Learning Outcomes

This article explains attribution methods for CFA Level 3 performance evaluation, including:

- Distinguishing clearly between multi-factor, macro, and micro attribution frameworks, their purposes, and where each sits in the overall performance evaluation process.

- Understanding how multi-factor models decompose portfolio return and risk into systematic factor exposures, idiosyncratic components, and residual active return across equity, fixed-income, and multi-asset portfolios.

- Describing how macro-attribution allocates total fund results to strategic policy decisions, active versus passive implementation, tactical tilts, currency policy, and other sponsor-level choices.

- Describing how micro-attribution breaks active return into allocation, selection, interaction, and implementation effects at the asset-class, sector, and manager level.

- Comparing the advantages, limitations, data requirements, and governance uses of multi-factor, macro, and micro attribution in realistic institutional settings.

- Applying the appropriate attribution framework to diagnose performance shortfalls, identify sources of value added, and avoid misattributing sponsor decisions to managers (and vice versa).

- Interpreting numerical attribution outputs, explaining what they imply about manager skill, factor exposures, and policy effectiveness, and recognizing common exam traps and analytical errors.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand how attribution methods are applied for performance evaluation, with a focus on the following syllabus points:

- Differentiating between multi-factor models, macro- and micro-attribution approaches

- Interpreting the relative advantages, limitations, and use cases of each method

- Explaining how to assign returns and risks to portfolio decisions, factors, and implementation effects

- Calculating, interpreting, and critically assessing performance attribution results in a multi-asset/factor context

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Explain the primary difference between multi-factor and micro-attribution models in evaluating portfolio performance.

- What are the main advantages of macro-attribution versus micro-attribution from an asset owner’s standpoint?

- Why might a manager use a multi-factor model for attribution rather than a pure asset-class approach?

- True or false? Micro-attribution always explains the portion of returns due to market timing.

Introduction

Performance attribution methods help investors, consultants, and asset owners assess value added by portfolio managers. Understanding the distinctions between multi-factor, macro, and micro attribution is essential for CFA Level 3 candidates. Each approach offers a unique framework for assigning return or risk to portfolio decisions, investment factors, or asset allocation effects.

Key Term: Attribution

The process of dividing a portfolio’s return or risk into components attributable to sources like asset allocation, security selection, or risk factor exposures. Key Term: Multi-factor attribution

An attribution framework that explains portfolio returns or risk using exposures to multiple systematic factors such as style, sector, or macroeconomic variables. Key Term: Macro-attribution

Attribution evaluating the impact of high-level policy and implementation decisions on total portfolio performance, focusing on asset owner or sponsor choices. Key Term: Micro-attribution

Attribution assessing the value added by the portfolio manager at the portfolio and sub-portfolio (e.g., asset class) level, decomposing return into allocation, selection, and interaction effects.Test Tip: When revising Multi-factor and macro vs micro attribution, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

The Purpose and Context of Attribution Analysis

In institutional investment management, attribution is essential for evaluating not only how much return or risk was achieved, but why and how it was generated. The three main approaches—multi-factor, macro, and micro attribution—serve different analytical and governance needs.

Multi-factor Attribution

Multi-factor models explain returns or risk by attributing outcomes to exposure to multiple systematic factors, such as size, value, or macroeconomic variables.

Key Term: Systematic factor

A broad risk or return driver (e.g., style, interest rate, sector) affecting many assets simultaneously and commonly estimated using statistical or economic models.

These models are widely used for equity, fixed income, or global asset allocation portfolios. They allow fine-grained examination of the specific factors driving performance, adjusting for fundamental risk exposures.

Macro-Attribution

Macro-attribution focuses on the decisions made at the total fund or policy level. It evaluates value added (or destroyed) by high-level choices such as strategic asset allocation, active vs passive management, tactical shifts, borrowing, currency policy, and implementation style.

Key Term: Policy portfolio

A reference strategic asset allocation that serves as the long-term benchmark for evaluating broader portfolio management decisions.

Macro-attribution is most useful to asset owners, fiduciaries, or oversight boards seeking to assess how fund governance or sponsor-level decisions impact overall results.

Micro-Attribution

Micro-attribution looks at the results achieved by managers at the asset class or portfolio level. It decomposes active return into effects due to:

- Allocation (over-/underweighting asset classes or sectors)

- Selection (security or instrument choice)

- Interaction (the combined effect of allocation and selection)

- Sometimes, timing, currency, or trading costs

Micro-attribution aligns closely with the assessment of portfolio managers, making it valuable for manager monitoring and compensation.

Worked Example 1.1

A global balanced fund assigns 50% to a core policy portfolio of equities and 50% to bonds. The equities are managed by a value manager. Toward the end of the year, equities outperform bonds, but the value manager underperforms the equity benchmark.

Question: Which type(s) of attribution—macro, micro, or multi-factor—would best diagnose performance shortfalls in each area?

Answer:

Macro-attribution will reveal whether overweighting equities versus the policy contributed to excess return at the total fund level. Micro-attribution will show whether the equity manager added value relative to the equity benchmark. A multi-factor model might clarify whether the underperformance was due to style drift (e.g., non-value factor exposures) or was pure security selection.

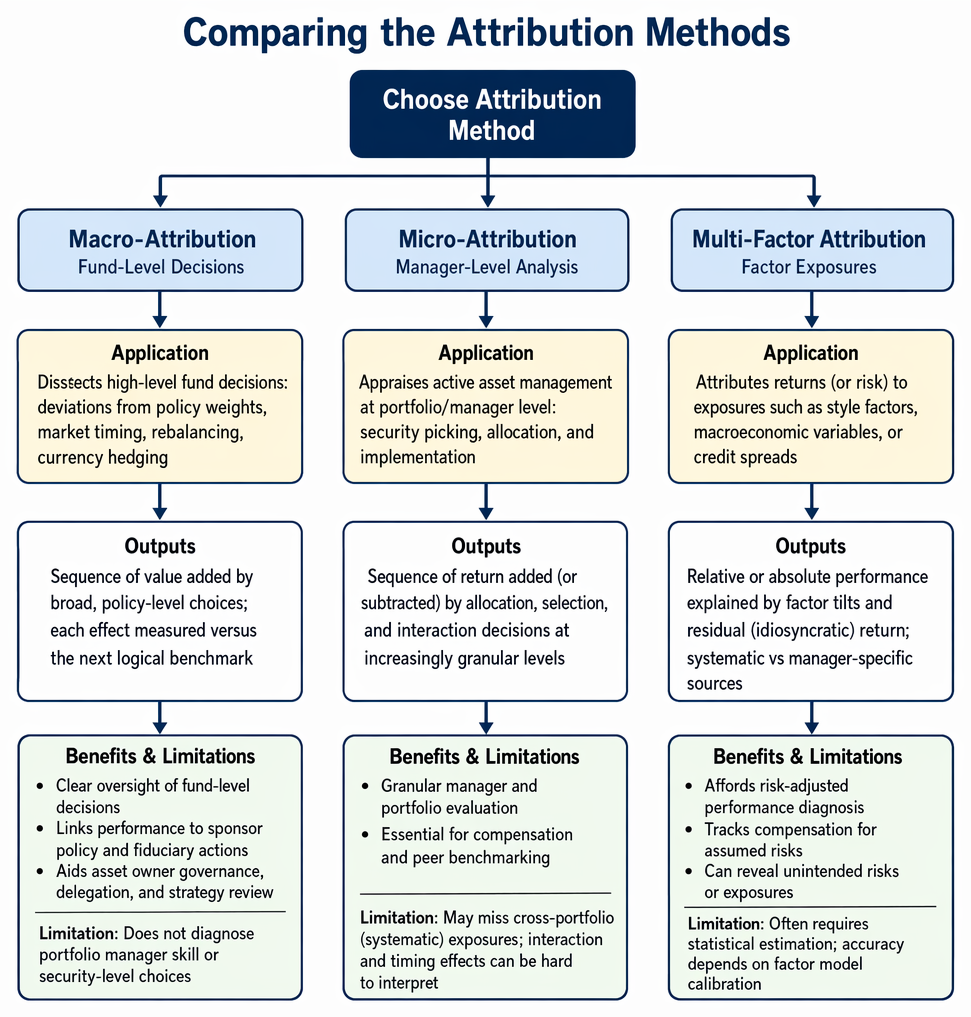

Comparing the Attribution Methods

Attribution framework selection maps policy decisions to macro analysis, manager-relative results to micro analysis, and factor sources to integrated assessment.

Application

- Multi-factor methods: Used to attribute returns (or risk) to exposures such as style factors (e.g., value, momentum, quality), macroeconomic variables, or credit spreads.

- Macro-attribution: Used to dissect the impact of high-level fund decisions, e.g., deviations from policy weights, market timing, rebalancing, currency hedging.

- Micro-attribution: Used to appraise active asset management, security picking, allocation, and implementation at portfolio/manager level.

Outputs

- Multi-factor: Relative or absolute performance explained by factor tilts and residual (idiosyncratic) return, enabling decomposition of returns into systematic and manager-specific sources.

- Macro: Sequence of value added by broad, policy-level choices (with each effect measured versus the next logical benchmark).

- Micro: Sequence of return added (or subtracted) by allocation, selection, and interaction decisions at increasingly granular levels.

Benefits and Limitations

Multi-factor approaches:

- Affords risk-adjusted performance diagnosis

- Tracks compensation for assumed risks

- Can reveal unintended risks or exposures

- Limitation: Often requires statistical estimation; accuracy depends on factor model calibration

Macro-attribution:

- Clear oversight of fund-level decisions

- Links performance to sponsor policy and fiduciary actions

- Aids asset owner governance, delegation, and strategy review

- Limitation: Does not diagnose portfolio manager skill or security-level choices

Micro-attribution:

- Granular manager and portfolio evaluation

- Essential for compensation and peer benchmarking

- Limitation: May miss cross-portfolio (systematic) exposures; interaction and timing effects can be hard to interpret

Worked Example 1.2

A total fund employs a reference portfolio benchmark of 60% global equities and 40% bonds. In one year, the actual weight averaged 70% equities/30% bonds. Equity markets delivered +8%, bonds –2%, and the actual portfolio returned +4.5%.

Question: What will a macro-attribution analysis reveal about the impact of asset allocation decisions this year? Could micro-attribution on the equity sub-portfolio explain the fund’s full performance outcome?

Answer:

Macro-attribution will show outperformance versus the policy portfolio from overweighting equities, quantifying the effect of the allocation deviation. Micro-attribution of the equity portfolio can further break the equity return into selection, allocation, and possibly currency and timing effects. However, micro-attribution will not capture the aggregate fund-level asset allocation effect—it analyzes only performance within each segment, relative to its own benchmark.

Attribution and Factor Models in Practice

Multi-factor attribution has become prevalent for large, complex portfolios where exposures to multiple systematic risks and cross-portfolio effects dominate. Macro-attribution is essential when reporting to governing boards or asset owners who set overall strategy. Micro-attribution remains standard for manager assessment, compensation, and search processes.

Key Term: Active return

The difference in return between a portfolio (or sub-portfolio) and its assigned benchmark; commonly further decomposed via attribution.Exam Warning: A common error is to apply micro-attribution results (e.g., security selection alpha) to conclusions about total fund-level value added. Always use macro-attribution for asset owner decisions and micro-attribution for manager evaluation.

Summary

Attribution analysis is central to investment performance evaluation. Multi-factor models dissect returns and risk by systematic factors, identifying exposures beyond asset class or sector. Macro-attribution decomposes value added at the policy and governance level, while micro-attribution targets sub-portfolio and manager-level skill across allocation and selection effects. Selecting the appropriate method is driven by the desired scope of the analysis and the decisions to be assessed.

Key Point Checklist

This article has covered the following key knowledge points:

- Distinguish between multi-factor, macro, and micro attribution and their use cases

- Recognize that multi-factor attribution explains performance by systematic risk factors

- Identify macro-attribution as focusing on asset owner or high-level decisions

- Identify micro-attribution as analyzing manager allocation and security selection

- Know when to apply each method and the limitations of using the wrong attribution scope

Key Terms and Concepts

- Attribution

- Multi-factor attribution

- Macro-attribution

- Micro-attribution

- Systematic factor

- Policy portfolio

- Active return