Learning Outcomes

This article explains intercorporate investments and business combinations for CFA Level 2, including:

- Distinguishing among investments in financial assets, associates, joint ventures, business combinations, and variable interest entities based on ownership, control, and significant influence thresholds.

- Determining when to apply fair value, equity method, or acquisition method and describing the recognition and measurement mechanics under each approach.

- Tracing how the equity method records initial cost, subsequent shares of profit or loss, dividends, and goodwill allocations for associates and joint ventures.

- Identifying when joint ventures and VIEs must be consolidated despite limited or no voting interests, with emphasis on the concept of primary beneficiary.

- Comparing how different methods affect reported assets, liabilities, revenue, net income, non‑controlling interest, and key ratios such as leverage, margins, and return on equity.

- Evaluating disclosures related to intercorporate investments to adjust financial statements for analytical purposes and to detect earnings management or off‑balance‑sheet financing.

- Applying these concepts to typical exam-style numerical problems and conceptual questions involving multiple investees with varying levels of influence and control.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are expected to understand how different types of intercorporate investments are classified and reported, with a focus on the following syllabus points:

- Describe and distinguish among investments in financial assets, associates, joint ventures, business combinations, and variable interest entities (VIEs)

- Explain the equity method, proportionate consolidation, and acquisition method

- Compare the effects of different investment classifications and methods on financial statements and key ratios

- Evaluate disclosures and assess the implications for analysis

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which ownership percentage typically requires use of the equity method for intercorporate investments?

- a) Less than 20%

- b) 20% to 50%

- c) More than 50%

- d) Any percentage if significant influence exists

-

When is a joint venture required to be accounted for using the equity method rather than the acquisition method?

-

What is a variable interest entity (VIE), and what triggers consolidation of a VIE?

-

How do investments in associates impact an investor’s net income and balance sheet differently from investments in financial assets?

Introduction

Intercorporate investments arise when one company obtains an ownership stake in another. The accounting method depends on the degree of control or influence the investor has over the investee. For CFA Level 2, it is critical to apply the correct method—cost/fair value, equity, or acquisition—and to analyze the effect on a firm's reported assets, liabilities, revenues, and income. Understanding joint ventures, associates, and variable interest entities is essential for interpreting published financial statements, comparing firms, and assessing earnings quality.

Key Term: significant influence

The power to participate in an investee's financial and operating policy decisions, but without having control. Evidence includes board representation, policy involvement, and material intercompany transactions. Key Term: control

The power to govern an investee’s financial and operational decisions, usually through majority voting rights or contracts.Test Tip: When revising Associates joint ventures and variable interest entities, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

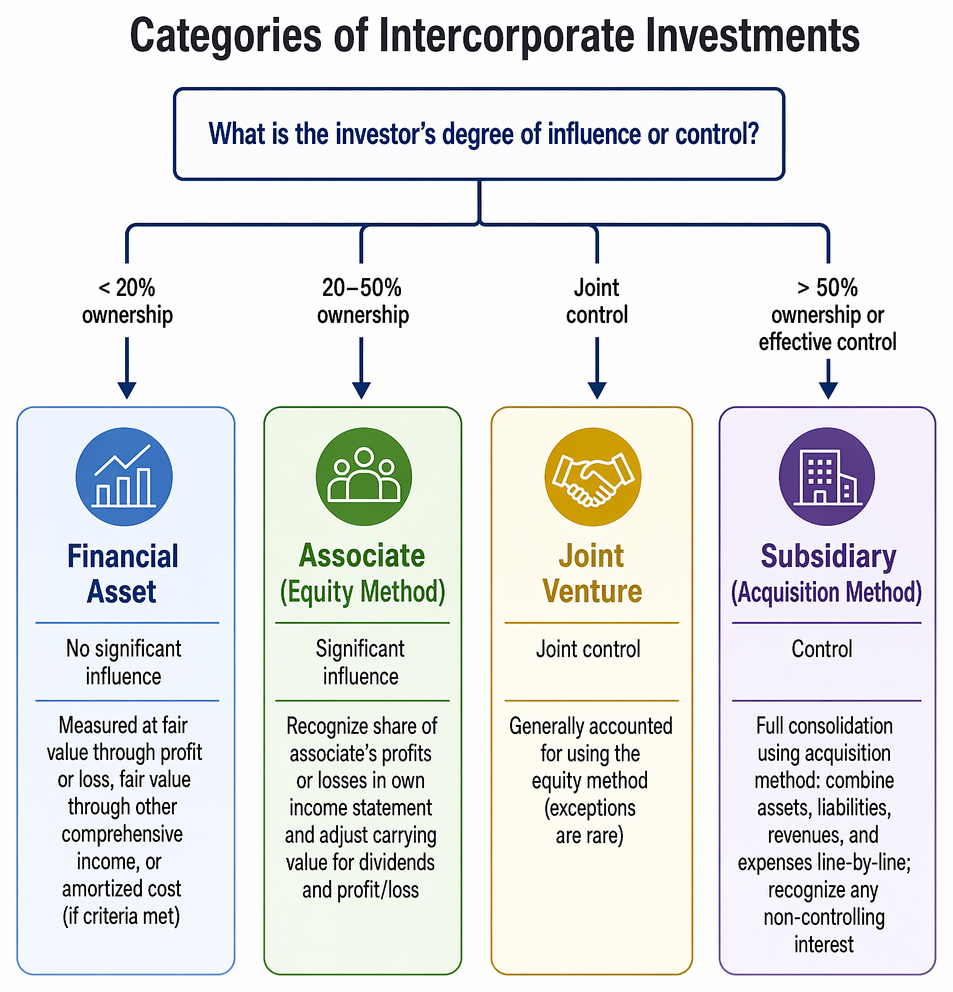

CATEGORIES OF INTERCORPORATE INVESTMENTS

The accounting for an investment is determined primarily by the investor’s degree of influence or control.

Equity method accounting records the investment at cost, adjusts for investee earnings and dividends, and allocates basis differences including goodwill.

Investments in Financial Assets

When the investor has no significant influence (generally less than 20% ownership), the investment is classified as a financial asset. Financial assets are reported at fair value through profit or loss, fair value through other comprehensive income, or at amortized cost if specific criteria are met.

Investments in Associates—The Equity Method

When an investor can exert significant influence (usually 20–50% ownership or established by other evidence), the equity method is used. The investor recognizes its share of the associate's profits or losses in its own income statement and adjusts the carrying value of the investment accordingly.

Key Term: equity method

An accounting technique in which the investor recognizes its share of the investee’s net income and adjusts the carrying value of the investment for dividends and profit/loss.

Investments in Joint Ventures

A joint venture is an arrangement in which two or more parties have joint control. Under both IFRS and US GAAP, joint ventures are generally accounted for using the equity method (exceptions are rare).

Key Term: joint venture

A contractual arrangement whereby two or more parties undertake an economic activity subject to joint control, typically involving shared decision-making.

Business Combinations—Acquisition Method

If control is established (more than 50% ownership or effective control otherwise), the parent must consolidate the investee’s financial statements using the acquisition method. This involves full consolidation—assets, liabilities, revenues, and expenses are combined line-by-line, and any non-controlling interest is recognized.

Key Term: acquisition method

The process by which a parent consolidates a subsidiary, recording identifiable assets and liabilities at fair value and recognizing goodwill for any excess consideration.

VARIABLE INTEREST ENTITIES (VIEs) AND SPECIAL PURPOSE ENTITIES

Key Term: variable interest entity (VIE)

A structure where control exists through arrangements other than voting rights, often created to achieve specific purposes, and which requires consolidation if the investor is the primary beneficiary. Key Term: special purpose entity (SPE)

A separate legal structure designed to isolate certain assets or activities.

A company must consolidate a VIE/SPE if it is exposed to most of the expected losses or gains (is the primary beneficiary), even if it does not hold a majority of voting shares.

Worked Example 1.1

A power company creates a legally separate entity to finance a power plant, providing guarantees on the SPE's debt. The sponsors hold only 10% of the voting equity but absorb most risks and benefits through contracts. Should the company consolidate the SPE?

Answer:

Yes. Despite owning less than 50%, the sponsor is exposed to variable returns and has the power to direct activities through guarantees and contracts, meeting the criteria for VIE consolidation.

ACCOUNTING FOR ASSOCIATES USING THE EQUITY METHOD

When using the equity method:

- The investment is initially recorded at cost.

- Each period, the carrying amount increases/decreases by the investor’s proportionate share of the associate’s net income/loss.

- Dividends received from the associate reduce the carrying value (they are not recognized as income).

- If the purchase price exceeds the investor’s share of fair value of net identifiable assets acquired, the difference is allocated first to identifiable assets (with fair value > book value), and any remainder is goodwill.

Worked Example 1.2

Alpha Co. acquires 30% of Beta Ltd. for $300,000. During the first year, Beta earns $120,000 and distributes dividends of $40,000.

- What is the effect on Alpha’s financial statements?

Answer:

Alpha recognizes $36,000 ($120,000 × 30%) as equity income, increasing the investment carrying amount. Receipt of $12,000 dividends ($40,000 × 30%) reduces the investment carrying amount. Therefore:

- Initial investment: $300,000

- Share of earnings: $36,000

- – Dividends received: $12,000

- Ending carrying value: $324,000

JOINT VENTURES: THE EQUITY METHOD

Accounting for joint ventures is conceptually identical to associates under the equity method, with each venturer recognizing its share of profit or loss and adjusting the investment carrying value similarly.

Worked Example 1.3

Suppose Company X and Company Y each hold 50% of a joint venture, JVCo. JVCo reports a $60,000 profit and pays $20,000 in total dividends this year. How will each venturer account for its share?

Answer:

Each recognizes $30,000 as equity income and reduces the investment by $10,000 upon receiving the dividend. The carrying value increases by net $20,000.

BUSINESS COMBINATIONS: THE ACQUISITION METHOD

When an investor obtains control, 100% of the investee’s assets, liabilities, revenues, and expenses are consolidated, regardless of the ownership percentage, with a non-controlling interest recognized for unowned shares.

Key consolidation steps:

- Measure identifiable assets and liabilities at fair value

- Recognize goodwill (purchase price above net fair value of identifiable assets/liabilities)

- Eliminate the investment in the subsidiary

- Recognize any non-controlling interest in equity

If less than 100% is acquired, non-controlling interest is measured at fair value (full goodwill) under US GAAP; IFRS permits either full or partial goodwill.

Key Term: non-controlling interest

The equity in a subsidiary not attributable directly or indirectly to the parent company.Exam Warning: It is common to mistakenly account for dividends from associates or joint ventures as income under the equity method. Only the share of net income increases the investment; dividends are treated as a return of capital and reduce the investment balance.

VARIABLE INTEREST ENTITIES: CONSOLIDATION REQUIREMENTS

A variable interest entity must be consolidated if the reporting entity is the primary beneficiary, i.e., it has both:

- The power to direct significant activities of the entity, and

- The obligation to absorb losses or right to receive benefits that could be significant to the VIE.

Recognition is required even if the holding in voting shares is minimal.

Worked Example 1.4

Company A sponsors an SPE for receivable securitization, providing credit support and receiving excess cash flow. It owns none of the SPE’s equity but controls key decisions. Is consolidation required?

Answer:

Yes, Company A must consolidate the SPE as a VIE, having both the power to direct its relevant activities and the right to residual returns.

IMPACT OF ACCOUNTING CHOICE ON ANALYSIS AND RATIOS

Choice of method (fair value, equity, or acquisition) affects reported assets, liabilities, equity, revenue, and net income, with important consequences for key ratios.

- Acquisition method: All subsidiary assets and liabilities consolidated, increasing gearing and size-based ratios.

- Equity method: Only net investment appears as an asset, with one-line equity income; understated assets/liabilities compared to acquisition, higher margins/ROE.

- Financial assets: Only dividends/realized gains/losses in income; no share of investee profit.

Worked Example 1.5

Consider an investor that simultaneously has a controlling investment (consolidated), significant influence (equity method), and a minor holding (fair value) in three companies. Which method will show the highest total assets?

Answer:

Consolidation via the acquisition method results in the highest reported assets, as the entire subsidiary balance sheet is combined with the parent’s. The equity method and fair value method show only a single-line investment asset.

Summary

Intercorporate investment accounting depends on control or influence. When significant influence, but not control, exists, use the equity method. Joint ventures apply the equity method by default. Controlling interests require full consolidation using the acquisition method, with any non-controlling interest recognized. Certain VIEs or SPEs must be consolidated if the investor is the primary beneficiary regardless of voting rights. Accounting choice materially affects reported results and ratios, which the analyst must consider.

Key Point Checklist

This article has covered the following key knowledge points:

- Determine the proper classification and method for intercorporate investments based on control/influence

- Apply the equity method for associates and joint ventures

- Consolidate subsidiaries under the acquisition method

- Recognize the requirement to consolidate VIEs if primary beneficiary

- Adjust analysis for the impact of different methods on financial statements and ratios

Key Terms and Concepts

- significant influence

- control

- equity method

- joint venture

- acquisition method

- variable interest entity (VIE)

- special purpose entity (SPE)

- non-controlling interest