Learning Outcomes

This article explains fixed-income performance attribution in a CFA Level 3 context, including:

- Clarifying the role of attribution in performance evaluation and distinguishing it from risk reporting.

- Describing how to decompose active fixed-income returns into yield curve, credit, and selection effects relative to a benchmark.

- Explaining the intuition behind key rate duration, curve positioning, credit spread changes, and sector or security selection within risk buckets.

- Comparing single-factor and multi-factor attribution approaches and recognizing when each is appropriate for a given portfolio strategy.

- Showing how to map portfolio and benchmark holdings to attribution factors and calculate effect contributions that reconcile to total active return.

- Interpreting attribution results to assess manager skill, style consistency, and the sources of outperformance or underperformance.

- Identifying common exam traps, such as double counting effects, misclassifying credit versus selection contributions, or ignoring benchmark structure.

- Practicing the application of attribution concepts to short numerical examples and vignette-style questions that mirror the CFA Level 3 exam format.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand fixed-income attribution methods and apply them for portfolio evaluation, with a focus on the following syllabus points:

- Identifying and explaining components of fixed-income attribution, including yield curve, credit, and selection effects

- Applying multi-factor models to decompose portfolio returns relative to a benchmark

- Assessing the effectiveness of fixed-income managers through attribution analysis

- Recognizing appropriate attribution techniques for different fixed-income strategies

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the purpose of fixed-income attribution, and why are yield curve and credit effects separated in the analysis?

- Identify the three main effects attributed to fixed-income performance in a multi-factor model.

- How does a manager's sector rotation between government, credit, and high-yield affect credit attribution?

- What might cause a selection effect to appear in fixed-income attribution, and how should it be interpreted?

Introduction

Performance attribution is a critical skill for fixed-income portfolio managers and analysts. It allows you to break down active returns into sources: changes in interest rates (yield curve), changes in credit spreads, and manager security or sector selection. Understanding attribution methods strengthens your ability to evaluate portfolio performance, review risk exposures, and explain relative results to clients and stakeholders.

Key Term: fixed-income attribution

The process of decomposing the active return of a fixed-income portfolio relative to a benchmark into distinct effects such as yield curve, credit, and selection.

FIXED-INCOME ATTRIBUTION: OVERVIEW

Fixed-income attribution frameworks serve two main goals: explaining how a portfolio performed relative to a benchmark and determining what caused the outperformance or underperformance. Unlike equities, fixed-income portfolios are especially sensitive to changes in interest rates and credit spreads. Attribution methods must distinguish these risk factors and isolate true active decisions from broad market movements.

Key Term: yield curve effect

The portion of active return attributable to mismatches in portfolio and benchmark duration and exposure to different points on the interest rate curve. Key Term: credit effect

The portion of active return explained by differences in exposure to credit sectors or changes in credit spreads between the portfolio and the benchmark. Key Term: selection effect

The return caused by superior/inferior security selection within a given risk bucket, after adjusting for yield curve and credit exposures.

Single-Factor and Multi-Factor Attribution

Early fixed-income attribution models were based on single factors, usually duration or parallel shifts in interest rates. Modern approaches use multi-factor frameworks to capture more nuances:

- Yield curve (interest rate) changes: Parallel or non-parallel shifts

- Credit spread changes: Sector or rating-specific spreads

- Selection: Security-specific or issuer-specific choices

The chosen model must reflect both the portfolio's investment process and risk exposures.

YIELD CURVE EFFECTS

The yield curve effect measures active return related to duration positioning, curve positioning (barbell vs. bullet), and any deviations in sensitivity to movements at specific maturities. If a portfolio is long duration when rates fall, the yield curve effect is likely positive.

Worked Example 1.1

A portfolio is overweight 10-year government bonds, while its benchmark is balanced across the curve. Over the period, the 10-year rate falls by 40 bps, while short and long rates are stable. What is the yield curve effect on relative return?

Answer:

The portfolio's overweight to the falling 10-year segment produced a positive yield curve effect, as it benefited more from the rate movement than the benchmark.

CREDIT EFFECTS

Credit effects analyse differences in return due to allocation across ratings or sectors, reflecting the manager's tilt toward (or away from) credit risk. For example, an overweight position in investment-grade credit compared to the benchmark enhances return if credit spreads narrow.

Worked Example 1.2

The benchmark holds 20% in A-rated corporate bonds, but the manager shifts to 40% A-rated bonds. During the period, A-rated spreads tighten by 25 bps, providing excess return. What is the primary attribution effect?

Answer:

This is a credit effect—the manager's overweight to A-rated credits caused performance to differ from the benchmark as these spreads tightened.

SELECTION EFFECTS

Selection effects reflect additional return not explained by systematic yield curve or credit exposures. These can be due to outperformance of specific securities, sectors, or issuers within a given risk bucket.

Key Term: sector selection

The portion of excess return from over- or underweighting particular sectors within the same credit rating or maturity segment.

Worked Example 1.3

A portfolio and its benchmark hold similar overall allocations to BBB credit, but the manager invests more in the technology sector, which outperforms other BBB sectors due to company-specific credit upgrades. Which effect captures this return?

Answer:

This is a selection (or sector selection) effect, as the manager's choices within the BBB bucket led to superior results compared to the benchmark's holdings.

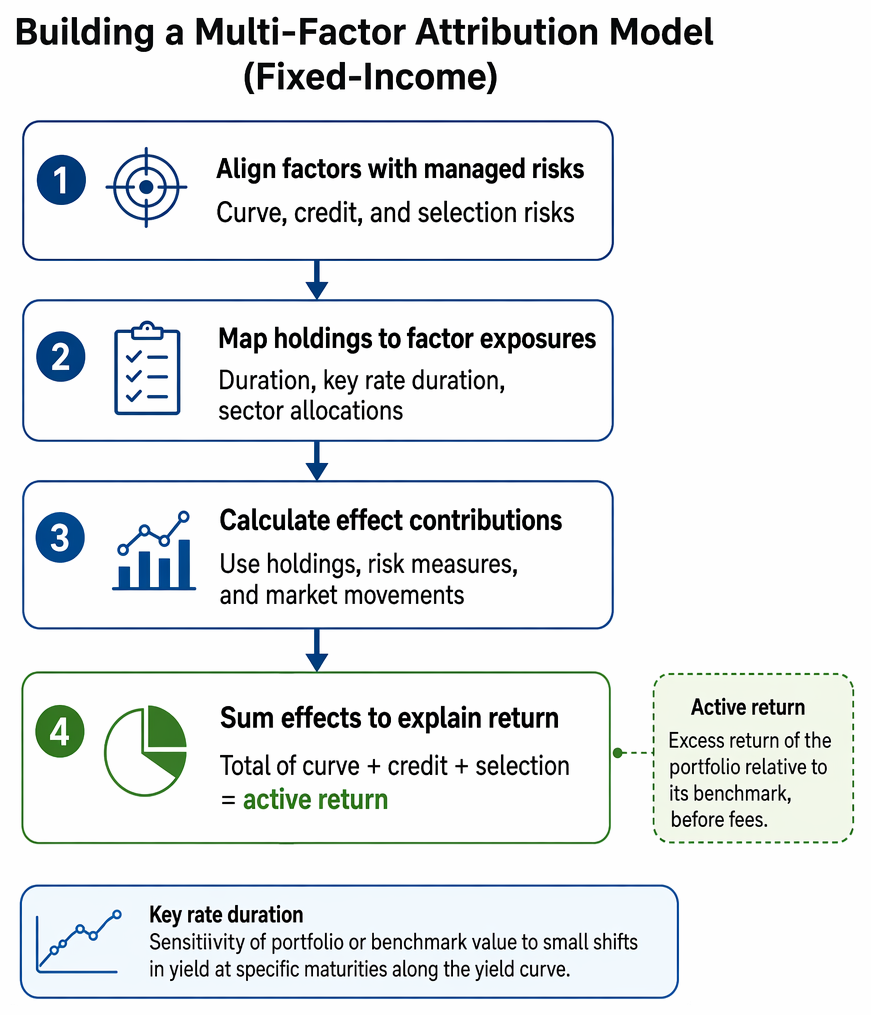

BUILDING THE MULTI-FACTOR ATTRIBUTION MODEL

A robust fixed-income attribution model requires:

Fixed-income active return attribution is presented as sequential steps from factor definition and exposure mapping to effect calculation and reconciliation.

- Aligning attribution factors (curve, credit, selection) with the risks managed by the portfolio.

- Accurately mapping portfolio and benchmark holdings to factor exposures (duration, key rate duration, sector allocations).

- Calculating effect contributions over the period using holdings, risk measures, and market movements.

- Summing the effects to explain total active return.

Key Term: key rate duration

The sensitivity of portfolio or benchmark value to small shifts in yield at specific maturities along the yield curve. Key Term: active return

The excess return of a portfolio relative to its benchmark, before fees.

INTERPRETING ATTRIBUTION RESULTS

Effective interpretation distinguishes systematic positioning from security selection results. For example, positive yield curve and credit effects suggest successful duration and sector allocation, while positive selection indicates effective security picking.

Exam Warning: A common candidate error is double-counting effects—such as attributing the same excess return to both credit allocation and selection. Be sure to allocate effects without overlap, following the model's definitions.

Revision Tip: Focus on understanding how curve, credit, and selection attributions interact. Practice breaking down sample returns into these components using attribution tables.

Summary

Fixed-income attribution is critical for evaluating manager skill and risk exposures. It breaks total active return into yield curve (interest rate), credit, and selection effects. Modern attribution methods use multi-factor models, mapping holdings to curve and credit sensitivities and separating systematic (beta) from active (alpha) sources. Accurate attribution supports meaningful performance evaluation and risk management.

Key Point Checklist

This article has covered the following key knowledge points:

- Break down active fixed-income return into yield curve, credit, and selection effects

- Yield curve effect: Differences in duration or curve exposure between portfolio and benchmark

- Credit effect: Sector or rating allocation versus benchmark exposure

- Selection effect: Security choice within curve/credit buckets, after other risk effects

- Multi-factor models are best practice for modern fixed-income attribution

- Attribution results should be interpreted in light of the portfolio's strategy and risk exposures

Key Terms and Concepts

- fixed-income attribution

- yield curve effect

- credit effect

- selection effect

- sector selection

- key rate duration

- active return