Learning Outcomes

This article covers portfolio construction and risk budgeting for multi-asset portfolios, including:

- explaining the purpose and mechanics of portfolio overlays for adjusting multi-asset exposures without trading existing holdings;

- distinguishing between strategic and tactical allocation overlays and how they interact with a core portfolio;

- describing the principles of risk budgeting and how risk contributions differ from capital allocations across asset classes and strategies;

- applying risk budgeting frameworks to set and adjust risk limits under changing market conditions and volatility regimes;

- evaluating the use of derivatives, ETFs, swaps, and forwards as instruments for implementing overlay strategies;

- analyzing how currency overlay approaches—passive, active, and hybrid—affect total portfolio risk, return, and tracking error;

- assessing when to use an overlay versus direct rebalancing to manage drift relative to strategic asset allocation targets;

- identifying best-practice monitoring, governance, and reporting processes needed to keep overlays aligned with investment policy statements and exam-relevant risk controls.

It reinforces exam-style reasoning and calculations for CFA Level 2.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are required to understand how overlays and currency management are used to construct and adjust multi-asset portfolios, with a focus on the following syllabus points:

- Explaining the concept and application of portfolio overlays for asset classes and risk exposures

- Describing the framework and objectives of risk budgeting in portfolio management

- Evaluating the rationale for implementing multi-asset allocation overlays

- Analyzing the key approaches for active and passive currency management

- Assessing the impact of currency overlay strategies on total portfolio risk and return

- Applying risk budgeting to maintain target risk profiles under changing market conditions

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

Northbridge Pension Fund is a global defined-benefit investor with a 60% equity / 40% bond strategic asset allocation. It delegates stock selection to external managers but wants to control total equity, duration, and currency risk using derivatives-based overlays at the total-fund level. The board has set a 10% annualized volatility target and a maximum 3% tracking error relative to its policy benchmark. A separate currency overlay manager is allowed to hedge between 0% and 100% of foreign currency exposure.

-

What is the primary purpose of using a portfolio overlay at the total-fund level for Northbridge?

- a) To replace all existing managers with a single derivatives strategy

- b) To adjust aggregate risk exposures efficiently without disrupting existing mandates

- c) To maximize leverage in the portfolio irrespective of risk limits

- d) To eliminate the need for an investment policy statement

-

Under a risk budgeting framework, how should the CIO react if equity volatility doubles while benchmark weights are unchanged?

- a) Keep all exposures constant because risk budgets are defined only in capital terms

- b) Reduce equity exposure or hedge it so its risk contribution moves back toward the target

- c) Increase equity exposure so the portfolio can reach its return target

- d) Ignore the change because volatility is not part of risk budgeting

-

Northbridge wants a predominantly passive approach to currency risk that stabilizes returns but allows some upside if foreign currencies appreciate. Which strategy is most consistent with this objective?

- a) A 100% discretionary currency overlay taking speculative positions

- b) A 70% systematic currency forward hedge rolled monthly

- c) Writing out-of-the-money currency call options on all foreign exposures

- d) Leaving all currency exposures fully unhedged at all times

-

When might Northbridge prefer to use an equity index futures overlay rather than physically rebalancing its equity holdings?

- a) When it wants to permanently change its strategic asset allocation

- b) When cash equities are illiquid or tax-sensitive and the allocation change is expected to be temporary

- c) When it wants to reduce counterparty risk relative to cash equities

- d) When it wants to increase tracking error relative to the benchmark

Introduction

Portfolio construction at the institutional level increasingly relies on overlays and risk budgeting to balance risk and return efficiently. Overlays are used to achieve dynamic allocation adjustments and to manage exposures such as currency, duration, or equity beta without trading the actual physical assets. Risk budgeting provides a discipline for allocating risk across asset classes or strategies in line with the investor’s targets, often expressed in terms of volatility, value at risk, or tracking error.

In many institutional settings, the core portfolio is implemented via physical securities and specialist active managers, while a separate overlay program is run centrally by the CIO or an overlay manager. This separation allows:

- consistent implementation of the fund’s strategic asset allocation,

- centralized management of aggregate risks (equity, rates, credit, currency), and

- efficient tactical adjustments across the whole fund.

Key Term: Overlay

An overlay is a separate account or strategy layered on top of an existing portfolio to efficiently modify exposure to specific asset classes, risk factors, or currencies, typically using derivatives or ETFs. Key Term: Risk Budgeting

Risk budgeting is the process of allocating allowable risk by setting quantitative risk limits for individual portfolio components based on total risk objectives, instead of focusing only on capital weights. Key Term: Currency Overlay

A currency overlay is a dedicated strategy used to adjust or hedge a portfolio’s currency exposures separately from the actual asset positions. Key Term: Strategic Asset Allocation (SAA)

Strategic asset allocation is the long-term, policy-level mix of asset classes chosen to meet the investor’s objectives and risk tolerance, usually expressed as target weights with rebalancing ranges. Key Term: Tactical Asset Allocation (TAA)

Tactical asset allocation is the deliberate, shorter-term deviation from strategic asset allocation to exploit perceived market opportunities or to respond to changing conditions.

Multi-asset overlays and currency management in the CFA Level 2 curriculum are tested at the application level: you must understand not only definitions, but how risk budgets, overlays, and hedges interact, and be able to reason through which tool is appropriate under different market and governance constraints.

Test Tip: When revising Multi-asset allocation overlays and currency management, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Portfolio Overlays in Multi-Asset Portfolios

Portfolio overlays are strategies that allow managers to adjust portfolio exposures rapidly and with minimal disruption to the existing portfolio. They are implemented using derivatives, ETFs, swaps, and forward contracts. Overlays are especially valuable in multi-asset portfolios where strategic and tactical asset allocation decisions frequently change.

Key Term: Asset Allocation Overlay

An asset allocation overlay is a derivatives-based program used to increase, decrease, or neutralize exposure to broad asset classes (e.g., equities, bonds) relative to the core portfolio. Key Term: Notional Exposure

Notional exposure is the dollar amount of reference market exposure referenced by a derivatives contract or overlay position, which may differ from the cash invested or margin posted.

Portfolio overlays enable:

- efficient rebalancing to target weights after market moves;

- fast strategic or tactical exposure shifts without liquidating core holdings;

- risk management through hedging (e.g., interest rate, equity, credit, or currency risks);

- implementation of regulatory or policy constraints (such as limiting asset class weights or regional exposures);

- centralized control of leverage and derivative usage at the total-fund level.

Strategic vs Tactical Allocation Overlays

Overlays can be aligned with either strategic or tactical objectives:

-

Strategic overlays maintain or complete the strategic asset allocation. For example, a fund that hires bottom-up equity managers might use an index futures overlay to ensure the total equity beta remains close to the policy benchmark even if managers temporarily hold large cash balances.

-

Tactical overlays express short- to medium-term views. For example, an overweight to equities implemented via index futures when the CIO is bullish, or a duration-reducing Treasury futures overlay when interest rates are expected to rise.

Key Term: Overlay Manager

An overlay manager is the specialist (internal or external) responsible for implementing, monitoring, and adjusting overlay positions to achieve specified risk or allocation objectives.

Because derivatives are used, overlays can change notional exposures by large amounts with relatively small capital outlays, which makes governance and risk control critical.

Key Term: Value at Risk (VaR)

Value at risk is a downside risk measure estimating the maximum expected loss over a specified horizon at a given confidence level, often used to define or monitor risk budgets for overlay programs.

Instruments for Overlays

Common instruments for multi-asset overlays include:

- Equity index futures and equity index swaps to adjust equity beta;

- Bond futures and interest rate swaps to alter duration and yield-curve exposure;

- Credit default swap indices to adjust credit spread exposure;

- ETFs to add or remove exposures quickly when derivatives are less liquid or not available;

- Currency forwards and swaps for currency overlays.

Key Term: Basis Risk

Basis risk is the risk that the price of the overlay instrument (e.g., an index future) does not move perfectly with the price of the reference portfolio exposure, creating residual tracking error. Key Term: Currency Forward

A currency forward is an over-the-counter contract to buy or sell a specified amount of one currency for another on a future date at a pre-agreed exchange rate. Key Term: Currency Swap

A currency swap is a derivative contract in which two parties exchange principal and interest payments in different currencies, often used to hedge long-term currency exposure. Key Term: Currency Hedged ETF

A currency hedged ETF is an exchange-traded fund that embeds a systematic currency hedge (typically via forwards) so that investors hold foreign assets while minimizing currency risk.

Because ETFs can be created and redeemed in-kind by authorized participants, they are often used in overlays to obtain or reduce exposures quickly with low transaction costs, especially when the securities are illiquid or trade in different time zones.

Sizing an Overlay Using Futures

When using futures for an asset allocation overlay, the key step is to translate a desired change in exposure into a number of contracts:

where:

- = number of futures contracts (positive for long, negative for short),

- = desired change in portfolio weight to the asset class,

- = current portfolio value,

- = futures price,

- contract multiplier = notional value per index point.

Worked Example 1.1

A pension fund’s strategic asset allocation is 60% equities and 40% bonds. After a sharp equity rally, the portfolio drifts to 68% equities. Instead of selling equities, the manager uses equity index futures to reduce equity exposure back to target.

Answer:

The manager wants to reduce equity exposure by 8 percentage points (from 68% down to 60%). Conceptually, the manager sells equity index futures with a total notional exposure equal to 8% of the portfolio value. If the portfolio is worth $400 million, the desired reduction in equity exposure is $32 million (0.08 × 400). If the relevant equity index future trades at 2,000 with a contract multiplier of 250, each contract represents $500,000 of notional exposure. The overlay size is:

Selling 64 futures contracts efficiently rebalances equity exposure while minimizing trading costs and taxes. The physical portfolio remains intact, and target risk is restored.

When to Use an Overlay vs Direct Rebalancing

Using an overlay instead of trading the existing holdings is usually preferred when:

- the allocation view is temporary (e.g., a 3–6 month tactical view);

- the assets are illiquid or have high transaction costs;

- selling physical holdings would crystallize taxable gains or breach mandate constraints;

- many managers would need to be traded to change aggregate risk.

Direct rebalancing is more appropriate for permanent changes in strategic asset allocation, or when the overlay would create unacceptable basis risk or leverage.

Key Term: Notional Exposure

Notional exposure is particularly important here, because overlays can create gross exposures that exceed portfolio market value even if net exposure remains near target. Risk controls typically limit gross notional amounts.

Risk Budgeting in Portfolio Construction

Risk budgeting is the discipline of assigning specific risk limits to portfolio components to ensure the entire portfolio remains within acceptable risk bounds. Rather than simply managing asset weights, a risk budgeting approach focuses on each investment’s contribution to total portfolio risk.

Key Term: Risk Budget

A risk budget is the amount of total portfolio risk that can be allocated to an asset class, strategy, or manager, often measured as volatility, VaR, or tracking error. Key Term: Risk Contribution

Risk contribution is the portion of total portfolio risk attributable to a specific position, calculated as the product of its weight and its marginal contribution to total risk. Key Term: Tracking Error

Tracking error (or tracking risk) is the standard deviation of active returns (portfolio minus benchmark), often used as a risk budget for active management or overlay programs.

Key applications include:

- ensuring the largest sources of portfolio risk are deliberate choices, not unintentional drifts;

- adjusting asset class, sub-asset class, or strategy exposures to meet a specific total volatility or VaR target;

- dynamically reallocating risk as market conditions change, responding to volatility spikes or structural breaks;

- efficient allocation of risk capital among internal and external managers or sleeves, often with ex-ante tracking error limits.

Risk Contributions vs Capital Weights

In a multi-asset portfolio, the percentage of capital allocated to an asset class often differs from its percentage contribution to risk because of differences in volatility and correlation.

Suppose the portfolio’s volatility is and asset has weight . Its marginal contribution to risk (MCR) is:

and its absolute risk contribution is:

The sum of all equals total portfolio volatility , and gives the percentage risk contribution. A risk budget might specify that no single asset class should contribute more than, say, 30% of total risk.

Key Term: Value at Risk (VaR)

VaR-based risk budgets specify maximum allowable loss over a given horizon and confidence level, with sub-budgets for asset classes or managers so that aggregate VaR stays within the investor’s tolerance.

Risk budgets can be applied using different measures:

- Volatility budgets: e.g., 10% annualized total volatility, with 6% allocated to equities, 2% to credit, 2% to alternatives.

- Tracking error budgets: e.g., a 3% active risk limit versus a strategic benchmark, applied at the total-fund level with sub-budgets for overlay and active managers.

- VaR budgets: e.g., 1-day 99% VaR must not exceed a specified dollar amount, with stress-test limits for crisis scenarios.

Dynamic Risk Budgeting Under Changing Volatility

Because risk budgets are defined in risk units, not capital units, allocations often need to change when asset volatilities or correlations change. For example:

- If equity volatility doubles while bond volatility is unchanged, equities will consume a much larger share of the risk budget even if weights stay the same.

- A volatility-targeting overlay may reduce equity exposure via futures when realized volatility is above target and increase it when volatility is low.

This is particularly important in regimes where correlations rise (e.g., across risky assets), causing total portfolio risk to increase faster than implied by weights alone.

Key Term: Risk Budgeting

In practice, risk budgeting is one of several risk constraints used by institutional investors, alongside position limits, scenario limits, and stop-loss limits. Overlays are often the primary tool for pushing risk contributions back within their budgets.

Worked Example 1.2

A balanced portfolio has equities, bonds, and alternatives. Capital weights are 50% equities, 30% bonds, and 20% alternatives. Because alternatives are more volatile and less correlated with bonds, they contribute 40% of total portfolio risk, while equities contribute 45% and bonds 15%. The CIO’s belief is that alternatives should not dominate risk.

Answer:

The risk analysis reveals that alternatives, despite a 20% capital weight, account for 40% of total risk—twice their capital share. The CIO sets a risk budget that caps alternatives at 25% of total risk. To bring the portfolio back in line with this budget, the CIO can:

- reduce the capital allocation to alternatives;

- introduce a hedging overlay on alternatives (e.g., via equity or volatility futures if those better represent the main risk drivers of the alternative strategies); or

- increase allocations to lower-risk diversifying assets while leaving the alternatives capital weight unchanged.

Overlay strategies are attractive here because they can quickly reduce the risk contribution without forcing a full-scale redemption from alternative managers, which may be illiquid or carry lock-up provisions.

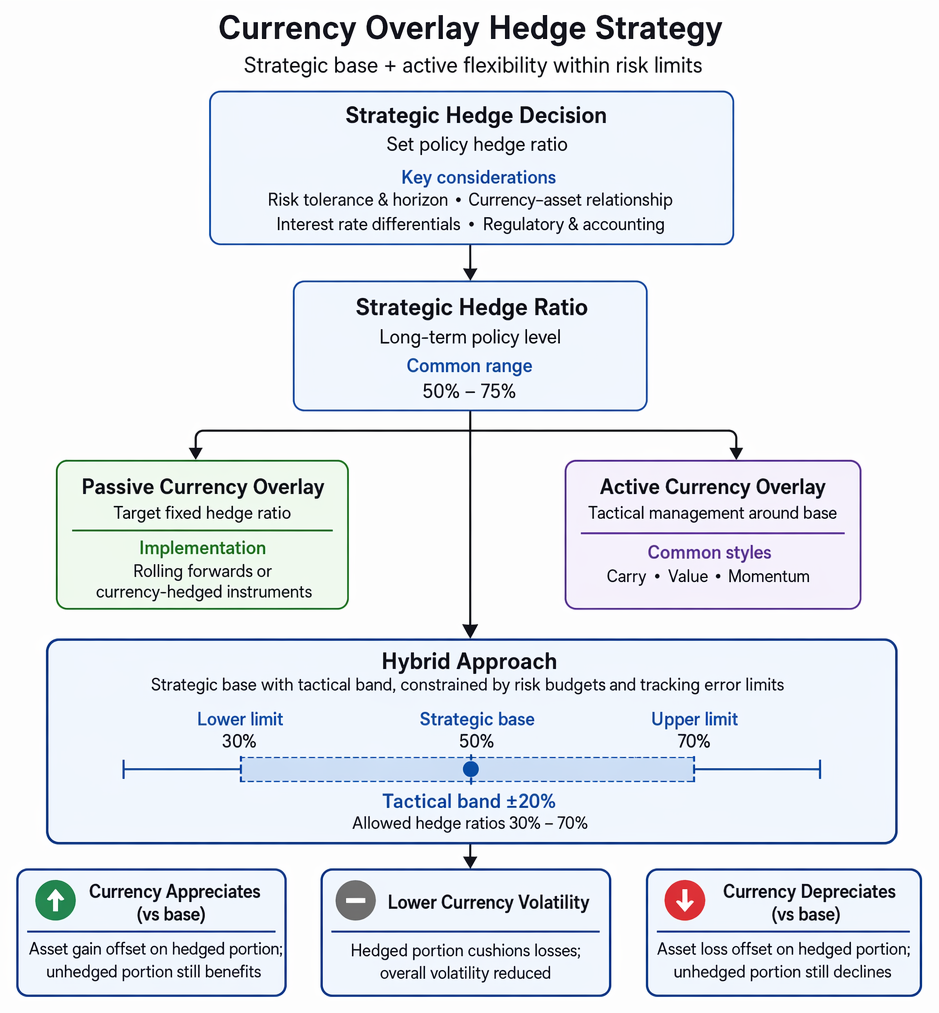

Currency Management Using Overlays

For globally diversified investors, currency exposures often become major contributors to total risk and return. Currency overlays allow managers to separate currency risk and manage it explicitly, without altering the actual asset positions. Currency management strategies include passive, active, and hybrid approaches.

Strategic and tactical overlay categories are presented with examples including completion of policy weights, equity futures, and duration reduction.

Key Term: Hedge Ratio

The hedge ratio is the proportion of a foreign currency exposure that is hedged back to the base currency using instruments such as forwards or swaps. Key Term: Passive Currency Hedge

A passive currency hedge is a systematic approach using forwards or currency-hedged instruments to reduce currency risk, typically aiming for a fixed hedge ratio such as 50% or 100%. Key Term: Active Currency Overlay

An active currency overlay is a discretionary or rule-based approach to manage currency exposures, seeking to generate alpha or control risk through tactical hedging or speculative positions that deviate from a neutral hedge ratio.

Strategic Hedge Decisions

The strategic currency hedge ratio is usually set at the policy level and reflects:

- the investor’s risk tolerance and investment horizon;

- how currency moves relative to the asset portfolio (e.g., whether foreign currencies tend to diversify or increase equity risk);

- expected interest rate differentials (which drive forward points and the cost or benefit of hedging);

- regulatory and accounting considerations.

For long-horizon investors, fully hedging may reduce volatility but also eliminate potential diversification benefits if foreign currencies behave defensively in downturns. A partial hedge (e.g., 50%–75%) is common in practice.

Key Term: Hedge Ratio

In an overlay context, changes in the hedge ratio are implemented at the total-portfolio level, even though managers may hold securities denominated in many currencies.

Passive vs Active Currency Management

Passive currency overlays aim to reduce the volatility caused by currency fluctuations by targeting a set hedge ratio (e.g., 50% or 100% hedged against the investor’s base currency). Implementation is typically via rolling forward contracts in each relevant currency.

Active overlays, in contrast, selectively hedge or unhedge exposures, or even take speculative currency positions if strong views are held. Common active styles include:

- carry (favoring higher-yielding currencies),

- value (based on purchasing power parity or real exchange rate misalignments),

- momentum (following recent currency trends).

Hybrid approaches often combine a strategic hedge ratio (e.g., 50%) with active tilts of ±20–30 percentage points around that base, constrained by risk budgets and tracking error limits.

Key Term: Hedge Ratio

For example, a strategic 50% hedge with a ±20% tactical band allows hedge ratios between 30% and 70%, providing scope for active management while keeping overall currency risk within policy limits.

Worked Example 1.3

A euro-based investor holds US equities, gaining when the dollar rises versus the euro and losing when the dollar falls. The manager implements a 70% passive currency hedge using rolling forward contracts.

Answer:

The investor has a long exposure to the US dollar (USD) through the equity holdings. A 70% hedge means that 70% of the USD exposure is offset using short-USD/long-EUR forward contracts, while 30% remains unhedged.

- If the dollar appreciates against the euro, the equity holdings gain in euro terms, but the forward hedge loses on 70% of the exposure. The portfolio still benefits from the 30% unhedged portion.

- If the dollar depreciates, the equity holdings lose in euro terms, but the forward hedge gains on 70% of the exposure, cushioning most of the currency loss.

The result is materially lower currency-driven volatility than a fully unhedged position, while preserving some potential upside from favorable currency moves.

Instruments and Risks in Currency Overlays

Overlays typically use:

- Forwards for flexible, OTC hedging tailored to specific exposures;

- Futures when standardized contracts and exchange trading are preferred;

- Options when asymmetric protection is desired (e.g., insuring against extreme moves);

- Currency swaps for long-dated or structural currency exposures (e.g., funding a foreign asset in the base currency).

Key overlay-specific risks include:

- Basis risk: the hedge may be based on an index or proxy currency that does not perfectly match the actual exposure;

- Liquidity and roll risk: forward markets can become illiquid or expensive to roll, especially in stressed conditions or for emerging market currencies;

- Counterparty and collateral risk: OTC derivatives introduce counterparty risk and require collateral management.

Exam Warning: In multi-asset portfolios, currency overlay strategies can have material impacts on portfolio risk and returns. Failing to monitor hedge ratios can cause large deviations from intended risk budgets. Always verify how derivatives, hedges, and overlays affect notional and effective exposures, and how they contribute to total portfolio volatility and tracking error.

Overlays, Dynamic Allocation, and Rebalancing

Overlays and risk budgeting are central to dynamic asset allocation. As markets move, managers need flexible tools to maintain the portfolio’s desired risk/return profile.

Key Term: Dynamic Asset Allocation

Dynamic asset allocation is the ongoing process of adjusting portfolio exposures over time in response to changing market conditions, often using overlays and rebalancing tools.

Overlays support dynamic allocation in several ways:

- Efficient exposure changes: Overlays allow managers to change exposure without liquidating positions, saving costs and minimizing market impact.

- Discipline and risk control: Overlay-driven rebalancing can rapidly bring portfolios back to target allocations after large market swings, supporting disciplined contrarian rebalancing.

- Risk-based rebalancing: Instead of rebalancing to fixed weights, overlays can adjust exposures to maintain a target volatility or VaR, consistent with a risk budget.

- Constraint management: Overlays can impose or relax risk constraints dynamically—e.g., to prevent overall portfolio volatility from exceeding a threshold during stress periods.

Key Term: Tracking Error

A key application is controlling tracking error relative to a policy benchmark. Over- or underweights to equities, duration, or currencies relative to the benchmark are primary sources of active risk. Overlays are often used to bring these back within tracking error limits without unwinding active manager positions.

Overlays vs Physical Rebalancing: Trade-Offs

Choosing between overlays and direct rebalancing involves several considerations:

- Time horizon of the view: For short-lived or uncertain views, overlays are preferred; for structural changes to the strategic allocation, physical rebalancing is more appropriate.

- Liquidity and cost: If portfolio holdings are illiquid or expensive to trade (e.g., private assets, small caps, emerging market debt), overlays using liquid futures or ETFs can substantially reduce costs.

- Taxation and accounting: Overlays may avoid realizing capital gains or disturbing book values, important for taxable investors and some institutional balance sheets.

- Basis risk and complexity: Overlays introduce derivatives-specific risks and operational complexity. Where suitable instruments do not exist or basis risk is high, physical rebalancing may be safer.

Worked Example 1.4

A $500 million portfolio currently has 70% in equities ($350 million) and 30% in bonds. The strategic equity target is 60%. The CIO expects this overweight to be temporary and decides to use an equity index futures overlay. The relevant index future trades at 2,500 and each contract has a multiplier of 50.

How many contracts should be traded and in which direction?

Answer:

The CIO wants to reduce equity exposure from 70% to 60%, a reduction of 10 percentage points of portfolio value:

Each futures contract has notional value:

The number of contracts to sell is:

The CIO sells 400 index futures contracts. This reduces effective equity exposure to the 60% target while leaving the existing stock holdings unchanged, consistent with a temporary tactical adjustment.

Monitoring, Governance, and Reporting of Overlays

Overlay strategies introduce leverage, derivatives usage, and potentially complex risk profiles. Robust governance is therefore essential.

Key elements of good practice include:

-

Clear policy documentation: The investment policy statement (IPS) and derivative risk policy should explicitly define overlay objectives, permitted instruments, leverage and notional limits, and acceptable hedge ratio ranges.

-

Quantitative risk limits:

- total volatility and VaR limits at the fund level;

- tracking error limits versus the policy benchmark;

- gross and net notional exposure limits for overlays;

- counterparty exposure limits for OTC derivatives.

-

Integrated risk budgeting: Risk budgets for the overlay program should be integrated with those of the existing managers, so that the sum of active risks from security selection and overlays remains within total-fund limits.

-

Regular monitoring and attribution:

- daily or weekly reports of overlay positions, hedge ratios, and notional exposures;

- performance attribution separating returns from the core portfolio and overlays;

- monitoring of slippage between target and realized hedge ratios, especially in fast-moving FX or rates markets.

-

Stress testing and scenario analysis: Overlay portfolios should be tested under extreme scenarios (e.g., large FX moves, rate shocks, volatility spikes) to understand potential losses and margin calls, and to ensure liquidity buffers are adequate.

-

Governance and oversight: Investment committees should receive periodic reports on overlay usage, adherence to risk budgets, and any breaches of limits. Changes in overlay mandates—such as expanding allowed instruments or increasing risk budgets—should go through formal approval processes.

These governance features link directly to the risk management readings in the curriculum, where risk budgeting, position limits, and scenario limits are presented as supplementary tools for controlling market risk.

Summary

In today’s multi-asset portfolios, overlays and risk budgeting provide essential tools for controlling exposures, implementing investment views, and limiting unwanted risks. Overlay strategies efficiently adjust allocations and hedges at the total-fund level, while risk budgeting links position sizes and risk contributions to overall objectives.

- Asset allocation overlays adjust equity, bond, and credit exposures without disturbing existing managers, using instruments such as futures, swaps, and ETFs.

- Currency overlays allow explicit management of FX risk, using passive, active, or hybrid frameworks defined by strategic hedge ratios and tactical bands.

- Risk budgeting ensures that the largest contributors to portfolio risk—whether asset classes, currencies, or overlay programs—are consistent with investor objectives, and can be dynamically adjusted as volatility and correlations change.

- Strong monitoring and governance are needed to manage leverage, basis risk, and tracking error introduced by overlays, keeping the overall portfolio aligned with the investment policy statement and exam-relevant risk controls.

Key Point Checklist

This article has covered the following key knowledge points:

- The use of overlays in multi-asset portfolios for efficient exposure management and rebalancing

- The distinction between strategic and tactical allocation overlays and their interaction with the core portfolio

- The mechanics of implementing overlays using futures, swaps, options, and ETFs, including sizing notional exposures

- Risk budgeting as a framework for controlling and allocating risk across portfolio components, using volatility, VaR, and tracking error

- How risk contributions can differ significantly from capital allocations and why that matters for portfolio construction

- Passive, active, and hybrid currency overlay techniques, and their impact on portfolio risk and return

- The concept of hedge ratios and how partial hedges can balance risk reduction with participation in favorable currency moves

- The application of dynamic asset allocation, enabled by overlays, for sustaining target risk profiles under changing volatility regimes

- Trade-offs between using overlays and direct rebalancing, considering liquidity, taxes, transaction costs, and basis risk

- Best practices for monitoring, rebalancing, and maintaining risk limits using overlays, risk budgets, and robust governance processes

Key Terms and Concepts

- Overlay

- Risk Budgeting

- Currency Overlay

- Strategic Asset Allocation (SAA)

- Tactical Asset Allocation (TAA)

- Asset Allocation Overlay

- Notional Exposure

- Overlay Manager

- Value at Risk (VaR)

- Basis Risk

- Currency Forward

- Currency Swap

- Currency Hedged ETF

- Risk Budget

- Risk Contribution

- Tracking Error

- Hedge Ratio

- Passive Currency Hedge

- Active Currency Overlay

- Dynamic Asset Allocation