Learning Outcomes

This article explains how regulatory frameworks shape banks’ and other institutions’ use of debt and investment constraints in an exam-focused way. It clarifies the purpose and structure of capital requirements, distinguishing risk-based capital ratios from simple capital-to-assets ratios and explaining how each limits balance-sheet expansion and asset growth. The discussion shows how capital adequacy standards such as Basel III, Solvency II, and related rules translate into practical limits on portfolio risk, concentration, and the selection of permissible asset classes. The article explains how liquidity regulations, including liquidity coverage requirements, influence the trade-off between yield and marketability, and why illiquid or complex instruments attract higher capital charges or outright restrictions. It highlights how regulatory borrowing limits, minimum capital cushions, and stress-testing regimes affect target capital structure, risk budgeting, and portfolio rebalancing decisions for banks and insurers. Finally, the article links these regulatory tools to typical CFA Level 3 item-set questions, preparing candidates to interpret exhibits, identify binding constraints, diagnose compliance breaches, and recommend portfolio adjustments that respect regulatory, liquidity, and risk-management objectives.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the regulatory and balance sheet constraints that apply to banks and other institutional investors, especially with regard to investment policy and borrowing limits. These are frequent areas of focus in exam case studies and item sets, with a focus on the following syllabus points:

- Understand how capital adequacy standards affect investment strategy for banks and insurers

- Explain the implications of liquidity regulations and stress testing requirements

- Assess constraints on borrowing within regulatory frameworks (Basel III, Solvency II, etc.)

- Evaluate the impact of external regulation on a bank/insurer’s permissible investments, use of debt, and risk appetite

- Identify operational risks arising from the use of debt and capital requirement breaches

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Explain how minimum capital requirements affect the risk allocation and use of debt of a commercial bank.

- What is the regulatory capital-to-assets ratio, and how does it differ from a risk-based capital ratio?

- A life insurer faces falling bond yields. What regulatory considerations might limit its response?

- Why might illiquid investments be restricted for some regulated institutions?

Introduction

Banks and similar financial institutions are subject to detailed regulatory frameworks designed to safeguard their solvency, control risk, and limit system-wide threats. These regulatory constraints shape their investment strategies—especially regarding the use of debt, capital allocation, and permitted assets. For CFA exam purposes, understanding these regulations and their practical effects is often tested in institutional case studies and scenario analysis.

Key Term: regulatory capital

The amount and quality of capital a regulated institution is required to maintain, as defined by supervisory rules, to absorb losses and protect depositors and policyholders. Key Term: capital-to-assets ratio

A regulatory measure comparing a bank’s Tier 1 capital to its total (unweighted) assets, acting as a backstop to risk-based capital ratios. Key Term: risk-based capital ratio

The ratio of an institution’s eligible capital to its risk-weighted assets. It requires firms with riskier exposures to hold more capital.Test Tip: When revising Regulatory constraints and leverage, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Regulatory Constraints: Capital and Use of Debt

Banks, insurers, and many other institutions can only operate with explicit authorization and under strict regulatory regimes. The rationale is to ensure the stability of the wider financial system, to protect depositors and policyholders, and to reduce the risk of catastrophic losses.

Capital adequacy monitoring computes capital-to-risk-weighted-assets and capital-to-assets ratios, compares them with minimum thresholds, and identifies the binding constraint.

Capital Requirements

Institutions are required to maintain a minimum level of capital—a cushion that absorbs losses and prevents default. The precise definition of "capital" is set by the relevant regulator and typically emphasizes high-quality equity-like capital (e.g., Common Equity Tier 1 for banks, or “own funds” for insurers).

Most capital requirements are risk-adjusted. That means the required capital is set in relation to the riskiness of the institution’s investments and other exposures, not just their nominal value.

Key Term: capital adequacy ratio

The ratio of a financial institution’s capital to its risk-weighted assets. It is used to determine if the institution has sufficient capital to absorb a reasonable amount of loss.

Risk-Based and Capital-to-Assets Ratios

Two major approaches to regulatory measurement exist:

- Risk-based capital ratios (e.g., Basel III Tier 1 and Total Capital Ratios for banks; Solvency II ratios for insurers): Capital is required in proportion to "risk-weighted assets." This approach incentivizes holding lower-risk assets, and penalizes concentrated or riskier exposures.

- Capital-to-assets ratio: Typically calculated as Tier 1 capital divided by total assets, without risk-weighting. Acts as a limiting safeguard so that banks cannot take on too much nominal debt by simply increasing exposures to low-risk-weight assets.

Regulators may impose both types of limits and require compliance with whichever is more conservative.

Key Term: Basel III

An international regulatory framework for banks that stipulates minimum capital ratios, liquidity requirements, and introduces the capital-to-assets ratio and new risk measurement standards.

Liquidity Requirements

Regulators commonly require institutions to maintain a minimum stock of highly liquid assets, to manage cash flow mismatches, and to survive short-term funding shocks. For example, the Liquidity Coverage Ratio (LCR) for banks mandates a sufficient holding of assets that can be quickly sold or pledged, reducing the risk of a run or forced-fire sales in stressed conditions.

Permissible Investments

Regulatory charter often restricts the types of investments an institution can make, both to reduce risk and to help align the institution’s risk profile with consumer protection goals. Illiquid or riskier investments (private equity, structured credit, long-dated alternatives) usually attract higher capital charges—or may be outright excluded.

Limits on Borrowing and Asset Growth

Regulators may impose direct limits on borrowing—that is, the use of debt funding relative to equity capital—either as a stand-alone absolute limit (the capital-to-assets ratio for banks), or as a consequence of risk-based capital and asset eligibility rules. These constraints reduce the scope for maximizing returns through asset growth or portfolio borrowing.

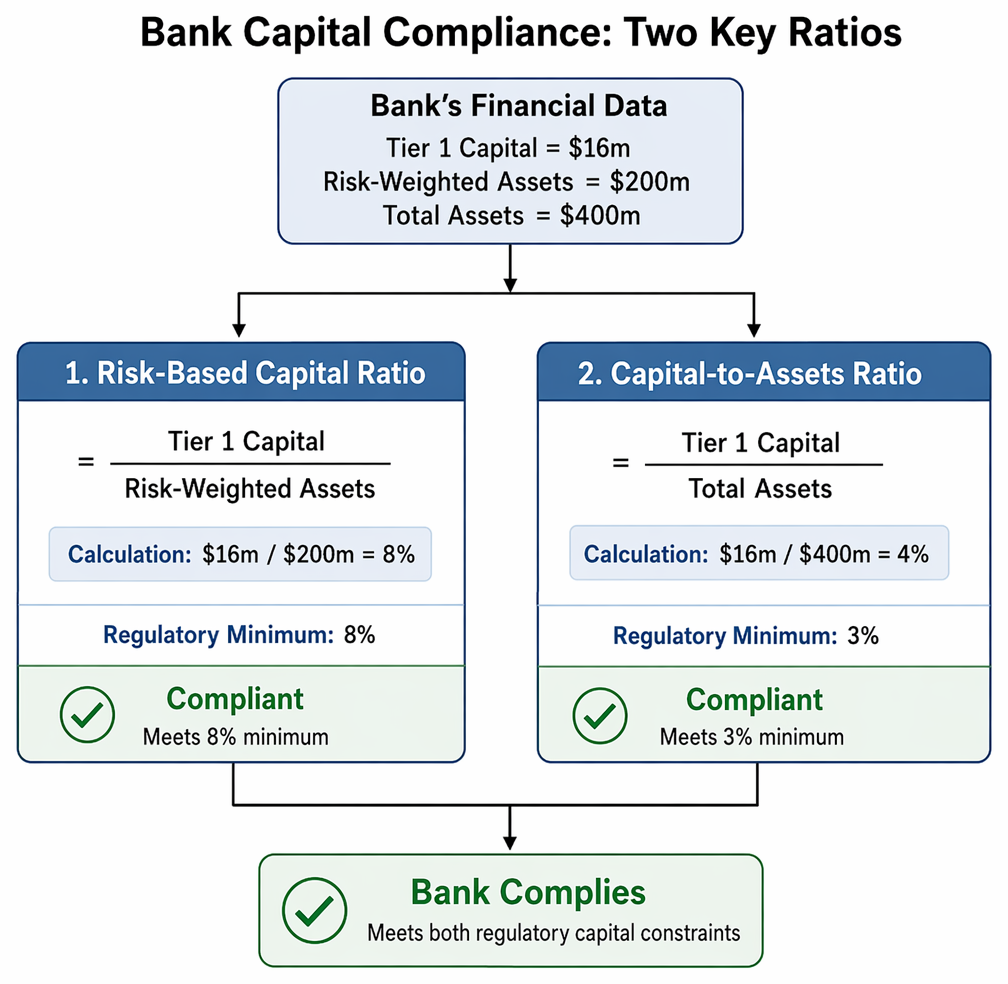

Worked Example 1.1

A bank holds $200 million in risk-weighted assets, of which its Tier 1 capital is $16 million. The regulator requires a minimum Tier 1 capital ratio of 8% and a minimum capital-to-assets ratio of 3%. The bank’s total assets are $400 million.

Question: Is the bank in compliance with both its risk-based and capital-to-assets requirements?

Answer:

- The Tier 1 capital ratio is $16m / $200m = 8%, which meets the 8% minimum.

- The capital-to-assets ratio is $16m / $400m = 4%, above the 3% minimum.

- The bank complies with both constraints.

Exam Warning: For the CFA exam, always distinguish between risk-based and capital-to-assets ratios. In case study problems, be ready to calculate both, using provided values for capital, total assets, and risk-weighted assets.

Regulatory Implications for Investment and Portfolio Management

The interaction of these regulatory constraints has several investment consequences for banks and similar institutions:

- They must ensure sufficient capital for their chosen asset mix, limiting risk concentration and asset growth.

- Asset allocations may favor lower-risk, lower-capital-charge investments over higher-yielding but more capital-intensive ones.

- Liquidity requirements restrict allocations to illiquid or alternative asset classes.

- Borrowing limits and capital ratios cap the size of the balance sheet.

- Investment policies—and risk appetites—must be monitored for compliance and regularly stress-tested. Breaches can result in sanctions or enforced asset sales.

Summary

Regulatory constraints define the investment policy set for banks and similar institutions. Minimum capital requirements, risk-based and capital-to-assets ratios, and liquidity rules govern asset allocation, portfolio risk, and permissible use of debt. For CFA candidates, the exam frequently tests your ability to apply capital adequacy, regulatory capital-to-assets ratio, and investment limit concepts to real-world bank and insurer portfolio scenarios.

Key Point Checklist

This article has covered the following key knowledge points:

- Regulatory capital and borrowing requirements constrain investment policies for banks and institutions.

- Risk-based capital ratios and capital-to-assets ratios operate jointly to limit risk and growth.

- Capital adequacy ratios incentivize prudent risk management and diversification.

- Liquidity coverage ratios restrict allocations to illiquid or high-risk assets.

- Excess borrowing or non-compliance raises operational and enforcement risks.

Key Terms and Concepts

- regulatory capital

- capital-to-assets ratio

- risk-based capital ratio

- capital adequacy ratio

- Basel III