Learning Outcomes

This article explains how credit migration and default risk affect the pricing and risk profile of credit and securitized portfolios for the CFA Level 3 exam. It clarifies the distinction between migration events and default events, and shows how each influences bond prices, credit spreads, and portfolio mark‑to‑market volatility. It explains how to interpret changes in credit spreads as signals of shifting migration and default expectations, and how to link those spreads to expected loss and required return. It develops your ability to use key quantitative tools—probability of default (PD), loss given default (LGD), exposure at default (EAD), and expected loss (EL)—to assess issuer and portfolio risk. It explains how credit transition matrices are constructed and applied to estimate migration probabilities, default rates, and portfolio credit loss distributions. It also covers the implications of rating changes for structured products, including tranche performance and subordination. Finally, it examines practical portfolio management techniques, such as diversification, limits, stress testing, and hedging with credit derivatives, to monitor, control, and mitigate exposure to credit migration and default risk.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand credit migration and default risk management, especially for credit and securitized portfolios, with a focus on the following syllabus points:

- Explain credit migration, default risk, and their influence on bond prices and portfolio value

- Assess the effect of migration and default events on structured securities (e.g., MBS, CDOs)

- Compare quantitative and qualitative methods for evaluating migration risk and credit deterioration

- Describe the role of credit spreads and spread risk in portfolio management

- Analyze strategies for monitoring and controlling exposure to credit migration and default

- Calculate and interpret key measures: probability of default (PD), loss given default (LGD), exposure at default (EAD), expected loss (EL)

- Assess approaches for stress testing, scenario analysis, and limits for migration risk

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which term best describes the risk that a bond is downgraded though the issuer does not default?

- What does a widening credit spread signal about credit migration or default expectations?

- If a corporate bond is downgraded from BBB to BB, how might this affect its required yield?

- Briefly explain the difference between probability of default (PD) and credit migration risk.

Introduction

Credit migration and default risk are critical factors in credit and securitized portfolios. Migration risk refers to changes in an issuer’s credit rating without outright default, often resulting in spread changes and price volatility. Default risk is the probability the issuer will fail to make scheduled payments, leading to principal loss. Both risks are fundamental drivers of credit spread behavior and portfolio value.

Credit and securitized strategies require analysis of these risks at both the individual security and portfolio levels. Migration can produce significant mark-to-market losses even absent default. For structured products, credit migration of reference assets may erode tranche values or trigger structural protections.

Key Term: credit migration risk

The risk that an issuer’s credit quality changes, typically measured by a downgrade, which may cause a bond’s spread and price to change even without default. Key Term: credit spread

The yield difference between a credit-risky bond and a comparable-maturity government or risk-free bond, reflecting compensation for expected loss and migration risk. Key Term: default risk

The risk that the issuer fails to make full and timely payments of interest or principal as required, resulting in potential loss to the investor.Test Tip: When revising Credit migration and default risk management, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

MIGRATION RISK AND PORTFOLIO IMPACT

Credit migration occurs when an issuer’s credit rating is revised by a rating agency (e.g., S&P, Moody’s, Fitch). A downgrade increases the perceived risk of default, raises required yields for the bond, and results in a price drop—even if no payments are missed. This price volatility matters for portfolios that must mark assets to market.

The magnitude of migration risk depends on the issuer’s credit profile, the size of the downgrade, and the bond’s spread sensitivity. Migration risk is especially relevant for tranches of structured products—where a pool of assets contains diverse ratings and downgrades may increase subordination risk for senior tranches.

Key Term: migration event

An upgrade or downgrade of credit rating, distinct from default; typically triggers changes in required return and price, influencing portfolio value.

Worked Example 1.1

A fund holds $5 million of a BBB-rated bond. The issuer is downgraded to BB. The bond’s credit spread widens by 120 bps. What is the immediate price effect on a 7-year bond with a duration of 5.5?

Answer:

The price loss ≈ Duration × Spread change = 5.5 × 1.20% = 6.6%. Loss = $5,000,000 × 6.6% = $330,000 loss, assuming spread widening is the only factor.

INTERPRETING CREDIT SPREADS

Credit spreads compensate investors not only for expected losses from defaults but also for migration risk. A bond with a higher probability of rating downgrade will command a larger spread, reflecting the risk of forced sales by rating-constrained buyers and market repricing.

A widening in credit spreads can signal market fears of future downgrades or defaults, even before fundamentals deteriorate. Conversely, spread tightening often precedes rating upgrades or improved fundamentals.

Key Term: spread risk

The risk that a bond’s credit spread widens, causing its price to fall even when interest rates are stable.

CREDIT MIGRATION RISK VERSUS DEFAULT RISK

Though related, credit migration and default risk are distinct:

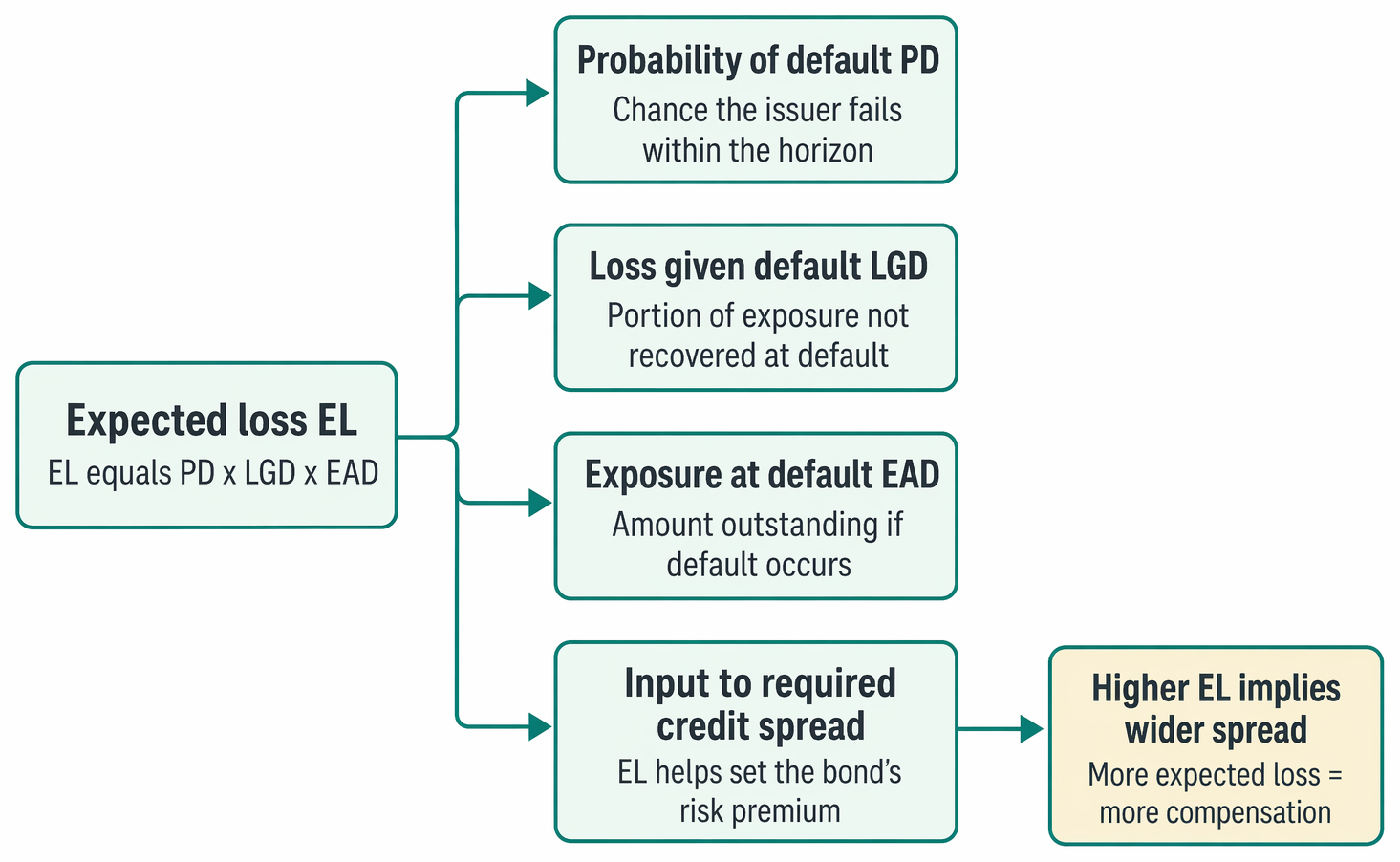

Expected loss, calculated as PD × LGD × EAD, feeds into credit spread setting, with higher expected loss implying wider spreads.

- Migration risk: Impact on price from changes in credit quality. Frequency is higher than default, but losses are typically smaller per event.

- Default risk: Probability the issuer fails to pay as agreed. Losses are typically severe when they occur.

Valuation and risk models often treat these separately, with migration risk driving volatility and default risk driving potential tail losses.

Key Term: probability of default (PD)

The likelihood, over a specified time horizon, that the issuer will fail to meet debt obligations. Key Term: loss given default (LGD)

The percentage of a bond’s value lost if default occurs, after recoveries. Key Term: expected loss (EL)

The average loss over a time horizon, estimated as EL = PD × LGD × EAD (exposure at default).

Worked Example 1.2

A bank holds $2 million face value of a corporate bond. Probability of default in 1 year is 5%. If LGD is 60%, what is the expected loss?

Answer:

Expected loss = EAD × PD × LGD = $2,000,000 × 5% × 60% = $60,000.

SOURCES OF CREDIT MIGRATION RISK

Migration risk arises from:

- Changing fundamentals (e.g., earnings, debt ratios, outlook)

- Industry shocks or macro events

- Model- or market-based early warning signals (quantitative risk factors)

- Active trading pressure on securities close to downgrade thresholds

For structured products or CDOs, migration risk in constituent assets can degrade tranche credit support or trigger performance tests, even without defaults.

MANAGING CREDIT MIGRATION AND DEFAULT RISK

Credit migration and default risk are managed at both security and portfolio levels.

Key techniques:

- Diversification across issuers, industries, and regions

- Regular stress testing and scenario analysis (simulate downgrades and spread shocks)

- Imposing exposure limits by rating grade or industry

- Quantitative models, including credit VaR (value-at-risk) and transition matrices

- Ongoing monitoring of fundamentals and market spreads

Portfolio managers may also seek to hedge migration risk with credit default swaps (CDS) or by dynamically re-allocating away from deteriorating credits.

Key Term: credit transition matrix

A statistical table showing probabilities of ratings changes (including default) over a period, used to forecast migration and expected losses.

Worked Example 1.3

Suppose a transition matrix indicates that, over 1 year, 15% of BBB-rated bonds migrate to BB, 4% default, and 81% remain at BBB. How does this inform portfolio risk management?

Answer:

Managers can anticipate roughly 19% (15% migration, 4% default) of BBB exposure may move into speculative or default status. They can constrain BBB allocations, stress test outcomes, and consider hedging or early exits.Exam Warning: Be careful: On the exam, do not confuse credit migration risk (price impact from rating changes) with default probability (missed payments). Both affect portfolio risk, but pricing impact occurs more frequently from migration events than outright defaults.

Summary

Credit migration and default risk are critical to the management and valuation of credit portfolios, influencing both expected return and portfolio volatility. Migration risk involves the impact of rating changes on bond prices and spreads, while default risk covers ultimate loss scenarios. Both can be modeled and managed using transition matrices, spread monitoring, diversification, and hedging instruments.

Key Point Checklist

This article has covered the following key knowledge points:

- Define and distinguish credit migration risk and default risk

- Recognize the impact of migration events on bond prices and portfolio value

- Interpret credit spreads as measures of both migration and default risk

- Calculate expected loss using PD, LGD, and EAD

- Describe and apply the use of credit transition matrices in portfolio risk analysis

- Manage exposure to migration and default risk through diversification, limits, and hedging

Key Terms and Concepts

- credit migration risk

- credit spread

- default risk

- migration event

- spread risk

- probability of default (PD)

- loss given default (LGD)

- expected loss (EL)

- credit transition matrix