Learning Outcomes

This article explains how behavioral biases—specifically risk perception, loss aversion, and framing—affect portfolio construction, investor risk assessment, and trading behavior in the CFA Level 3 context. It clarifies the distinction between objective risk and perceived risk, showing how changing market conditions, recent returns, and emotional responses can distort stated risk tolerance and lead to inconsistent investment choices. It details how loss aversion drives holding losers too long, selling winners prematurely, resisting rebalancing, and taking excess risk after losses, and links these behaviors to common exam vignette patterns. It discusses framing bias in client communication, risk-tolerance questionnaires, and performance reporting, emphasizing how alternative presentations of identical information can generate different recommendations or client decisions. It highlights practical techniques candidates should be able to recommend, including structured discovery of true risk capacity, multi-frame presentation of risk statistics, disciplined rebalancing rules, and client education about behavioral traps. It also reinforces how to interpret and answer CFA-style questions that test for these biases, focusing on identifying the specific bias, explaining its portfolio impact, and justifying appropriate mitigation strategies.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand how behavioral biases impact both the process and outcomes of investment decisions, with a focus on the following syllabus points:

- Identify and describe risk perception, loss aversion, and framing bias in the context of portfolio construction.

- Assess the effects of these biases on asset allocation and investment policy.

- Recommend mitigation techniques for behavioral biases during portfolio development.

- Evaluate how client risk preferences and stated tolerance may be distorted by framing or loss aversion.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Explain the concept of loss aversion and describe how it can affect portfolio rebalancing decisions.

- How can the framing of risk tolerance questionnaire questions influence a client's perceived willingness to take risk?

- Provide an example of how risk perception and actual risk tolerance may diverge in the context of a market downturn.

- What is one practical strategy for mitigating the influence of framing bias during investment policy statement development?

Introduction

Behavioral portfolio construction recognizes that actual investor decisions often deviate from those predicted by classical finance theory. Core behavioral biases—including risk perception, loss aversion, and framing—can lead portfolio strategies away from optimal allocations. For CFA candidates, understanding the effect of these biases is essential for building robust, client-appropriate portfolios and for exam performance.

Key Term: loss aversion

The tendency for individuals to strongly prefer avoiding losses to acquiring gains, leading to risk-averse choices when considering gains and risk-seeking behavior with losses. Key Term: risk perception

The subjective assessment an investor has about the riskiness of an investment or portfolio, often shaped by recent experience, emotions, and context, rather than by objective analysis. Key Term: framing bias

A cognitive bias where the way information or questions are presented shapes decisions and risk assessments, even when the fundamental facts are unchanged.

Behavioral Biases in Portfolio Construction

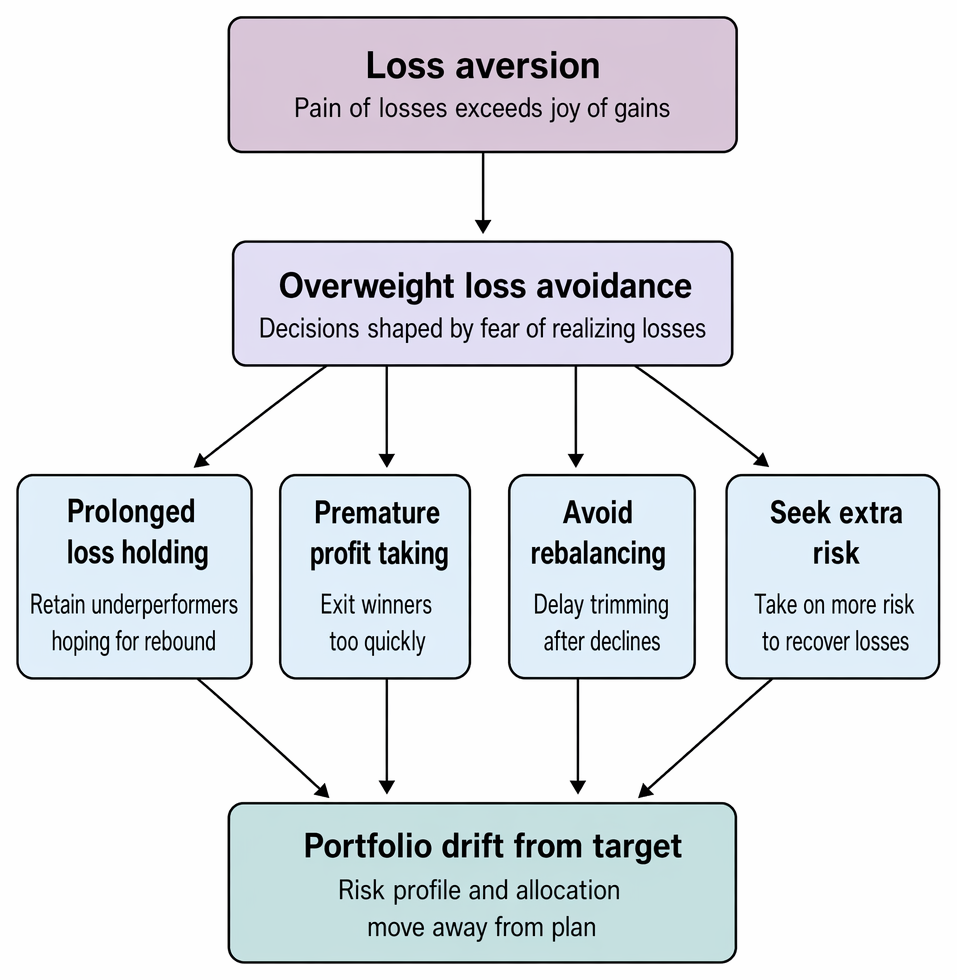

Loss-averse behavior causes investors to retain losing positions, realize gains early, resist rebalancing after declines, and increase risk, misaligning allocations.

Risk Perception Versus Objective Risk

Investors' perception of risk can differ significantly from measurable portfolio volatility. Recent market shocks or vivid losses often lead to overestimation of downside risk, while long bull markets can lower perceived risk and encourage overconfidence.

Loss aversion compounds these perception errors: the pain of a loss is psychologically greater than an equivalent gain. As a result, investors may avoid selling loss-making positions or may demand a high risk premium to accept downside risk, distorting asset allocation.

Exam Warning: CFA questions often test the difference between actual risk tolerance and perceived risk—ensure you do not equate short-term survey responses with long-term strategic risk capacity.

Loss Aversion and Its Investment Consequences

Loss aversion is central in behavioral finance and is consistently observed in both retail and institutional investors. It causes several measurable distortions:

- Holding losing investments too long, hoping for a recovery.

- Selling winners quickly to "lock in" gains.

- Higher propensity to take on risk to recover losses than to pursue new gains.

- Reluctance to rebalance away from positions that have declined below cost basis.

Revision Tip: When constructing or reviewing a portfolio, always consider if the client is "anchoring" to purchase prices and resisting necessary rebalancing due to loss aversion.

Framing Bias: Risk Tolerance and Suitability

How information is presented directly shapes risk assessment. For example, describing a portfolio as "having a 10% chance of loss" evokes a different response than saying "90% chance of gains," regardless of the actual statistics.

Framing bias can manifest in several portfolio construction steps:

- Questionnaire results vary if options are presented as gains versus losses.

- Investors may overestimate risk if shown worst-case scenarios without context.

- Recommendations can be accepted or rejected based solely on the positive or negative wording in suitability reports.

Worked Example 1.1

An advisor presents two asset allocation options to a client: Portfolio X: "95% chance your wealth remains above 80% of initial value." Portfolio Y: "5% chance your wealth declines below 80% of initial value." The client chooses Portfolio X as "safer" despite both being identical. Why?

Answer:

The advisor has presented the same investment using different frames. The positive frame (Portfolio X) induces more risk aversion, while the negative frame (Portfolio Y) triggers a more cautious response due to loss aversion and the salience of potential loss.

Worked Example 1.2

Question: A client is reluctant to sell a large holding in Company Z at a loss, insisting on waiting for a break-even price. Is this rational? What behavioral principle is at play?

Answer:

This is classic loss aversion. Holding the losing position to avoid "realizing" a loss leads to sub-optimal risk, increasing the chance of further loss if fundamentals remain weak. The desire to wait for break-even is not rational from a risk-return or expected utility standpoint.

Worked Example 1.3

Question: During a bull market, a new investor rates her risk tolerance as "high" after seeing multi-year gains. After a 20% portfolio loss, she suddenly becomes risk-averse and demands a move to cash. What explains this shift?

Answer:

Risk perception is context-dependent and prone to framing bias. The investor's subjective view of risk changed in response to recent losses, revealing the effect of framing and loss aversion—her true long-term risk capacity likely did not change, but short-term emotions dominated.

Strategies to Mitigate the Effects of Biases

- Use both quantitative and qualitative risk assessments. Regularly revisit risk tolerance in calm, not volatile, conditions.

- Present portfolio risk and return data in multiple frames (absolute, percentage loss/gain, probability, and time horizon) to allow for more objective decisions.

- Educate clients (and committees) about behavioral traps such as framing and loss aversion.

- Encourage pre-commitment to rebalancing rules to reduce emotional, loss-motivated trades.

Revision Tip: In CFA exam scenarios addressing behavioral biases, prioritize answers recommending an explicit, rules-based investment process over those relying on "gut feel" or emotional responses.

Summary

Risk perception, loss aversion, and framing all shape real investor behavior and the resulting portfolios. Loss aversion causes investors to avoid necessary reallocations or to take excess risk after losses. Framing can induce different risk responses to identical investment information. Effective portfolio construction recognizes these biases and introduces systematic process checks, client education, and objective risk measures to keep behavioral traps from undermining objectives.

Key Point Checklist

This article has covered the following key knowledge points:

- Distinguish between risk perception and objective risk in portfolio construction.

- Recognize how loss aversion leads to holding losers and selling winners prematurely.

- Explain framing bias and its effect on interpreting risk information and survey responses.

- Apply behavioral awareness to mitigate biases during risk assessment and allocation.

- Recommend processes and communication techniques to reduce the impact of framing and loss aversion.

Key Terms and Concepts

- loss aversion

- risk perception

- framing bias