Learning Outcomes

This article explains the investment objectives, return sources, and benchmark considerations for banks and other financial institutions within the CFA Level 3 curriculum, including:

- Defining how banks differ from other institutional investors and how their liability structures, funding stability, and business models shape conservative investment policies.

- Describing primary investment objectives such as capital preservation, liquidity maintenance, income generation, and strict compliance with regulatory capital and liquidity requirements.

- Explaining how regulatory frameworks, asset-permissibility rules, and accounting classifications constrain portfolio construction, risk-taking capacity, and reported earnings volatility.

- Identifying the main sources of return for banks, particularly net interest income and low-risk securities portfolios, and linking these to asset–liability management.

- Analyzing trade-offs between yield, credit quality, duration, and market liquidity when selecting government, agency, municipal, and corporate bonds for the investment book.

- Describing appropriate benchmark characteristics for bank portfolios, including quality, duration, currency, and liquidity alignment with policy and regulatory requirements.

- Evaluating when standard government bond indices are suitable versus when customized or blended benchmarks are needed to reflect actual permissible holdings.

- Highlighting common CFA Level 3 exam pitfalls, such as endorsing benchmarks that embed impermissible assets, excessive risk, or insufficient liquidity for regulated institutions.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the specific investment policy requirements and benchmarking considerations for banks and other financial institutions, with a focus on the following syllabus points:

- Determining the unique investment objectives of banks (liquidity, income, regulatory capital, risk tolerance)

- Explaining the relationship between a bank's liabilities, investment policy, and sources of return

- Evaluating appropriate performance benchmarks for banks and similar institutions

- Interpreting regulatory and accounting constraints as they affect investment portfolio design and performance assessment

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the primary investment objective of a commercial bank's investment portfolio?

- When is a government bond index an appropriate benchmark for a bank's investment book?

- Why must a bank manage both liquidity and interest rate risk in its portfolio?

- What regulatory constraint is particularly significant in determining a bank's permissible asset mix?

Introduction

Banks and other financial institutions are unique among institutional investors. Unlike pension funds and endowments, their investment portfolios are deeply intertwined with operating businesses, regulatory capital, and liquidity management. For the CFA Level 3 exam, you must understand how banks approach their investment policy, the distinct return sources they pursue, and how they select benchmarks compatible with their business and regulatory context.

Key Term: investment objective

The specific risk and return goals set by an institution for its investment portfolio, considering balance sheet needs, regulations, and business model. Key Term: regulatory capital

The minimum capital required by regulators that banks must maintain relative to their risk-weighted assets for safety and soundness. Key Term: benchmark

A standard against which the performance and risk of an investment portfolio is measured. For banks, commonly a market index reflecting both return and liquidity risk.

Investment Objectives of Banks and Similar Institutions

Banks play a dual role in financial markets: they provide loans and other assets as part of core business, and they manage significant investment securities portfolios. Compared to other institutional investors, banks are more constrained by regulation and internal risk considerations.

Capital, liquidity, asset-eligibility, and accounting requirements collectively shape bank portfolios toward high-quality liquid assets and conservative duration.

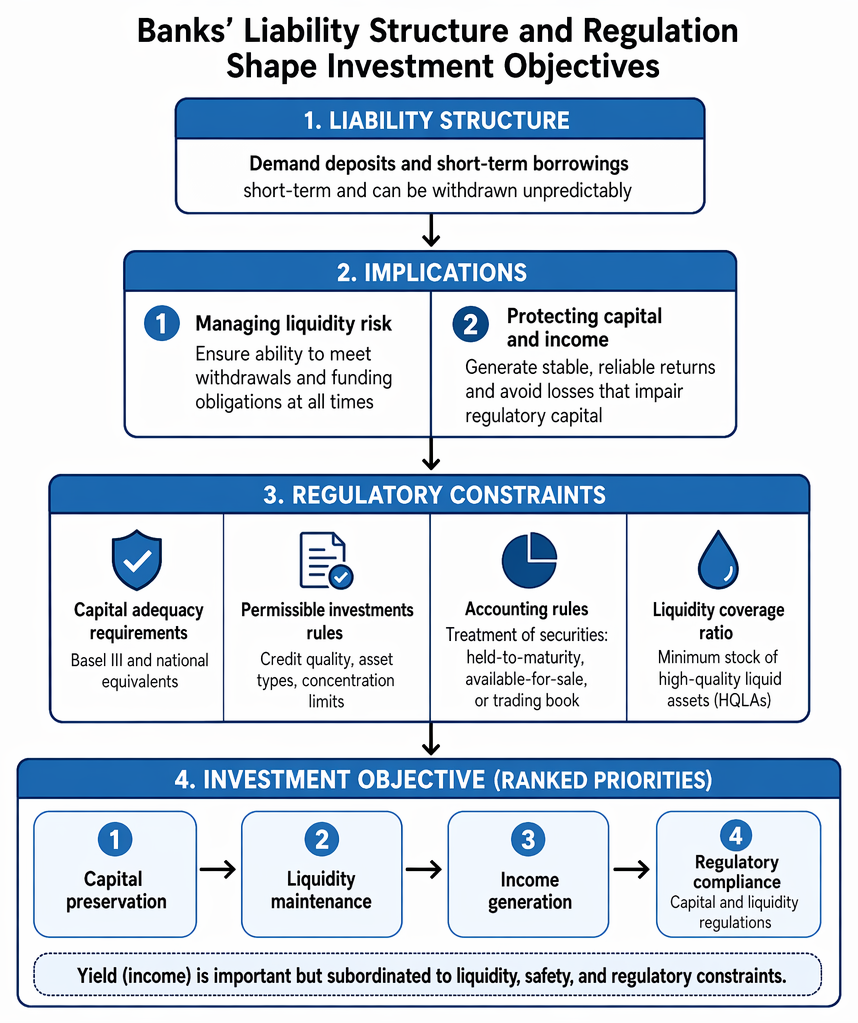

Liability Structure and Implications

Commercial banks take deposits and provide loans. Their liabilities, such as demand deposits and other short-term borrowings, are usually short-term and can be withdrawn unpredictably. This structure creates two dominant investment policy objectives:

- Managing liquidity risk – ensuring the bank can meet withdrawals and funding obligations at all times.

- Protecting capital and income – generating stable, reliable returns on the investment portfolio while minimizing volatility in reported earnings and avoiding large losses that could impair regulatory capital.

Key Term: liquidity risk

The risk that an institution cannot meet expected or unexpected cash flow needs without incurring unacceptable losses.

Regulatory Constraints and Investment Objectives

Bank portfolios are regulated to protect depositors and the financial system. The main regulatory constraints affecting their investment policy include:

- Capital adequacy requirements (Basel III and national equivalents)

- Strict rules on permissible investments (credit quality, asset types, concentration limits)

- Accounting rules affecting the treatment of securities (e.g., held-to-maturity, available-for-sale, or trading book)

- Liquidity coverage ratios requiring a minimum stock of high-quality liquid assets (HQLAs)

Banks must maintain sufficient high-quality, liquid assets. Therefore, the investment objective is generally a combination of:

- Capital preservation

- Liquidity maintenance

- Income generation

- Compliance with capital and liquidity regulations

Yield (income) is important but is strictly subordinated to liquidity, safety, and regulatory constraints.

Return Sources for Banks and Institutions

Banks earn returns in three main ways:

- Net Interest Income: The spread between the yield on loans and other assets and the cost of liabilities (deposits and borrowings). Portfolio construction must protect this spread from adverse interest rate movements.

- Fee and Commission Income: Outside typical investment portfolios, but relevant for total bank profitability.

- Investment Portfolio Return: The income (primarily interest and occasional capital gains) from securities holdings—most commonly bonds.

Key Term: net interest income

The difference between the interest earned on assets and the interest paid on liabilities.

The investment book is typically constructed to supply liquidity, act as a buffer under stress, and generate modest, stable income. Asset choices (usually government and high-grade bonds) are made for low credit risk and high marketability.

Return Drivers and Risk Exposures

- Interest rate management: Matching asset and liability durations helps control net interest income volatility.

- Credit management: High-quality assets are prioritized to avoid impairment.

- Market liquidity preference: Assets must be liquid enough to meet regulatory ratios and actual withdrawal scenarios.

Worked Example 1.1

A mid-sized national bank holds $1.2 billion in deposits. Its main investment book consists of short- and medium-term government and investment-grade bonds. The CFO is reviewing the investment policy.

Question: Should the CFO advocate for a greater allocation to corporate bonds with higher yield but lower liquidity?

Answer:

No. While higher-yielding corporate bonds may lift portfolio income, they introduce higher credit risk and lower liquidity. This could conflict with regulatory liquidity coverage ratio (LCR) requirements and impair the bank's ability to meet withdrawals. The primary investment objectives are safety and liquidity, thus expansion into lower-rated bonds should be tightly limited and justified only if liquidity and regulatory metrics are not compromised.

Benchmarking for Banks and Institutions

Performance assessment must consider regulatory constraints and business objectives. The portfolio benchmark for a bank typically reflects the policy portfolio agreed with the board, considering regulatory, liquidity, and risk criteria.

Selecting a Benchmark

A bank's benchmark should:

- Reflect the return and risk of a portfolio constructed to meet liquidity and regulatory requirements (commonly a government bond index)

- Be composed of market instruments with high liquidity, similar duration, and risk profile to the bank's investment book

- Exclude risky or illiquid assets not permitted by policy

Benchmarks are most often market indices (e.g., local government bond index, high-quality bond index) or custom bond indices matching portfolio duration and quality profile. Broad equity indices are generally not appropriate, as banks typically have limited or no allocation to equities for regulatory reasons.

Key Term: benchmark

A standard, usually a bond index, for measuring investment performance and risk, tailored to reflect policy and regulatory constraints for banks.

Worked Example 1.2

A bank runs its portfolio to match the risk and duration of the national government bond index. However, management has added a small allocation to municipal bonds and agency securities.

Question: How should the bank adjust or supplement its benchmark?

Answer:

If material, the benchmark should be modified to include representative proportions of municipal bonds and agency securities, provided these are consistent with policy and regulatory allowances. If these allocations are small, the primary government bond index remains suitable but with supplemental monitoring of returns on these added asset classes for oversight.Exam Warning: For banks, benchmarks must not include assets that are not policy-permitted or are inconsistent with regulatory requirements. Including risky or illiquid securities in the benchmark can create a misleading picture of relative performance and might incentivize excessive risk-taking.

Special Considerations for Other Institutions

Insurance companies, government-related investment pools, and supranational investment institutions share similarities with banks in their investment policy formulation. Their investment objectives are shaped by:

- Nature of their liabilities (long-term fixed, short-term variable, or contingent)

- Regulatory and accounting standards

- Board or stakeholder investment goals (e.g., minimizing contribution volatility for insurance and pension funds)

Portfolio benchmarks are chosen to reflect these objectives and regulatory requirements. For life and general insurers, asset-liability management (ALM) is often central to maintaining solvency and stability.

Revision Tip: Always relate banks' investment objectives and benchmark construction back to their liability structure, regulatory standards, and risk management framework. Portfolio optimization is secondary to regulatory and liquidity compliance.

Summary

- Banks' investment policies focus first on capital preservation and liquidity, then on stable income.

- Regulatory constraints (especially on capital and liquidity) shape both permissible asset allocations and risk limits.

- Return sources arise mainly from net interest income and low-risk bond portfolios; fee income is usually separate.

- Benchmarks should reflect the limited risk tolerance implicit in policy, regulation, and liquidity requirements—commonly government or high-grade bond indices.

- Risk management and performance monitoring must always consider both internal policy and external regulatory standards.

Key Point Checklist

This article has covered the following key knowledge points:

- Banks’ unique liability and regulatory structures shape conservative investment objectives.

- Primary objectives are liquidity, safety, and modest income consistent with regulations.

- Net interest income and liquid bond portfolios are the main sources of return.

- Benchmarks must reflect liquidity, regulatory, and risk constraints—typically high-quality bond indices.

- Careful benchmark selection discourages excessive risk-taking and aligns performance analysis with policy.

Key Terms and Concepts

- investment objective

- regulatory capital

- benchmark

- liquidity risk

- net interest income