Learning Outcomes

This article explains option valuation and Greek-based hedging for CFA Level 2 candidates, including:

- Understanding the economic intuition behind option payoffs and non-linear risk profiles.

- Valuing European options using binomial trees and the Black-Scholes-Merton model, with attention to key assumptions and limitations.

- Computing delta, gamma, theta, vega, and rho from model outputs or scenario changes, and interpreting their units and signs.

- Relating each Greek to specific risk exposures—directional, convexity, time decay, volatility, and interest rate risk.

- Constructing single-period and multi-period delta and gamma hedges using the reference asset and additional options.

- Evaluating how changes in volatility, interest rates, and time to expiration affect option prices and hedge effectiveness.

- Applying Greeks to design and evaluate practical hedging strategies, including dynamic rebalancing and volatility trades.

- Distinguishing the risk profiles of long versus short option positions and explaining why delta neutrality does not eliminate gamma and theta risk.

- Solving typical CFA exam problems that involve option valuation, sensitivity analysis, and the diagnosis of flawed hedging approaches.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are required to understand how derivatives valuation incorporates option sensitivity measures (Greeks) and to analyze and apply hedging strategies using delta, gamma, theta, vega, and rho, with a focus on the following syllabus points:

- Explaining and using binomial and Black-Scholes-Merton option pricing models.

- Calculating, interpreting, and applying option Greeks (delta, gamma, theta, vega, rho).

- Constructing and adjusting single-period and multi-period hedges using delta and gamma.

- Assessing the impact of changes in volatility, time to expiration, and interest rates on option values.

- Executing dynamic hedging strategies and understanding their limitations in practice.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

Use the following information to answer Questions 1–4.

An analyst manages an equity portfolio worth $5,000,000 invested in a non-dividend-paying stock (price $50). To hedge the downside risk over the next few weeks, she trades European options on the same stock, all with one month to expiration. The risk-free rate is negligible over this horizon.

Her current derivatives positions and option Greeks (per option) are:

| Position | Quantity | Type | Strike | Delta | Gamma | Vega | Theta |

|---|---|---|---|---|---|---|---|

| Position A | +10,000 | Call | 50 | 0.55 | 0.035 | 0.18 | –0.04 |

| Position B | –5,000 | Put | 50 | –0.45 | 0.030 | 0.16 | –0.03 |

(All Greeks are per option, theta is per day, vega is per 1 percentage point change in volatility.)

-

Based only on the positions in A and B (ignore the stock for this question), what is the net delta of the option portfolio?

- a) –500

- b) +1,000

- c) +2,750

- d) +5,500

-

Including the $5,000,000 stock position, how many shares of stock should the analyst short (approximately) to create a delta-neutral portfolio?

- a) 100,000 shares

- b) 90,000 shares

- c) 80,000 shares

- d) 70,000 shares

-

Suppose implied volatility falls by 2 percentage points, with no change in the stock price. What is the approximate change in the value of the combined option portfolio (A and B only)?

- a) Loss of $5,600

- b) Loss of $6,800

- c) Loss of $8,000

- d) Gain of $8,000

-

Which statement about the analyst’s hedging profile is most accurate?

- a) The delta hedge also neutralizes gamma risk because total gamma is close to zero.

- b) The portfolio is short gamma overall, so large stock moves will likely generate losses from the options.

- c) The portfolio is long gamma overall, so large stock moves will likely generate profits from the options.

- d) The portfolio is vega-neutral, so changes in volatility will not materially affect option values.

Introduction

Options are contracts whose value depends on the price of an associated asset. Unlike linear instruments (such as stocks or bonds), options are highly sensitive to multiple variables including the asset price, volatility, interest rates, and time remaining until expiration. Because the payoff is non-linear in the reference asset price, the risk exposure of an option position cannot be fully described by a single beta or duration.

To measure and manage these risks, CFA candidates must understand the key option Greeks—delta, gamma, theta, vega, and rho—which quantify the sensitivity of option values to different risk factors. These sensitivities come directly from option valuation models such as binomial trees and the Black–Scholes–Merton (BSM) model and underpin most practical hedging strategies.

Key Term: Greeks

Derivative metrics that measure the sensitivity of an option’s value to a small change in a particular risk factor (asset price, volatility, time, or interest rates). Key Term: Delta

The rate of change of the option’s price with respect to the price of the reference asset; it also serves as the hedge ratio in many models. Key Term: Gamma

The rate of change of delta with respect to the price change of the reference asset; it captures the curvature (convexity) of the option’s price–asset price relationship. Key Term: Theta

The rate at which an option’s value changes as time passes, holding all else constant; it measures time decay. Key Term: Vega

The sensitivity of an option’s value to changes in the volatility of the reference asset, typically expressed per 1 percentage point change in volatility. Key Term: Rho

The sensitivity of an option’s value to changes in the risk-free interest rate, typically expressed per 1 percentage point change in the rate. Key Term: Delta-neutral hedge

A portfolio construction in which the sum of deltas across all positions is zero, making the portfolio (approximately) insensitive to small changes in the reference asset’s price. Key Term: Gamma-neutral hedge

A portfolio construction in which the sum of gammas across all positions is zero, so the portfolio’s overall delta is stable with respect to reference asset price movements. Key Term: Vega-neutral portfolio

A portfolio for which the sum of vegas is zero, so small changes in implied volatility do not affect the portfolio’s value. Key Term: Dynamic hedging

A hedging approach in which hedge ratios (for example, the number of shares held to maintain delta neutrality) are updated repeatedly as market conditions and Greeks change.

Understanding how to compute and interpret these quantities, and how to use them in hedging, is central to the Level 2 derivatives readings. Exam questions often embed Greek data in a vignette and ask you to recommend or assess a hedging strategy.

Test Tip: When revising Delta gamma theta vega and rho hedging, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

The Greeks: Measuring Option Risk

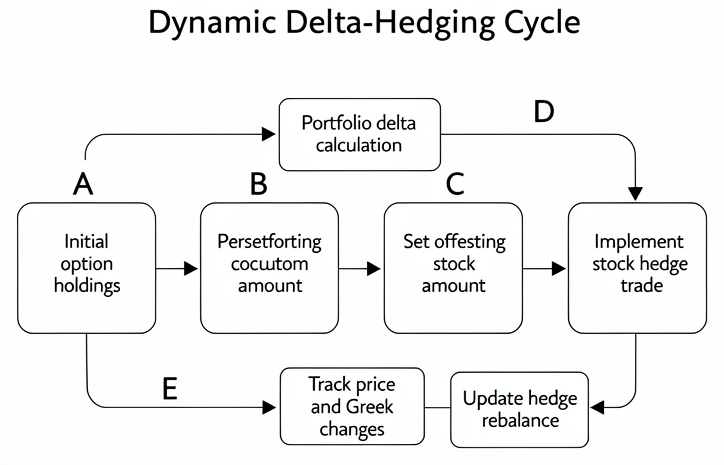

Dynamic delta-neutral hedging uses the underlying asset to offset portfolio delta and requires repeated recalculation and rebalancing over time.

Delta: Directional Sensitivity

Delta measures how much an option’s value will change for a small change in the price of the reference asset. Formally, for option price and asset price :

Delta can also be interpreted as the equivalent position in the reference asset per option.

- Call options: Delta is positive (between 0 and 1 for a non-dividend-paying asset).

- Put options: Delta is negative (between –1 and 0).

At-the-money (ATM) options have delta near 0.5 (calls) or –0.5 (puts). Deep in-the-money (ITM) calls have deltas close to +1; deep out-of-the-money (OTM) calls have deltas close to 0. The opposite holds for puts: deep ITM put deltas approach –1, deep OTM put deltas approach 0.

In the BSM framework for a European call on a non-dividend-paying stock, delta is:

and for the corresponding put:

where is the standard normal cumulative distribution function and is the usual BSM term. For a non-dividend-paying asset, call delta can be interpreted as the (risk-neutral) probability that the call will expire in the money.

From a hedging standpoint, if you are long one call with delta 0.6, you can offset its directional exposure by shorting 0.6 units of the reference asset. For a portfolio, portfolio delta is simply the quantity-weighted sum of individual deltas.

Gamma: Sensitivity of Delta

Gamma quantifies how much the delta of an option will change following a unit change in the price of the reference asset:

High gamma means the delta is very sensitive to asset price moves.

- Long options (long calls or long puts): Positive gamma.

- Short options: Negative gamma.

Gamma is highest for ATM options and increases as time to expiration decreases, up to a point. Deep ITM or deep OTM options have low gamma because their deltas are already close to +1/–1 or 0 and do not change much with small asset price moves.

In practice:

- A long gamma position (e.g., long straddles, long options in general) tends to profit from large moves in the asset price, whichever the direction, but usually has negative theta (time decay cost).

- A short gamma position (e.g., net option writing) tends to lose on large moves in either direction but typically has positive theta (earns time decay).

Call and put options on the same asset with the same strike and time to expiration have identical gamma.

Because delta alone only gives a linear approximation, gamma is used to refine the estimated change in option value for larger asset price moves:

This is directly tested at Level 2.

Theta: Time Decay

Theta represents the erosion of option value with the passage of time, commonly called “time decay.” Formally:

where is time (often measured in years). Because time is flowing forward, most practitioners quote theta as the change in option value per day.

For most long options:

- Theta is negative: as time passes, the option’s time value decays.

- The rate of decay accelerates as expiration approaches, especially for ATM options.

- Deep ITM or deep OTM options tend to have lower theta because they have relatively little time value.

Short option positions have positive theta—they benefit from time decay as long as the asset price does not move too much.

There is an important detail for European puts: deep ITM puts very close to expiration can have positive theta. Intuitively, as time passes, the present value of the exercise price falls slightly (because of discounting), which can, in extreme cases, more than offset the loss of time value.

Theta interacts strongly with gamma:

- Positions with positive gamma are usually negative theta.

- Positions with negative gamma are usually positive theta.

This trade-off—convexity versus time decay—is central to risk management.

Vega: Volatility Sensitivity

Vega measures the sensitivity of an option’s value to a 1% (or 0.01 in decimal terms) change in implied volatility :

Higher vega indicates greater price movement for changes in volatility.

- Long options (calls or puts): Positive vega.

- Short options: Negative vega.

Key patterns:

- ATM options have the largest vega because their value is mostly time value and very sensitive to volatility.

- For a given moneyness, vega generally increases with time to expiration—longer-dated options are more exposed to volatility changes.

- Vega is symmetric: long calls and long puts with the same strike and maturity have the same vega.

Vega is particularly important because implied volatility is not directly observable from the cash market; it is inferred from option prices. Volatility trading strategies (such as long straddles, strangles, or calendar spreads) are designed to express views on volatility and are analyzed in terms of vega.

Rho: Interest Rate Sensitivity

Rho is the change in option value due to a 1 percentage point (0.01) change in the risk-free rate :

For European options on non-dividend-paying assets:

- Call options: Rho is positive—higher interest rates increase call values.

- Put options: Rho is negative—higher interest rates decrease put values.

Intuition: increasing interest rates raise the present value of holding the asset (relative to paying the exercise price later), favoring calls and hurting puts.

In most equity options, rho is relatively small compared with delta, gamma, theta, and vega. However, for long-dated options, index options, or options on interest-rate-sensitive assets, rho can be material.

Option Hedging Using the Greeks

The Greeks are not just theoretical constructs; they drive practical hedging strategies.

Key Term: Delta hedging

A hedging technique that uses positions in the reference asset to offset the net delta of an option position, creating a delta-neutral portfolio.

Delta Hedging

A delta hedge means holding a position in the reference asset that offsets the delta of the option position, making the portfolio’s value (approximately) insensitive to small moves in the reference asset.

For a portfolio with total option delta , you choose a stock position such that:

If one share has delta 1, then:

- Number of shares to buy (if option delta is negative) or short (if option delta is positive) is:

For options quoted per contract, remember to multiply the per-option delta by the contract size.

Delta hedging is approximation-based:

- It protects against small price changes only.

- As the asset price moves, delta changes (because of gamma), so the hedge must be rebalanced dynamically.

This is known as dynamic hedging and is conceptually linked to the BSM derivation, which replicates an option payoff by continuously rebalancing a stock–bond portfolio.

Gamma Hedging

While delta hedging neutralizes exposure to small price changes, gamma hedging further addresses changes in delta itself.

A gamma hedge involves:

- Adding positions (typically in other options) to adjust the total gamma of the portfolio to zero (gamma-neutral).

- At the same time, re-adjusting positions to keep delta at or near zero.

Because the reference asset has zero gamma, you cannot change gamma using only that asset; you must use other options.

Mechanically, suppose you have:

- Existing portfolio with delta and gamma .

- A second option with known delta and gamma per contract.

If you add contracts of the second option, you solve:

- Gamma-neutrality:

- Then adjust the stock position to restore delta neutrality:

Gamma hedging is more complex and costly than simple delta hedging because it uses additional options and must be updated as markets move. In practice, many hedgers accept some gamma exposure and focus on managing the trade-off between gamma and theta.

Vega and Volatility Hedging

To hedge vega, an options trader must use additional options, as vega cannot be hedged using only the reference asset (which has zero vega).

A vega-neutral portfolio satisfies:

where are position sizes. Typically:

- If you are long vega (e.g., long ATM options), you hedge by shorting other options with similar vega.

- If you are short vega (e.g., short options), you may buy options to cap volatility risk.

Because gamma and vega are often positively related (a position with large positive gamma is usually long vega), hedging one will affect the other. Multi-Greek hedging problems on the exam often require you to solve simultaneously for delta, gamma, and vega neutrality.

Theta and Time Risk

All options experience time decay (theta risk). While this is unavoidable for long option positions, some strategies deliberately harvest theta:

- Short option strategies (covered calls, cash-secured puts, short straddles) have positive theta: they earn premium over time if the asset price does not move too much.

- Long option strategies (protective puts, long straddles) have negative theta: they pay the time decay cost in exchange for convex payoff protection.

There is no instrument that directly hedges theta; managing theta risk is about position sizing and horizon management. A long option hedge that looks cheap in terms of delta can be expensive in terms of cumulative theta over several months.

Rho and Interest Rate Risk

Interest rate sensitivity (rho) is typically modest for short-dated equity options but becomes relevant for:

- Long-dated options.

- Interest-rate options (caps, floors, swaptions).

- Currency options, where interest rate differentials play a major role.

Hedging rho usually involves interest rate derivatives (futures, swaps) rather than the equity or index itself.

Calculating and Interpreting Greeks

In the BSM model for a European call option on a non-dividend-paying stock:

- Call price:

- Put price:

The Greeks for a European call are:

-

Delta (Δ):

-

Gamma (Γ):

-

Theta (Θ):

-

Vega (V):

-

Rho (ρ):

For the corresponding European put, gamma and vega are identical, while delta, theta, and rho differ in sign in predictable ways.

On the exam, you are rarely required to memorize or derive these formulas from scratch. More often you:

- Use model outputs (e.g., a table of Greeks) to compute hedge positions.

- Approximate Greeks using finite differences:

- Delta .

- Vega , etc.

Understanding the units of each Greek is critical:

- Delta: change in option price per $1 change in asset price.

- Gamma: change in delta per $1 change in asset price.

- Vega: change in option price per 1 percentage point change in volatility.

- Theta: change in option price per day (or per year).

- Rho: change in option price per 1 percentage point change in interest rate.

Interpreting signs and magnitudes correctly is a frequent source of exam traps.

Worked Example 1.1

A European call option on a stock (S = \50X = $50T = 1\sigma = 20%r = 5%) has a delta of 0.60 and a gamma of 0.025. If the stock price increases by \2, estimate the change in the option price using:

- A delta-only approximation.

- A delta-plus-gamma approximation.

Answer:

Delta-only estimate: \Delta V \approx \Delta \cdot \Delta S = 0.60 \times 2 = \1.20\Delta V \approx 0.60 \times 2 + \tfrac{1}{2} \times 0.025 \times 2^2 = 1.20 + 0.05 = $1.25$. The gamma adjustment improves the accuracy, especially for larger moves, by capturing curvature.

Worked Example 1.2

Suppose you are long 100 call options (each on 1 share) with delta 0.52 and the reference asset price is $30. How many shares must you short to delta-hedge the position?

Answer:

Total option delta =

To neutralize delta, short 52 shares of the reference asset. After hedging, a small move in the asset price should have little impact on portfolio value.

Worked Example 1.3

An option portfolio is long 200 calls (delta +0.60 each, gamma +0.04 each) and short 100 puts (delta –0.40 each, gamma +0.03 each). What is the net delta and gamma of the portfolio (ignoring the asset)?

Answer:

\text{Call delta} &= 200 \times 0.60 = +120 \\ \text{Put delta} &= 100 \times (-0.40) = -40 \\ \text{Net delta} &= +120 - 40 = +80 \\ \text{Call gamma} &= 200 \times 0.04 = +8 \\ \text{Put gamma} &= 100 \times 0.03 = +3 \\ \text{Net gamma} &= +8 + 3 = +11 \end{aligned}$$ The portfolio is long both delta and gamma: it benefits from asset price increases and also from large moves due to convexity.

Worked Example 1.4

You manage an option book currently having total delta +80 and total gamma +11 (as in Example 1.3). You have access to another European call option on the same asset (1 share per option) with delta 0.40 and gamma 0.02 per option. You want to make the portfolio gamma-neutral and then delta-neutral using only this call and the stock. How many calls and how many shares should you trade?

Answer:

Let x be the number of new calls (positive if long, negative if short). Gamma-neutrality:

So you must short 550 calls to neutralize gamma. New total delta = existing delta + delta from new calls =

To make delta zero, set

Thus, buy 140 shares of the stock. The resulting portfolio is both gamma-neutral and delta-neutral (at current prices).

Worked Example 1.5

A trader is short 1,000 ATM one-month call options on a stock. Each option has vega 0.10 and theta –0.03 (per option, per day). The trader wants to be vega-neutral using a longer-dated call option with vega 0.25 per option (theta –0.04). How many long-dated calls should she buy, and what is the net daily theta after the vega hedge (ignoring the asset)?

Answer:

Current vega =

(short vega). Let y be the number of long-dated calls. Vega-neutrality:

She should buy 400 longer-dated calls. Theta from short calls (since she is short an option with theta –0.03, short position has +0.03) =

Theta from long-dated calls =

Net theta =

After vega hedging, the portfolio is approximately vega-neutral but still positive theta, benefiting from time decay.

Exam Warning: A frequent exam error is assuming that delta hedges eliminate all risk from an option position. In reality:

- Delta neutrality protects only against small moves in the reference asset over a short horizon.

- Large moves or the passage of time will cause the hedge to drift due to gamma (delta changes as the asset price moves) and theta (value changes as time passes).

- Changes in volatility and interest rates also affect option value and are not addressed by a pure delta hedge.

Continuous monitoring and rebalancing are necessary, and in practice, transaction costs, discrete hedging intervals, and jumps in the asset price all limit hedge effectiveness. Level 2 questions often ask you to recognize why a hedging strategy that looks neutral at inception will not remain neutral over time.

Summary

Understanding the Greeks is fundamental for analyzing options and applying risk management strategies.

- Delta measures price sensitivity and is the core of delta hedging. It approximates the first-order impact of small asset price changes and can be interpreted as an equivalent stock position.

- Gamma measures the stability of delta and reflects convexity. Long gamma positions gain from large asset price moves but typically suffer from negative theta; short gamma positions have the opposite profile.

- Theta reflects time value erosion. Long options usually have negative theta, while option writers benefit from positive theta—subject to gamma and vega risks.

- Vega expresses sensitivity to implied volatility. Long options are long vega and benefit from volatility increases; short options are short vega and are harmed by volatility spikes.

- Rho measures interest rate impact. It is often secondary for short-dated equity options but can be significant for long-dated or rate-sensitive options.

Practical hedging relies most on delta and gamma, often requiring ongoing adjustment in response to market movements. Exam questions frequently require you to:

- Aggregate Greeks across positions.

- Recommend trades to achieve delta-, gamma-, or vega-neutral portfolios.

- Assess how changes in asset price, volatility, and time affect both the option value and hedge effectiveness.

- Diagnose why a proposed hedge is incomplete or unstable.

Key Point Checklist

This article has covered the following key knowledge points:

- Identify and interpret delta, gamma, theta, vega, and rho for options, including sign, magnitude, and economic intuition.

- Compute Greeks using analytical formulas, scenario shifts, or model outputs, and interpret their units.

- Construct single- and multi-period delta hedges and understand the residual gamma and theta risk.

- Design gamma- and vega-neutral portfolios using additional options and the reference asset.

- Assess the effects of volatility, time decay, and interest rates on option values and hedging strategies.

- Distinguish the risk profiles of long versus short option positions, particularly with respect to gamma, vega, and theta.

- Evaluate the limitations of dynamic hedging in the presence of transaction costs, discrete rebalancing, and large price jumps.

Key Terms and Concepts

- Greeks

- Delta

- Gamma

- Theta

- Vega

- Rho

- Delta-neutral hedge

- Gamma-neutral hedge

- Vega-neutral portfolio

- Dynamic hedging

- Delta hedging