuation). - Is the question asking for: - The FRA **rate** at initiation? - The **cash settlement** amount (who pays whom)? - The **mark-to-market value** of the outstanding FRA? Finally, check your answer’s **direction**: - If the question says rates have risen, a long FRA should now be better off than at inception. - If the question says rates have fallen, a short FRA should be better off. If your computed sign does not match that basic pattern, revisit the inputs. ### FRAs, Forwards, Futures, and Swaps — Comparison FRAs sit in the broader family of forward commitments: - A standard forward on an asset (equity index, bond, commodity): - Locks in a future **price** for an asset. - Usually involves delivery (physical or cash) of the asset or its equivalent at maturity. - An FRA: - Locks in a future **interest rate** on a notional principal. - No exchange of principal; only the discounted interest differential is exchanged at the start of the period. Valuation commonality: - Forward contracts and FRAs are both valued as the present value of the difference between a locked-in term (price or rate) and the **current** fair forward price or rate. ### FRAs vs interest rate futures Interest rate futures, particularly Eurodollar futures, are the exchange-traded cousins of FRAs. > **Key Term: Eurodollar futures** > A standardized futures contract on a 3‑month USD deposit, quoted as 100 minus the annualized 3‑month interest rate. It reflects market expectations of future short-term interest rates and serves as a liquid proxy for FRAs. Similarities between FRAs and interest rate futures: - Both reflect expectations of future short-term rates. - Both can hedge future borrowing or investing over short horizons. - Both are priced at initiation so that the contract’s initial value is (approximately) zero. Key differences: - Trading venue and standardization: - FRAs: OTC, customizable maturities, tenors, and notionals. - Futures: exchange-traded, standardized contract sizes and maturities. - Credit risk and margin: - FRAs: bilateral credit risk; payoff occurs on a single future date; no daily margining. - Futures: guaranteed by a clearinghouse; daily marking to market with margin requirements; greatly reduced counterparty risk. - Cash-flow timing: - FRAs: one settlement cash flow at the start of the reference period. - Futures: daily gains/losses realized; the economic effect depends on the path of rates because gains/losses are reinvested or funded daily. - Quotation conventions: - FRA: quoted directly as an annualized interest rate (for example, 3.80%). - Eurodollar futures: quoted as a price: $$ \text{Futures price} = 100 - \text{implied 3-month rate}.$$ > **Key Term: convexity bias (FRA vs futures)** > The small difference between forward rates implied by interest rate futures and by FRAs, arising because futures are marked to market daily while FRAs settle once. Under positive correlation between rates and reinvestment opportunities, futures-implied rates tend to be slightly higher than FRA rates. Qualitatively: - In a world where rates are stochastic and correlated with the mark‑to‑market process, the futures-implied forward rate is biased upward relative to the true forward rate; this is the convexity bias. For exam purposes, you only need the qualitative direction, not the exact numerical adjustment. Hedging direction: - Long Eurodollar futures gains when the implied forward rate rises (futures price falls), mirroring a long FRA. - Short Eurodollar futures gains when the implied rate falls (futures price rises), mirroring a short FRA. In practice, dealers often hedge FRA books with interest rate futures. For Level 2, focus on: - Reading a futures quote as an implied forward rate. - Understanding that this implied rate approximates the FRA rate, subject to convexity bias. ### Worked Example 1.7 – Linking a Eurodollar futures quote to an FRA rate A 3‑month Eurodollar futures contract maturing in six months is quoted at 95.80. Ignoring convexity effects, what is the implied 6×9 FRA rate? > **Answer:** > Eurodollar futures are quoted as: > > $$> \text{Price} = 100 - \text{annualized rate}$$ > > So a price of 95.80 implies: > > $$> \text{Implied rate} = 100 - 95.80 = 4.20\%$$ > > The futures market implies a 3‑month reference rate of about 4.20% in six months’ time. Ignoring convexity bias, this is approximately the fair 6×9 FRA rate. ### FRAs and swaps: strip interpretation > **Key Term: interest rate swap** > A derivative where two parties exchange fixed and floating interest payments on a notional principal over multiple reset periods. In a fixed-for-floating swap, the fixed rate is set so the swap has zero value at initiation. > **Key Term: strip of FRAs** > A sequence of FRAs, each covering one reset period of a swap, with the same fixed rate and successive start and end dates. A plain‑vanilla fixed-for-floating swap with: - Notional $L$. - Payment dates $T_1, T_2, \ldots, T_n$. - Fixed rate $R_{\text{swap}}$. can be decomposed into a strip of FRAs: - Each FRA covers period $T_{i-1}$–$T_i$. - Each has fixed rate $R_{\text{swap}}$. - Each settles at $T_{i-1}$ using the newly set floating rate for $T_{i-1}$–$T_i$. At each reset date: - The floating rate for the next period is set. - The net payment on the swap (fixed minus floating, or vice versa) over that period equals the payoff on a FRA that fixed the floating rate at $R_{\text{swap}}$ for that period. Summing the PVs of all those FRA-like payments gives the swap’s value. ### Worked Example 1.8 – Swap payment as an FRA payoff You enter a 3‑year quarterly fixed-for-floating swap with: - Notional \$50 million. - Fixed rate 3.5% (annual, actual/360). - Floating leg referenced to 3‑month LIBOR (actual/360). At the end of year 1, the 3‑month LIBOR fixing for the next quarter is 4.1%; the accrual period is 90 days. Show how the next net swap payment relates to a FRA payoff. > **Answer:** > For the quarter starting at year 1: > > - Fixed interest: > > $$> \text{Fixed} = 0.035 \times \frac{90}{360} \times 50{,}000{,}000 > = 0.035 \times 0.25 \times 50{,}000{,}000 > = 437{,}500$$ > > - Floating interest: > > $$> \text{Floating} = 0.041 \times \frac{90}{360} \times 50{,}000{,}000 > = 0.041 \times 0.25 \times 50{,}000{,}000 > = 512{,}500$$ > > Net payment (payer‑fixed, receiver‑floating swap): > > $$> \text{Net} = \text{Floating} - \text{Fixed} = 75{,}000$$ > > Now view this as a FRA payoff: > > - Notional $L = 50{,}000{,}000$ > - FRA fixed rate $R*{\text{FRA}} = R*{\text{swap}} = 3.5\%$ > - Reference rate $R_{\text{ref}} = 4.1\%$ > - Period $D = 90$ days > > Interest differential at period end: > > $$> L \times (R_{\text{ref}} - R_{\text{FRA}}) \times \frac{D}{360} > = 50{,}000{,}000 \times 0.006 \times 0.25 > = 75{,}000$$ > > This is exactly the net swap payment due at the end of the quarter. If valued **before** the quarter begins, this amount would be discounted back to the reset date, just as with a FRA payoff. Thus, a fixed-for-floating swap is economically equivalent to a strip of FRAs, one for each reset period, all with the same fixed rate. ### FRAs vs swaps: practical distinctions Even though a swap can be decomposed into FRAs, there are practical distinctions: - A swap fixes a single rate for multiple future periods, leading to a smoother exposure over time. - A series of FRAs (especially if entered sequentially rather than up front) could involve different fixed rates for different periods and more operational complexity. - Credit exposure: - A swap presents multi-period bilateral exposure. - Individual FRAs might be traded with different counterparties, or some periods might be left unhedged. For Level 2, focus on: - The conceptual equivalence: swap = strip of FRAs. - Using forward rates and discount factors to derive a **par swap rate**, which is analogous to the FRA rate at which the strip has zero value at initiation. ### Common Applications of FRAs FRAs are widely used for: - Hedging known future borrowings or investments. - Locking in reinvestment rates for known cash inflows (coupon receipts, bond redemptions). - Managing discrete segments of interest rate exposure within a broader portfolio. - Speculating on interest rate movements or yield curve shape. Most exam applications fall into hedging future borrowing or investing. > **Key Term: basis risk (FRA hedging)** > The risk that the interest rate underlying the FRA does not move perfectly in line with the rate on the exposure being hedged (due to different benchmarks, tenors, or timing), leading to an imperfect hedge. ### Hedging a future borrowing A firm that knows it will borrow a certain amount at a future date faces the risk of higher rates. To hedge: - Take a **long FRA** covering the future borrowing period. - If rates rise: - The loan will be more expensive in the cash market. - The FRA long receives a payment that offsets the higher borrowing cost. - If rates fall: - The loan is cheaper. - The firm pays on the FRA, giving up some savings but having effectively locked in a pre‑agreed rate. Timing and notional alignment: - The FRA should be an $M \times N$ contract where: - $M$ ≈ time until the borrowing starts. - $N - M$ ≈ planned loan tenor. - The FRA notional should match (or approximate) the future borrowing amount. In the curriculum, you generally assume **no basis risk** unless the item set describes a mismatch between the FRA’s reference rate and the actual borrowing rate. ### Hedging a future investment A firm expecting to invest cash in the future faces the risk that deposit or money market rates may **fall**. To hedge: - Take a **short FRA** covering the future investment period. - If rates fall: - The firm earns less on its deposit. - The short FRA receives a payment that compensates for the lower return. - If rates rise: - The deposit earns more. - The firm pays on the FRA, giving up some upside. Again, match the $M \times N$ structure and notional to the timing and size of the exposure. ### Worked Example 1.9 – Hedging a future borrowing with a long FRA A CFO expects to borrow \$15 million for 90 days starting in 60 days. The current term structure implies a fair 2×5 FRA rate of 3.8%. The CFO wants to lock in this rate. At FRA settlement (in 60 days), the actual 90‑day reference rate is 5.0%. Ignoring basis risk, what is the effect of the hedge? > **Answer:** > The firm is a future borrower and fears **rising** rates, so it should take a **long** 2×5 FRA at 3.8%. > Without the hedge: > > - Borrow \$15 million for 90 days at the market rate 5.0%. > - Interest cost: > > $$> 0.050 \times \frac{90}{360} \times 15{,}000{,}000 > = 187{,}500$$ > > With the hedge: > > - Same loan at 5.0% in the money market. > - FRA payoff to the long: > > $$> \text{Payoff}_{\text{long}} = > \frac{15{,}000{,}000 \times (0.050 - 0.038) \times 0.25} > {1 + 0.050 \times 0.25}$$ > > $$> = \frac{15{,}000{,}000 \times 0.012 \times 0.25}{1.0125} > = \frac{45{,}000}{1.0125} > \approx 44{,}444$$ > > Effective borrowing cost (roughly) is: > > - Actual interest paid: 187,500. > - Less FRA receipt (PV of interest savings): 44,444. > > Adjusting for discounting, this is approximately equivalent to borrowing at 3.8% instead of 5.0%. The long FRA successfully hedges the borrowing against rate increases. In exam questions, you typically only need to identify the correct position (long FRA) and compute the settlement, not the precise effective borrowing rate. ### Worked Example 1.10 – Hedging a future investment with a short FRA An asset manager expects to receive \$8 million in 3 months and to invest it for 6 months. Current annualized MRRs (actual/360) are: - 3‑month (90 days): 2.2% - 9‑month (270 days): 3.0% The manager wants to lock in the 6‑month investment rate for months 3–9 using a single FRA. 1. Determine the appropriate FRA position and contract rate. 2. Evaluate the hedge if the 6‑month reference rate set at settlement is 1.8%. > **Answer:** > Step 1 – FRA position and rate. > > - The cash will be **invested**, so the manager fears **falling** rates → take a **short** FRA. > - The relevant contract is a 3×9 FRA (months 3–9). > > Compute the arbitrage-free FRA rate from 3‑ and 9‑month MRRs: > > - $M = 90$ days, $N = 270$ days. > - $r_3 = 2.2\%$, $r_9 = 3.0\%$. > - Period yields: > > $$> R_{90} = 0.022 \times \frac{90}{360} = 0.0055$$ > > $$> R_{270} = 0.030 \times \frac{270}{360} = 0.0225$$ > > - Forward yield for days 90–270: > > $$> R_{(90,270)} = \frac{1.0225}{1.0055} - 1 \approx 0.0169$$ > > - Annualized FRA rate for 180 days: > > $$> R_{\text{FRA}} = 0.0169 \times \frac{360}{180} > \approx 0.0338 = 3.38\%$$ > > So the manager should short a 3×9 FRA at about 3.38%. > Step 2 – Outcome if the 6‑month rate at settlement is 1.8%. > At settlement: > > - $R_{\text{ref}} = 1.8\% = 0.018$ > - $R_{\text{FRA}} = 3.38\% = 0.0338$ > - $L = 8{,}000{,}000$ > - $D = 180$, so $D/360 = 0.5$ > > Long FRA payoff: > > $$> \text{Payoff}_{\text{long}} = > \frac{8{,}000{,}000 \times (0.018 - 0.0338) \times 0.5} > {1 + 0.018 \times 0.5} > \approx \frac{-63{,}200}{1.009} > \approx -62{,}642$$ > > Short FRA payoff: > > $$> \text{Payoff}_{\text{short}} \approx +62{,}642$$ > > The actual 6‑month investment earns only 1.8%, but the FRA payoff of about \$62,600 compensates for much of the shortfall versus the locked 3.38% rate. The short FRA hedge is effective against the rate decline. ### Other FRA applications and yield-curve trades Beyond single-period hedging, FRAs can be used for: - **Reinvestment risk management**: Locking the reinvestment rate on coupons or principal repayments expected at future dates. - **Partial hedging of floating-rate exposures**: Hedging only one upcoming reset period on a floating-rate loan, instead of entering a full swap. - **Curve trades**: Taking offsetting positions in FRAs on different segments of the yield curve to express views on steepening or flattening. For example: - Long a near-term FRA and short a longer-term FRA to bet on steepening. - Short the near-term FRA and long the longer-term FRA to bet on flattening. These applications are conceptually straightforward once you are comfortable with FRA payoff direction and its link to forward rates. ### FRA vs caps, floors, and swaptions (conceptual link) While not central to the FRA learning objective, it helps to recognize that: - An interest rate **cap** is a portfolio of call options on future reference rates (caplets). Each caplet payoff resembles that of a long FRA when rates exceed a cap strike. - An interest rate **floor** is a portfolio of put options on reference rates (floorlets), analogous to short FRA payoffs when rates fall below a floor strike. - A **swaption** (option on a swap) can be thought of as an option on a strip of FRAs. Conceptually: - Long cap ≈ synthetic protection against rate increases (similar motivation to a long FRA for a borrower). - Long floor ≈ synthetic protection against rate decreases (similar motivation to a short FRA for an investor). The exam may ask you to recognize these equivalences qualitatively; the pricing of caps/floors and swaptions is handled elsewhere in the curriculum. ### Summary of hedging directions Quick reference: - Future borrower → **long FRA**. - Future lender/investor → **short FRA**. If you are unsure, restate the hedging objective in plain language: - “I worry that borrowing costs might be higher than I would like” → take long FRA. - “I worry that investment income might be lower than I would like” → take short FRA. ### Exam warning: directional confusion and notation Common mistakes: - Confusing “long the loan” (a borrower) with “long the FRA rate.” - A borrower suffers if rates rise; the long FRA gains. - The FRA is a hedge precisely because its payoff has opposite sign to the loan’s interest sensitivity. - Misreading $M \times N$ notation: - $M$ is months to the **start** of the period. - $N$ is months to the **end**. - Period length is $N - M$ months. - Mixing up FRA rate vs reference rate vs forward rate at valuation time. - Forgetting to convert months into days when using $D/360$. - Failing to specify who pays whom at settlement. Tie your final answer back to the economic direction: “long wins if rates rise, short wins if rates fall.” ## Summary - An FRA is a forward contract on a future interest payment: it fixes a rate today for a notional loan/deposit over a future period. - In market notation, an $M \times N$ FRA references a loan period from $M$ to $N$ months. The loan tenor is $N - M$ months. - The **FRA rate** at initiation is set equal to the **arbitrage-free forward rate** implied by the money market term structure: - Use spot MRRs or discount factors to derive the forward simple rate for the period. - Re-annualize on the relevant day-count basis (usually 360). - This ensures the FRA’s initial value is zero to both parties. - At **settlement**, the reference rate $R_{\text{ref}}$ is observed; the FRA payoff to the long is: $$ \text{Payoff}_{\text{long}} = \frac{L \times (R_{\text{ref}} - R_{\text{FRA}}) \times \frac{D}{360}} {1 + R_{\text{ref}} \times \frac{D}{360}},$$ with the short receiving the negative of this amount. - The long FRA benefits when $R_{\text{ref}} > R_{\text{FRA}}$ (rates rise); the short benefits when $R_{\text{ref}} < R_{\text{FRA}}$ (rates fall). - **Before settlement**, the mark-to-market value of a FRA is the present value of the expected settlement payoff, computed using the **current forward rate** for the FRA period: - Compute a new forward rate $R^{\text{new}}_F$ for the remaining FRA period. - Plug $R^{\text{new}}_F$ into the settlement payoff formula in place of $R_{\text{ref}}$. - Discount back to the valuation date. - FRAs are intimately related to other interest rate derivatives: - They share pricing logic with standard forwards (no-arbitrage forward pricing). - They are closely related to interest rate futures such as Eurodollar futures; futures-implied forward rates approximate FRA rates, with a small **convexity bias**. - A plain‑vanilla fixed-for-floating interest rate swap can be viewed as a **strip of FRAs**, one for each reset period, all at the swap fixed rate. - FRAs are powerful tools for hedging: - Future borrowers hedge with **long FRAs**. - Future lenders/investors hedge with **short FRAs**. - Basis risk arises if the FRA’s reference rate, tenor, or timing does not perfectly match the underlying exposure. - Typical exam pitfalls include: - Misinterpreting $M \times N$ notation and the timing of the underlying loan. - Confusing FRA rate, reference rate, and current forward rate. - Omitting the **discounting** in the payoff formula and using only the interest difference. - Using incorrect day-count fractions (30/360 vs actual/360) or inconsistent bases. - Assigning the settlement payment to the wrong side (long vs short). - Conceptual understanding of FRAs, including their link to swaps and futures and to changes in the term structure, is essential for applying derivative valuation tools across the Level 2 curriculum. ## Key Point Checklist _This article has covered the following key knowledge points:_ - FRA notation ($M \times N$), timeline, and the economic meaning of long and short positions. - Pricing FRAs at initiation from money market reference rates or discount factors using no-arbitrage forward-rate relationships. - Deriving and applying the FRA settlement payoff formula, including proper discounting to the settlement date with the reference rate. - Mark-to-market valuation of FRAs before settlement using updated forward rates and money market discount factors. - Interpreting how the sign and magnitude of FRA values change when the yield curve shifts. - Using FRAs to hedge future borrowing and investing exposures: - Long FRA to hedge future borrowing. - Short FRA to hedge future lending/investment. - Recognizing and managing basis risk when FRA terms do not perfectly match the underlying exposure. - Understanding the relationships among FRAs, interest rate futures (especially Eurodollar futures), and swaps: - FRA vs futures pricing and convexity bias. - Viewing a fixed-for-floating swap as a strip of FRAs. - Avoiding common exam errors: - Misreading $M \times N$. - Confusing FRA, reference, and forward rates. - Ignoring discounting in settlement calculations. - Mis-assigning payoff direction between long and short. - Integrating FRA valuation with broader term-structure concepts (spot rates, forward rates, discount factors) and yield-curve interpretation. ## Key Terms and Concepts - forward rate agreement (FRA) - FRA rate - money market reference rate (MRR) - settlement date (FRA) - notional principal - day-count fraction - reference rate (FRA) - forward rate (FRA context) - long FRA position - short FRA position - arbitrage-free forward rate (FRA context) - mark-to-market value (of an FRA) - Eurodollar futures - convexity bias (FRA vs futures) - interest rate swap - strip of FRAs - basis risk (FRA hedging)