Learning Outcomes

This article explains binomial interest rate tree construction and calibration for fixed income valuation in the CFA Level 2 context, including:

- Deriving the structure of a binomial interest rate tree from an initial term structure and volatility assumption.

- Interpreting the economic intuition behind up and down moves, node rates, and the evolution of short-term forward rates.

- Implementing calibration so that model-implied prices of benchmark bonds exactly match the observed spot or par curves.

- Applying backward induction step-by-step to compute present values of cash flows for fixed-rate, option-free bonds.

- Contrasting backward induction with pathwise valuation, and explaining why both approaches yield identical prices in an arbitrage-free tree.

- Assessing how interest rate volatility assumptions affect the spacing of node rates and the realism of the modeled term structure.

- Identifying common exam pitfalls, such as using market spot rates instead of calibrated node rates when valuing bonds in the tree.

- Reinforcing the link between arbitrage-free valuation theory and its practical implementation in binomial interest rate trees for exam-style questions.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are expected to understand arbitrage-free valuation and the use of binomial interest rate trees in modeling term structures and pricing bonds, with a focus on the following syllabus points:

- Understand the principles of arbitrage-free valuation for fixed income instruments.

- Describe the structure and logic of a binomial interest rate tree.

- Explain the calibration process to ensure the tree matches observed spot or par curves.

- Value fixed-rate and option-free bonds using backward induction within the tree.

- Compare pathwise valuation with backward induction.

- Identify the role of interest rate volatility assumptions in the tree construction.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What property must a binomial interest rate tree have to ensure it is arbitrage-free?

- What is the primary purpose of calibrating a binomial interest rate tree?

- Why is backward induction necessary for valuing bonds within the tree?

- In a binomial model, what is the typical relationship between adjacent forward rates within the same period?

Introduction

Binomial interest rate trees provide a practical way to value fixed income securities under the condition that markets are arbitrage-free. By using a tree structure with branching rates at each period, they allow for the modeling of various interest rate paths and enable consistent pricing of both option-free and embedded option bonds. Correct calibration is essential for the tree to reflect real-world observed rates and to produce reliable valuations for CFA Level 2 questions.

Test Tip: When revising Binomial interest rate tree construction and calibration, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Building a Binomial Interest Rate Tree

A binomial tree is a graphical representation of possible future interest rate movements, where each node branches to two possible rates for the next period ("up" or "down"). The structure is designed so that at each time step, rates can follow either of two possible paths, creating a lattice of outcomes over time.

Arbitrage-free term-structure calibration adjusts trial short rates and reprices benchmark cash flows until the model value matches the observed price.

Key Term: Binomial Interest Rate Tree

A branching model that depicts possible one-period interest rate movements—up or down—at each node across multiple periods, used to value bonds and derivatives.

At every node, the interest rate reflects a forward rate relevant for that time and scenario. The branching ensures each possible sequence of interest rate changes can be traced, providing a series of potential future spot rates.

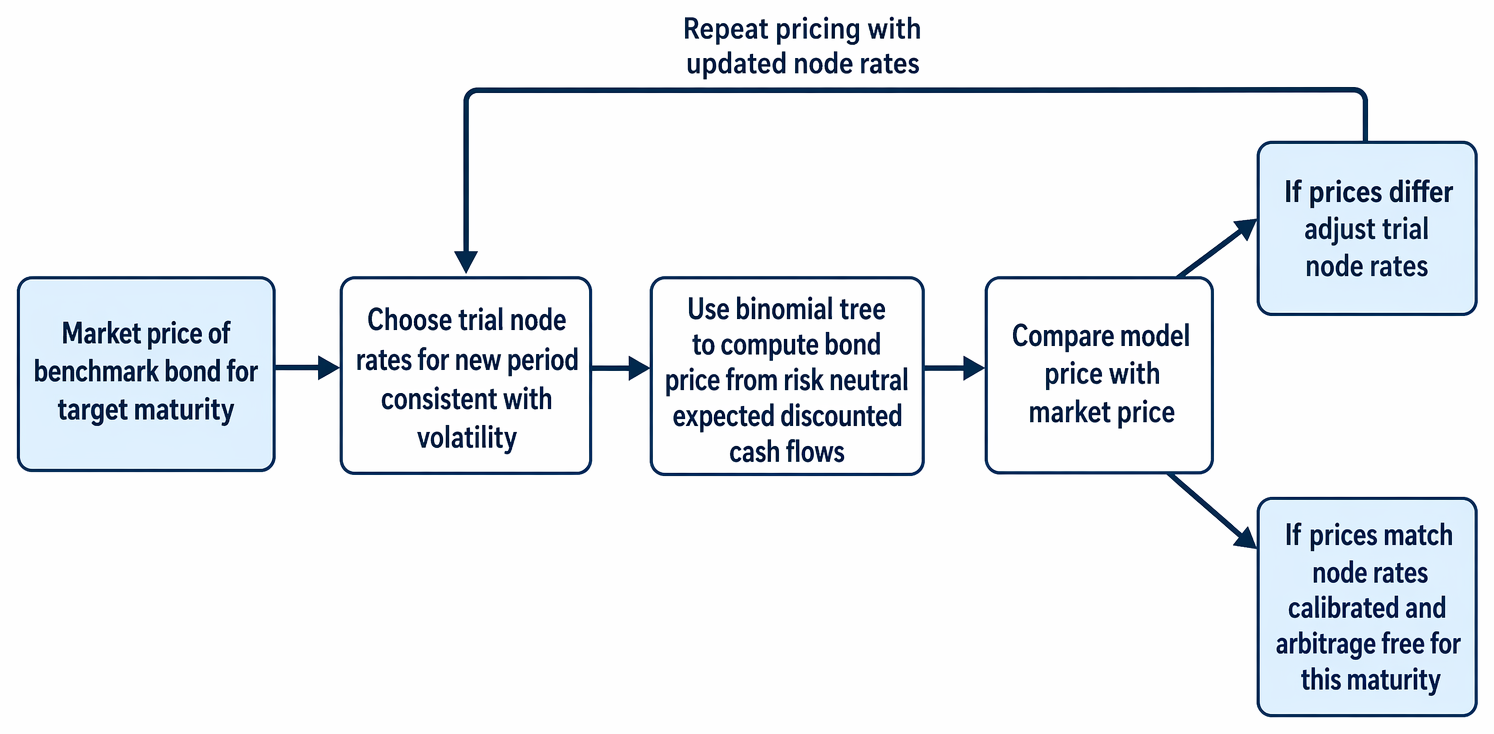

Calibration to Match the Term Structure

To be useful, the binomial tree must be calibrated so it is consistent with the observed market yield curve, usually the observed spot (zero-coupon) or par rate curve. Calibration ensures the value of bonds priced using the tree matches their current market values.

Key Term: Calibration

The process of adjusting the interest rates at each node of the tree so that present values produced by the tree align with observed prices of benchmark securities.

This process involves:

- Setting the initial node rate equal to the current short-term spot rate.

- Solving for the required rates at each subsequent node so that the expected, discounted value of cash flows equals the market price for all bonds used in calibration.

- Ensuring arbitrage opportunities are eliminated, meaning all model prices equal observed prices for the set of calibration securities.

Key Term: Arbitrage-Free Valuation

Valuing securities such that no riskless profit can be earned by exploiting price differences, ensuring model prices match observed market prices. Key Term: Backward Induction

A method of valuation where the value at each prior node is determined by averaging the appropriately discounted expected values from succeeding nodes, working from maturity back to the present.

Interest rate volatility is a key input in constructing the tree. Higher volatility implies greater spread between the potential "up" and "down" rates at each node. The volatility parameter may be specified or implied from market data (such as option prices).

Step-by-Step Tree Construction and Node Calculations

- Initialize the Tree: The first node is set to the current one-period spot rate.

- Branching: For each time step, rates in the next period are calculated as "up" and "down" moves from each current node, reflecting possible rate changes.

- Apply Volatility: The ratio between "up" and "down" moves at each node is determined by the annualized volatility assumption.

- Calibrate: Adjust the rates so that for each node and possible path, the discounted expected cash flows equate to real bond prices used for calibration.

Worked Example 1.1

Question: A three-period binomial tree must be calibrated to match observed spot rates of 3% for year 1, 4% for year 2, and 5% for year 3. Each time period is 1 year. The annual volatility is assumed to be 20%. How is the tree constructed so that it is arbitrage-free?

Answer:

- Step 1: Set the initial node, period 0, to 3%.

- Step 2: Use volatility to calculate period 1 up and down rates (one above and one below 3%, separated by the volatility factor).

- Step 3: For period 2, calculate possible rates for each path, again separated by volatility, then calibrate so that bonds priced on the tree produce present values matching prices implied by the observed 2-year and 3-year spot rates.

- Step 4: Adjust each node iteratively, using discounted expected cash flows and solving backward from maturity for node rates that ensure bond prices on the tree equal current market prices.

- This results in a unique set of future rates at each node so the tree fits the observed term structure.

Bond Valuation and Backward Induction

Once calibrated, use backward induction to value bonds:

- At maturity, the bond value at each final node equals the principal plus any final coupon.

- At each preceding node, the value equals the present value (discounted at the node rate) of the average of the values of its two forward branches (for option-free bonds).

- For bonds with embedded options, at exercise dates, check whether it is optimal to call or put, and adjust node values accordingly.

Worked Example 1.2

Using the calibrated tree from Worked Example 1.1, calculate the value today of a two-year, 4% coupon, $100 face value bond. Ignore credit risk.

Answer:

- Start by filling the tree with appropriate "up" and "down" rates for each node, as determined above.

- Calculate the bond values at maturity nodes (year 2): $104 (principal plus coupon) discounted by that node's rate.

- At each year 1 node, take the average of the future values from its two branches, discount each to present value at that node's 1-year forward rate, and add the year 1 coupon.

- At the root (today), repeat the process: average the two period-1 nodes’ discounted values, add the period 0 coupon, and discount by the initial node’s rate.

- The resulting value matches the theoretical price from spot rates.

Exam Warning: The exam often tests whether you use spot rates, forward rates, or tree-produced rates when pricing bonds. When working with a binomial tree, always use the tree’s node rates as set by calibration, not raw market spot or par rates from the original term structure. Backward induction uses only the rates in the tree.

Comparing Backward Induction and Pathwise Valuation

- Backward induction is the standard method for binomial trees, moving from the end nodes back to the start, averaging present values at each step.

- Pathwise valuation involves calculating the present value of cash flows along each possible path through the tree, and then averaging the results, accounting for probabilities.

In arbitrage-free, risk-neutral trees with properly calibrated probabilities, both methods yield the same result.

Worked Example 1.3

Question: A bond's price is calculated by backward induction as $98.90 using a binomial tree. Is it correct to expect pathwise valuation using the same tree and rates to yield $98.90? Why?

Answer:

Yes. If the tree is arbitrage-free and uses consistent risk-neutral probabilities, the average of all discounted cash flows along each path (pathwise valuation) will match the price calculated via backward induction.

Key Point Checklist

This article has covered the following key knowledge points:

- Building a binomial interest rate tree starts from observed market rates and a specified volatility.

- Calibration adjusts rates at each node so tree-based prices match observed bond prices.

- Arbitrage-free valuation ensures no riskless profit can be made; all benchmark bond prices are matched.

- Backward induction values bonds by moving from final nodes to present, averaging and discounting at each step using node rates.

- Correct rates and calibration must always be used—never raw market rates in the backward induction step.

- Both backward induction and pathwise valuation should yield identical results if the tree is fully calibrated and probabilities are consistent.

Key Terms and Concepts

- Binomial Interest Rate Tree

- Calibration

- Arbitrage-Free Valuation

- Backward Induction