Learning Outcomes

This article explains performance evaluation and risk management for CFA Level 2 candidates, including:

- how to interpret active portfolio returns versus benchmarks in both equity and fixed income;

- how to decompose equity performance into factor/sector and security selection effects using Brinson-style models;

- how to attribute fixed income performance to duration, yield curve positioning, sector allocation, and issuer selection;

- how to link attribution outputs to a manager’s stated investment process and risk exposures;

- how to compute and interpret active return, active risk (tracking error), and the information ratio from given data;

- how benchmark choice and portfolio construction affect measured value added and risk-adjusted results;

- how to distinguish intended factor bets from unintended exposures revealed by attribution;

- how attribution and risk metrics jointly support manager evaluation, performance review, and exam-style problem solving.

It reinforces exam technique through worked attribution examples, step-by-step decompositions of active return, and interpretation of risk-adjusted performance measures in both equity and fixed income settings.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are expected to understand the principles of portfolio performance evaluation and risk management, with an emphasis on performance attribution for both equity and fixed income, with a focus on the following syllabus points:

- Explain how to attribute investment performance to different return sources in equity and fixed income portfolios.

- Distinguish between factor effects and security selection effects.

- Calculate and interpret active return, active risk, and the information ratio.

- Use multifactor models to evaluate portfolio risk and return components.

- Apply performance attribution techniques to identify the drivers of portfolio performance.

- Explain the impact of benchmark choice and portfolio construction on risk assessment.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which metric measures the manager's ability to generate return relative to benchmark risk in active portfolio management?

- In fixed income attribution, what does the term ‘curve positioning’ refer to?

- What is the main difference between factor return and security selection return in equity attribution?

- True or false: The information ratio adjusts active return by the total risk of the portfolio.

Introduction

Accurate performance evaluation is critical for assessing a portfolio manager’s effectiveness and for managing risk. In both equity and fixed income management, performance attribution breaks down active portfolio return into its components—revealing whether results are due to market timing, sector positioning, security selection, or even unintended exposures. For CFA Level 2, you must be able to calculate, interpret, and evaluate performance attribution and risk measures for each asset class.

Key Term: performance attribution

The analysis of a portfolio’s active return by allocating it to identifiable sources such as asset allocation, sector selection, factor exposures, or security selection. Key Term: active return

The difference between a portfolio’s return and the return of its benchmark.Test Tip: When revising Performance attribution equity and fixed income, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

PERFORMANCE ATTRIBUTION IN EQUITIES

Performance attribution for equity portfolios aims to explain the sources of active return relative to a benchmark. The typical framework separates total active return into:

- Factor (style or sector) effects.

- Security selection effects.

Factor and Security Selection Effects

Factor effects refer to the added (or reduced) return from intentionally tilting the portfolio toward certain risk factors (such as value, size, momentum), or sectors, versus the benchmark. Security selection effects represent the additional return from choosing particular securities within a sector or style.

Key Term: factor effect

The performance difference attributable to having a portfolio exposure to a given risk factor or sector different from the benchmark’s exposure. Key Term: security selection effect

The performance difference attributable to choosing securities that outperform (or underperform) their sector or style group within a benchmark.

Attribution Model (Brinson Model)

The most common equity attribution model decomposes active return as follows:

Active Return = [Factor Effect] + [Security Selection Effect] + [Interaction]

Where:

- Factor Effect: Difference from benchmark due to overweighting/underweighting sectors or styles.

- Security Selection Effect: Outperformance due to picking better (or worse) stocks within each sector.

- Interaction: Combined effect when sector weights and security returns differ simultaneously.

Worked Example 1.1

A global equity manager has overweighted Technology (20% vs. 15% benchmark) and selected stocks that outperform the sector index by 2%. Tech returned 12%, benchmark Tech returned 9%, and non-Tech sectors are matched in weight and return.

Question: What are the factor (sector allocation) and security selection effects of this decision?

Answer:

- Factor Effect: (20% – 15%) × 9% = 0.45%

- Security Selection Effect: 20% × (12% – 9%) = 0.6%

- Total active return from Tech: 0.45% + 0.6% = 1.05%

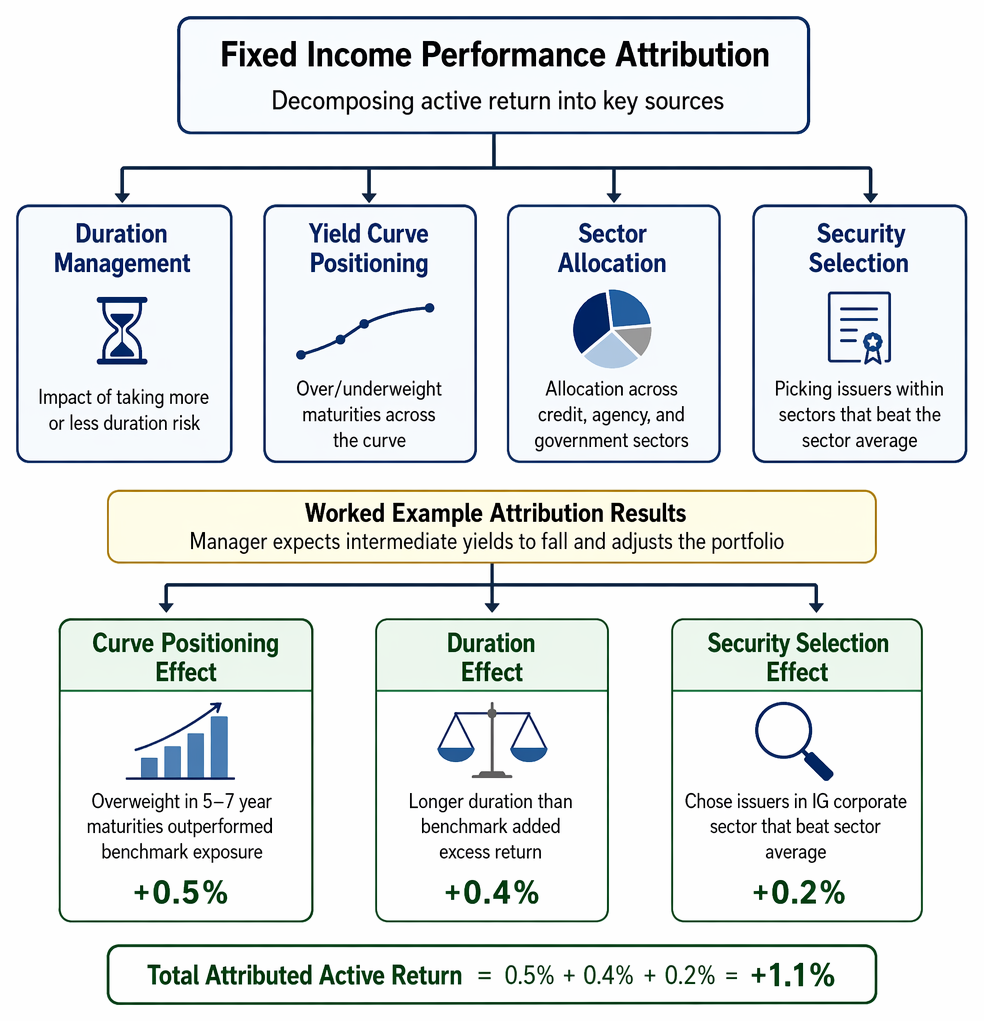

PERFORMANCE ATTRIBUTION IN FIXED INCOME

Fixed income attribution traces active return to sources such as:

Fixed-income attribution separates active return into duration risk, maturity positioning, sector exposure, and issuer selection components.

- Duration (interest rate) management.

- Yield curve positioning.

- Sector allocation (credit, agency, or government).

- Security selection within sectors.

Yield Curve, Duration, and Credit Effects

Portfolios can be over- or underweighted in duration and positioned differently on the yield curve compared to the benchmark. Additionally, sector exposure (corporate vs. government, high-yield vs. investment grade) and credit quality choices affect performance.

Key Term: yield curve positioning

The tactic of adjusting portfolio weights to maximize benefit from expected changes in rates at specific maturities.

Worked Example 1.2

A bond manager expects intermediate-term yields to fall. She overweight bonds with 5-7 years to maturity, which outperform the benchmark’s similar maturity exposure by 0.5%. The portfolio has a longer duration than the benchmark, which also contributes 0.4% in excess return.

Question: What are the attribution effects for curve positioning versus duration?

Answer:

- Curve Positioning Effect: Excess return due to overweighting the part of the curve where yields fell most: 0.5%

- Duration Effect: Excess return from taking more duration risk than the benchmark: 0.4%

Security Selection in Fixed Income

Security selection effect in fixed income refers to the additional return from choosing individual issues within a sector that outperform the sector average.

Worked Example 1.3

Within the investment grade corporate bond sector, the manager selects issuers that outperform the sector by 0.2% (after controlling for duration and curve risk).

Question: What is the security selection effect in this case?

Answer:

- Security Selection Effect: 0.2% active return attributed to superior issuer selection within the sector.

RISK MANAGEMENT METRICS

Effective risk management requires understanding both total and active risks.

Key Term: active risk

The standard deviation of active returns, also known as tracking error.

The Information Ratio

The information ratio (IR) measures risk-adjusted active return:

A higher IR indicates the manager earns more active return per unit of benchmark-relative risk.

Exam Warning: Information ratio and Sharpe ratio are not interchangeable—Sharpe compares excess total return to total risk, while IR focuses on active returns versus benchmark risk. Use the correct metric for evaluating active portfolio management.

Summary

Performance attribution allows you to break down active return into specific sources: factor (or sector/style) effects and security selection. For fixed income, further decompose active return into duration, curve, sector, and selection effects. Proper risk evaluation means focusing on both total and active (tracking) risk, using the information ratio to compare risk-adjusted performance.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain the concept and purpose of performance attribution in equity and fixed income.

- Distinguish between factor/sector and security selection effects in equity attribution.

- Attribute fixed income returns to duration, yield curve, sector, and selection effects.

- Calculate and interpret active return and active risk.

- Use the information ratio to evaluate risk-adjusted active performance.

- Recognize the importance of benchmark choice in measuring manager value-add.

Key Terms and Concepts

- performance attribution

- active return

- factor effect

- security selection effect

- yield curve positioning

- active risk