Learning Outcomes

This article explains industry and company analysis in the context of competitive forces, growth drivers, and economic moats, including:

- Applying Porter’s Five Forces to evaluate industry structure, bargaining power, threat levels, and expected profitability, and to identify where excess returns are most and least sustainable.

- Distinguishing industry life‑cycle stages and cyclicality, and translating these patterns into assumptions about revenue growth, margins, reinvestment needs, and risk when building cash‑flow forecasts and valuation models.

- Identifying key industry and company‑specific growth drivers—macroeconomic, demographic, technological, competitive, and regulatory—and evaluating whether each source of growth is realistic, sustainable, and consistent with long‑term economic constraints.

- Analyzing major categories of economic moats—cost advantages, intangible assets, network effects, switching costs, and efficient scale—and linking them to expected return on invested capital and competitive strength.

- Assessing the durability of competitive advantage under potential disruptions such as technological change, new regulation, or shifting customer preferences, and reflecting these risks in scenario analysis for the exam.

- Combining analysis of industry structure, growth prospects, and moats into coherent equity investment views, including valuation, risk assessment, and exam‑style recommendations consistent with CFA Level 2 expectations.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are required to understand theories and frameworks for industry and company analysis, with a focus on the following syllabus points:

- Analyzing industry structure and competitive forces using recognized frameworks (e.g., Porter’s Five Forces) and linking them to revenue, margin, and risk forecasts

- Identifying and assessing industry growth drivers and company-specific growth prospects using top‑down, market growth/market share, and hybrid approaches

- Evaluating the impact and durability of competitive advantages (economic moats) on return on invested capital and valuation

- Applying industry and company analysis when building DCF and multiples-based equity valuations, including scenario and sensitivity analysis

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

You are evaluating Orion Air, a regional airline, and Medexa, a branded specialty pharmaceutical firm. For Orion Air, fuel is a major input cost, aircraft can be leased from several manufacturers, and customers are mainly price-sensitive leisure travelers who can easily search fares online. Industry capacity has recently expanded faster than demand. For Medexa, revenue is dominated by two patented drugs used in chronic conditions, sold mostly to hospitals and insurers under long-term contracts. Regulators have just announced that generic competition will be allowed earlier than previously expected for drugs in Medexa’s category.

-

For Orion Air, which of Porter’s Five Forces most directly explains its weak pricing power and low operating margins?

- a) Threat of new entrants due to low capital intensity

- b) Bargaining power of buyers in a commoditized service with low switching costs

- c) Bargaining power of suppliers as there are many aircraft manufacturers

- d) Threat of substitutes due to high-speed rail

-

Which statement best characterizes Medexa’s current economic moat before the regulatory change takes effect?

- a) It mainly benefits from efficient scale in a small local market

- b) It relies on cost advantages from being the lowest‑cost producer globally

- c) It has strong intangible asset and switching cost moats around patented therapies

- d) Its moat is driven primarily by network effects among end consumers

-

The new regulation that accelerates generic entry for Medexa’s drug class will most likely have which impact on your long‑term valuation assumptions?

- a) Increase terminal growth and widen the forecast horizon of excess returns

- b) Reduce the duration of excess ROIC over the cost of capital and increase cash-flow risk

- c) Raise Medexa’s pricing power because generics are perceived as lower quality

- d) Improve Medexa’s bargaining power over suppliers of active ingredients

-

Suppose a low-cost carrier announces aggressive route expansion into Orion Air’s core markets while several marginal competitors are struggling financially. Which forecast adjustment is most appropriate for Orion Air?

- a) Increase near‑term revenue growth and expand long‑run operating margins

- b) Leave revenue forecasts unchanged but increase the long‑run sustainable growth rate

- c) Lower expected load factors and reduce operating margins due to intensified rivalry

- d) Increase capex and reduce discount rates to reflect improved industry structure

Introduction

Analyzing industry forces and company positioning is fundamental to equity valuation. A company’s ability to generate superior returns depends not only on its internal strengths but also on the structure and forces of the industry in which it operates. Industry competition, growth drivers, and the presence of robust economic moats determine whether a firm can sustain above-average profitability. These factors ultimately shape expected cash flows, risk, and valuation multiples.

Key Term: Industry structure

Industry structure refers to the configuration of competitors, customers, suppliers, entry barriers, and substitutes that shape pricing power, costs, and long‑term profitability in a given industry. Key Term: Return on invested capital (ROIC)

ROIC is net operating profit after tax divided by invested capital (operating assets minus operating liabilities) and measures how effectively a company generates returns from the capital used in its operations.

For Level 2, you are expected to move beyond description and apply these ideas: link industry forces to ROIC relative to the cost of capital, translate life-cycle and cyclicality patterns into explicit revenue and margin assumptions, and test whether claimed moats can plausibly sustain excess returns in your valuation models.

Test Tip: When revising Competitive forces growth drivers and moats, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

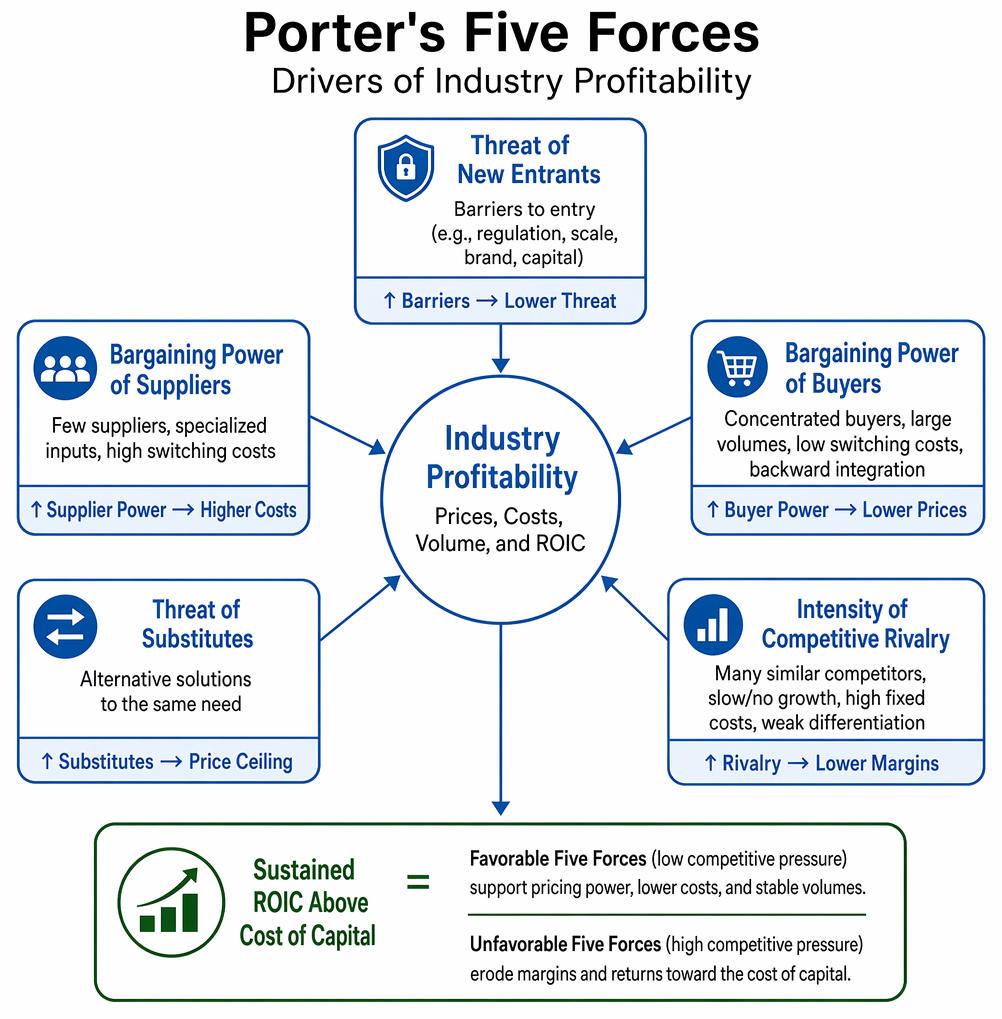

Understanding Industry Structure: Porter’s Five Forces

Industry profitability is shaped by the intensity of competition, which can be systematically examined using Porter’s Five Forces framework. This model helps identify the sources of value and risk within any industry by assessing the following competitive pressures:

Forecasting assumptions evolve across introduction, growth, maturity, and decline as growth, margins, reinvestment, and risk profiles change.

Key Term: Porter’s Five Forces

A framework evaluating five sources of competition—threat of new entrants, bargaining power of suppliers, bargaining power of buyers, threat of substitutes, and intensity of rivalry—that collectively determine industry profitability.

At CFA Level 2, you should be able to explain how each force affects prices, costs, volume, and ultimately ROIC.

Key Term: Barriers to entry

Barriers to entry are structural features—such as regulation, capital requirements, scale economies, or brand strength—that make it difficult or costly for new competitors to enter an industry. Key Term: Economies of scale

Economies of scale arise when average cost per unit declines as output increases, typically because fixed costs are spread over more units or because larger buyers obtain better input prices.

Threat of new entrants

High barriers to entry reduce the risk of new competitors eroding existing profits. Barriers can include regulation, brand loyalty, economies of scale, and capital requirements. When entry is easy, excess returns attract new firms, increasing supply and pushing margins toward the cost of capital.

Analytically:

- Low threat of entry supports the sustainability of ROIC above the cost of capital.

- High threat of entry implies any current excess returns are likely short‑lived, and valuation models should fade margins and growth toward industry averages sooner.

Example indicators of high barriers: exclusive licenses, high up‑front capital spending (semiconductors, utilities), strong distribution networks, or long regulatory approval processes.

Bargaining power of suppliers

Powerful suppliers can demand higher prices or better terms, squeezing industry margins. Supplier power increases when there are few alternative suppliers, when inputs are specialized or differentiated, or when switching costs for firms are high.

In forecasts:

- High supplier power increases cost volatility and may cap operating margins.

- Firms that are vertically integrated or can switch inputs (e.g., between energy sources) are less exposed.

Bargaining power of buyers

Powerful customers can force down prices or demand higher value, undermining profitability. Buyer power is stronger when customers are concentrated, purchase large volumes, face low switching costs, or can backward integrate.

Key Term: Switching costs

Switching costs are the financial, time, or psychological costs incurred by customers when changing suppliers, making them less likely to switch and reducing competitive pressure for the incumbent.

High switching costs weaken buyer power because customers are reluctant to change providers, supporting stability in revenue and margins. Low switching costs, combined with transparent pricing (e.g., online travel), lead to intense price competition.

Threat of substitute products or services

The presence of alternatives places a ceiling on prices and limits market power. Substitutes need not be identical products; they can be different solutions to the same need (e.g., ride‑sharing vs car ownership, video conferencing vs business travel).

A high threat of substitutes:

- Restricts a firm’s ability to raise prices, even if direct rivalry is limited.

- Is especially important in valuation when new technologies create potential substitutes that may not yet have large market share but could rapidly scale.

Intensity of competitive rivalry

Widespread rivalry can result in price wars, increased marketing costs, rapid product cycles, and reduced industry returns. Rivalry tends to be most intense when:

- There are many competitors of similar size.

- Industry growth is slow or negative.

- Fixed costs and exit barriers are high (capacity must be kept filled).

- Products are weakly differentiated.

These conditions push margins down and make earnings more volatile. When analyzing a case, look for descriptive cues (price matching, frequent promotions, overcapacity) that point to high rivalry and justify conservative margin assumptions.

Industry Evolution and Cyclicality

Industries progress through various life-cycle stages—introduction, growth, maturity, and decline—each with distinct growth drivers and competitive forces. Cyclicality refers to the degree to which industry demand fluctuates with macroeconomic cycles, affecting forecasting and valuation.

Key Term: Industry cycle

The sequence of development stages through which an industry typically passes: introduction, growth, maturity, and decline. Key Term: Cyclicality

Cyclicality is the extent to which an industry’s sales and profits rise in expansions and fall in recessions relative to the overall economy.

Life-cycle stages and forecasting implications

-

Introduction stage:

- Low revenues, negative or low margins, high uncertainty.

- Cash flows are usually negative due to heavy R&D and marketing.

- Five Forces: high threat of entry (if IP is weak), low rivalry (few players), but also high failure risk.

- Forecasting: emphasize scenario analysis; do not project early high growth indefinitely.

-

Growth stage:

- Rapid volume growth, improving margins as economies of scale build.

- New entrants attracted by growth; rivalry starts to increase.

- Firms may enjoy temporary moats (innovative products, patents).

- Forecasting: high revenue growth and rising margins are plausible, but model gradual slowing and eventual normalization of ROIC.

-

Maturity stage:

- Slower, GDP‑like growth; margins stabilize; industry consolidation common.

- Five Forces: rivalry typically high; differentiation and cost leadership strategies become critical.

- Forecasting: assume growth modestly above or below nominal GDP, and margins near long‑run sustainable levels.

-

Decline stage:

- Shrinking demand due to substitutes or saturation; capacity rationalization and exit decisions become key.

- Potential price competition if exit barriers are high (e.g., specialized assets).

- Forecasting: declining revenues, possibly shrinking margins, and lower reinvestment; consider restructuring or liquidation scenarios.

On the exam, life‑cycle cues in the vignette (growth rates, capex intensity, number of competitors, product innovation) often signal how aggressive or conservative your growth and margin assumptions should be.

Cyclical vs defensive industries

Cyclical industries (e.g., autos, steel, luxury goods) experience amplified swings in sales and earnings relative to GDP. Defensive industries (e.g., utilities, staple foods, basic healthcare) show relatively stable demand.

Cyclical industries often exhibit:

- High fixed costs and operating leverage

- Greater earnings volatility and higher beta

- Deep downturns that require strong balance sheets and access to capital

When valuing cyclical companies, exam questions may require you to:

- Use normalized earnings or margins over a cycle rather than peak or trough values

- Stress‑test cash flows under adverse macro scenarios

- Be cautious about treating peak margins as sustainable

Key Factors Affecting Industry Attractiveness

Factors such as industry concentration, capital intensity, product differentiation, excess capacity, and switching costs influence the power of each force. Highly concentrated industries with strong barriers tend to be more attractive for sustaining above-average returns.

- Concentration: A few dominant firms can sometimes maintain rational pricing and defend margins, especially if capacity additions are disciplined. In fragmented industries, intense rivalry often erodes profits.

- Capital intensity and exit barriers: Heavy irreversible investment (e.g., refineries, airlines) raises exit barriers, encouraging continued production even at low margins and contributing to chronic overcapacity.

- Product differentiation and switching costs: Strong brands, unique features, or significant switching costs reduce price sensitivity and support premium pricing.

- Vertical coordination: Controlling key inputs or distribution can weaken supplier or buyer power but may require substantial capital and managerial capability.

For Level 2, you should connect these structural features explicitly to expected ROIC and the length of time that excess returns can persist in your models.

Company-Specific Growth Drivers

A company’s ability to achieve long-term growth depends on both industry-level and firm-specific factors.

Key Term: Growth driver

A growth driver is a key factor—such as macroeconomic conditions, demographics, technology, competitive positioning, or regulation—that influences the trajectory of a firm’s revenues and earnings.

- Industry growth: Driven by macro trends (GDP, demographics, technology, regulation). For example, rising incomes may support premium consumer goods; aging populations support healthcare demand.

- Company growth drivers: Innovation, operational efficiency, access to capital, effective strategy (cost leadership, differentiation, or focus), and M&A.

From the syllabus standpoint, you should be comfortable distinguishing:

- Volume vs price growth: Is the company gaining from higher prices, increased volumes, or a better mix? Volume growth is often constrained by industry capacity and demand; price growth is constrained by Five Forces and inflation pass‑through.

- Organic vs acquisition-driven growth: Acquisition-based growth may not be sustainable and often involves post-acquisition risk and potentially lower ROIC.

- Top‑down vs bottom‑up approaches:

- Top‑down: Start from expected GDP and industry growth, then estimate the firm’s revenue as a function of industry share or “growth relative to GDP.”

- Bottom‑up: Build from product lines, new launches, and customer cohorts; particularly useful when a firm diverges meaningfully from industry averages.

Sustainable Growth and Forecasting

Long-term growth rates are rarely above the broader economy’s growth unless supported by unique advantages. Even then, they cannot exceed the economy’s nominal growth indefinitely. Evaluate sources of growth carefully for reasonableness and sustainability in financial models.

Key Term: Sustainable growth rate

The sustainable growth rate is the maximum rate at which a company’s earnings (and dividends) can grow while keeping its capital structure constant and without issuing new equity, typically approximated by the product of the retention ratio and return on equity.

Denoting the retention ratio by and return on equity by ROE, the sustainable growth rate is:

This formula ties growth directly to profitability and reinvestment. On the exam, aggressive long‑run growth assumptions that exceed a plausible sustainable growth rate, or long‑term nominal GDP, are a red flag.

Analysts should also distinguish:

- Near‑term high growth: Often supported by innovation or market share gains; appropriate for the explicit forecast period.

- Long‑run terminal growth: Usually set close to long‑run nominal GDP for mature firms, often slightly below for conservative valuations.

Worked Example 1.1

Question: You are analyzing a telecommunications company with a patented technology generating faster data speeds than competitors. How does this affect its competitive position and your growth assumptions?

Answer:

The company’s patented technology is an intangible asset that establishes a barrier to entry, reducing the threat of new entrants and partly protecting it from rivalry. In the near term, this can support above‑industry revenue growth (from market share gains or premium pricing) and elevated margins. However, patents expire and rivals may innovate around them, so you should gradually fade growth and ROIC toward industry levels rather than assume permanent outperformance.

Economic Moats: Assessing Durable Competitive Advantage

Economic moats describe factors that protect a company from competitive threats, enabling it to consistently earn returns above its cost of capital.

Key Term: Economic moat

An economic moat is a structural, durable advantage that shields a company from competition and secures its long-term ability to earn ROIC above its cost of capital.

Common sources of moats include:

Key Term: Cost advantage

A cost advantage is a structural ability to produce at lower unit cost than competitors, allowing a firm to earn superior margins at the same price or undercut rivals while still earning acceptable returns. Key Term: Intangible assets

Intangible assets are non-physical resources such as brands, patents, licenses, and proprietary technology that create barriers to entry or allow premium pricing. Key Term: Network effects

Network effects arise when the value of a product or service to each user increases as the number of users grows, making it harder for new entrants to compete. Key Term: Efficient scale

Efficient scale occurs when a limited number of firms can serve the entire market at the lowest cost, and additional entrants would depress returns for all participants, deterring entry.

- Cost advantages: Lowest-cost producers can survive price competition and often gain share in downturns. Sources include scale, superior processes, advantaged locations, or exclusive access to low-cost inputs.

- Intangible assets: Strong brands support premium pricing; patents and licenses block imitation; regulatory franchises (e.g., bank charters) restrict entry. The economic value depends on enforceability and the relevance of the core technology or brand over time.

- Network effects: Platforms, marketplaces, and communication networks become more valuable as more users participate (e.g., payment networks, social media, enterprise marketplaces). These can create a winner‑take‑most structure and very durable moats.

- Switching costs: High customer switching costs lock in clientele (for example, enterprise software systems deeply embedded in workflows). They reduce churn and allow pricing power without significant volume loss.

- Efficient scale: Niche markets dominated by a single or a few players (e.g., local utilities, certain transportation hubs) discourage entry because new capacity would drive down returns for everyone.

Well‑defended moats show up as:

- ROIC consistently above the cost of capital across cycles

- Stable or rising market share despite attractive industry economics

- Ability to pass input cost inflation through to customers (high inflation pass‑through)

Evaluating the Durability of Moats

Not all competitive advantages are sustainable. Scrutinize whether a company’s moats are likely to endure disruptive innovation, regulatory change, or shifts in consumer preference. Moats must be continuously reinforced through innovation, customer loyalty, and cost leadership.

Key questions for durability:

- Imitability: How costly or time‑consuming is it for competitors to replicate the advantage?

- Substitutability: Are there emerging substitutes that bypass the moat (e.g., streaming vs cable TV)?

- Regulatory risk: Could regulators weaken the moat (for example, by forcing open access to networks or limiting patent protection)?

- Customer behavior: Are customer preferences shifting in ways that erode brand value or reduce switching costs?

For exam purposes, durable moats imply that elevated ROIC and margins can be modeled for a longer period before fading. Weak or eroding moats require faster convergence to competitive levels.

Worked Example 1.2

Question: A large utility company is the sole provider of water in its region and heavily regulated. What forms of moat does it possess, and how should that shape your valuation assumptions?

Answer:

The company benefits from efficient scale (a natural monopoly) and high capital requirements that deter entry. Regulation effectively replaces competitive forces, limiting both upside (through allowed returns) and downside (through protective tariffs and cost recovery mechanisms). You should model relatively stable revenues and margins with ROIC close to the regulator’s allowed return, low growth, and lower discount rates than for cyclical, unregulated businesses. Exam Warning: Do not assume that any competitive advantage is permanent. In exam vignettes, carefully consider the risk that new technology, changes in regulation, or changing customer needs could erode moats or alter industry structure. Reflect this by adjusting the length of the high‑growth period, the speed at which ROIC converges toward the cost of capital, and by testing downside scenarios.

Worked Example 1.3

You are valuing a global payments platform with strong user growth and rising margins. The case notes that merchants benefit as more consumers join the platform, and consumers benefit as more merchants accept it. Regulators, however, are considering open‑banking rules that could make it easier for new payment providers to access bank accounts.

Answer:

The platform currently has a strong network‑effects moat: the value to both merchants and consumers increases with the size of the network, reinforcing its dominance and supporting high ROIC and revenue growth. Potential open‑banking regulation threatens to reduce barriers for rivals and weaken those network effects by making multi‑homing easier. In your model, you might still assume elevated growth and margins in the near term but shorten the horizon over which the platform can sustain excess returns and increase the dispersion of outcomes in scenario analysis.

Applying Industry and Company Analysis

For effective company analysis:

- Review current and projected industry conditions, including the Five Forces and life‑cycle stage.

- Examine company positioning, specific growth initiatives, and the sources and threats to its moats.

- Consider management quality, capital allocation discipline, and adaptability to structural change.

In the Level 2 curriculum, this analysis feeds directly into valuation.

-

Translate structure into economics:

- Strong moats and favorable industry structure (high entry barriers, limited substitutes) support ROIC persistently above the cost of capital, justifying higher valuation multiples and longer explicit high‑growth periods.

- Weak moats in highly competitive industries imply faster reversion of margins and ROIC, lower PVGO (present value of growth opportunities), and more cautious multiples.

-

Forecast revenue and margins:

- Use top‑down or market‑share approaches anchored in industry growth and Five Forces.

- Incorporate the impact of input cost volatility and pricing power: industries with weak supplier and buyer power can more easily pass inflation through to prices; others may see margin compression when input costs rise.

-

Model reinvestment and growth consistency:

- The sustainable growth rate links growth to profitability and reinvestment. For a given ROE or ROIC, higher growth requires higher reinvestment.

- If management’s growth targets imply reinvestment that would drive ROIC below the cost of capital, treat the incremental growth as value‑destroying and be wary of paying for it.

-

Embed risk and scenario analysis:

- Use scenarios to capture potential changes in industry structure (e.g., entry of a low‑cost competitor, regulatory shifts, technological disruption).

- Reflect structural risk in discount rates and in the breadth of valuation ranges, not just in a single point estimate.

Worked Example 1.4

A case describes a mid‑sized packaged foods company operating in a mature market with low volume growth but strong brands and significant advertising spend. Private-label competitors have gained share in recessions, but the company has historically maintained stable gross margins and modestly growing dividends.

How should you combine industry and company analysis to inform your valuation?

Answer:

The industry appears mature and somewhat defensive, with low base volume growth. Competition from private labels increases buyer power and rivalry, but the firm’s strong brands are intangible assets that provide a moat and support premium pricing. You should assume revenue growth roughly in line with nominal GDP, stable to slightly improving margins (if brands remain strong), and a long period of modest but sustainable excess ROIC. A Gordon Growth or stable-growth DCF model with a conservative long‑run growth rate and relatively low discount rate would be appropriate, recognizing that most of the value comes from the steady cash‑flow stream rather than explosive growth.

Key Point Checklist

This article has covered the following key knowledge points:

- Use Porter’s Five Forces to evaluate industry profitability and competition, and link each force to pricing power, costs, and ROIC.

- Recognize industry growth drivers and life‑cycle stages, and distinguish cyclical from structural growth in company forecasting.

- Assess how factors such as concentration, capital intensity, differentiation, and switching costs affect industry attractiveness.

- Identify and evaluate economic moats—cost advantages, intangible assets, network effects, switching costs, and efficient scale—and relate them to the sustainability of excess returns.

- Analyze how regulatory and technological change can erode moats and adjust forecast horizons and scenarios accordingly.

- Connect industry and company analysis to valuation choices, growth and margin assumptions, and the durability of PVGO in exam-style problems.

Key Terms and Concepts

- Industry structure

- Return on invested capital (ROIC)

- Porter’s Five Forces

- Barriers to entry

- Economies of scale

- Switching costs

- Industry cycle

- Cyclicality

- Growth driver

- Sustainable growth rate

- Economic moat

- Cost advantage

- Intangible assets

- Network effects

- Efficient scale