Learning Outcomes

This article explains market-based and private company valuation using price and enterprise value multiples in a CFA Level 2 setting, including:

- describing the role of price and enterprise value multiples in equity and enterprise valuation, and distinguishing between P/E, P/B, P/S, P/CF, and EV/EBITDA;

- demonstrating how to select appropriate peer groups and apply the method of comparables to estimate equity value for public and private firms;

- showing how to compute, interpret, and evaluate valuation multiples, including diagnosing when a multiple appears inconsistent with fundamentals or peer data;

- detailing how and why to normalize financial statements for nonrecurring items, owner-specific transactions, and non-market compensation before applying multiples;

- comparing market, income, and asset-based valuation approaches for private companies and assessing when each is most appropriate;

- explaining the concepts of discounts and premiums related to control and marketability, and incorporating DLOC and DLOM into private company valuations;

- integrating normalized earnings, selected multiples, and appropriate discounts or premiums to derive exam-style valuation estimates and to evaluate alternative valuations.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are required to understand market-based approaches to valuation for both public and private companies, with a focus on the following syllabus points:

- Recognizing and computing common price multiples (P/E, P/B, P/S, P/CF, EV/EBITDA) and their uses in valuation.

- Explaining and applying the method of comparables for both public and private company appraisal.

- Understanding and implementing normalization adjustments to earnings and other financial metrics.

- Evaluating the effect of control and marketability on private company valuations and correctly applying related discounts or premiums.

- Comparing income, market, and asset-based approaches to private company valuation.

- Calculating valuations using normalized earnings and multiples.

- Identifying rationale for discounts for lack of control (DLOC) and lack of marketability (DLOM).

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

Maria Lopez, CFA, is valuing a private manufacturing company, Alpha Tools, for a potential partial sale. Alpha Tools has historically paid its owner a salary far above market rates and rents its main facility from a related party at below-market rent. Maria constructs a peer group of listed tool manufacturers with similar products and business risk. The public peers report positive earnings and EBITDA, but differ in size, leverage, and geographic exposure. Maria observes that:

- The peer group’s average forward P/E (based on next year’s expected earnings) is 10.

- The peer group’s average EV/EBITDA (based on latest-twelve-month EBITDA) is 7.

- Control acquisitions of similar private companies in the sector have occurred at EV/EBITDA multiples around 8, reflecting meaningful expected combination benefits.

-

Before applying a P/E multiple to Alpha Tools, which normalization adjustment is most appropriate for Maria to make?

- a) Remove all depreciation expense because the peers use different depreciation methods.

- b) Replace the owner’s salary with a market-based salary for a professional manager.

- c) Eliminate all rent expense because the facility is owned by a related party.

- d) Capitalize advertising expense to align with peer accounting policies.

-

One of the following companies is least appropriate for inclusion in Maria’s peer group for the method of comparables. Which one is it?

- a) A listed tool manufacturer of similar size, margins, and growth, but with higher financial leverage.

- b) A listed industrial machinery company with similar leverage and margins but exposed to a different end market and business cycle.

- c) A listed small-cap tool manufacturer with lower liquidity but similar products and geographic exposure.

- d) A listed tool manufacturer in the same region with temporarily depressed earnings due to a one-off plant closure.

-

Maria wants to value a 25% minority interest in Alpha Tools using the EV/EBITDA multiple of 8 observed in recent control transactions. Which statement best describes the implication for her valuation?

- a) The control-based multiple already embeds a discount for lack of control, so she should apply a DLOC to reach a control value.

- b) Using a control-based multiple gives a control-equivalent value; she should then apply a DLOC if she needs a minority, marketable value.

- c) Using a control-based multiple gives a minority-equivalent value; she should then apply a control premium to reach a control value.

- d) The control-based multiple automatically incorporates a discount for lack of marketability, so no DLOM should be applied.

-

If Maria is most concerned about differences in depreciation methods and capital structure between Alpha Tools and its peers, which multiple is least affected by these differences?

- a) Trailing P/E based on net income.

- b) P/B based on book value of equity.

- c) EV/EBITDA based on enterprise value and EBITDA.

- d) P/CF based on cash flow from investing activities.

Introduction

Market-based valuation is central in security analysis and transaction practice. You need to know how to apply, interpret, and evaluate multiples—both for public markets and private companies—on the CFA exam. Multiples provide a quick tool to assess value using current market prices and comparables. For private companies, normalizing earnings and considering discounts or premiums are critical for credible results. This article covers these essential analysis tools for exam day.

Key Term: price multiple

A ratio that relates a firm’s market value (for example, share price or total equity value) to a specific financial metric such as earnings, book value, sales, or cash flow. Key Term: enterprise value

A measure of total firm value equal to market value of equity plus market value of debt and any noncontrolling interests, minus cash and cash equivalents; it represents the value of core operations available to all capital providers. Key Term: EV/EBITDA multiple

An enterprise value multiple that divides enterprise value by earnings before interest, taxes, depreciation, and amortization; it compares the value of the firm’s operations to a pre-interest, pre-tax, and largely pre-accounting-income measure of performance. Key Term: method of comparables

An approach that values a subject company by comparing its valuation multiples to those of similar companies, under the assumption that similar assets should have similar valuations. Key Term: normalization

The adjustment of reported financial results to better reflect a company's typical, sustainable performance—by removing unusual, nonrecurring, or non-market items—to improve comparability and relevance for valuation. Key Term: normalized earnings

An estimate of earnings that removes nonrecurring, transitory, and owner-specific effects, and reflects the level of earnings expected over a full business cycle under typical operating conditions. Key Term: discount for lack of control (DLOC)

A percentage deduction from a pro-rata share value to reflect the absence of rights to make key operating or financial decisions, commonly applied to minority equity interests in private firms. Key Term: discount for lack of marketability (DLOM)

A deduction applied to the value of an ownership interest to account for its illiquidity or the inability to readily convert it to cash at prevailing market prices. Key Term: minority (noncontrolling) interest

An equity interest that does not provide the holder with the power to direct corporate policies, appoint management, or initiate strategic actions such as mergers, major asset sales, or dividend changes. Key Term: control premium

The percentage by which the purchase price of a controlling interest in a company exceeds the value implied by its current market price on a noncontrolling, marketable basis. Key Term: levels of value

A framework describing valuation bases such as controlling, marketable interest value; noncontrolling, marketable interest value; and noncontrolling, nonmarketable value, which are linked by discounts and premiums for control and marketability. Key Term: market approach

A valuation approach that estimates value by reference to observable prices and multiples from comparable publicly traded companies or completed transactions. Key Term: income approach

A valuation approach that estimates value as the present value of expected future cash flows or earnings, discounted at an appropriate rate. Key Term: asset-based approach

A valuation approach that derives equity value by adjusting the company’s assets and liabilities to current market (fair) value and subtracting the adjusted liabilities from the adjusted assets.

Market-Based Valuation: Price Multiples and Comparables

Price multiples are widely used to estimate the value of companies. The most common are price-to-earnings (P/E), price-to-book (P/B), price-to-sales (P/S), price-to-cash-flow (P/CF), and enterprise value-to-EBITDA (EV/EBITDA). For each, you divide the market value measure (for example, price per share, market capitalization, or enterprise value) by the measure of fundamental performance.

At a high level:

- Equity value multiples use an equity numerator (price per share or market capitalization) and an equity denominator (earnings to equity, book value of equity, sales per share, or cash flow to equity).

- Enterprise value multiples use enterprise value in the numerator and a pre-interest, operating-level denominator (EBIT, EBITDA, or revenue), making them less sensitive to capital structure.

The method of comparables involves determining an appropriate multiple from a group of similar companies (the “peer group” or “guideline companies”) and applying it to the subject company’s financial measure. This provides an estimate of value if the subject were to trade in line with its peers.

In addition to market prices of listed peers, you may also use multiples from recent transactions:

- Guideline public company method: uses trading multiples of similar listed companies.

- Guideline transactions method: uses observed transaction multiples from acquisitions of comparable companies, which typically reflect control premiums and sometimes expected combination benefits.

Key Term: guideline public company method

A market approach that values the subject company by applying trading multiples derived from similar publicly traded companies to the subject’s fundamentals. Key Term: guideline transactions method

A market approach that values the subject company by applying valuation multiples observed in completed acquisitions of comparable companies to the subject’s fundamentals.

Using transaction-based multiples without recognizing that they embed control and possibly value from anticipated combination benefits is a common exam trap.

Selection of Comparables

Selecting valid comparables requires careful judgment. For the CFA exam, expect item sets that test whether a proposed peer group is appropriate. Key considerations include:

-

Sector/industry and line of business:

- Products and services.

- Customer base and distribution channels.

- Regulatory environment.

-

Size, growth prospects, and profitability:

- Revenue scale.

- Margin profile (gross margin, EBITDA margin, net margin).

- Historical and forecast growth rates.

-

Business risk and cyclicality:

- Exposure to economic cycle, commodity prices, or regulation.

- Stability of cash flows.

-

Geography and local market conditions:

- Currency risk.

- Country risk and inflation environment.

-

Financial leverage and capital structure:

- Debt-to-equity and interest coverage.

- Lease versus own, off–balance sheet obligations.

Where material differences exist, you have three choices:

- Adjust the subject company’s financials (normalization).

- Adjust the multiples you use (for example, use a lower multiple for slower growth or higher risk).

- Exclude the unsuitable peer and refine the peer group.

When computing the peer multiple, medians are often preferred to means because they are less influenced by outliers. Large differences between peer mean and median multiples in exam tables are a signal that outliers exist.

Computing and Interpreting Multiples

Suppose you are using the P/E ratio:

You must be clear which earnings measure is in the denominator:

- Trailing P/E: uses historical earnings (often last fiscal year or last twelve months).

- Forward P/E: uses forecast earnings (for example, next year’s EPS).

For valuation via comparables, forward P/Es are common because they reflect expected performance. However, you must ensure the peers’ earnings forecasts and the subject’s earnings estimate are on a comparable basis (same forecast horizon, same accounting basis).

To value a privately held company using P/E:

- Calculate normalized earnings (adjust for nonrecurring items, non-market compensation, or other owner-specific factors).

- Compute earnings per share (or use total earnings if valuing the whole equity).

- Apply the peer group average (or median) P/E multiple to the subject’s normalized earnings.

The same approach works for P/B, P/S, or EV/EBITDA by substituting the relevant metric and making suitable adjustments:

- P/B uses book value of equity (per share or total).

- P/S uses revenue (per share or total).

- EV/EBITDA uses enterprise value in the numerator and EBITDA in the denominator.

A key exam point is matching the level of value:

- Equity multiples (P/E, P/B, P/S, P/CF) give you an equity value directly.

- Enterprise multiples (EV/EBITDA, EV/EBIT, EV/Sales) give you enterprise value; you then subtract net debt and non-equity claims and add excess cash to reconcile to equity value.

Worked Example 1.1

You are valuing PrivateCo, which reports $2,200,000 in net income adjusted for non-market owner salary. Three public peer companies have normalized P/E ratios averaging 11. You assess a reasonable DLOM of 20%. What is the indicated minority equity value of PrivateCo?

Answer:

PrivateCo equity (marketable, minority basis) = $2,200,000 × 11 = $24,200,000. After DLOM for nonmarketability of the shares: $24,200,000 × (1 – 0.20) = $19,360,000.

Choosing the Right Multiple

Different multiples convey different information and have different strengths and weaknesses.

-

P/E (price-to-earnings):

-

Advantages:

- Directly relates price to earnings, the primary driver of equity value.

- Widely used and well understood.

-

Limitations:

- Sensitive to accounting policies (for example, depreciation, revenue recognition).

- Distorted when earnings are very low, negative, or highly cyclical.

- Affected by financial leverage, since net income is after interest.

-

-

P/B (price-to-book):

-

Advantages:

- More stable than earnings and rarely negative.

- Useful for financials and asset-heavy firms where book value approximates economic value.

-

Limitations:

- Less meaningful for firms with significant intangible assets (brands, IP) not fully captured on the balance sheet.

- Affected by accounting choices in asset valuation and impairment.

-

-

P/S (price-to-sales):

-

Advantages:

- Sales are less subject to accounting manipulation than earnings.

- Meaningful even when earnings are negative.

-

Limitations:

- Ignores differences in cost structure and profitability.

- High P/S can be justified only if margins and growth are strong.

-

-

P/CF (price-to-cash-flow):

-

Advantages:

- Based on cash flow to equity (for example, CFO or free cash flow to equity).

- Less affected by noncash accounting charges.

-

Limitations:

- Requires consistent cash flow definitions across peers.

- CFO can be influenced by working-capital management and classification choices.

-

-

EV/EBITDA:

-

Advantages:

- Neutral to capital structure, because EBITDA is before interest and EV includes all capital providers.

- Less affected by differences in depreciation, which is useful across firms with different asset ages and accounting methods.

- Often used in private equity and M&A contexts.

-

Limitations:

- EBITDA ignores capital expenditures; high EBITDA may not mean high free cash flow.

- Not meaningful when EBITDA is negative or extremely volatile.

-

When using multiples from transactions (for example, for private company sales), ensure the deal context is comparable:

- Were the transactions for controlling stakes? If so, the multiples likely incorporate control premiums and possibly expected combination benefits.

- Were the buyers strategic (industrial) or financial (private equity)? Strategic buyers may pay more due to expected combination benefits.

- Were there distressed sales or special situations that may bias the observed multiples?

Using a control-based multiple without adjusting for the level of value can misstate your subject company’s minority interest value.

Linking Multiples to Fundamentals

Multiples are not arbitrary; they can be linked to fundamental drivers. For example, under a constant-growth dividend discount model, the justified P/E is:

where:

- = retention ratio.

- = required return on equity.

- = sustainable growth rate.

Similarly, the justified P/B ratio can be expressed as:

A stock with higher expected ROE, higher growth, or lower risk (lower ) should, all else equal, have a higher justified P/E and P/B. On the exam, you may be asked to determine whether a company’s observed multiple is “too high” or “too low” relative to its fundamentals:

- A low P/E for a firm with high expected growth, high ROE, and similar risk can indicate undervaluation.

- A high P/B for a firm with ROE barely covering the cost of equity may signal overvaluation.

The method of comparables implicitly assumes the peers’ multiples are justified by their fundamentals. Comparing fundamentals alongside multiples allows you to diagnose inconsistencies.

Worked Example 1.2

A listed peer group has the following characteristics:

- Peer median ROE = 12%.

- Peer median growth rate in earnings = 4%.

- Peer median P/B = 1.8.

- Required return on equity for the sector is 8%.

Company X has:

- ROE = 16%.

- Expected earnings growth = 6%.

- Same required return (8%).

- Observed P/B = 1.9.

Based on fundamentals, is Company X more likely overvalued, undervalued, or fairly valued relative to peers?

Answer:

The justified P/B for the typical peer is approximately

Yet the peer median P/B is 1.8, suggesting the group may trade at a slight discount to fundamental value. For Company X, justified P/B is

X’s fundamentals (higher ROE and growth at similar risk) justify a higher multiple than peers. A P/B of 1.9 is low relative to its justified 2.5 and only slightly above the peer median, suggesting X is more likely undervalued than overvalued relative to peers.

Exam Warning: Be sure to normalize the financial metric used as the multiple’s denominator—do not blindly apply multiples to reported net income or EBITDA, as owner-specific or nonrecurring adjustments may materially distort value. Failing to adjust can overstate or understate fair market value and is a common exam trap.

Normalization Adjustments and Private Company Valuation

Privately owned businesses often report results that do not reflect market-based, sustainable performance. Normalization is necessary to enable valid comparison with public peers.

Two broad categories of normalization are important:

- Company-specific, nonrecurring, or non-market items.

- Business-cycle or trend-related adjustments.

Company-Specific Normalization

Common adjustments include:

-

Non-market owner salaries or benefits:

- Owners may pay themselves above-market salaries, bonuses, or fringe benefits.

- Adjust reported expenses to reflect what an independent manager would be paid at market rates.

-

Excess or below-market rent/lease agreements with related parties:

- Replace related-party rent expense with an estimate of market rent.

-

One-off income or expense items:

- Remove litigation settlements, gains or losses on asset sales, insurance recoveries, restructuring charges, and major impairment losses that are not expected to recur.

-

Pro-forma for recent major acquisitions/divestitures or temporary business disruptions:

- Adjust historical results as if the acquisition, divestiture, or plant opening/closing had been in effect for the whole period.

-

Capitalization policy and classification differences:

- Ensure that major repairs, R&D, and advertising are treated consistently with peers (for example, expensed versus capitalized).

For private companies, there may also be issues of incomplete adherence to GAAP/IFRS, cash versus accrual accounting, and related-party transactions that must be adjusted to approximate public-company comparability.

Worked Example 1.3

The owner of EquipmentCo pays herself $500,000 per year, but public peers pay $250,000 for similar roles. EquipmentCo’s reported net income is $700,000. What is normalized net income?

Answer:

Normalize owner compensation: reported expense is $500,000, but market-based is $250,000. Excess expense = $500,000 – $250,000 = $250,000. Add back the excess to net income: Normalized net income = $700,000 + $250,000 = $950,000.

Business-Cycle Normalization

For cyclical companies, a single-year metric can misrepresent sustainable performance. Normalization may require:

- Averaging margins or returns over a full business cycle (for example, 5–10 years).

- Using mid-cycle commodity prices rather than current spot prices.

- Adjusting for temporarily high or low capacity utilization.

On the exam, you might see a company with exceptionally high earnings in a boom year. Applying a peer P/E to current “peak” earnings would overstate value. Instead, you would normalize earnings toward a mid-cycle level.

Worked Example 1.4

CycCo operates in a cyclical industry. Over the last five years, its EPS has been: –1.00, 0.50, 2.00, 3.00, and 1.50. The current year EPS (3.00) coincides with a demand boom. Peers trade at a trailing P/E of 8, based on normalized demand. Which EPS should you use in the denominator to estimate value with the peer P/E?

Answer:

A simple average EPS over the cycle is:

Using the current boom-year EPS of 3.00 would overstate sustainable earnings and hence value. The analyst should use a normalized EPS, such as the cycle average of 1.20, when applying the peer P/E of 8.

Discount and Premium Adjustments

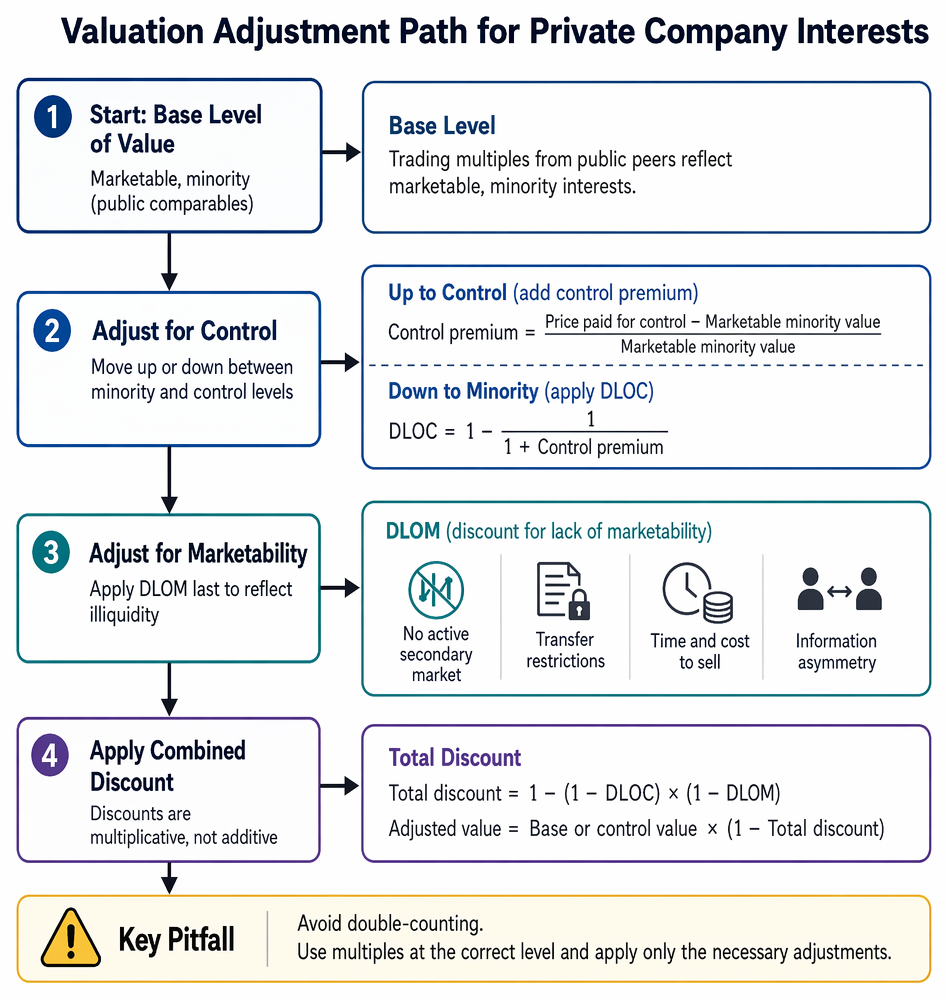

When using public company multiples for private company valuation, you must adjust for differences in both control and marketability and for the level of value at which the peer multiples are measured.

Equity-value and enterprise-value ratios are grouped by valuation basis, with representative measures including P/E, P/B, EV/EBITDA, and EV/Sales.

Control Versus Minority Interests

Public market prices generally reflect the value of a minority, marketable interest (small shareholdings with liquidity, but no control). Control transactions (acquisitions of 100% or a controlling block) typically occur at prices above this level, reflecting control premiums.

- A control premium is often expressed as:

- The equivalent DLOC that converts a control value back to a minority value is:

If you:

- Start with trading multiples from public peers (minority, marketable level), and you are valuing a controlling interest, you may add a control premium or use higher “control-level” multiples if justified.

- Start with transaction multiples based on control deals, and you are valuing a minority interest, you should apply a DLOC to move from control value down to minority, marketable value.

Worked Example 1.5

Recent acquisitions of comparable companies occurred at prices representing an average 40% control premium to the pre-announcement public share prices. What is the implied DLOC if you start from a control-equivalent value and want to arrive at a minority, marketable value?

Answer:

Control premium = 40% → 0.40. The implied DLOC is:

So, DLOC ≈ 28.6%. If the control-equivalent value is $10 million, minority, marketable value ≈ $10 million × (1 – 0.286) = $7.14 million.

Marketability (Liquidity) Adjustments

Private company interests are typically illiquid, particularly small minority interests with restrictions on transfer. A DLOM is applied to reflect:

- Absence of an active secondary market.

- Legal or contractual transfer restrictions.

- Expected time and cost to sell the interest.

- Information asymmetry and buyer negotiating power.

Estimating DLOM in practice involves empirical studies (for example, restricted stock and pre-IPO studies) or option-pricing models. On the exam, you will be given a DLOM percentage to apply.

The total discount for lack of control and lack of marketability is multiplicative, not additive:

Worked Example 1.6

You estimate a DLOC of 15% and a DLOM of 25%. What is the total combined discount to apply to the value of a minority private company share?

Answer:

Total discount

Combined discount = 36.25%. If the marketable, minority value is $1,000,000, the nonmarketable, minority value is $1,000,000 × (1 – 0.3625) = $637,500.

Ordering matters conceptually:

- Start from the appropriate base level of value (often marketable, minority, based on public comparables).

- Move up or down the levels of value with control premiums or DLOC.

- Apply DLOM last to adjust for lack of marketability.

A common exam pitfall is double-counting either control or marketability effects when the multiples already reflect them (for example, using private transaction multiples that already embed illiquidity and then adding a DLOM).

Valuation Methods for Private Companies

There are three primary approaches to valuing private companies:

- Market approach

- Income approach

- Asset-based approach

Market Approach

The market approach relies on comparison with observable prices for similar assets. In private-company contexts, three methods are common:

-

Guideline public company method:

- Select a peer group of similar listed firms.

- Compute relevant multiples (P/E, EV/EBITDA, P/S, etc.).

- Apply peer multiples to the subject’s normalized metrics.

- Adjust for differences in size, growth, and risk as needed.

-

Guideline transactions method:

- Use multiples from completed M&A transactions involving comparable firms.

- Be explicit about whether the multiples reflect control and combination-benefit values.

-

Prior transaction method:

- Use pricing from recent transactions in the subject company’s own shares, if arm’s length and representative.

Advantages of the market approach:

- Grounded in observable market data.

- Relatively simple and intuitive.

- Often persuasive in transaction and tax settings.

Limitations:

- Requires truly comparable companies or transactions.

- Market mispricing or unusual transaction conditions can bias the multiples.

- Harder to apply when the subject firm is unique or in a niche.

Income Approach

The income approach estimates value as the present value of expected future economic benefits. Two variants are particularly relevant:

-

Discounted cash flow (DCF) method:

- Forecast free cash flow to the firm (FCFF) or free cash flow to equity (FCFE).

- Discount at the weighted average cost of capital (for FCFF) or cost of equity (for FCFE).

- Use an explicit forecast period plus a terminal value.

-

Capitalized cash flow method:

- Use a single normalized cash flow figure.

- Capitalize it by dividing by a capitalization rate:

- Suitable for mature firms with stable growth.

Private company discount rates typically incorporate:

- Small-size risk premiums.

- Company-specific risk premiums (for concentration, key person risk, limited diversification).

Normalization is critical here as well—cash flows used must be sustainable and consistent with the discount rate assumptions.

Asset-Based Approach

The asset-based approach estimates equity value as:

Key steps:

- Adjust book values of assets and liabilities to fair values (market-based).

- Include off–balance sheet assets and liabilities where relevant (for example, operating lease commitments, contingent liabilities).

- For operating businesses, value intangible assets where possible.

The asset-based approach is most appropriate when:

- The company is asset-rich and earnings are not the primary value driver (for example, an investment holding company, real estate holding company, or natural resource firm).

- The business is not a going concern, and liquidation value is relevant.

- Earnings or cash flows are too volatile or unreliable for an income approach.

For many operating companies with significant intangible value, the asset-based approach will understate going-concern value.

Worked Example 1.7

You are valuing a private manufacturing firm, ManuCo, using the market approach with EV/EBITDA. ManuCo has:

- Normalized EBITDA = $4 million.

- Interest-bearing debt = $6 million.

- Cash and cash equivalents = $1 million.

- No noncontrolling interests or preferred stock.

A guideline public company analysis yields a median EV/EBITDA of 7. Apply the multiple and derive ManuCo’s equity value (marketable, minority basis).

Answer:

Enterprise value estimate: EV = 7 × $4 million = $28 million. Equity value = EV – net debt Net debt = Debt – Cash = $6 million – $1 million = $5 million. Equity value = $28 million – $5 million = $23 million. This $23 million reflects a marketable, minority interest level of value, assuming the peer multiples are from publicly traded minority shares.

Choosing the Appropriate Approach

On the exam, you may be asked to select the most appropriate valuation approach given a scenario:

-

Market approach is often preferred when:

- Sufficient, reliable data on comparable public companies or transactions exist.

- The subject company is profitable and operates in a reasonably active segment.

-

Income approach is preferred when:

- The company’s fundamentals (cash flows, growth, risk) are the primary drivers.

- Comparable companies are scarce or not truly comparable.

-

Asset-based approach is preferred when:

- The business is asset-intensive and earnings are secondary.

- The firm may be liquidated, or has poor earnings but substantial asset value.

In practice (and on the exam), analysts often triangulate among approaches, using one as the primary method and the others as reasonableness checks.

Revision Tip: For CFA exam questions, always check if normalization is needed before applying a multiple. Watch for owner compensation, related-party rents, one-time gains or losses, and unusual tax situations, as exam questions often hide these inside the financials.

Summary

Market-based valuation with multiples is a central skill for CFA candidates. Accurately valuing public and private companies requires selecting suitable comparables, using appropriate multiples, and making necessary normalization adjustments. Understanding which multiples are most robust to accounting differences and capital structure, and linking observed multiples to fundamentals, allows you to diagnose mispricing and evaluate valuations.

For private companies, differences in control and liquidity materially impact value. You must determine the level of value implied by your data (control vs minority, marketable vs nonmarketable) and apply DLOC and DLOM only where appropriate, avoiding double-counting. Integrating normalized earnings or cash flows, carefully chosen multiples, and appropriate discounts or premiums leads to credible valuation estimates and sound exam answers.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain and calculate common price and enterprise value multiples (P/E, P/B, P/S, P/CF, EV/EBITDA) and understand their strengths and limitations.

- Apply the method of comparables, distinguishing between guideline public company and guideline transactions methods.

- Normalize financial results for owner-specific, nonrecurring, and business-cycle effects to derive normalized earnings or cash flows.

- Match equity and enterprise value multiples to the correct denominators and reconcile enterprise value to equity value.

- Recognize and correctly apply discounts and premiums for control (DLOC, control premium) and marketability (DLOM), and combine them multiplicatively.

- Compare market, income, and asset-based approaches to private company valuation and identify when each is most appropriate.

- Integrate normalized metrics, selected multiples, and appropriate discounts or premiums to compute and evaluate private company valuations in exam-style scenarios.

Key Terms and Concepts

- price multiple

- enterprise value

- EV/EBITDA multiple

- method of comparables

- normalization

- normalized earnings

- discount for lack of control (DLOC)

- discount for lack of marketability (DLOM)

- minority (noncontrolling) interest

- control premium

- levels of value

- market approach

- income approach

- asset-based approach

- guideline public company method

- guideline transactions method