Learning Outcomes

This article explains behavioral portfolio construction in the context of goals-based investing and mental accounting, including:

- How mental accounting leads investors to segment wealth into separate "buckets" and how this segmentation affects risk, return, and diversification at the total portfolio level.

- The distinction between traditional mean–variance optimization and goals-based portfolio construction, with emphasis on how each framework defines risk tolerance and success.

- The structure of goals-based portfolios, including assigning goals, time horizons, required returns, and probabilities of goal attainment to distinct sub-portfolios.

- How to diagnose portfolio inefficiencies created by behavioral biases, and when consolidating or rebalancing segmented accounts can improve alignment with client objectives.

- Practical techniques for articulating trade-offs between competing goals, recommending suitable asset allocations for each goal, and justifying any departures from the mean–variance efficient frontier in exam-style case vignettes.

- How to interpret CFA Level 3 vignette data to identify investor goals, behavioral biases, and appropriate recommendations for revising the IPS and portfolio structure.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand how behavioral biases affect portfolio construction, with a focus on the following syllabus points:

- Identifying the impact of behavioral biases, especially mental accounting, on portfolio design

- Explaining the structure and rationale behind goals-based investing

- Recognizing portfolio segmentation and its effects on risk/return outcomes

- Comparing goals-based to traditional mean–variance optimization

- Applying behavioral finance concepts to real-world portfolio recommendations

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is mental accounting, and how can it affect an investor's asset allocation?

- How does goals-based investing modify the traditional portfolio construction process?

- Give one example of how portfolio segmentation can lead to risk inefficiency.

- Briefly contrast the focus of goals-based investing with that of traditional mean–variance optimization.

Introduction

Investor behavior often departs from the rational, integrated approach assumed by traditional finance. Two central behavioral concepts—mental accounting and goals-based investing—have direct effects on real-world portfolio construction. Understanding their impact allows you to identify investor preferences, how portfolios are segmented, and why clients may resist recommended changes. This article covers the definition and consequences of mental accounting, the format and logic of goals-based investing, and the practical issues for exam scenarios and advice.

Key Term: mental accounting

The behavioral process where individuals treat different sums of money as non-interchangeable, often based on source or intended use, rather than considering overall wealth in aggregate. Key Term: goals-based investing

A portfolio construction approach that divides assets into separate sub-portfolios, each aligned to a distinct client financial goal, with allocation driven by goal-specific time horizon and risk tolerance.

MENTAL ACCOUNTING AND PORTFOLIO SEGMENTATION

Mental accounting is the cognitive bias where investors "bucket" assets by mental categories, for example, retirement funds vs. vacation savings. Rather than optimize across total wealth, each bucket is managed independently—leading to sub-optimal risk/return trade-offs.

How Mental Accounting Alters Investment Decisions

Investors often:

- Segment portfolios by purpose (e.g., "safe money" vs. "opportunity money")

- Invest risk-averse buckets mostly in cash or bonds, while allocating small parts to very high risk, hoping for a "windfall"

- Focus on income generation in some segments, leaving capital unrealized for long periods

This "layered" approach matches the behavioral tendency to avoid losses on essential needs, but also results in inefficient overall diversification and can increase portfolio risk or reduce expected returns.

Worked Example 1.1

Scenario: A client places $700,000 in a "security" bucket (cash and government bonds for essential living expenses) and $300,000 in a "growth" bucket (high-risk equity for aspirational goals). Both buckets are managed without reference to the aggregate portfolio.

Answer:

The client is likely to have an aggregate portfolio risk/return profile that is inconsistent with their stated preferences. Overall return can be lower and risk higher than if the whole portfolio were optimized as a unit. Bucketing by "purpose" leads to missed diversification benefits, which mean the same target wealth could be achieved with less portfolio risk or higher return.

Consequences for Portfolio Construction

- Aggregated portfolios built via mental accounting often fall inside the efficient frontier.

- Sub-bucket allocations may contradict the client's overall risk tolerance.

- Behavioral biases, such as loss aversion, strengthen clients' reluctance to rebalance or consolidate buckets.

Revision Tip: Focus on examples where treating each bucket separately leads to an inefficient total allocation, and be prepared to explain the difference versus a single, optimized portfolio.

GOALS-BASED INVESTING: STRUCTURE AND RATIONALE

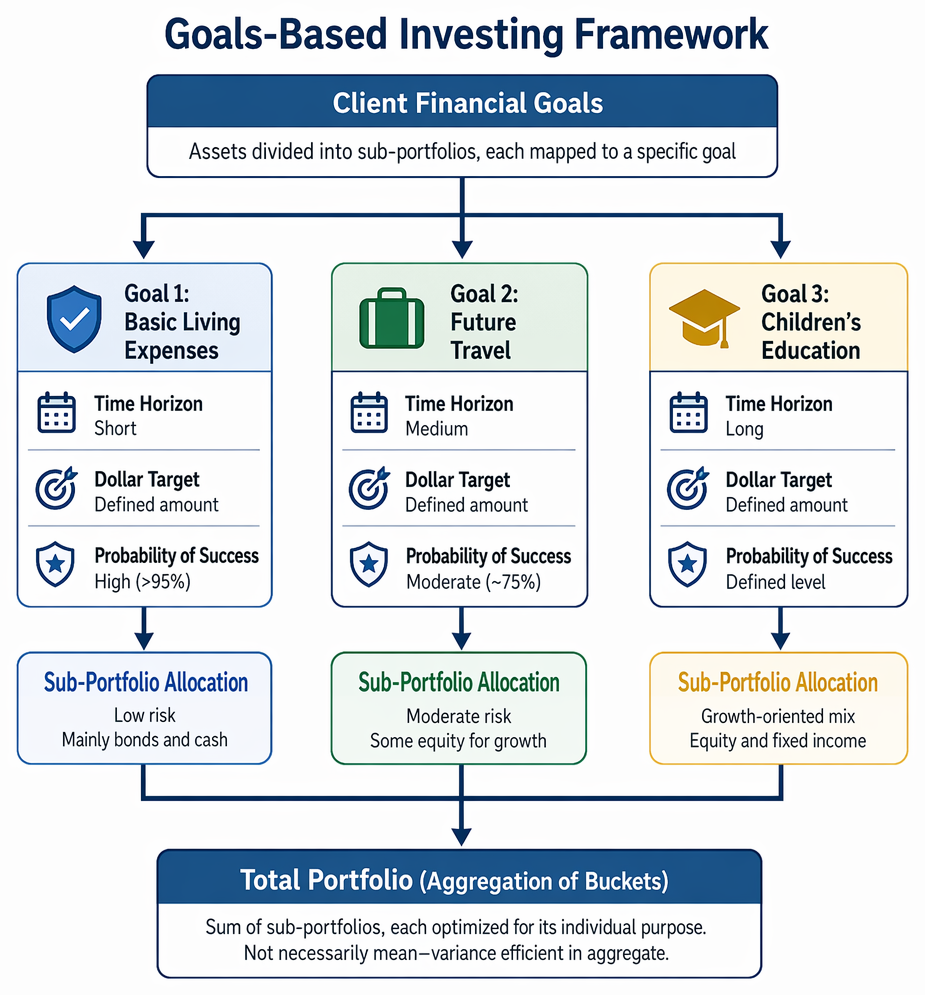

Goals-based investing builds on mental accounting but takes a deliberate approach: assets are divided into sub-portfolios, each mapped to a specific financial objective (e.g., emergency fund, retirement, legacy).

Goals-based portfolio construction proceeds from defining client objectives to allocating goal-specific sub-portfolios, aggregating them, and rebalancing as funding progress changes.

Key features:

- Each goal is assigned a dollar target, time horizon, and minimum probability of success.

- Asset allocation for each goal is determined by its required return, acceptable risk, and time horizon.

- The aggregation of all sub-portfolios forms the client's overall portfolio, but each is optimized for its individual purpose.

Key Term: probability of goal attainment

In goals-based investing, the likelihood, based on portfolio modeling, that assets allocated to a goal are sufficient to meet or exceed that goal with an acceptable level of risk.

Comparison with Traditional Portfolio Construction

Traditional mean–variance optimization seeks the most efficient total portfolio based on total wealth, an overall risk tolerance, and return target. Goals-based investing instead:

- Seeks to maximize the likelihood of meeting each major financial goal

- Accepts some overall portfolio inefficiency in exchange for client-specific psychological comfort and improved client engagement

- Encourages acceptance of investment risk for growth through aspiration-oriented buckets, while prioritizing safety for essential needs

Worked Example 1.2

Scenario: A client identifies three primary goals—(1) basic living expenses, (2) future travel, and (3) providing for children’s education. Each is assigned a time horizon and confidence level.

Answer:

Each goal's sub-portfolio is constructed independently:

- Living expenses: high probability of success (>95%), low risk, mainly bonds and cash

- Travel: moderate confidence (~75%), some equity for growth, small allocation

- Education: goal cost, time horizon, and probability of success determine a mix of equity and fixed income The total portfolio is a sum of these buckets, each with its own optimal mix, but not necessarily "mean–variance efficient" in aggregate.

Exam Warning: Goals-based portfolios often aggregate to allocations that are less efficient than those from a single-portfolio optimization. Do not fall into the trap of believing goals-based methods always maximize total wealth; they align allocations with the client’s willingness to take on risk per goal, not globally.

PRACTICAL IMPLICATIONS FOR CFA EXAM SCENARIOS

On the CFA exam, you will need to:

- Identify instances of mental accounting and describe how it affects the client’s current or proposed portfolio.

- Recommend actions: consolidate segmented accounts, encourage aggregated analysis, or optimize by overall risk and return where appropriate.

- Be able to explain why goals-based investing "works" for certain clients: it structures and communicates risk in a more psychologically acceptable way, increases client buy-in, and can help prevent panic selling or risky behavior at inopportune times.

- Recognize limitations: goals-based approaches can reduce overall efficiency; may require client education when trade-offs between goals are needed.

Summary

Behavioral portfolio construction, shaped by mental accounting and goals-based investing, leads investors to segment their wealth into separate buckets corresponding to different objectives. This segmentation can create portfolio inefficiencies, but also increases psychological comfort and client engagement. Goals-based investing constructs sub-portfolios for each client goal, prioritizing probability of attainment for essential needs and reducing the emotional burden of risk. This approach differs from traditional, integrated portfolio optimization, and CFA exam questions will require you to recognize both the benefits and limitations in practical recommendations.

Key Point Checklist

This article has covered the following key knowledge points:

- Mental accounting leads investors to treat different assets separately by purpose, affecting risk and return

- Portfolio segmentation can reduce diversification and decrease efficiency versus integrated optimization

- Goals-based investing structures portfolios by aligning sub-portfolios to specific objectives and assigns asset allocation separately for each

- Probability of goal attainment guides risk tolerance for each sub-portfolio in goals-based frameworks

- Goals-based portfolios often are less efficient when viewed as a whole, but improve client alignment and communication

- For the CFA exam, identify and evaluate mental accounting and segmentation, and be ready to advise on behavioral and traditional approaches as required

Key Terms and Concepts

- mental accounting

- goals-based investing

- probability of goal attainment