Learning Outcomes

This article explains the term structure of interest rates and the use of interest rate trees for CFA Level 2 fixed-income valuation, including:

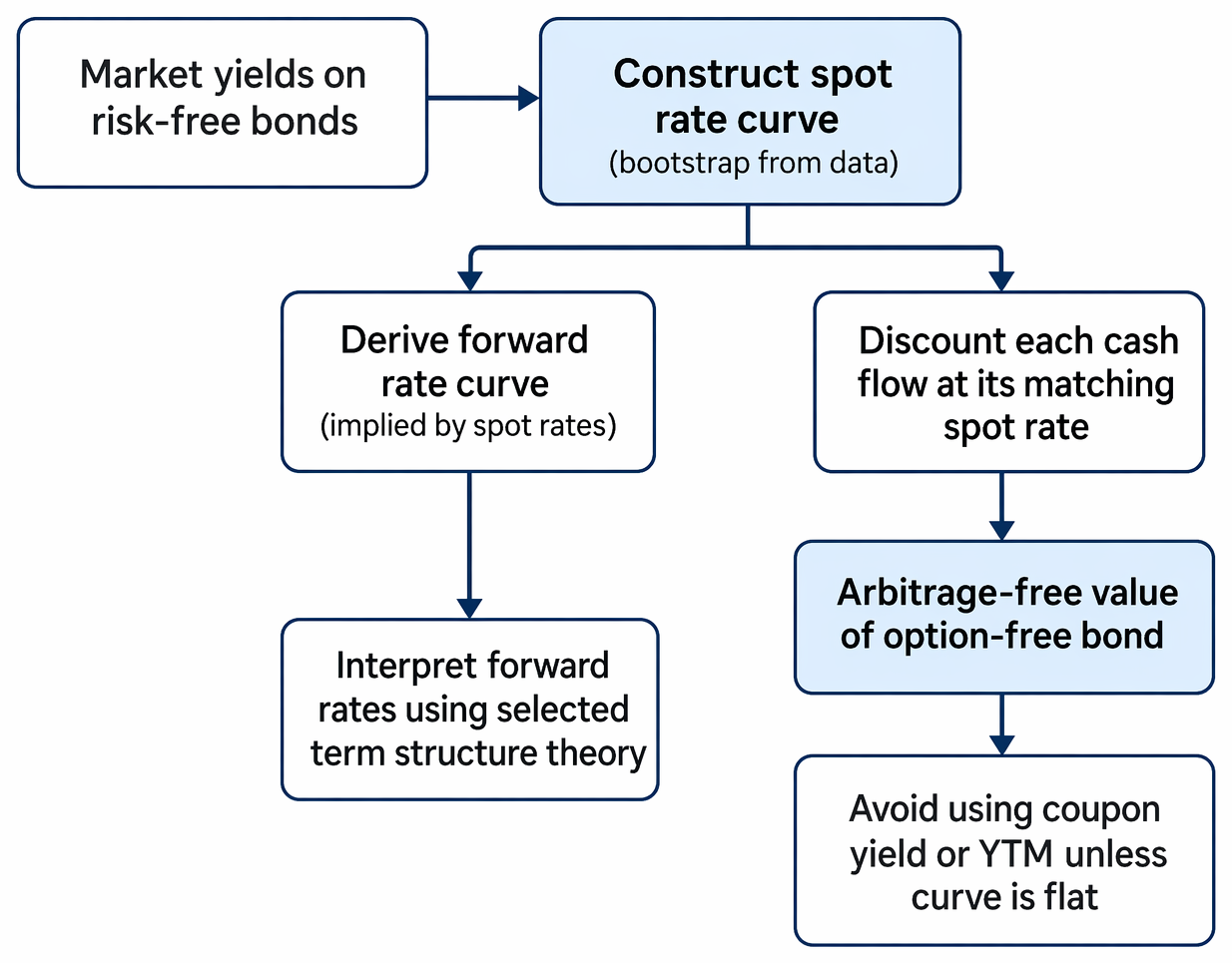

- Defining the term structure of interest rates, the yield curve, spot rates, and forward rates, and linking these concepts to risk-free discounting of bond cash flows.

- Explaining pure expectations, liquidity preference, segmented markets, and preferred habitat theories, and comparing how each theory interprets the shape of the yield curve and embedded information about future interest rates.

- Describing how expectations about future short-term rates translate into spot and forward rate relationships, and how liquidity premia modify the information content of forward curves.

- Distinguishing equilibrium from arbitrage-free term structure models, emphasizing their assumptions, calibration approaches, typical model examples, and the exam-relevant advantages and limitations of each class.

- Outlining the construction of binomial interest rate trees, including node structure, up and down movements, calibration to the current yield or spot curve, and treatment of interest rate volatility.

- Demonstrating how trees are used to value option-free and option-embedded bonds, stress-test interest rate paths, and avoid common CFA exam errors such as misusing yields or inconsistent tree calibration.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are expected to understand the construction and applications of term structure models and their importance in active bond portfolio management, with a focus on the following syllabus points:

- Explain traditional theories of the term structure of interest rates and describe their implications for forward rates and the shape of the yield curve.

- Describe how equilibrium and arbitrage-free term structure models are used and compare their features.

- Describe the assumptions and calibration of binomial interest rate trees.

- Explain how expectations about spot and forward rates relate to yield curve modeling.

- Demonstrate pricing of fixed-income instruments using interest rate trees.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the liquidity premium theory’s prediction about the typical shape of the yield curve?

- When is it necessary to use an arbitrage-free interest rate tree instead of spot rate discounting for bond valuation?

- Briefly explain the main difference between equilibrium and arbitrage-free term structure models.

- How do forward rates relate to future spot rates under the unbiased expectations theory?

Introduction

The term structure of interest rates describes the relationship between interest rates and maturities for risk-free debt securities. Understanding the main term structure models and interest rate trees is essential for bond valuation, risk analysis, and constructing interest rate derivatives. CFA Level 2 candidates must be able to distinguish between different yield curve theories, apply their implications to portfolio management, and perform calculations using interest rate trees.

Key Term: term structure of interest rates

The relationship between yields and maturities for default-free debt within a given currency. Often visualized as the yield curve.Test Tip: When revising Term structure models and expectations, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Theories of the Term Structure

Yield curve models attempt to explain why the curve assumes various shapes over time and what it implies about future rates.

Observed default-free yields generate spot and forward curves used for arbitrage-free bond valuation rather than yield-to-maturity on a nonflat curve.

Key Term: yield curve

A graphical representation showing yields for bonds of identical credit quality but different maturities.

Pure Expectations Theory

The pure expectations (unbiased expectations) theory states that long-term rates are determined solely by market expectations for future short-term rates. Forward rates implied by the curve are unbiased predictors of future spot rates.

Liquidity Preference Theory

This model adds a liquidity premium to the pure expectations theory, compensating investors for interest rate risk associated with longer maturities. As a result, yield curves tend to slope upward.

Segmented Markets and Preferred Habitat Theories

Both posit that supply and demand imbalances within particular maturity segments or “habitats” drive the yield curve’s shape.

Implications for Forward and Spot Rates

Under the pure expectations theory, forward rates equal the expected future spot rates. The liquidity preference theory implies forward rates will overestimate future spot rates if there is a positive liquidity premium.

Key Term: forward rate

The agreed interest rate today for a loan to be made at a specific future start date for a stated period. Key Term: spot rate

The current yield for a zero-coupon, risk-free bond maturing at a particular future date.

Interest Rate Trees and Model Types

Accurately pricing fixed-income securities and derivatives requires modeling potential future interest rates. Interest rate trees provide a framework to do this.

Equilibrium vs. Arbitrage-Free Models

- Equilibrium models (such as Vasicek and Cox-Ingersoll-Ross) derive the evolution of rates from assumptions about economic factors and investor preferences.

- Arbitrage-free models (such as the Ho-Lee model) calibrate directly to observed market prices and the current yield curve, ensuring that securities are priced consistently with market data.

Key Term: arbitrage-free model

A pricing model for interest rates that ensures all fixed-income securities are consistent with current market prices, admitting no risk-free arbitrage opportunities. Key Term: equilibrium model

A term structure model that specifies the evolution of interest rates based on an economic rationale and assumed processes for investors’ behavior and economic variables.

Constructing and Calibrating Interest Rate Trees

Interest rate trees (most commonly binomial trees) simulate the evolution of interest rates at discrete time intervals, enabling bond pricing and risk assessment.

- Each “node” in a tree represents a possible short-term rate at a future point in time.

- Trees are calibrated so that they are consistent with the current observed yield (or spot rate) curve.

- At each node, two possible rate outcomes are assumed for the next period: an “up” move and a “down” move.

Key Term: binomial interest rate tree

A model that represents multiple possible future paths for short-term interest rates, where each period features two possible moves for the rate.

Model Assumptions and Use of Trees

- Interest rate trees may assume either constant or state-dependent volatility.

- For option-free bonds, discounting expected cash flows at the risk-free spot rates is usually sufficient. For bonds with embedded options or path-dependent cash flows, lattice (tree) approaches are essential.

- Arbitrage-free trees ensure valuations match observed market prices for benchmark bonds.

Worked Example 1.1

A 2-year option-free bond has a 5% annual coupon and $1,000 par value. The one-year spot rate is 4% and the two-year spot rate is 5%. Calculate the arbitrage-free price of the bond.

Answer:

- Discount Year 1 cash flow: \frac{\50}{1.04} = $48.08$

- Discount Year 2 cash flow: \frac{\1,050}{(1.05)^2} = $952.38$

- Total price = $48.08 + $952.38 = $1,000.46

Worked Example 1.2

Suppose you wish to value a 2-year, 6% coupon bond (par = $100) using a binomial tree. The current 1-year rate is 4%, the “up” and “down” rates for Year 2 are 6% and 3%. Both states are equally probable. How do you calculate its price?

Answer:

- At each Year 2 node, compute value: $106 at 6%, $106 at 3%

- Discount back to present using 1-year rates:

- Add Year 1 coupon, then discount by current 1-year rate:

Exam Warning: A frequent CFA exam mistake is using coupon bond yields or forward rates as discount rates for bonds, rather than zero-coupon (spot) rates. Always discount each separate cash flow at its corresponding spot rate, not the bond’s YTM, unless the curve is flat.

Summary

Term structure models are central to understanding how interest rates change with maturity and time. Key yield curve theories include the pure expectations, liquidity preference, and segmented markets models. Interest rate trees—especially the binomial tree—are calibrated to match the current yield curve and allow for valuation of bonds, especially those with embedded options. It is critical to distinguish between equilibrium and arbitrage-free models for the exam.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain traditional term structure theories and their implications for the yield curve.

- Describe equilibrium and arbitrage-free models and their main differences.

- Construct and calibrate an interest rate tree given the current yield curve.

- Apply the binomial tree to price fixed-income securities.

- Recognize when each modeling approach is required for exam scenarios.

Key Terms and Concepts

- term structure of interest rates

- yield curve

- forward rate

- spot rate

- arbitrage-free model

- equilibrium model

- binomial interest rate tree