Learning Outcomes

This article explains currency options and cross-currency swaps in the CFA Level 2 derivatives curriculum, including:

- Distinguishing between currency calls and puts, their contractual features, and how option style (European vs American) affects exercise flexibility and value.

- Interpreting payoff diagrams and numeric payoff calculations for long and short currency option positions under different spot and strike scenarios.

- Applying core option pricing relationships and intuition (parity, time value, volatility effects, interest rate differentials) to judge whether an option is fairly valued.

- Describing the structure of cross-currency swaps, with emphasis on initial notional exchanges, periodic interest payments, and principal re-exchange at maturity.

- Valuing and comparing alternative swap structures (fixed–fixed, fixed–floating) using given interest rates, discount factors, and exchange rates.

- Assessing how currency options and cross-currency swaps are used in practice for hedging, speculative positioning, and arbitrage strategies.

- Evaluating which instrument is more appropriate for a firm’s risk management objective given its cash flow pattern, risk tolerance, and view on exchange rates.

- Identifying common exam pitfalls, such as misreading the payoff currency, confusing premium cost with payoff, or ignoring credit and liquidity considerations in swaps.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are expected to understand the nature, valuation, and applications of derivative products linked to currencies and interest rates, with a focus on the following syllabus points:

- Explaining the structure and payoffs of currency options (calls and puts).

- Describing the cash flows, exchange rate implications, and risk exposures in cross-currency swaps.

- Calculating the value and cash flows of currency options and swaps given exchange rates and interest rates.

- Applying options and swaps for currency hedging, market speculation, and arbitrage.

- Recognizing the differences in risk and accounting between options and swaps.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

A European firm expects to receive $2 million in 3 months and fears USD will depreciate. Which of the following would directly protect against a weak dollar?

- a) Buy a USD call option

- b) Sell a USD put option

- c) Sell a USD call option

- d) Buy a USD put option

-

In a cross-currency swap, which of the following is true at initiation?

- a) Only the notional in the base currency is exchanged

- b) Both notionals in both currencies are exchanged

- c) Payments are made only at maturity

- d) Cash flow amounts are fixed for both currencies

-

True or false? An American currency option always has the same value as a European option with identical terms.

-

Briefly explain why a multinational might use a cross-currency swap instead of multiple forward contracts.

Introduction

Currency options and cross-currency swaps are major tools for managing foreign exchange and interest rate risk for CFA Level 2 candidates. Both products offer structured ways for firms to hedge or speculate in global markets. Understanding the cash flows, valuations, and strategic applications of these instruments is essential for exam readiness.

Key Term: currency option

A derivative contract giving the holder the right, but not the obligation, to exchange a set amount of one currency for another at a predetermined rate on or before a specified date. Key Term: cross-currency swap

An agreement where two parties exchange principal and interest payments in different currencies, typically involving periodic interest payments and re-exchange of principal at maturity.

CURRENCY OPTION BASICS

Currency options are commonly available as either calls or puts on a particular currency pair. The option premium is paid upfront by the buyer. Options can be European-style (exercisable only at maturity) or American-style (exercisable at any time up to expiry).

- Call Option: Right to buy the base currency against the quote currency at the strike.

- Put Option: Right to sell the base currency at the strike.

Payoff to the holder at expiry is determined by the relative spot rate and strike rate, net of premium paid.

Key Term: strike price

The agreed exchange rate at which the option can be exercised. Key Term: notional principal

The face value amount upon which option or swap cash flows are calculated.

Currency Option Payoff Profiles

Payoff diagrams for currency calls and puts mirror those for equity options but represent gains and losses in terms of the quote currency. At expiry, the call option holder benefits if the spot rate is above the strike; the put holder if the spot is below the strike.

Premiums are influenced by time to expiry, volatility of reference exchange rates, and relative interest rates.

Worked Example 1.1

A UK company buys a 3-month EUR/USD call (notional €1m, strike 1.0800, premium $0.0150/EUR). At expiry, spot is 1.1050. What is the net payoff in USD if the company exercises?

Answer:

Exercising allows the company to buy €1,000,000 at $1.0800/€ = $1,080,000, while selling on the spot market at $1,105,000 gives a gain of $25,000. Subtracting the $15,000 premium, net gain = $10,000.

Valuation of Currency Options

Currency option pricing can employ the Garman-Kohlhagen model (a variant of Black-Scholes), which considers volatility, spot, strike, time, and domestic/foreign interest rates. Depth of calculation is less critical for the exam than understanding the direction and shape of payoffs.

Worked Example 1.2

A Japanese exporter sells an American-style put option to hedge $500,000 receivable, strike 110 JPY/$, at a $0.0070/JPY premium. If JPY/$ drops to 105 at expiry, what does the exporter gain or lose if the option expires unexercised?

Answer:

The exporter receives the option premium of ¥3,500,000, but since the option is out-of-the-money (spot > strike for a put), there is no exercise. Gain = premium received = ¥3,500,000. Option provided insurance but was not needed.Exam Warning: American currency options are worth at least as much as European-style options due to their greater exercise flexibility, but will only be more valuable if early exercise provides economic advantage (e.g., in-the-money puts with high interest rates).

CROSS-CURRENCY SWAPS: STRUCTURE AND USE

A cross-currency swap facilitates the periodic exchange of both principal and interest amounts in two different currencies. Typically, both principal amounts are exchanged at start and re-exchanged at maturity; throughout the swap, each party pays interest on the principal it receives at a rate set in its currency. Fixed-to-fixed or fixed-to-floating structures are common.

Currency option valuation is decomposed into call and put intrinsic value, time value drivers, and the early-exercise effect of option style.

Key Term: swap spread

The difference between the swap rate and the yield on a government bond of the same maturity, reflecting credit and liquidity differentials.

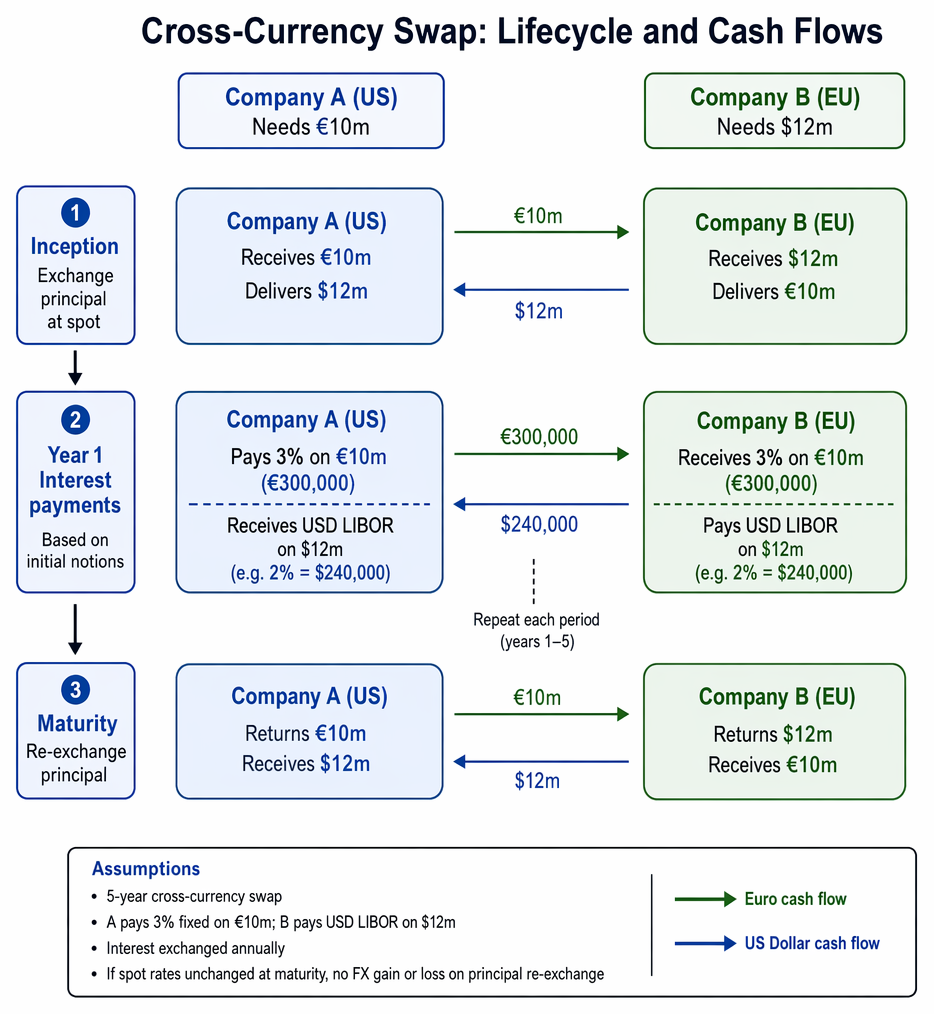

Lifecycle and Cash Flows

At initiation, parties exchange notional amounts in two currencies at spot. Over the life of the swap, they exchange interest payments (fixed or floating) calculated on the initial notional. At maturity, principal amounts are re-exchanged.

Worked Example 1.3

Company A (US) needs €10 million, Company B (EU) needs $12 million. Spot rate is 1.2000 USD/EUR. Both agree to a 5-year cross-currency swap, exchanging principal at inception, then paying floating USD LIBOR on $12 million and 3% fixed on €10 million annually. At end, principals swapped back. Outline net cash flows for year one, assuming spot rates remain unchanged.

Answer:

At inception: A delivers $12m, receives €10m; B receives $12m, delivers €10m. Year 1: A pays 3% on €10m (€300,000) to B; receives USD LIBOR on $12m (say, LIBOR=2% ⇒ $240,000) from B. At maturity: principals are re-exchanged—no FX gain/loss if spot is unchanged.

Using Cross-Currency Swaps

- Hedge currency and interest rate risk: Firms match currency of cash inflows/outflows to manage foreign-denominated debt or receivables.

- Access markets with better borrowing rates: Corporates can borrow where their credit is stronger and swap to required currency.

- Alter exposure: Swaps can be used to change floating to fixed-rate interest or vice versa, or to synthetically alter currency profile of liabilities.

Comparison: Currency Options vs Cross-Currency Swaps

- Options provide the right but not the obligation to transact at the strike, yielding asymmetric payoff protection useful for flexible hedging.

- Swaps commit parties to a bilateral exchange, replicating a series of forward contracts; typically used for longer-term, more predictable cash flow management.

Revision Tip: When deciding between an option and a swap for hedging, consider if you need protection against adverse FX moves only (option) or you are prepared to lock in all currency exchanges for the duration (swap).

Summary

Currency options grant the holder flexibility to hedge or speculate on currency moves with limited risk, while cross-currency swaps facilitate complex multi-currency financing or risk management by exchanging principal and interest payments. CFA candidates must know structure, typical use cases, payoff profiles, and the basics of pricing and risk for each instrument.

Key Point Checklist

This article has covered the following key knowledge points:

- Describe structure, payoffs, and common uses for currency options (calls/puts, strike, premium).

- Calculate and interpret currency option payoffs for various spot and strike scenarios, considering premium paid/received.

- Explain the structure, notional exchange, and cash flows in cross-currency swaps.

- Identify main uses of cross-currency swaps for risk management and market access.

- Differentiate between the risk exposures and strategic roles of currency options and swaps.

- Recognize exam traps regarding early exercise and valuation basis for options and swaps.

Key Terms and Concepts

- currency option

- cross-currency swap

- strike price

- notional principal

- swap spread