Learning Outcomes

This article explains the capital adequacy and liquidity management framework for banks and other financial institutions in a CFA Level 3 context, including:

- Interpreting the structure of bank and insurer balance sheets, highlighting ALM objectives implied by funding models, business lines, and regulatory constraints.

- Describing regulatory capital components, risk-weighted assets, leverage measures, and key ratios, and assessing how different asset mixes affect capital consumption in exam-style cases.

- Explaining how capital functions as a buffer against unexpected losses, how capital buffers operate, and how stress testing feeds into capital planning decisions.

- Calculating and evaluating liquidity risk metrics (LCR and NSFR), linking them to funding profiles, HQLA composition, and strategic asset allocation trade-offs.

- Analyzing asset–liability mismatches—interest rate, liquidity, currency, and maturity transformation—and judging their implications for earnings stability, solvency, and regulatory metrics.

- Assessing how regulatory and internal ALM constraints shape portfolio construction, risk-taking capacity, and the design of investment mandates for banks and similar entities.

- Comparing ALM challenges of banks versus insurers across different liability structures, investment horizons, and product sets, and drawing out implications for portfolio strategy.

- Formulating concise, exam-appropriate recommendations that improve capital and liquidity positions while remaining consistent with risk appetite, regulation, and franchise value preservation.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand how banks and other financial institutions manage their balance sheets with respect to ALM, capital adequacy, and liquidity risk, with a focus on the following syllabus points:

- Describing regulatory capital requirements for banks and insurance companies.

- Explaining the function of capital as a buffer against unexpected losses.

- Evaluating key liquidity needs, including the role of the liquidity coverage ratio (LCR), net stable funding ratio (NSFR), and liquidity stress testing.

- Analyzing the impact of asset–liability mismatches on risk management and required capital.

- Understanding how regulatory and internal constraints affect strategic asset allocation for banks and similar entities.

- Comparing the ALM challenges of banks and insurers across different liability structures and investment horizons.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

A bank’s CET1 ratio falls close to its regulatory minimum plus capital conservation buffer. Which management response is most consistent with regulatory expectations?

- a) Increase cash dividends and buy back common shares to signal confidence.

- b) Grow the loan book aggressively to restore profitability.

- c) Restrict capital distributions and reduce risk‑weighted assets through de‑risking.

- d) Replace common equity with more Tier 2 subordinated debt.

-

A bank reports an LCR of 80% and an NSFR of 115%. Which statement is most accurate?

- a) The bank is non‑compliant on both short‑term and structural liquidity.

- b) The bank meets short‑term liquidity standards but relies too heavily on short‑term funding.

- c) The bank fails the 30‑day stress liquidity test but has adequate stable funding over one year.

- d) The bank has excess HQLA but insufficient available stable funding.

-

A retail bank funds long‑dated fixed‑rate mortgages mainly with non‑interest‑bearing current accounts. What is the most significant risk from an ALM standpoint?

- a) Equity price risk from falling stock markets.

- b) Currency risk if domestic interest rates fall.

- c) Interest rate risk in the banking book due to duration and repricing mismatches.

- d) Credit risk from borrowers defaulting on mortgages.

-

When constructing a strategic asset allocation for a bank’s investment portfolio, which constraint is most likely binding relative to a typical pension fund?

- a) Minimum allocation to real assets for inflation protection.

- b) Upper limit on HQLA holdings to avoid excess idle liquidity.

- c) Tight regulatory requirements on LCR, NSFR, and capital ratios.

- d) Requirement to fully immunize liabilities using long‑duration bonds.

Introduction

The stability of banks and analogous financial institutions relies heavily on effective asset-liability management (ALM) and ongoing compliance with capital and liquidity regulations. The objective is to ensure that the institution maintains sufficient capital buffers and high-quality liquid assets to absorb unexpected losses and to meet obligations as they come due, even during periods of market disruption. These requirements are not just regulatory box-ticking—they are critical for maintaining trust in the wider financial system and for preserving franchise value.

Key Term: Asset-Liability Management (ALM)

Asset-liability management is the ongoing process of monitoring, measuring, and managing the risks arising from mismatches between the assets and liabilities of financial institutions, with the aim of maintaining balance sheet stability and meeting obligations under both normal and stressed conditions.

Balance sheet structure and ALM context for banks

Banks are unusual among institutional investors because they:

- Create both assets (loans, securities) and liabilities (deposits, wholesale funding) as part of their core business.

- Operate with high leverage, so small percentage changes in asset values can significantly affect equity.

- Engage in maturity transformation—funding longer‑term, illiquid assets with shorter‑term liabilities.

From the curriculum standpoint:

- Assets are dominated by loans (often 50%+ of the balance sheet), followed by debt securities, cash, and central bank reserves.

- Liabilities are dominated by deposits (retail and corporate), supplemented by wholesale funding and long‑term debt.

- Capital (equity and certain subordinated instruments) provides the residual buffer against losses.

ALM for banks therefore has three intertwined objectives:

- Maintain solvency: adequate capital relative to risk exposures.

- Maintain liquidity: enough cash and HQLA to survive funding stress.

- Control earnings and value volatility: especially from interest rate and credit spread movements.

Capital and liquidity regulations codify minimum standards for these objectives, while internal ALM policies and risk appetite statements set tighter constraints tailored to the institution’s strategy.

CAPITAL ADEQUACY: THE ROLE OF REGULATORY CAPITAL

Banks and insurers must hold a minimum amount of capital relative to their risk-weighted assets. This minimum is set by regulators to protect depositors, policyholders, and the broader economy from institutional failures. The major international framework is the Basel III Accord, which provides detailed definitions for various capital ratios and risk measurements.

Key Term: Regulatory Capital

Regulatory capital is the amount of capital that a bank or similar financial institution must hold, as defined by regulators, to absorb losses and protect against insolvency while continuing to operate. Key Term: Risk-Weighted Assets (RWA)

Risk-weighted assets are on- and off-balance-sheet exposures adjusted by regulatory risk weights that reflect their credit, market, and operational risk, forming the denominator for capital ratios. Key Term: Capital Adequacy Ratio (CAR)

The capital adequacy ratio is the ratio of a bank's eligible regulatory capital to its risk-weighted assets, used to assess the institution’s ability to withstand losses relative to the risk of its exposures.

Tiers of regulatory capital

Regulation distinguishes between high‑quality, permanent capital and lower‑quality, more subordinated instruments.

Key Term: Common Equity Tier 1 (CET1)

Common Equity Tier 1 is the highest quality capital comprising common shares and retained earnings, net of regulatory deductions such as goodwill and certain intangibles. Key Term: Tier 1 Capital

Tier 1 capital consists mainly of CET1 plus certain additional going-concern instruments (e.g., qualifying perpetual preferred shares and contingent convertible securities) that can absorb losses while the bank remains a going concern. Key Term: Tier 2 Capital

Tier 2 capital includes lower-quality, gone-concern instruments such as dated subordinated debt that can absorb losses only in resolution or liquidation.

Total regulatory capital is typically:

Capital ratios most commonly referenced:

- CET1 ratio:

- Tier 1 capital ratio:

- Total capital ratio (CAR):

Regulations prescribe minimum levels for these ratios. Basel III specifies global minima, and jurisdictions often layer on additional requirements. In exam questions, the relevant minimums are always given; use those rather than memorizing jurisdiction‑specific numbers.

Key Term: Leverage Ratio

The leverage ratio is a non-risk-weighted capital measure defined as Tier 1 capital divided by a bank’s total exposure measure (on-balance-sheet assets plus certain off-balance-sheet exposures), intended as a backstop to risk-based capital ratios.

Capital buffers and SIFI add-ons

In addition to minima, banks must hold buffers above them:

Key Term: Capital Conservation Buffer (CCB)

The capital conservation buffer is an additional CET1 requirement above minimum capital ratios that must be built up in normal times and can be drawn down in stress but triggers restrictions on distributions when breached. Key Term: Countercyclical Capital Buffer (CCyB)

The countercyclical capital buffer is a time-varying CET1 buffer, set by national authorities, that increases in credit booms and can be released in downturns to support lending. Key Term: Systemically Important Financial Institution (SIFI) Capital Surcharge

The SIFI capital surcharge is an extra CET1 requirement imposed on systemically important banks to reflect their greater potential impact on financial stability.

Capital ratios plus buffers determine:

- How much risk-weighted assets the bank can hold for a given capital base.

- How much capital is “free” to support growth or distributions.

- Whether the bank must restrict dividends, share buybacks, or variable remuneration.

From an ALM and portfolio standpoint, high‑risk assets with high risk weights (e.g., unsecured corporate loans) consume much more capital per unit of exposure than low‑risk assets (e.g., government bonds).

The function of capital as a loss buffer

Conceptually, expected credit losses are covered by provisions and pricing; capital is there to absorb unexpected losses. If cumulative losses exceed:

- First, loan loss provisions and current earnings, they start to erode capital.

- Second, CET1 — at which point the bank may breach regulatory minima and face restrictions or resolution.

Key Term: Economic Capital

Economic capital is an internally estimated capital level that management believes is needed to absorb losses at a chosen confidence level over a specified horizon, often higher and more risk-sensitive than regulatory capital.

ALM uses both regulatory and economic capital measures to evaluate trade‑offs among:

- Asset mix (e.g., loan growth versus securities portfolios).

- Concentrations (sector, geography, single-name).

- Interest rate risk positions (duration gap).

- Liquidity profile (amount and composition of HQLA).

Worked Example 1.1

A regional bank has total risk-weighted assets of $100 billion. Its core equity (Tier 1) capital is $8 billion, and its total regulatory capital is $11 billion. Calculate the bank’s Tier 1 and Total CAR, and assess compliance if the regulatory minimums are 6% for Tier 1 and 8% for total capital.

Answer:

- Tier 1 CAR = $8 billion / $100 billion = 8%.

- Total CAR = $11 billion / $100 billion = 11%.

- Both the Tier 1 (8% > 6%) and Total (11% > 8%) CAR exceed the required minimums, indicating regulatory compliance. In practice, the bank would also compare these ratios to any applicable buffers; exam questions will indicate buffer requirements if relevant.

Worked Example 1.2

A bank has $90 billion of RWA and holds $4.5 billion of CET1 capital and $2.7 billion of additional Tier 1 capital. The minimum CET1 ratio is 4.5%, the minimum Tier 1 ratio is 6%, and there is a 2.5% capital conservation buffer that must be met with CET1. Ignore other buffers.

Determine whether the bank meets:

- The CET1 minimum plus CCB.

- The Tier 1 minimum.

Answer:

- CET1 ratio = $4.5 / $90 = 5.0%. The CET1 minimum plus CCB is:

so the bank does not meet the CET1 minimum plus CCB.

- Tier 1 capital = $4.5 + $2.7 = $7.2 billion, so Tier 1 ratio = $7.2 / $90 = 8.0%, which exceeds the 6% minimum.

- Interpretation: The bank satisfies minimum Tier 1 requirements but has insufficient CET1 relative to the combined minimum plus conservation buffer. This would likely trigger constraints on dividends and buybacks until CET1 is rebuilt or RWA are reduced.

ALM, growth strategy, and capital

For Level 3, you must be able to link balance sheet strategy to capital ratios:

- Growing high‑risk loan books increases RWA and tends to reduce capital ratios unless matched by new capital.

- Shifting portfolios toward lower‑risk assets (e.g., sovereign bonds) can improve capital ratios even if nominal assets stay constant.

- Selling non‑core assets, securitizing loans, or using credit risk transfer instruments can reduce RWA and free up capital, but may affect earnings.

Portfolio decisions for banks are therefore made in a liability‑relative context: the asset mix must fit within both capital and liquidity constraints.

LIQUIDITY NEEDS AND MANAGEMENT

A key vulnerability for banks is funding liquidity risk—the potential for a sudden inability to obtain the cash needed to meet obligations. Banks must balance maximizing returns with maintaining sufficient high-quality liquid assets (HQLA). Global standards set specific liquidity risk metrics.

Key Term: Funding Liquidity Risk

Funding liquidity risk is the risk that a bank will not be able to meet its cash or collateral obligations as they fall due, at a reasonable cost, because it cannot roll over or replace funding. Key Term: Market Liquidity Risk

Market liquidity risk is the risk that a bank cannot quickly sell an asset at or near its fair value because market depth has deteriorated. Key Term: High-Quality Liquid Assets (HQLA)

High-quality liquid assets are assets that can be rapidly and reliably converted to cash at little or no loss in value, even under stressed market conditions, as defined by regulators for liquidity coverage purposes.

Regulators introduced two key ratios after the global financial crisis:

Key Term: Liquidity Coverage Ratio (LCR)

The liquidity coverage ratio is the ratio of a bank’s stock of HQLA to its expected total net cash outflows over a 30-day stress scenario. It must be at least 100%, ensuring enough HQLA to survive a severe short‑term stress. Key Term: Net Stable Funding Ratio (NSFR)

The net stable funding ratio is the ratio of available stable funding to required stable funding over a one-year horizon. It must be at least 100%, limiting reliance on unstable short-term funding and reducing structural funding risk.

Formally:

Key Term: Available Stable Funding (ASF)

Available stable funding is a weighted sum of a bank’s funding sources, where more stable items (e.g., retail term deposits, long-term debt, equity) receive higher ASF factors. Key Term: Required Stable Funding (RSF)

Required stable funding is a weighted sum of a bank’s assets and off-balance-sheet exposures, where less liquid and longer‑dated items (e.g., loans, illiquid securities) receive higher RSF factors.

Composition of HQLA and cash outflows (exam intuition)

While you are not expected to memorize detailed haircuts or factors, you should understand the economic logic:

-

HQLA includes:

- Level 1 assets (e.g., central bank reserves, sovereign bonds of high quality) with minimal haircuts.

- Certain Level 2 assets (e.g., some corporate bonds and covered bonds) with larger haircuts and caps.

-

Net cash outflows over 30 days reflect:

- Expected run-off of unstable deposits and wholesale funding.

- Drawdowns on committed credit and liquidity facilities.

- Contractual cash inflows, subject to caps.

A bank can improve its LCR by:

- Increasing HQLA (e.g., holding more government bonds or central bank reserves).

- Reducing expected stressed outflows (e.g., shifting from volatile wholesale funding to stickier retail deposits).

- Reducing undrawn commitments that generate contingent liquidity needs.

For NSFR, actions include:

- Increasing stable funding (more long-term debt, more equity, more sticky retail deposits).

- Reducing RSF by shortening asset maturities or holding more liquid assets.

Liquidity metrics shape the strategic asset allocation of banks. Institutions optimize so that maturities of funding sources and assets are aligned or offset using liquid buffers.

Worked Example 1.3

A bank has $40 billion in HQLA and estimated 30-day net cash outflows of $35 billion under a stress test. What is its LCR, and does it comply with the Basel III minimum requirement?

Answer:

- LCR = $40 billion / $35 billion = 114%.

- Since the LCR must be at least 100%, the bank is above the minimum and thus compliant. Management could, in principle, take more term funding risk or modestly reduce HQLA if capital and other constraints allow.

Worked Example 1.4

A bank’s balance sheet includes:

- $50 billion of equity and long-term debt considered 100% stable (ASF factor = 100%).

- $80 billion of retail deposits considered 90% stable (ASF factor = 90%).

- $20 billion of short-term wholesale funding (ASF factor = 50%).

On the asset side, the bank holds $60 billion of loans (RSF factor = 85%), $50 billion of securities (RSF factor = 50%), and $10 billion of cash and central bank reserves (RSF factor = 0%).

Calculate the NSFR and comment on compliance with a 100% minimum.

Answer:

- Available stable funding:

- Equity and long-term debt: $50 × 100% = $50

- Retail deposits: $80 × 90% = $72

- Wholesale funding: $20 × 50% = $10

- Total ASF = $50 + $72 + $10 = $132 billion

- Required stable funding:

- Loans: $60 × 85% = $51

- Securities: $50 × 50% = $25

- Cash/reserves: $10 × 0% = $0

- Total RSF = $51 + $25 + $0 = $76 billion

- NSFR = $132 / $76 ≈ 174%.

- The bank is comfortably above the 100% minimum. From an ALM standpoint, it may have room to modestly increase long‑dated assets or reduce reliance on expensive long-term funding, subject to other constraints (e.g., capital and risk appetite).

Exam Warning: A frequent exam error is to confuse LCR with NSFR. The LCR applies to short-term (30 days) acute liquidity stress, while the NSFR is a structural measure for stable funding over one year. LCR is about HQLA vs stressed 30‑day outflows; NSFR is about funding profile vs asset profile over one year.

ASSET-LIABILITY MISMATCHES AND CAPITAL IMPLICATIONS

Mismatches in the timing and characteristics of assets and liabilities—such as funding long-term, illiquid assets with short-term wholesale funding—introduce market and liquidity risks.

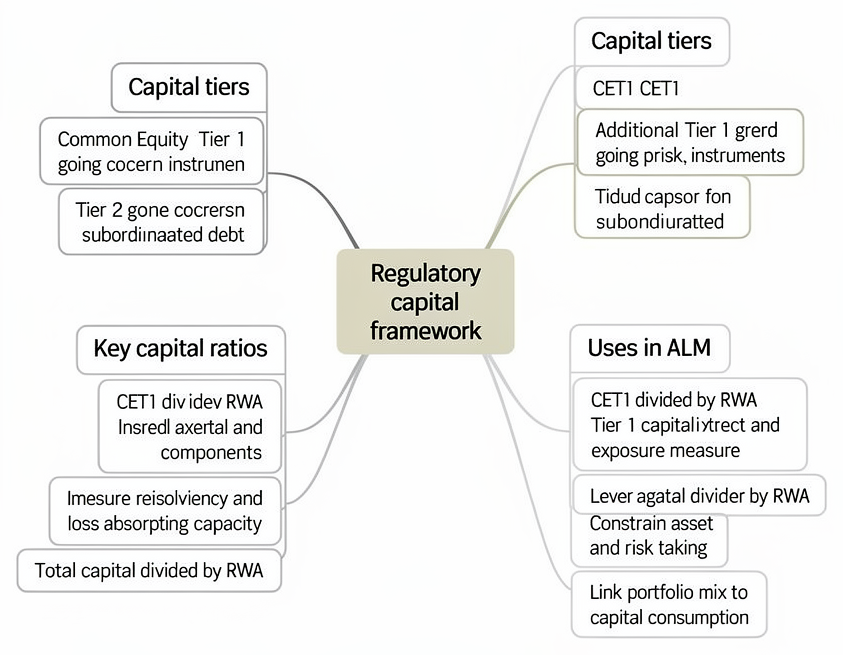

Bank capital adequacy structure summarizes CET1, Additional Tier 1, Tier 2, RWA measurement, leverage, and ALM implications.

Key Term: Maturity Mismatch

Maturity mismatch is a situation in which the maturities or repricing dates of assets and liabilities differ significantly, increasing exposure to refinancing risk and interest rate risk.

Banks can have mismatches in:

- Maturity: long-term assets vs short-term liabilities (classic maturity transformation).

- Repricing: fixed-rate assets vs floating-rate liabilities or vice versa.

- Currency: assets and liabilities in different currencies.

- Liquidity: illiquid assets funded by liabilities that may run off quickly under stress.

These mismatches can increase:

- Interest rate risk exposure.

- Funding costs and access risk in stress scenarios.

- Regulatory capital requirements by raising RWA (e.g., if higher risk or longer-dated assets are added).

- The chance of regulatory action or rating downgrades.

Key Term: Interest Rate Risk in the Banking Book (IRRBB)

Interest rate risk in the banking book is the risk to a bank’s earnings and economic value arising from adverse movements in interest rates affecting assets, liabilities, and off-balance-sheet positions that are not held for trading.

Earnings and value views

ALM typically measures interest rate risk from two angles:

- Earnings view: sensitivity of net interest income (NII) over a short horizon to changes in rates.

- Economic value view: impact on the present value of assets, liabilities, and off-balance-sheet items (economic value of equity).

A positive duration gap (asset duration > liability duration) means rising rates:

- Reduce the present value of assets more than liabilities (negative impact on economic value).

- May increase NII if assets reprice faster or to higher margins.

ALM must weigh these impacts, taking into account regulatory expectations and risk appetite.

Worked Example 1.5

A bank funds 10-year fixed-rate loans with 3‑month deposits. If short-term rates increase sharply, what risks does the bank face and what ALM steps should be taken?

Answer:

- The bank’s interest expense on 3‑month deposits will reset quickly at higher rates, while the interest income on 10‑year fixed‑rate loans is locked in. Net interest margin is compressed and may turn negative, harming earnings.

- The bank also faces refinancing risk: depositors may withdraw or demand higher rates, and wholesale markets may be reluctant to roll over funding at reasonable terms.

- ALM responses could include:

- Increasing longer‑term funding (e.g., issuing term debt) to reduce maturity mismatch.

- Using interest rate derivatives (e.g., pay‑fixed swaps) to hedge the duration gap.

- Holding more HQLA to provide a liquidity buffer against deposit outflows.

- Adjusting pricing and product design (e.g., offering more floating‑rate loans) to reduce structural mismatch over time.

ALM, capital, and risk appetite

Maturity mismatches interact with capital in several ways:

- A bank that takes large interest rate positions may face higher economic capital requirements, even if regulatory capital does not explicitly capture IRRBB.

- Adverse rate movements can reduce earnings and retained profits, slowing capital generation.

- Large liquidity mismatches that increase reliance on short-term wholesale funding can heighten funding liquidity risk, potentially triggering regulatory concerns and higher required buffers.

From an exam standpoint, you should be able to:

- Identify whether an ALM profile increases or reduces risk.

- Recommend balance sheet adjustments consistent with regulatory ratios, internal limits, and franchise considerations.

SETTING ALM POLICY: INTERNAL CONSTRAINTS AND BALANCE SHEET MANAGEMENT

Regulators require banks and insurers to have robust internal risk controls governing ALM, capital, and liquidity positions. Internal risk appetite statements set limits for:

- Overall leverage (assets/equity).

- Sector, country, or product exposures.

- Maximum permitted asset-liability gaps by maturity bucket.

- Concentration risk (e.g., large depositors or borrowers, single‑name or sector limits).

- Minimum capital and liquidity buffers above regulatory thresholds.

The ALM framework must balance regulatory requirements, business strategy, and shareholder value. The ALM committee (ALCO) typically governs these processes, overseeing monitoring and management of all material balance sheet risks.

Key Term: ALM Committee (ALCO)

The ALM committee is the senior management group responsible for setting, monitoring, and controlling the institution’s ALM strategy, risk appetite, and balance sheet structure, including capital and liquidity positions.

ALCO responsibilities typically include:

- Approving target ranges for capital ratios and liquidity metrics (LCR, NSFR, internal stress metrics).

- Setting interest rate risk limits (e.g., maximum NII sensitivity or economic value sensitivity to parallel and non‑parallel shocks).

- Approving structural hedges (e.g., interest rate swaps used to manage duration).

- Overseeing funding strategy (mix of retail vs wholesale, maturity ladder, currency composition).

- Reviewing stress test results and contingency funding plans.

Key Term: Contingency Funding Plan (CFP)

A contingency funding plan is a documented set of strategies and actions that a bank will undertake to address liquidity shortfalls under stress scenarios, including asset sales, collateral usage, and alternative funding sources.

In the Level 3 context, you may have to:

- Evaluate whether a proposed ALM action (e.g., lengthening asset duration, increasing illiquid assets) is consistent with stated risk appetite and risk limits.

- Recommend adjustments when regulatory measures (capital ratios, LCR, NSFR) approach internal floors.

ADVANCED TOPICS: STRESS TESTING AND LIQUIDITY BUFFERS

Stress testing is required by both regulators and prudent management to assess vulnerability to extreme scenarios. Stress test outputs drive decision making for buffer size and composition, contingency funding plans, and capital actions, such as dividend policies.

Key Term: Liquidity Stress Testing

Liquidity stress testing is the process of projecting a bank’s cash flows, liquidity position, and regulatory ratios under adverse but plausible scenarios to assess its ability to meet obligations and maintain regulatory compliance.

Stress tests can be:

- Sensitivity analyses: examining the effect of isolated shocks (e.g., +200 bps rate shift, 10% deposit outflow).

- Scenario analyses: modeling combined macroeconomic and market stresses (e.g., recession, spread widening, equity market fall).

- Reverse stress tests: starting from a failure outcome (e.g., breach of CAR or LCR) and inferring what scenario could cause it.

They are performed for:

- Capital adequacy (credit losses, market risk losses, earnings paths, impact on capital ratios).

- Liquidity adequacy (projected outflows, HQLA usage, LCR/NSFR paths).

Worked Example 1.6

A bank currently has:

- CET1 ratio: 9.5% (minimum including buffers = 8.0%).

- LCR: 120%.

- NSFR: 105%.

A regulatory stress test projects that under a severe recession:

- Credit losses reduce CET1 ratio by 2.0 percentage points.

- Funding stress and asset sales reduce LCR to 95% at the trough.

- NSFR remains above 100%.

What actions should management consider before the stress test scenario materializes?

Answer:

- Under stress, CET1 ratio would fall to 7.5% (9.5% – 2.0%), below the 8.0% threshold, and LCR to 95%, below 100%. NSFR remains compliant.

- Proactive actions could include:

- Strengthening capital: retain a higher share of earnings, issue new common equity or AT1 instruments, or reduce RWA (e.g., through loan sales or tighter underwriting standards).

- Enhancing liquidity: increase HQLA holdings (e.g., more sovereign bonds, central bank reserves) or improve funding stability (e.g., lengthen funding maturities, attract more retail term deposits).

- Reassessing dividend and buyback policies to preserve CET1.

- The key ALM point is that both capital and short‑term liquidity buffers are thin relative to stress losses; management should build these up preemptively to maintain flexibility and avoid forced asset sales in a downturn.

Revision Tip: Practical CFA questions often require you to link stress testing results to management actions: for example, raising capital, increasing buffers, adjusting risk exposures, or revising distribution policies. Always explain why an action addresses the identified capital or liquidity shortfall.

Summary

Banks and similar institutions must rigorously manage ALM, capital adequacy, and liquidity risks to ensure financial stability and regulatory compliance. Capital ratios (CET1, Tier 1, CAR) relative to RWA measure solvency and the ability to absorb unexpected losses. Liquidity metrics (LCR, NSFR) ensure that the funding profile is robust both over 30‑day stress horizons and over a one‑year structural horizon.

Effective ALM involves:

- Understanding the risk implications of maturity, repricing, and liquidity mismatches.

- Designing internal limits and risk appetite that are tighter than regulatory minima.

- Using stress testing and contingency funding plans to determine the appropriate size and composition of capital and liquidity buffers.

- Integrating balance sheet management with strategic asset allocation decisions, recognizing that for banks the asset portfolio exists to serve liabilities and regulatory constraints, not just to maximize returns.

For Level 3, you are expected to integrate these elements—capital, liquidity, and ALM policy—when evaluating balance sheets and recommending portfolio and risk management actions.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain why capital adequacy is central to bank safety, regulatory policy, and shareholder value.

- Distinguish CET1, Tier 1, Tier 2, and total regulatory capital, and relate them to risk-weighted assets and leverage.

- Calculate and interpret capital ratios and liquidity risk metrics (CAR, LCR, NSFR) in exam-style scenarios.

- Identify and manage asset-liability mismatches (maturity, repricing, currency, liquidity) and understand their risk and capital consequences.

- Distinguish LCR (short-term liquidity risk) from NSFR (structural funding risk) and recommend actions to improve each.

- Relate stress testing results to appropriate capital and liquidity management actions, including buffers and distribution policies.

- Use ALM limits, risk appetite statements, and governance via ALCO to align risk, profitability, and regulatory compliance.

Key Terms and Concepts

- Asset-Liability Management (ALM)

- Regulatory Capital

- Risk-Weighted Assets (RWA)

- Capital Adequacy Ratio (CAR)

- Common Equity Tier 1 (CET1)

- Tier 1 Capital

- Tier 2 Capital

- Leverage Ratio

- Capital Conservation Buffer (CCB)

- Countercyclical Capital Buffer (CCyB)

- Systemically Important Financial Institution (SIFI) Capital Surcharge

- Economic Capital

- Funding Liquidity Risk

- Market Liquidity Risk

- High-Quality Liquid Assets (HQLA)

- Liquidity Coverage Ratio (LCR)

- Net Stable Funding Ratio (NSFR)

- Available Stable Funding (ASF)

- Required Stable Funding (RSF)

- Maturity Mismatch

- Interest Rate Risk in the Banking Book (IRRBB)

- ALM Committee (ALCO)

- Contingency Funding Plan (CFP)

- Liquidity Stress Testing