Learning Outcomes

This article explains Brinson-Fachler performance attribution for multi-sector portfolios, including:

- Distinguishing clearly between allocation, selection, and interaction effects and relating each effect to active return versus a benchmark.

- Applying the Brinson-Fachler formulas to calculate sector-level and total portfolio allocation, selection, and interaction contributions using weights and returns.

- Interpreting the sign and magnitude of each effect to diagnose the sources of outperformance or underperformance in equity and multi-sector portfolios.

- Reconciling the sum of sector attribution effects with total active return and checking calculations for internal consistency.

- Identifying typical CFA Level 3 exam question formats, such as “explain,” “calculate,” and “interpret,” and mapping each to the appropriate attribution steps.

- Spotting and avoiding common exam errors, including using benchmark instead of portfolio weights for selection, misclassifying interaction, and miscomputing benchmark return.

- Linking numerical attribution results to concise written conclusions that would score well on constructed-response questions.

- Comparing the Brinson-Fachler approach with alternative attribution schemes at a high level so you can recognize which framework is being tested in the exam.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand and apply attribution methods, especially those for equity and multi-sector portfolios based on the Brinson-Fachler framework, with a focus on the following syllabus points:

- Understanding the purpose and context of portfolio performance attribution.

- Explaining the components of Brinson-Fachler attribution (allocation, selection, interaction).

- Calculating each effect for segmented portfolios and reconciling to total active return.

- Interpreting the financial significance and exam relevance of each effect.

- Identifying practical uses and exam pitfalls in attribution analysis and manager evaluation.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

In the Brinson-Fachler attribution framework, which effect isolates the impact of choosing different sector weights than the benchmark, evaluated at benchmark sector returns?

- a) Selection effect

- b) Allocation effect

- c) Interaction effect

- d) Total active return

-

A manager overweights the energy sector relative to the benchmark, and the energy sector underperforms the overall benchmark during the period. What is the most likely sign of the allocation effect for energy?

- a) Positive allocation effect

- b) Zero allocation effect

- c) Negative allocation effect

- d) Cannot be determined without portfolio returns

-

For a given sector, the portfolio weight is 20%, the benchmark weight is 15%, the portfolio sector return is 12%, and the benchmark sector return is 8%. What is the Brinson-Fachler selection effect for this sector?

- a) 0.8%

- b) 0.6%

- c) 0.4%

- d) 0.3%

-

Which statement best explains why the interaction effect is sometimes grouped with allocation or selection in practice?

- a) It is always exactly zero for well-diversified portfolios.

- b) It represents pure timing skill separate from allocation and selection.

- c) It is typically small, adds complexity, and does not change high-level conclusions.

- d) It only applies to fixed-income portfolios, not equity portfolios.

Introduction

Performance attribution is the discipline of explaining why a portfolio outperformed or underperformed its benchmark. At Level 3, attribution is not just arithmetic; you are expected to turn numbers into concise, defensible statements about manager skill and investment decisions.

Key Term: performance attribution

Performance attribution is the process of decomposing portfolio returns relative to a benchmark into distinct sources, such as allocation and selection effects, to explain active return. Key Term: active return

Active return is the difference between the portfolio return and the benchmark return over the same period:

A common exam setting is an equity or multi-asset portfolio segmented into sectors or asset classes, with an index as the policy benchmark. The Brinson-Fachler method is the standard arithmetic framework for decomposing active return into allocation, selection, and interaction components.

Key Term: Brinson-Fachler method

The Brinson-Fachler method is a holdings-based attribution framework that decomposes active return into allocation, selection, and interaction effects across predefined segments (e.g., sectors), using portfolio and benchmark weights and returns. Key Term: benchmark

The benchmark is a specified portfolio or index representing the neutral or policy asset mix against which portfolio performance is evaluated. Key Term: sector

In performance attribution, a sector is any defined segment of the investment universe (e.g., industry group, region, asset class) used to group securities for weight and return comparisons.

Brinson-Fachler is tested because:

- It links directly to manager decisions: sector tilts (top-down) and security selection (bottom-up).

- It produces additive sector-level contributions that reconcile exactly to total active return (subject to rounding).

- It gives a clear structure for written evaluation of a manager’s strengths and weaknesses.

Test Tip: When revising Brinson-fachler allocation selection and interaction, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Exam Warning: Do not rely on keyword recognition alone; check the precise condition, exception, calculation step, or evidence the question requires.

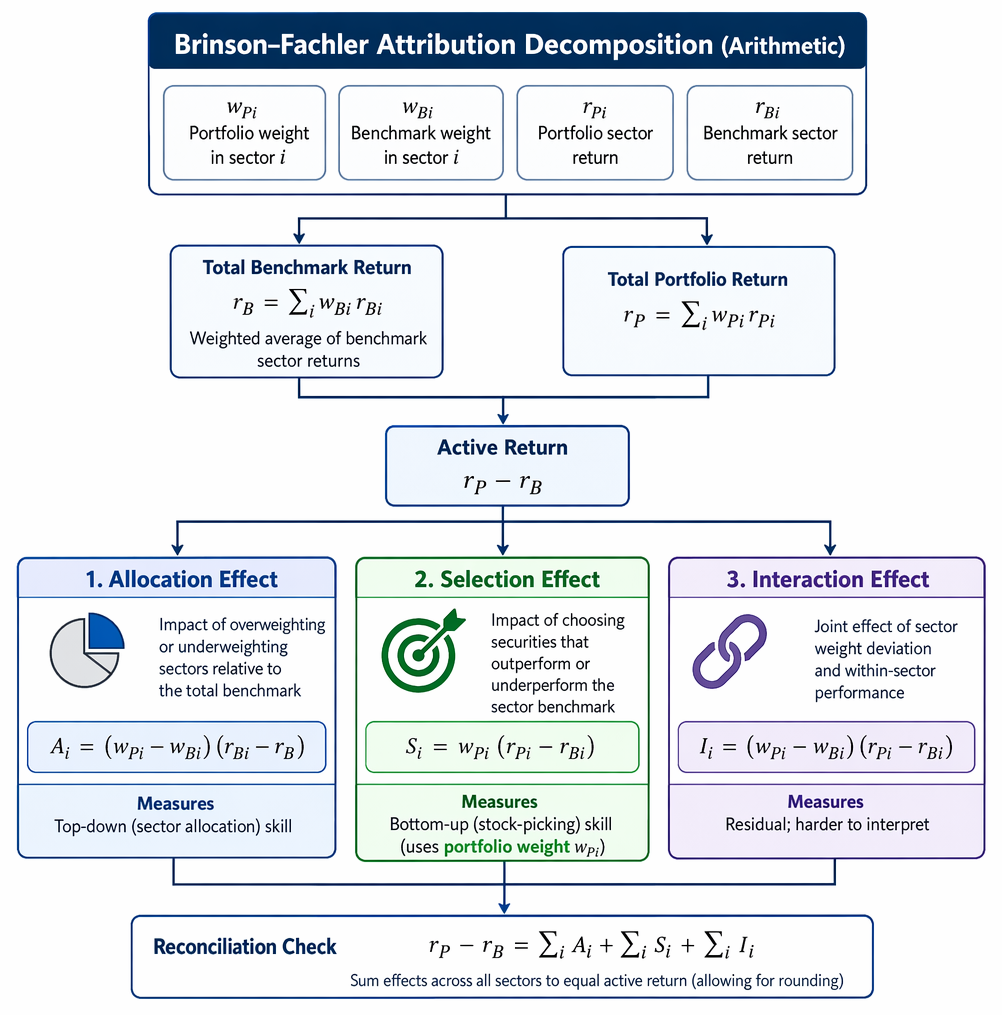

The Brinson-Fachler Attribution Framework

Central to attribution is comparing what the manager actually did (portfolio weights and returns) with what would have happened by simply holding the benchmark. The portfolio and benchmark are both decomposed into the same set of sectors.

Brinson-Fachler equations map sector weights and returns to allocation, selection, and interaction components that reconcile to active return.

The Three Effects

Brinson-Fachler splits active return into three effects for each sector :

- Allocation effect

- Selection effect

- Interaction effect

Key Term: allocation effect

The allocation effect is the portion of active return attributed to the portfolio’s sector weights being different from those of the benchmark, evaluated at benchmark sector returns. Key Term: selection effect

The selection effect is the part of active return assigned to the difference between the portfolio’s sector return and the benchmark sector return, weighted by the portfolio’s sector weight. Key Term: interaction effect

The interaction effect is the value added (or lost) when the portfolio both deviates in sector weight and in performance versus the benchmark within that sector.

Conceptually:

- Allocation asks: “If I had held benchmark-like securities in each sector but used my actual sector weights, how much value would I have added or lost?”

- Selection asks: “Given my actual sector weights, how much value came from choosing securities that outperformed or underperformed the sector benchmark?”

- Interaction captures the joint effect of “right sector” and “right security” (or “wrong sector” and “wrong security”) decisions occurring together.

In manager evaluation:

- Allocation is associated with top-down skill.

- Selection is associated with bottom-up stock-picking skill.

- Interaction is usually treated as a residual; its interpretation is less straightforward.

Key Term: top-down attribution

Top-down attribution is an approach that first attributes active return to broad decisions such as asset allocation or sector tilts, before drilling down to security selection within each segment.

Mathematical Formulation

Let for sector :

- = portfolio weight in sector

- = benchmark weight in sector

- = portfolio sector return

- = benchmark sector return

- = total benchmark return

Key Term: total benchmark return

Total benchmark return is the weighted average of benchmark sector returns using benchmark sector weights.

Formally:

Total active return is:

and Brinson-Fachler decomposes this as:

where, for each sector :

- Allocation effect:

- Selection effect:

- Interaction effect:

These formulas reflect the Brinson-Fachler arithmetic attribution.

Key Term: arithmetic attribution

Arithmetic attribution is an attribution approach in which sector-level effects add up linearly to the total active return over the period.

For exam purposes, you typically:

- Compute sector-level , , and .

- Sum across sectors to obtain total allocation, selection, and interaction.

- Check that the sum equals (within rounding).

Exam tip: In the Brinson-Fachler version, the allocation term uses:

This centers sector performance relative to the overall benchmark, which improves interpretability of sector tilts.

Brinson-Fachler versus Other Attribution Schemes (High Level)

You may see references to alternative schemes such as Brinson-Hood-Beebower (BHB). At Level 3, you are not required to memorize alternative formulas, but you should recognize key differences conceptually:

- Brinson-Fachler measures allocation against how each sector did relative to the total benchmark .

- BHB measures allocation against the sector’s own level .

Practically, both frameworks decompose active return into allocation and selection-like components. In the exam, you will be told which method to use, or the formulas will be given. Your task is to apply that specific framework consistently.

Step-by-Step Calculation Process

A robust attribution answer follows a clear sequence:

- Step 1: Compute each sector’s portfolio and benchmark returns if not already provided.

- Step 2: Confirm portfolio and benchmark weights for each sector; ensure they sum to 100%.

- Step 3: Compute the total benchmark return .

- Step 4: Compute total portfolio return and the active return .

- Step 5: For each sector, compute allocation, selection, and interaction using the Brinson-Fachler formulas.

- Step 6: Sum each effect across sectors and verify that the totals reconcile to (allowing for small rounding differences).

- Step 7: Interpret the sign and magnitude of each effect, linking back to manager decisions.

Exam warning: For the selection effect, always use portfolio weights:

not benchmark weights. Using benchmark weights is a common error that leads to incorrect contributions and may cost marks.

Worked Example 1.1

A portfolio is invested in two sectors.

-

Sector X:

- Portfolio weight: 60%

- Portfolio return: 6%

- Benchmark weight: 50%

- Benchmark sector return: 4%

-

Sector Y:

- Portfolio weight: 40%

- Portfolio return: 10%

- Benchmark weight: 50%

- Benchmark sector return: 8%

Compute:

- The benchmark total return .

- Allocation, selection, and interaction effects for each sector.

- Total allocation, selection, interaction, and active return.

Answer:

First compute the total benchmark return:

Portfolio total return:

Active return:

Sector X Allocation:

Selection:

Interaction:

Sector Y Allocation:

Selection:

Interaction:

Totals across sectors Total allocation:

Total selection:

Total interaction:

Sum of effects:

which matches the active return of 1.6%. The manager added value primarily through selection; sector allocation detracted.

This example is typical of exam questions where you must both calculate and interpret which decision (allocation or selection) drove value added.

Interpreting Signs and Typical Patterns

Understanding the direction of each effect is essential for quick interpretation and for written justifications in constructed-response questions.

Common patterns for a given sector:

-

Overweight a sector that outperforms the total benchmark:

- Allocation effect tends to be positive.

-

Overweight a sector that underperforms the total benchmark:

- Allocation effect tends to be negative.

-

Underweight a sector that outperforms the total benchmark:

- Allocation effect tends to be negative.

-

Underweight a sector that underperforms the total benchmark:

- Allocation effect tends to be positive.

For selection and interaction:

-

If the portfolio sector return exceeds the benchmark sector return :

- Selection is positive if the portfolio has any weight in that sector.

- Interaction has the same sign as : overweighting a winning sector with good selection yields positive interaction; underweighting it yields negative interaction.

-

If the portfolio sector return lags :

- Selection is negative.

- Interaction is negative when overweighting a losing sector and positive when underweighting it.

In written exam answers, link sign and magnitude directly to decisions. For example:

- “The manager’s overweight to healthcare reduced active return (negative allocation) because healthcare underperformed the overall benchmark, indicating poor sector allocation decisions.”

Worked Example 1.2

An equity portfolio overweights the healthcare sector compared to the benchmark. During the period, healthcare underperforms the overall benchmark. What is the expected sign of the Brinson-Fachler allocation effect for healthcare?

Answer:

The allocation effect will be negative. The portfolio overweighted a sector whose benchmark return was below the total benchmark return, so

is positive and

is negative, making their product negative.

Note that this statement holds regardless of the portfolio’s within-sector selection result; selection and interaction are separate components.

Worked Example 1.3 – Synthesis and Interpretation

You are given the following sector-level Brinson-Fachler attribution (all numbers in percentage points of active return):

-

Financials:

- Allocation: +0.40

- Selection: −0.10

- Interaction: +0.05

-

Technology:

- Allocation: −0.30

- Selection: +0.80

- Interaction: +0.10

-

All other sectors combined:

- Allocation: −0.10

- Selection: −0.05

- Interaction: 0.00

Total active return is therefore:

- Allocation:

- Selection:

- Interaction:

- Total active return:

Provide a concise evaluation of the manager’s performance.

Answer:

The portfolio outperformed the benchmark by 0.80%, driven entirely by stock selection and interaction; allocation decisions were neutral overall. Sector tilts offset each other—good allocation to financials was canceled by poor allocation to technology and other sectors. The main strength was strong stock selection in technology (0.80% selection plus 0.10% positive interaction), partially offset by modestly negative selection in financials and other sectors. Overall, the manager appears to add value primarily through bottom-up security selection rather than top-down sector allocation.

This is the type of synthesis the exam expects: convert a table of numbers into a clear, prioritized assessment of manager skill.

Geometric Versus Arithmetic Attribution (High Level)

Key Term: geometric attribution

Geometric attribution is a performance attribution approach that compounds returns multiplicatively over time, allocating the relative performance over multiple periods in a way that links exactly to the geometric excess return.

Most Level 3 questions use single-period arithmetic Brinson-Fachler attribution. In practice, multi-period attribution requires linking single-period effects (e.g., using geometric linking methods). You are not required to perform geometric attribution calculations, but you should be aware that:

- Arithmetic Brinson-Fachler works cleanly for one period.

- For several periods, managers apply a linking algorithm to produce period-by-period and cumulative effects.

If a question does not mention geometric methods or multi-period linking, you should assume a single-period arithmetic Brinson-Fachler context.

Practical and Exam Pitfalls

Common issues to watch for:

-

Using the wrong weights in selection

- Selection must use portfolio weights . Using understates or overstates selection and may prevent reconciliation to total active return.

-

Miscomputing the benchmark total return

- Always compute as the sum of benchmark weights times benchmark sector returns. Do not use portfolio weights for .

-

Ignoring cash or residual sectors

- Cash and residual sectors (e.g., “other”) should be treated as additional sectors with their own weights and returns.

-

Forgetting the overall check

- After calculating all effects, verify:

- Minor differences due to rounding are acceptable; material differences indicate an error.

-

Over-interpreting interaction

- Interaction often is small and noisy. Many practitioners combine it with allocation or selection when making qualitative comments (the exam may do so explicitly). Unless asked specifically, focus interpretations on allocation and selection.

Summary

The Brinson-Fachler attribution method decomposes a portfolio’s active return into three components:

- Allocation: Value from deviating sector weights from the benchmark, evaluated at benchmark sector performance relative to the total benchmark.

- Selection: Value from choosing securities within sectors that outperform or underperform the sector benchmark, based on portfolio weights.

- Interaction: The joint effect when weight deviations and within-sector performance differences occur together.

For CFA Level 3, it is important to:

- Apply the formulas correctly at the sector level.

- Reconcile sector effects to total active return.

- Translate numeric attribution into clear, prioritized statements about a manager’s top-down and bottom-up skill.

- Avoid common calculation errors, especially around weights and benchmark returns.

Key Point Checklist

This article has covered the following key knowledge points:

- Define and explain the allocation, selection, and interaction effects using the Brinson-Fachler method.

- Compute benchmark and portfolio total returns and derive active return.

- Perform step-by-step calculations of allocation, selection, and interaction effects for multi-sector portfolios.

- Reconcile the sum of sector attribution effects with total active return and identify errors when they do not match.

- Recognize the impact of sector weights and returns in each attribution component and link them to top-down versus bottom-up skill.

- Avoid exam mistakes by using portfolio weights for selection and interpreting interaction appropriately.

- Interpret the real-world meaning of attribution results to evaluate manager performance in constructed-response and item-set questions.

- Distinguish, at a high level, the Brinson-Fachler arithmetic framework from alternative attribution schemes and geometric attribution.

Key Terms and Concepts

- performance attribution

- active return

- Brinson-Fachler method

- benchmark

- sector

- allocation effect

- selection effect

- interaction effect

- top-down attribution

- total benchmark return

- arithmetic attribution

- geometric attribution