Learning Outcomes

This article explains behavioral portfolio construction and heuristic-driven asset allocation, including:

- defining key investor heuristics such as naive diversification (1/N), status quo bias, anchoring, framing, mental accounting, and home bias in the context of portfolio decisions

- distinguishing how these heuristics differ from fully rational, optimization-based asset allocation frameworks

- analyzing how rules of thumb and mental shortcuts influence strategic and tactical asset allocation, diversification choices, and risk exposures

- evaluating the portfolio-level consequences of naive diversification across fund menus with different fundamental risk and correlation characteristics

- assessing how status quo bias and framing effects affect rebalancing discipline, risk perception, and willingness to realize losses

- examining how mental accounting and familiarity preferences can create fragmented sub-portfolios and concentrated home-market exposures

- identifying exam-style scenarios in which heuristic-driven behavior leads to sub-optimal allocations or hidden concentrations relative to investor objectives and constraints

- formulating practical, exam-relevant recommendations—such as structured decision processes, periodic reviews, and scenario analysis—to mitigate heuristic-driven errors and realign portfolios with rational risk–return trade-offs

- relating heuristic-driven allocations to asset-only, liability‑relative, and goals‑based frameworks in order to evaluate client behavior in a Level 3 exam setting

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand how investors’ use of heuristics—rules of thumb and mental shortcuts—impacts the asset allocation process and portfolio outcomes, with a focus on the following syllabus points:

- Explain common heuristics (such as 1/N, status quo, and framing) and their roles in investor decision-making for portfolio construction

- Assess implications of heuristic-driven behaviors for diversification and rebalancing

- Evaluate the effects of behavioral heuristics on asset allocation, including bias towards home market and naive diversification

- Distinguish between cognitive and emotional influences in asset class allocation

- Recommend strategies for mitigating sub‑optimal asset allocation outcomes caused by heuristics

- Contrast heuristic-driven allocations with asset-only, liability-relative, and goals-based asset allocation approaches

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

A defined contribution plan offers eight funds: six equity funds and two bond funds. A participant uses the 1/N rule. Which statement best describes the likely outcome?

- a) The participant will hold an efficient mix because equal weights always minimize risk for a given return.

- b) The participant will unintentionally take a high equity risk exposure driven by the fund menu.

- c) The participant will underweight equities relative to a global market-capitalization benchmark.

- d) The participant will achieve a liability-relative allocation aligned with retirement needs.

-

An investor insists on maintaining a 60/40 stock/bond allocation “because that has always worked historically,” despite a substantial decline in real bond yields and an extension of her retirement horizon. Which heuristic is most evident, and what is the main risk?

- a) Framing; excessive trading driven by short-term performance comparisons.

- b) Anchoring; misalignment between portfolio risk/return and current objectives.

- c) Mental accounting; excessive focus on income rather than total return.

- d) Status quo bias; over-diversification across too many asset classes.

-

A client views her portfolio in two buckets: one “safe” account for capital preservation and one “growth” account for long-term wealth, with no consideration of how the buckets interact. Which portfolio-level risk is most likely?

- a) Over-hedging inflation risk because both buckets hold inflation-indexed bonds.

- b) Double-counting liquidity because both buckets are invested in illiquid assets.

- c) Inefficient total risk exposure because correlations across buckets are ignored.

- d) Excessive currency risk because each bucket is globally diversified.

-

An investor holds 95% of her equity allocation in domestic stocks, arguing that “I understand my home market best.” Which adviser response is most consistent with exam-relevant best practice to address this behavior?

- a) Emphasize the lower transaction costs of home-market investing and accept the bias.

- b) Recommend switching entirely to global equities to eliminate country-specific risk.

- c) Use scenario and historical analysis to demonstrate diversification benefits of global equities and propose gradual rebalancing.

- d) Encourage market-timing decisions in foreign markets to offset the home bias.

Introduction

Behavioral portfolio construction recognizes that many investors do not follow a strictly rational, quantitative framework for asset allocation. Instead, real-world decisions are shaped by heuristics—mental shortcuts and simple rules of thumb—that help investors simplify complex choices but can also introduce systematic errors and inefficiencies into the portfolio construction process. For CFA candidates, understanding the link between common heuristics and sub-optimal asset allocation is critical, both when evaluating client behavior and constructing robust strategic and tactical allocations.

Heuristic-driven behavior should be contrasted with normative asset allocation approaches examined at Level 3—such as mean–variance optimization (MVO) in an asset‑only setting, liability‑relative allocation for institutions, and goals‑based allocation for individuals. Those frameworks explicitly model risk, return, correlations, and sometimes liabilities or goals. Heuristics, by contrast, often ignore one or more of these inputs and rely on simple rules like “equal weight everything” or “age equals bond percentage.” On the exam, you are frequently asked to identify where a client is following such rules, diagnose the consequences at the portfolio level, and recommend corrective actions consistent with the IPS and the appropriate allocation framework.

Key Term: heuristic

A mental shortcut or rule of thumb used to simplify decision-making under uncertainty. Heuristics can help investors make quick choices but often lead to predictable errors or biases in complex financial settings.

Heuristics and Portfolio Construction

Investor heuristics affect key asset allocation and portfolio construction decisions. These effects are especially prominent in environments where information is difficult to interpret, uncertainty is high, or the calculation of optimal allocations is cognitively demanding. The most commonly observed heuristics with portfolio-level impact include naive diversification (the "1/N" rule), the status quo bias, anchoring, framing, mental accounting, and familiarity.

From a curriculum standpoint, it is useful to see these heuristics as sitting on a spectrum:

- At one end, fully model-based approaches (MVO, factor-based allocation, risk budgeting) explicitly use estimates of expected returns, volatilities, and correlations.

- In the middle, more structured but simplified rule-based approaches (such as risk parity) use some risk information but ignore expected returns.

- At the other end, “pure” heuristics (such as 1/N or 60/40 for all investors) ignore both detailed risk characteristics and individual circumstances.

The exam often asks you to evaluate where on this spectrum a client’s behavior lies and whether the resulting allocation is defensible given objectives and constraints.

Naive Diversification (The "1/N" Rule")

Many investors fall back on the simple rule of allocating equal proportions across all available asset classes or choices, regardless of the relative risk, return, or correlation properties.

Key Term: naive diversification

Allocating assets equally across available choices (e.g., each of N funds receives 1/N of the total), without analysis of risk, return, or diversification.

This behavior is commonly observed in defined contribution (DC) plans and superannuation schemes: when faced with a list of funds, participants frequently split contributions equally across options. Behavioral research suggests they do this because:

- they lack the time or ability to analyze detailed risk–return characteristics

- equal weighting feels “fair” and diversified

- they misinterpret diversification as “owning a bit of everything” rather than managing correlated risks

In practice, the resulting allocation can be very far from what a rational optimization would recommend, especially when the menu is unbalanced across asset classes (more equity options than bond options, or vice versa).

Implications for Asset Allocation

Naive diversification often leads to sub-optimal risk/return profiles as investors overlook important differences between options. The effective economic exposure is driven as much by the menu design as by investor preferences. If a DC plan offers:

- three equity funds and two bond funds, the 1/N rule yields an equity weight of

- four equity funds and two bond funds, the same heuristic yields in equities

The investor’s equity risk changes dramatically even though their “strategy” (equal weighting) is unchanged. This undermines the link between the investor’s risk tolerance and the portfolio’s actual risk.

Moreover, equal weighting ignores differing volatilities and correlations:

- High-volatility funds (e.g., emerging market equities) receive the same weight as low-volatility funds (e.g., short-term bond funds), so they dominate portfolio risk.

- Highly correlated funds (e.g., multiple domestic equity style funds) are treated as if they provide independent diversification benefits.

From an exam standpoint, you should be able to:

- identify when an equal-weight allocation is driving unintended risk (e.g., too much equity, credit, or illiquidity exposure)

- compare it to a more rational benchmark (e.g., a global market-capitalization allocation or an MVO-derived mix)

- explain whether 1/N is particularly harmful or relatively benign in a given context (for example, equal weighting across very similar index funds within one asset class may be less problematic than across very different asset classes)

Rules-Based Risk Approaches Versus Heuristics

The curriculum also introduces risk-based allocation methods such as risk parity. These are not heuristics in the behavioral sense, but they are rule-based and omit expected return estimates.

A simple risk parity framework aims to allocate portfolio weights such that each asset contributes equally to total portfolio variance:

where:

- = weight of asset

- = covariance of asset with the portfolio

- = number of assets

- = portfolio variance

Risk parity uses risk and correlation information but ignores expected returns. Naive 1/N ignores both risk and return. MVO uses both. On the exam, you may need to:

- contrast a 1/N allocation with a risk parity allocation and an MVO allocation

- note that both 1/N and risk parity are highly sensitive to the definition of the opportunity set (for 1/N, how many funds of each type are offered; for risk parity, which asset classes or factors are included)

- argue which approach is more appropriate for a particular client given their sophistication and objectives

Status Quo, Framing, and Anchoring

Status Quo Bias

Status quo bias causes investors to stick with existing allocations or default choices, even when circumstances change or new information is presented. This often results in portfolios that are outdated or misaligned with goals, risk tolerance, or current market conditions.

Key Term: status quo bias

The preference to maintain the current allocation or default setting, avoiding change even when better alternatives are available.

Examples include:

- DC plan participants remaining in the default fund long after it ceases to be appropriate for their age or circumstances.

- Private clients failing to adjust their equity exposure after major changes in wealth, employment risk, or spending needs.

- Institutional committees delaying necessary de-risking of a maturing defined benefit plan because changing policy is uncomfortable.

Rational asset allocation practice, as outlined in the curriculum, calls for periodic review of the strategic asset allocation when goals, constraints, or beliefs change (for example, when a university’s spending policy or a pension plan’s funded status shifts). Status quo bias is directly at odds with this discipline.

Framing Effects

How investment questions or information are presented (framed) can affect investor choices and tolerance for risk. Investors might respond very differently to:

- “This allocation has a 90% chance of meeting your retirement income target” versus

- “There is a 10% chance you will fall short of your retirement income target”

Even though the probabilities are identical, the loss-framed version typically induces greater risk aversion.

Key Term: framing

The influence of the way choices, returns, or risks are presented on investor decision-making and asset allocation choices.

Framing matters for:

- Perceived diversification: Presenting asset allocation as a list of funds rather than risk-factor exposure can obscure concentration (e.g., several domestic equity funds appearing as “diversified”).

- Rebalancing decisions: Focusing on realized losses in a single asset class can discourage selling losers to rebalance, even when the total portfolio risk has increased.

- Goals-based investing: Describing outcomes in terms of probabilities of meeting specific goals (education funding, essential retirement spending) may be more intuitive than presenting an abstract efficient frontier.

On the exam, be ready to point out when an adviser’s presentation of risk (shortfall probabilities, maximum drawdown, or volatility) is likely to trigger excessive conservatism or risk seeking due to framing.

Anchoring

Anchoring in portfolio construction refers to the tendency of investors to rely heavily on initial values, such as the purchase price of a security, a historical allocation (e.g., 60/40), or a popular age-based rule, and to adjust insufficiently when new data are presented.

Key Term: anchoring

Relying too heavily on an initial value or reference point (anchor) in decision-making, which may lead to biased asset allocation.

In asset allocation, common anchors include:

- traditional “balanced” allocations such as 60/40, treated as universally appropriate

- simple life-cycle rules like “age in bonds” or “120 minus age in equities”

- a prior peak portfolio value, which becomes the reference for acceptable losses

Anchoring becomes problematic when key conditions change:

- Bond yields falling to historically low levels may make a 60/40 allocation much less attractive for a retiree than in the past.

- Increased longevity risk may make “age in bonds” too conservative for a healthy investor expected to live well into their 90s.

- A portfolio that has doubled in value may justify taking some risk off the table, but investors anchored to the peak may resist any drawdown.

The curriculum stresses evaluating allocations against current objectives, constraints, and capital market expectations, not historical anchors.

Mental Accounting and Home Bias

Mental accounting leads investors to separate their wealth into distinct "buckets"—each with unique risk preferences and time horizons, such as treating retirement savings differently from other investments. This separateness can result in inefficient, non-optimal aggregate portfolios.

Key Term: mental accounting

Treating different pools of money as non-substitutable sub-portfolios, with distinct objectives and constraints for each, rather than optimizing at the total portfolio level.

Examples include:

- maintaining a “never touch” capital preservation account invested only in cash, while taking very high equity risk in a speculative account

- managing taxable and tax-deferred accounts independently, with inconsistent asset allocations

- failing to integrate human capital (future labor income) and defined benefit pension entitlements into the overall risk picture

The curriculum’s goals-based asset allocation framework can be seen as a disciplined, rational evolution of mental accounting. Goals-based investing intentionally creates sub-portfolios aligned with specific goals, each with its own time horizon and required probability of success. The key difference is that the adviser explicitly models risk, return, and correlations within and across goal “layers,” whereas naive mental accounting ignores those interactions.

Additionally, the use of heuristics and preference for the familiar often translates into a home bias, where investors disproportionately allocate to domestic equities or bonds, missing out on potential diversification benefits.

Key Term: home bias

Overweighting investments in domestic (home market) assets relative to their weight in the global opportunity set. Key Term: familiarity bias

A preference for investments that feel familiar or well-known (such as domestic assets or employer stock), often leading to under-diversification and concentrated risk.

Home bias may arise from:

- perceived informational advantage in local markets

- regulatory or tax incentives favoring domestic holdings

- discomfort with currency risk or foreign political risk

However, from a total-portfolio standpoint, excessive home bias concentrates country, sector, and currency risk and reduces the benefits of low correlations across regions.

Behavioral Heuristics and Diversification

Behavioral heuristics interact strongly with diversification decisions. Rather than deliberately constructing a diversified portfolio across risk factors, regions, and asset classes, investors often:

- treat each fund choice independently (1/N heuristic)

- focus on the number of holdings rather than the actual correlations

- segment assets into mental accounts, ignoring cross-account diversification

- stay close to the status quo allocation, allowing market movements to drive risk

Worked Example 1.1

An investor is presented with a defined contribution plan offering six funds: three equity and three bond funds. The investor uses a 1/N allocation rule, investing equally across all six funds. What are the likely consequences for risk and return?

Answer:

The investor will have a 50% allocation to equities simply due to the structure of available choices, not as a result of a deliberate risk/return analysis. If the menu had four equity and two bond funds, the same heuristic would produce 67% equity exposure. This demonstrates how fund menu design and naive diversification can affect portfolio outcomes without the investor's awareness. On the exam, you should note that:

- the effective risk level is driven by the plan’s menu, not the investor’s stated risk tolerance

- the allocation ignores differences in volatility and correlation across funds

- a simple change in the opportunity set could materially alter the investor’s total risk, even with unchanged behavior

Worked Example 1.2

A client insists on keeping 100% of their equity allocation in their home country's stock market, citing "familiarity." What is the potential risk, and how can the adviser address this bias?

Answer:

Concentrating equity holdings in the home market increases exposure to country-specific risks (economic, political, currency, and regulatory) and potentially reduces risk-adjusted returns through lack of global diversification. The portfolio may also be overly exposed to the client’s employment and human capital risk if their job is tied to the home economy. An adviser can:

- use education and scenario analysis to show historical periods when the home market underperformed global equities

- demonstrate how adding even a modest allocation to non-domestic equities can reduce volatility for a given expected return

- propose phased rebalancing (e.g., gradually increasing foreign exposure over several years) to make the change more acceptable

For exam answers, emphasize both diversification benefits and practical, incremental implementation.

Worked Example 1.3

A retiree uses the "age-in-bonds" heuristic (allocating 65% to bonds at age 65) as the main allocation rule. If the individual's risk tolerance, goals, or market conditions change, what is the risk of relying on this rule?

Answer:

The portfolio's risk/return profile may no longer align with the investor's actual needs or circumstances. Such rules-of-thumb ignore:

- individual preferences and risk capacity (for example, guaranteed pension income may justify more equity exposure than “age-in-bonds” implies)

- life expectancy and longevity risk, which may require maintaining substantial growth assets beyond age 65

- the market environment (for example, extremely low real bond yields may make a high bond allocation insufficient to meet spending goals)

While age-based rules capture the idea that human capital (a bond-like asset) declines over time, a goals-based or liability-relative analysis provides a more tailored allocation than a single heuristic.

Worked Example 1.4

A client holds two accounts: a “safe” cash account for emergencies and a “growth” account invested 100% in equities. She sees no reason to rebalance because “the safe account will never be touched.” How might mental accounting affect her total risk, and what could an adviser recommend?

Answer:

By viewing the accounts in isolation, the client underestimates her total equity risk. If both accounts ultimately fund the same set of goals (retirement and lifestyle), the total portfolio may be more aggressive than appropriate. The “safe” bucket is small relative to the growth bucket, so overall volatility is high. An adviser could:

- present a consolidated balance sheet and show the total equity percentage

- map the accounts to specific goals with explicit required probabilities of success, as in goals-based investing

- recommend reallocating some equity risk to fixed income within the growth account to achieve an appropriate overall risk level while maintaining an emergency cash reserve

Implications for Rebalancing and Risk Management

Heuristics can also lead to avoidance or delay of rebalancing. Many investors fail to rebalance due to inertia or status quo bias, resulting in allocations that drift from targets and expose the portfolio to unintended risk concentrations. This is particularly acute after strong equity markets, when equities become a larger share of the portfolio and downside risk increases.

Framing plays a role: when rebalancing is framed as “selling winners” and “realizing losses,” investors may resist executing trades even when they understand the logic of returning to target weights. This interacts with another behavioral phenomenon:

Key Term: disposition effect

The tendency for investors to sell assets that have appreciated (“winners”) too quickly and hold assets that have depreciated (“losers”) too long, relative to a rational strategy.

When risk is framed primarily in terms of realized loss rather than overall portfolio volatility or probability of shortfall, clients may:

- refuse to sell underperforming assets to rebalance into better opportunities

- hold concentrated positions in legacy winners (e.g., employer stock) that no longer fit the IPS

- avoid de-risking near retirement because it would require selling appreciated positions

From a process standpoint, the curriculum emphasizes:

- Time-based rebalancing: rebalancing at fixed intervals (e.g., quarterly or annually), which can help overcome status quo bias by institutionalizing review points.

- Threshold-based rebalancing: rebalancing when asset class weights deviate from target by a specified corridor. Here, behavioral issues can lead to clients overriding the rule when it would force uncomfortable trades.

Exam questions may ask you to:

- evaluate a rebalancing policy in the presence of taxes, transaction costs, and behavioral tendencies

- explain how wider corridors might reduce transaction costs but increase the risk of behavioral drift

- recommend how an IPS and pre-specified rules can be used to counteract status quo and disposition effects

Exam Warning: Over-reliance on simple rules (such as 1/N or "60/40") may mask hidden concentration, risk mismatches, or lead to signals that are out of step with market changes or personal goals. CFA exam questions may test the ability to evaluate these heuristics or identify when they produce sub-optimal results. Pay particular attention to:

- how menu design interacts with 1/N behavior in DC plans

- whether a “classic” 60/40 or age-based rule is still appropriate given updated capital market expectations and client circumstances

- whether mental accounting is leading a client to ignore cross-account or cross-goal diversification

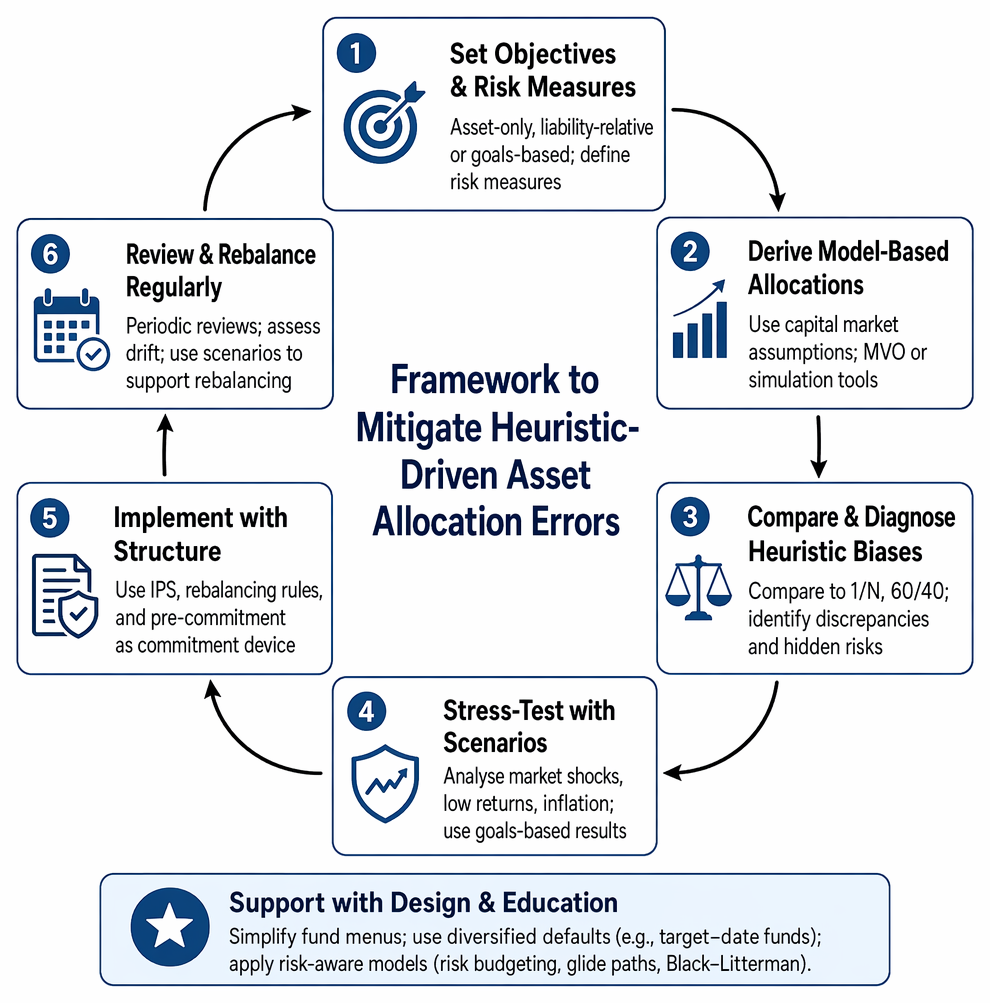

Mitigating Heuristic-Driven Asset Allocation Errors

Advisers and sophisticated investors can reduce the impact of behavioral heuristics in asset allocation and portfolio construction through structured processes that make rational choices easier to implement and maintain.

Equal-weight allocation across offered funds causes equity weight to mirror the proportion of equity options, creating unintended risk concentrations.

Key techniques include:

-

Structured decision processes:

- Start from clearly articulated objectives (asset-only, liability-relative, or goals-based) and risk measures (volatility, probability of shortfall, surplus volatility).

- Use capital market assumptions and, where appropriate, MVO or simulation-based tools to derive candidate allocations.

- Compare heuristic-based allocations (1/N, 60/40) to model-based allocations to highlight discrepancies and hidden risks.

-

Investment policy statements (IPSs) and pre-commitment:

- Formalize strategic asset allocation, rebalancing rules, and conditions for revisiting the allocation (changes in goals, constraints, or beliefs).

- Use the IPS as a commitment device to counteract status quo and disposition effects during periods of market stress.

-

Periodic portfolio reviews and rebalancing:

- Schedule regular reviews (e.g., annually) to assess whether the strategic allocation remains appropriate and whether drift has become significant.

- Where clients resist rebalancing, use scenario analysis to show how unrebalanced portfolios would have performed in adverse historical periods (e.g., equity market crashes).

-

Scenario analysis and education around diversification:

- Simulate outcomes for portfolios with and without home bias, naive diversification, or concentrated legacy positions.

- Present results in terms of probabilities of meeting specific goals (goals-based framing) to make risk more tangible.

- Stress-test allocations under different market environments (e.g., low-return scenarios, inflation shocks) to challenge over-reliance on historical rules of thumb.

-

Menu and product design (especially for DC plans):

- Simplify fund menus to reduce naive 1/N behavior across highly correlated options.

- Use well-diversified default options (such as appropriately designed target-date funds) that embed rational life-cycle principles rather than simple age rules.

- Consider white-labelled or multi-asset funds that reduce the temptation to “own a bit of everything” at the fund level.

-

Use of robust, simplified models rather than pure heuristics:

- For clients unwilling or unable to engage with full MVO, consider rule-based but risk-aware approaches (e.g., risk budgeting, simple glide paths informed by human capital considerations) instead of pure 1/N or fixed 60/40 allocations.

- Employ Bayesian or Black–Litterman frameworks to anchor on market-capitalization weights and adjust for client-specific views, thereby avoiding extreme allocations that may trigger behavioral resistance.

Worked Example 1.5

A 45-year-old executive has:

- a large position in her employer’s stock in a taxable account

- a DC plan where she splits contributions 1/N across all available funds

- a strong home bias in both accounts

You are asked to recommend changes to improve her asset allocation while recognizing likely behavioral barriers.

Answer:

Key behavioral issues include: Naive diversification in the DC plan. Familiarity bias and home bias in equity exposure. Potential overconfidence and loyalty bias in the concentrated employer stock position. A practical, exam-appropriate recommendation would: Consolidate DC holdings into a smaller number of broadly diversified, global equity and bond funds or a suitable target-date fund, reducing the scope for harmful 1/N behavior. Gradually reduce the employer stock position via a pre-agreed plan (e.g., selling a set percentage each year), reallocating proceeds into diversified global funds to mitigate single-stock and home-country risk. Use scenario analysis to demonstrate the impact on wealth if the employer’s stock or the home market underperforms, framing changes as risk reduction rather than speculation. The answer should explicitly note how these steps realign the portfolio with her risk tolerance and long-term objectives while respecting likely emotional resistance to abrupt change.Revision Tip: When evaluating a client's portfolio construction, always check for equal weighting, default allocations, or heavy reliance on market "rules of thumb"—hallmarks of heuristic-driven choices. Then link your assessment to the appropriate allocation framework (asset-only, liability-relative, or goals-based) as required by the case.

Summary

Behavioral heuristics such as naive diversification, status quo bias, framing, and anchoring frequently shape investor decisions during portfolio construction and asset allocation. These rules of thumb offer simplicity but may result in sub-optimal diversification, excessive home bias, failure to rebalance, or misalignment with investor goals and risk tolerance.

For CFA Level 3, it is not enough to recognize a bias; you must:

- evaluate its portfolio-level consequences in terms of risk, return, and goal attainment

- compare heuristic-driven allocations to those implied by rational frameworks (MVO, liability-relative, goals-based)

- recommend realistic, process-based interventions—IPS design, structured rebalancing, menu simplification, and scenario analysis—to mitigate errors

By systematically identifying and addressing heuristic-driven behavior, advisers can move asset allocation outcomes closer to the rational, quantitative standards emphasized in the curriculum while acknowledging real-world behavioral constraints.

Key Point Checklist

This article has covered the following key knowledge points:

- Heuristics are mental shortcuts that frequently shape asset allocation decisions and often substitute for full optimization.

- Naive diversification (the 1/N rule) often leads to suboptimal diversification in practice, with risk determined by menu design rather than investor preferences.

- Status quo and framing effects strengthen inertia and influence risk perception during allocation and rebalancing, contributing to drift and disposition effects.

- Anchoring to historical allocations or popular rules of thumb can prevent necessary adjustments when goals, constraints, or market conditions change.

- Mental accounting and familiarity bias can embed unexamined risk exposures—such as concentrated home-market or employer-stock positions—in portfolio construction.

- Home bias arises from familiarity, regulatory, and informational factors, reducing global diversification and increasing country-specific risk.

- Mitigating behavioral heuristics involves structured decision processes, clear IPSs, scenario analysis, periodic reviews, and investor education on diversification and risk.

- Exam answers should explicitly connect heuristic-driven behavior to asset-only, liability-relative, or goals-based frameworks and provide concrete, implementable recommendations.

Key Terms and Concepts

- heuristic

- naive diversification

- status quo bias

- framing

- anchoring

- mental accounting

- home bias

- familiarity bias

- disposition effect