Learning Outcomes

This article explains how to value plain vanilla interest rate swaps using discount factors and zero-coupon curves, enabling you to determine the fair fixed rate at initiation and confirm that the swap's initial market value is zero. It explains how to decompose swap structures into fixed and floating legs, map each leg’s periodic cash flows to specific settlement dates, and construct a complete payment schedule suitable for exam-style questions and spreadsheet implementation. It also explains how to revalue an existing swap after interest rates move, calculate its mark-to-market value from the standpoint of either the fixed-rate payer or receiver, and interpret how changes in the yield curve affect each leg's present value. In addition, this article explains how to use swap cash flow mapping for hedging, duration management, and asset–liability matching, and how to distinguish which cash flows are most sensitive to movements in the market reference rate. Finally, it explains common exam pitfalls in swap valuation and cash flow mapping and how to avoid them.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are expected to understand the structure and valuation of swaps, and how to map and analyze swap cash flows in practice, with a focus on the following syllabus points:

- Pricing interest rate swaps and identifying the fair fixed rate.

- Calculating the market value of swaps after initiation.

- Interpreting and reconstructing swap cash flow schedules.

- Analyzing fixed and floating legs.

- Applying cash flow mapping to portfolio and risk management.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Briefly explain how the fair fixed rate in a plain vanilla interest rate swap is determined at initiation.

- What happens to the market value of a swap after interest rates change?

- When mapping swap cash flows, how do the fixed leg and floating leg differ in their payment calculations at each settlement date?

- Which swap legs are most sensitive to changes in market reference rates, and why?

Introduction

Interest rate swaps are essential tools for risk management and synthetic asset-liability adjustments. For the CFA Level 2 exam, you must understand both how to compute the value of a swap and how to accurately map swap cash flows over its lifespan. This article focuses on the key valuation steps for fixed-for-floating interest rate swaps, as well as best practices in mapping their periodic payments and understanding their impact on balance sheet and risk exposures.

Key Term: interest rate swap

A derivative contract exchanging a stream of fixed rate payments for a stream of floating rate payments based on a notional principal, with both legs typically in the same currency. Key Term: swap fixed rate (SFR)

The agreed fixed interest rate paid on the fixed leg of a swap, set at initiation to ensure zero market value. Key Term: market reference rate (MRR)

The floating rate index (e.g., SOFR, LIBOR replacement) used to set floating leg payments in swaps. Key Term: mark-to-market value (of swap)

The current value of a swap position, reflecting prevailing rates and projected future cash flows.Test Tip: When revising Swap valuation and cash flow mapping, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Swap Valuation at Initiation

A plain vanilla interest rate swap involves two parties, each agreeing to exchange interest cash flows over several dates. At inception, the fixed swap rate is set such that the present value of the swap’s fixed leg equals the present value of the floating leg—making the initial value to both parties zero.

To price a plain vanilla swap, follow these steps:

- Calculate discount factors: Use zero-coupon rates or forward rates for all payment dates.

- Sum the present values of future floating payments: The floating leg’s initial value equals par (notional), as first reset floating payments are known.

- Sum the present values of fixed payments: Use the unknown fixed rate as a variable and set the present value of this leg equal to the notional.

- Solve for the swap fixed rate: The swap rate equals the notional minus the final discount factor, divided by the sum of all discount factors (see formula below).

Key Term: discount factor

The present value of $1 received at a future settlement date, calculated using the term structure for the swap's currency.

Formula for the Fair Swap Fixed Rate

Where:

- = discount factor for period (based on zero-coupon rates)

- = number of swap periods

The fixed payments occur on scheduled settlement dates. The floating leg payments reset at each settlement, reflecting then-current market reference rates, and are paid in arrears.

Worked Example 1.1

A 2-year, annual fixed-for-floating interest rate swap is initiated on $10,000,000 notional. Market zero-coupon rates for 1 and 2 years are 3% and 3.8%, respectively (both annual compounding). Find the fair fixed rate for the swap.

Answer:

Discount factors:

or 3.853% The fair fixed rate is 3.853% (rounded), payable on each settlement date.

Swap Valuation After Initiation

After the swap starts, interest rates usually shift. The market value of a swap becomes nonzero once rates change. The fixed and floating legs are valued by discounting projected payments as of the valuation date.

- Fixed leg: Present value of all remaining fixed payments, discounted at current zero-coupon rates.

- Floating leg: Present value of next floating payment (determined at last reset), plus the notional, both discounted at current rates.

The swap's value to the fixed payer (receiver) is the difference between the present value of the floating leg and the present value of the fixed leg.

Worked Example 1.2

Suppose the swap from Example 1.1 is now 1 year old. The floating payment due equals $10,000,000×3.4%×1 = $340,000, to be paid in one year (based on known MRR at last reset). Current 1-year zero-coupon rate is 4% (annual). What is the swap's current value to the fixed-rate receiver?

Answer:

- PV (fixed payment): $10,000,000 × 3.853% × (1/1.04) = $370,484

- PV (floating leg): ($340,000 + $10,000,000) × (1/1.04) = $10,096,154

- PV (fixed leg): $10,000,000 × 1.03853 × (1/1.04) = $9,975,510

- Swap value = PV(floating leg) – PV(fixed leg) = $10,096,154 – $9,975,510 = $120,644 The fixed-rate receiver now has a positive market value position.

Exam Warning: A common error is failing to discount all remaining payments at current zero-coupon rates after initiation. Do not use original swap rates or average rates—always revalue using the latest zero curve.

Mapping Swap Cash Flows

Swap cash flow mapping involves laying out the full schedule of payments for both legs over the life of the swap. This is critical for performance attribution, risk analysis, and hedging.

Plain-vanilla interest rate swap revaluation applies current zero-coupon rates to remaining cash flows and derives the fixed receiver's market value.

- Fixed leg: Each payment date, payor sends the fixed rate × notional × accrual fraction since last payment.

- Floating leg: Each payment date, payor sends prior reset’s MRR × notional × accrual fraction.

At each settlement, the net payment is the difference between the fixed and floating legs.

Key Term: net settlement

The net payment exchanged on a settlement date, equaling the difference between the fixed and floating leg amounts.

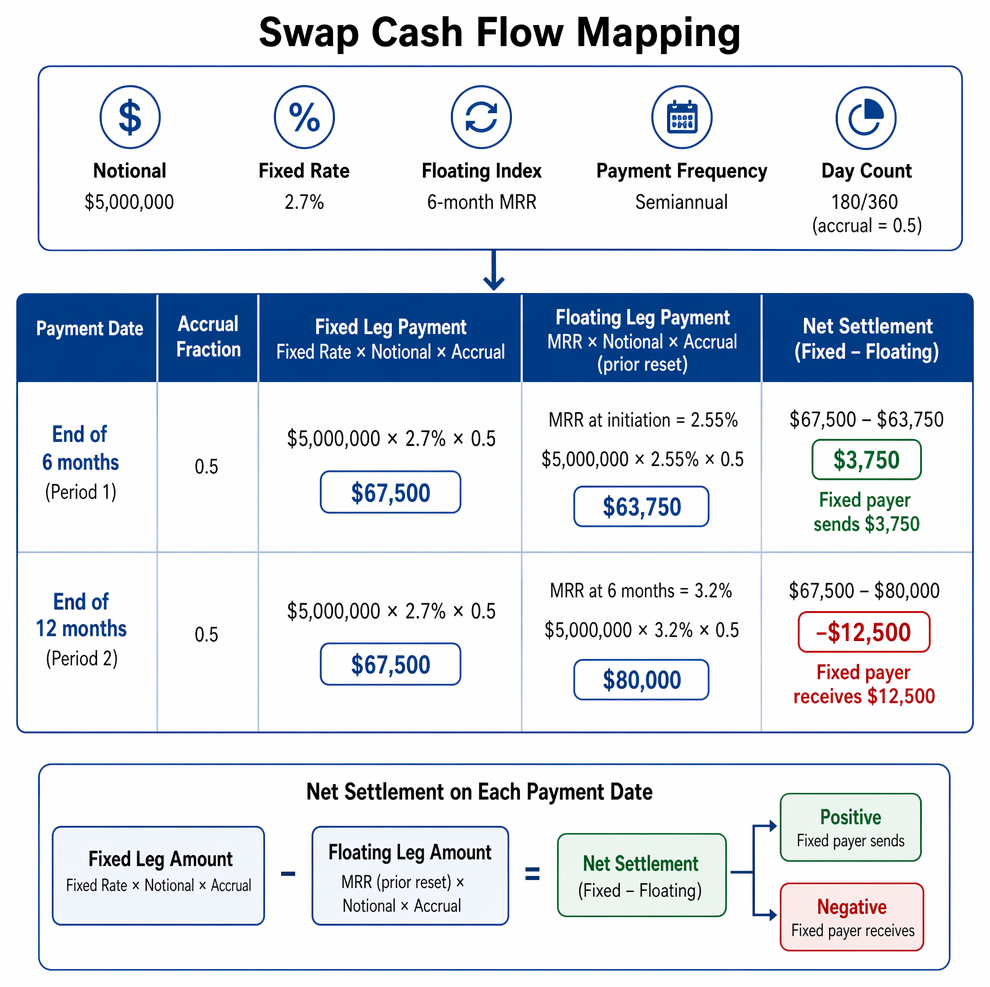

Worked Example 1.3

A 1-year swap on $5 million notional pays/seeks fixed at 2.7% and floating at the 6-month MRR. Payments are semiannual (two periods per year, 180/360 convention). At initiation, 6-month MRR is 2.55%; at 6 months, it’s 3.2%. Map the cash flows for both legs and the net settlements.

Answer:

- Period 1 (end of 6 months):

- Fixed payment: $5,000,000 × 2.7% × 0.5 = $67,500

- Floating payment: $5,000,000 × 2.55% × 0.5 = $63,750

- Net: Fixed payer sends $3,750.

- Period 2 (end of 12 months):

- Fixed payment: $67,500

- Floating payment: $5,000,000 × 3.2% × 0.5 = $80,000

- Net: Fixed payer receives $12,500.

Summary

- The fair fixed rate sets the swap’s initial value to zero.

- Swap value is the difference in present value between the floating and fixed legs, recalculated as rates change.

- Mapping swap cash flows means building a schedule showing the fixed and floating payments at each settlement date, and netting the result.

- Only net payments are exchanged; notional is never exchanged in plain vanilla swaps.

Key Point Checklist

This article has covered the following key knowledge points:

- Calculation of the fair fixed rate for an interest rate swap using discount factors.

- Mark-to-market valuation of swaps after changes in interest rates.

- Mapping fixed and floating cash flows across settlement periods.

- Construction of swap payment schedules and net settlements.

- Role of swaps in hedging and portfolio risk management.

Key Terms and Concepts

- interest rate swap

- swap fixed rate (SFR)

- market reference rate (MRR)

- mark-to-market value (of swap)

- discount factor

- net settlement