Learning Outcomes

This article explains how the Black-Scholes-Merton (BSM) option valuation framework and Greeks are used in pricing and risk management for CFA Level 2, including:

- Describing the structure, assumptions, and intuition of the Black-Scholes-Merton model for European calls and puts, and recognizing where the model’s assumptions break down in real markets.

- Interpreting each BSM input—spot price, strike, time, risk-free rate, dividend yield, and volatility—and assessing the direction and relative magnitude of their impact on call and put values.

- Calculating and interpreting the primary option Greeks (Delta, Gamma, Vega, Theta, Rho) across different regions of moneyness and maturities, and relating them to exam-style scenario analysis.

- Using first- and second-order Greeks to approximate option price changes for joint moves in the asset price, volatility, interest rates, and time, and understanding the limitations of these linear and quadratic approximations.

- Defining implied volatility, explaining how it is inferred from market prices, contrasting it with historical and realized volatility, and linking it to volatility smiles and surfaces across strikes and maturities.

- Applying Greeks and implied volatility to tasks such as constructing and rebalancing delta-neutral hedges, managing Vega exposure in option portfolios, and evaluating whether options are rich or cheap relative to a stated volatility view or risk-management objective.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are required to understand how Black-Scholes-Merton valuation and volatility concepts are applied to equity and currency options, with a focus on the following syllabus points:

- Applying the Black-Scholes-Merton option valuation model assumptions and formula for European-style options on non-dividend and dividend-paying assets.

- Identifying and interpreting the option Greeks and their use in measuring and managing sensitivity to key risk factors.

- Explaining how changes in price, volatility, interest rates, and time jointly affect call and put values and Greek exposures.

- Defining implied volatility and describing how it is extracted from market prices and used in trading and risk management.

- Analyzing option price changes due to variations in Greeks and volatility, including volatility smiles and surfaces.

- Applying option Greeks to delta hedging and assessing volatility-risk exposures at the portfolio level.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

A portfolio manager holds a long position in 10,000 shares of a non-dividend-paying stock currently priced at $50. The manager considers hedging with 3‑month at-the-money European calls priced using the BSM model; each call has a delta of 0.52 and a Vega of 0.10 (per 1% volatility). Which statement about a delta hedge using these calls is most accurate?

- a) The manager should buy 5,200 calls, creating a net long delta exposure of +5,200.

- b) The manager should short 5,200 calls, making the portfolio approximately delta-neutral to small stock-price moves.

- c) The manager should short 10,000 calls, fully eliminating both delta and gamma risk.

- d) The manager should buy 10,000 calls to offset the stock’s positive delta and gain positive Vega.

-

Consider a 6‑month European call and put on the same stock with the same strike. The options are priced with the Black-Scholes-Merton model. Which change in an input will increase the value of both the call and the put?

- a) A decrease in the stock price.

- b) A decrease in volatility.

- c) An increase in time to expiration.

- d) A decrease in the risk-free interest rate.

-

A trader observes that 3‑month at-the-money calls on a stock are trading at an implied volatility of 18%. Based on fundamental and statistical analysis, she expects realized volatility over the next 3 months to be 25%. Assuming she wants to express only a volatility view (not a directional price view), which position is most consistent with her expectations?

- a) Short calls to exploit the overpricing of implied volatility.

- b) Long calls or long straddles to gain positive Vega exposure.

- c) Short straddles to benefit from time decay (Theta).

- d) Short stock and long calls to form a synthetic put position.

-

A risk manager analyzes a portfolio that is short a large number of near-expiry at-the-money options. The portfolio has small net delta but large negative gamma and large negative theta. Which risk description is most appropriate?

- a) The portfolio is well-hedged because delta is near zero; gamma and theta are second-order and can be ignored.

- b) The portfolio will benefit from large jumps in the asset price but will lose if the price does not move.

- c) The portfolio is vulnerable to abrupt price moves (gamma risk) and gains from the passage of time if the asset price is stable.

- d) The portfolio has positive exposure to volatility (positive Vega) and therefore profits when implied volatility falls.

-

A European call on a dividend-paying stock is valued using the BSM model with a continuous dividend yield . Which interpretation of is most consistent with risk-neutral valuation?

- a) The actual (real-world) probability that the option expires in the money.

- b) The risk-neutral probability that the option expires in the money.

- c) The delta of the call option.

- d) The Vega of the call option.

Introduction

Valuing options accurately is essential for CFA Level 2. European-style options on stocks, indices, currencies, and other assets are typically valued using the Black-Scholes-Merton (BSM) model, which assumes particular market conditions and provides a closed-form pricing formula. The BSM model output is highly sensitive to the inputs—especially volatility—making an understanding of the Greeks and implied volatility critical for exam success and for real-world application in risk management and option trading.

Key Term: Black-Scholes-Merton model

Mathematical model that produces theoretical prices for European options by discounting expected payoffs under risk-neutral pricing, based on stock price, strike price, time to maturity, risk-free rate, volatility, and dividend yield. Key Term: option Greeks

Partial derivatives of an option’s price with respect to key model parameters (asset price, volatility, time, and interest rates), summarizing the option’s sensitivity to market changes. Key Term: implied volatility

The volatility of the asset that, when used as the volatility input in the BSM model, makes the model price equal to the observed market price of the option. Key Term: moneyness

The relationship between the current asset price and the option’s strike: in-the-money (ITM), at-the-money (ATM), or out-of-the-money (OTM).

In the BSM framework, Greeks quantify how model prices react to changes in each input. Implied volatility links those model prices to actual market quotes: rather than plugging in a volatility estimate and computing a price, traders often start from the observed price and “back out” the volatility that the market is implying. Level 2 questions often require analyzing how a combination of price moves, time decay, and volatility changes affects option values and risk exposures.

THE BLACK-SCHOLES-MERTON OPTION VALUATION MODEL

The BSM model values options on non-dividend and dividend-paying stocks, assuming frictionless markets, constant volatility and interest rates, continuous trading, and no early exercise (European-style).

For a stock with continuous dividend yield , the BSM formula for a European call and put is:

Where:

- , = current call and put values

- = current asset price

- = exercise price

- = time to expiration (in years)

- = continuously compounded risk-free rate

- = continuous dividend yield

- = cumulative standard normal probability

and

where is the annual volatility of the asset’s continuously compounded return.

The core BSM assumptions, which are frequently tested conceptually, are:

- Asset prices follow a continuous “random walk” (geometric Brownian motion) with constant drift and volatility—no jumps.

- The risk-free rate and volatility are constant and known.

- Markets are frictionless: no taxes, no transaction costs, no restrictions on short selling, and continuous trading.

- The asset can be shorted, and borrowing/lending is at the risk-free rate.

- Dividends (or other yields) are paid at a constant continuously compounded rate .

- Options are European; early exercise is not permitted.

Key Term: risk-neutral probability

Probability measure under which all assets are expected to grow at the risk-free rate; under this measure, discounted expected payoffs equal current prices.

Under risk-neutral valuation:

- is the risk-neutral probability that a call finishes in-the-money.

- can be interpreted as the present value of the expected asset price at expiry, conditional on exercise.

- A European call can be viewed as a leveraged position: long units of the stock, financed partly by borrowing .

These economic interpretations are often more important at Level 2 than memorizing the exact formulas.

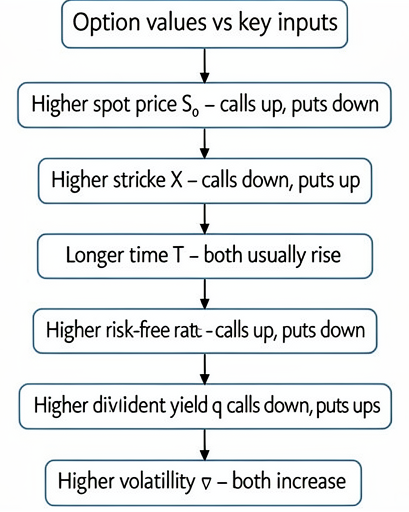

BSM Inputs and Directional Effects

For European options on a stock paying a continuous dividend yield:

- Higher : increases call values, decreases put values.

- Higher : decreases call values, increases put values.

- Longer : usually increases both call and put values (more time = more optionality).

- Higher : increases calls, decreases puts (carrying cost of the strike).

- Higher : decreases calls, increases puts (dividends reduce the expected stock price).

- Higher : increases both calls and puts (more uncertainty = more optionality).

Exam questions may ask you to rank sensitivities or identify which input change could explain an observed price move.

OPTION GREEKS: SENSITIVITY TO KEY FACTORS

The Greeks quantify an option’s value response to small input changes. The five primary Greeks are:

- Delta (): Sensitivity to changes in the asset price.

- Gamma (): Sensitivity of delta to changes in the asset price.

- Vega (): Sensitivity to changes in volatility.

- Theta (): Sensitivity to the passage of time (time decay).

- Rho (): Sensitivity to changes in the risk-free rate.

For a stock with continuous dividend yield , closed-form expressions (not required to memorize, but useful conceptually) are:

- Call delta:

- Put delta:

- Gamma (same for call and put):

- Vega (same for call and put, per 1 unit of ):

- Rho and Theta have more complex forms but their signs and relative magnitudes are most important.

Here is the standard normal density function.

Delta ()

Delta measures the change in the option’s value for a small change in the asset price:

For calls, Delta ranges from 0 to (approximately 0 to 1 when is small). For puts, Delta ranges from (approximately -1) to 0.

Key Term: delta (Δ)

The rate of change of an option’s price with respect to changes in the price of the asset; for calls it is positive, for puts it is negative.

Key patterns:

- Deep OTM call: Delta near 0 (little sensitivity).

- ATM call: Delta around 0.5 (or ).

- Deep ITM call: Delta near 1.

- ATM put: Delta around −0.5.

- Deep ITM put: Delta near −1.

As time passes (holding the asset price fixed):

- ITM call delta tends toward 1; OTM call delta tends toward 0.

- ITM put delta tends toward −1; OTM put delta tends toward 0.

Delta has two key uses at Level 2:

- Directional risk measure: A call with delta 0.6 behaves like 0.6 shares of stock.

- Tool for hedging: Delta-neutral strategies choose option quantities so that the net delta of a position is approximately zero.

Key Term: delta-neutral hedge

A combination of positions in the asset and options constructed to have net delta approximately zero, so that small moves in the asset price have minimal impact on the portfolio’s value.

Gamma ()

Gamma quantifies how Delta itself changes as the asset price moves:

Key Term: gamma (Γ)

The sensitivity of an option’s delta to small changes in the asset price; it captures the curvature of the option value with respect to the asset price.

Key properties:

- Long calls and long puts both have positive gamma.

- Gamma is highest for at-the-money options and increases as time to expiration decreases (for a fixed level of volatility).

- Deep ITM and deep OTM options have low gamma.

Gamma is central to understanding hedging error:

- A delta hedge is exact only for infinitesimal price changes.

- For larger moves, the hedge error is driven by gamma: high gamma portfolios require more frequent rebalancing to stay delta-neutral.

Key Term: gamma risk

The risk that large or abrupt moves in the asset price will cause significant changes in delta, making a previously delta-neutral hedge ineffective and leading to hedging losses.

Including gamma, a better approximation for the change in an option’s value is:

This parallels the way convexity improves the duration-only approximation for bond price changes.

Vega ()

Vega measures the sensitivity of the option price to changes in volatility:

Because both calls and puts become more valuable when volatility rises (greater range of possible favorable outcomes), Vega is positive for both.

Key Term: vega (ν)

The change in an option’s price for a 1 percentage point (1%) change in the volatility of the asset.

Key Vega patterns:

- Highest for at-the-money options with longer time to expiration.

- Lower for deep ITM/OTM options or very short-dated options.

- Long option positions (calls or puts) have long Vega; short options have short Vega.

Vega is central for volatility trading and risk management: a trader who believes implied volatility is too low will typically seek a long Vega position (e.g., buying options), whereas a trader who thinks implied volatility is too high prefers short Vega (e.g., selling options).

Theta ()

Theta is the rate of change of the option value with respect to the passage of time, holding other inputs constant. It is usually quoted as the change in price per day:

Key Term: theta (Θ)

Sensitivity of an option’s price to the passage of time, reflecting time decay of the option’s extrinsic value; typically negative for long options.

Because an option’s time value erodes as expiration approaches:

- Theta is usually negative for both long calls and long puts.

- Short option positions have positive theta (they gain from time decay).

- Time decay accelerates for near-expiry, at-the-money options (these tend to have large negative theta).

There is one important exception: deep ITM puts very close to maturity can exhibit positive theta, because the time decay of the discounting of the strike can outweigh the loss of optionality. This detail is exam-relevant.

Rho ()

Rho measures the sensitivity of the option value to changes in the risk-free interest rate:

Key Term: rho (ρ)

The rate of change of an option’s price for a 1 percentage point (1%) change in the risk-free interest rate.

For European options:

- Call rho is positive: higher increases call values (the discounted strike becomes cheaper).

- Put rho is negative: higher decreases put values.

Rho is generally small for short-dated options and becomes more important for long-term options (LEAPS). Exam questions tend to focus on the sign of rho rather than its exact magnitude.

VOLATILITY AND OPTION PRICING

The BSM model is particularly sensitive to the volatility input. Because future volatility is not directly observable, practitioners often start from market prices and solve for the implied volatility that equates the BSM price to the observed option price.

Option valuation comparative statics indicate how changes in S0, X, T, r, q, and sigma affect call prices versus put prices.

Key Term: historical volatility

A backward-looking measure of volatility, typically computed from past returns of the asset over a specified window. Key Term: realized volatility

The volatility actually experienced over a period, computed from historical return data after the fact; used to compare against implied volatility.

Market-observed prices frequently disagree with a BSM price computed using historical volatility. The difference is captured by implied volatility, which reflects the market’s risk-neutral expectation of future volatility plus volatility risk premia and supply–demand effects.

Worked Example 1.1

A call option on a non-dividend-paying stock trades at $2.50 with the share price at $45, strike $45, 6 months to expiry (), and a continuously compounded risk-free rate of 3%. Volatility is unknown. What is the implied volatility if this call option’s market price is consistent with the BSM model?

Answer:

Set up the BSM call formula with the unknown σ:

where

There is no closed-form algebraic solution for σ, so traders solve numerically (trial and error or a root-finding algorithm). For example:

- At σ = 20%, the BSM price is approximately 2.86 (too high).

- At σ = 16%, the price is approximately 2.37 (too low). Interpolating between these values gives an implied volatility of roughly 17%. Any volatility estimate that makes the BSM price equal 2.50, given the other parameters, is by definition the implied volatility.

The Significance of Implied Volatility

Implied volatility (IV) reflects the market’s aggregate assessment—under risk-neutral pricing—of uncertainty in the asset price over the option’s life. Important exam points:

- IV is forward-looking; historical volatility is backward-looking.

- IV can be higher than realized volatility on average because option sellers demand compensation (a volatility risk premium).

- IV need not be constant across strikes or maturities for the same asset.

Key Term: volatility smile

The pattern of implied volatilities across strikes for options with the same asset and expiry, often showing higher IV for deep ITM and OTM options than for ATM options. Key Term: volatility surface

The three-dimensional pattern of implied volatilities across both strikes and maturities for a given asset.

In equity markets, implied volatility often exhibits a smirk or skew (higher IV for lower strikes), reflecting crash risk and demand for downside protection.

A trader who believes IV is lower than future realized volatility may buy options because they are “cheap” relative to perceived risk; if IV is higher, selling options could be preferred for a volatility trader.

Worked Example 1.2

Suppose an at-the-money option currently trades with an implied volatility of 18%. An analyst expects realized volatility over the option’s life to be closer to 25%, and is neutral on the direction of the asset price. How should the trader position the portfolio?

Answer:

The options appear underpriced on a volatility basis because implied volatility (18%) is below the forecast of realized volatility (25%). A rational volatility trader would seek long Vega exposure, for example by:

- Buying calls, buying puts, or

- Buying straddles (call + put at the same strike). All of these positions profit from higher-than-implied volatility, holding other factors constant.

OPTION SENSITIVITY IN PRACTICE

Understanding the effect of each input is critical for risk control and exam-style scenario analysis. For small changes, the combined impact of different factors on a call option’s value can be approximated as:

An analogous expression holds for puts. Qualitatively:

- An increase in the asset price raises call values and lowers put values (effect strongest near the money).

- Higher volatility increases the value of both calls and puts (positive Vega).

- The passage of time typically reduces the value of long options (negative Theta).

- Higher interest rates increase call values and decrease put values (through discounting of the strike).

- Dividend yield (or foreign interest rates for currency options) has the opposite effect of the risk-free rate on calls and puts.

Worked Example 1.3

A portfolio holds a short position in at-the-money call options with a Delta of 0.5 and a Vega of 0.12 (per 1% volatility). What is the immediate sensitivity of the portfolio to:

a) a $2 increase in the share price, and b) a 1% increase in implied volatility?

Answer:

a) The call price will increase by approximately

per option due to the price change. Because the position is short calls, the portfolio loses $1 per option. b) With Vega of 0.12, a 1% increase in volatility increases the option price by about $0.12 per option. A short call position therefore incurs a $0.12 loss per option. For small moves, the total P&L impact from simultaneous price and volatility changes would be approximately the sum of these effects, adjusted for gamma if the price move is large.

Delta Hedging and Gamma Risk

Delta and Vega exposure must be managed, especially for hedged portfolios. A common application of delta is dynamic hedging:

- To hedge a long stock position, an investor can short calls so that the net delta is near zero.

- Because option delta changes as the asset price moves (gamma), the hedge must be rebalanced frequently.

Key Term: dynamic hedging

A hedging strategy that requires frequent rebalancing of positions in the asset and options to maintain target Greek exposures (such as a delta-neutral position).

Worked Example 1.4

You hold 40,000 shares of a non-dividend-paying stock at $50. Three-month European calls with strike $50 have a delta of 0.5. Each option contract is on 100 shares. How many call contracts must you short to create a delta-neutral hedge against small price moves?

Answer:

The share position has total delta:

Each call option on 1 share has delta 0.5, so each contract (100 shares) has delta:

To offset +40,000 delta, the number of contracts to short is:

Shorting 800 call contracts creates a portfolio with approximate net delta zero. Because gamma is negative (long stock, short options), the hedge must be rebalanced as prices move.

Revision Tip: Learn how Delta, Gamma, Vega, and Theta change across:

- Moneyness (deep ITM, ATM, deep OTM), and

- Time to expiry (short vs long maturity).

Exam questions often focus on which Greeks dominate in different regions of the option surface, for example:

- ATM, near-expiry options: high Gamma and large negative Theta.

- Longer-dated ATM options: high Vega and moderate Gamma.

- Deep ITM options: Delta near ±1, low Gamma and Vega, relatively small time value.

Exam Warning: The BSM model assumes constant volatility, but real market volatility changes over time and is not directly observable. Historical volatility is a noisy proxy for future volatility and typically differs from implied volatility. Exam questions may expect you to:

- Explain why implied volatility can differ from historical/realized volatility.

- Discuss how volatility smiles and surfaces indicate violations of the constant-volatility assumption.

- Recognize that using a single volatility input for all strikes and maturities is an approximation.

Summary

The Black-Scholes-Merton model is central for CFA Level 2 option pricing. It provides closed-form values for European calls and puts under a set of assumptions, and gives intuitive interpretations for the components and . The option Greeks—Delta, Gamma, Vega, Theta, and Rho—summarize how option values respond to small changes in asset price, volatility, time, and interest rates.

Implied volatility connects observed market prices to the theoretical BSM model by identifying the volatility consistent with those prices. Comparing implied volatility to forecasts of realized volatility allows traders to assess whether options are expensive or cheap on a volatility basis. Greeks and implied volatility together underpin practical tasks such as:

- Constructing and maintaining delta-neutral hedges.

- Managing Vega and Gamma risk in option portfolios.

- Evaluating the impact of changes in volatility, interest rates, and time on portfolio risk and value.

For the exam, focus on understanding the direction and relative magnitude of Greek sensitivities, the qualitative effects of changes in BSM inputs, and the conceptual role of implied volatility rather than memorizing complex formulas.

Key Point Checklist

This article has covered the following key knowledge points:

- Describe the Black-Scholes-Merton model, its input variables, and its main assumptions.

- Interpret and in terms of risk-neutral probabilities and leveraged positions in the asset.

- Calculate and interpret the primary Greeks—Delta, Gamma, Vega, Theta, Rho—and understand their signs and ranges.

- Explain how volatility, time to expiration, and moneyness affect option prices and Greek magnitudes.

- Define and interpret implied volatility and distinguish it from historical and realized volatility.

- Use implied volatility views to motivate long or short Vega positions (e.g., buying or selling options).

- Apply option Greeks to approximate price changes, construct delta-neutral hedges, and assess gamma and Vega risk.

- Recognize how changes in BSM inputs affect call and put values and how volatility smiles and surfaces indicate model limitations.

Key Terms and Concepts

- Black-Scholes-Merton model

- option Greeks

- implied volatility

- moneyness

- risk-neutral probability

- delta (Δ)

- delta-neutral hedge

- gamma (Γ)

- gamma risk

- vega (ν)

- theta (Θ)

- rho (ρ)

- historical volatility

- realized volatility

- volatility smile

- volatility surface

- dynamic hedging