Learning Outcomes

This article explains how mortgage-backed security (MBS) cash flows are shaped by borrower prepayments and interest rate movements, and sets out the structure, assumptions, and practical use of standard prepayment models. It describes PSA and CPR conventions in detail, including how market participants translate these assumptions into conditional prepayment rates, single monthly mortality (SMM) measures, and pool factors for agency and non-agency MBS. The article distinguishes static from stochastic prepayment modeling frameworks, highlighting how model choice and calibration affect projected cash flows, average life, price sensitivity, and the reliability of duration and convexity estimates. It then analyzes the concept, calculation, and interpretation of option-adjusted spread (OAS) in a Monte Carlo framework, emphasizing how OAS isolates compensation for credit and liquidity risk after stripping out the value of embedded borrower options. Finally, the article reviews how prepayment and OAS analysis are combined to assess relative value across MBS, callable corporates, and other option-embedded securities, and discusses common modeling limitations and exam-relevant pitfalls in interpreting prepayment paths and spread measures.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the prepayment risk, valuation, and risk measures for mortgage-backed and other securitized fixed-income products, with a focus on the following syllabus points:

- Describe the types of prepayment models (static and stochastic) and their assumptions

- Interpret PSA and CPR conventions and relate them to MBS amortization

- Explain the sources of cash flows and prepayment risk in mortgage-backed securities (MBS)

- Analyze the effect of prepayment modeling on expected cash flows, average life, and price/yield relationships for pass-through MBS and tranches

- Define and interpret option-adjusted spread (OAS) in the context of securities with prepayment options

- Apply OAS analysis to compare relative value across securities or portfolios with embedded options

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What convention is commonly used to express prepayment rates for US agency mortgage-backed securities, and how does it translate to expected CPR percentages?

- Briefly explain the economic rationale for using option-adjusted spread (OAS) rather than nominal spread for comparing the value of MBS or callable bonds.

- If current mortgage rates fall and prepayments accelerate, what happens to the average life of a pass-through MBS?

- How does OAS change if you increase the volatility assumption in a prepayment model (assuming a positively convex security)?

Introduction

Mortgage-backed securities (MBS) and other securitized products expose investors to prepayment risk, making traditional fixed-cash-flow valuation methods unsuitable. Investors and analysts need to apply specialized prepayment modeling and spreads that account for the option-like behavior of borrowers.

Key Term: prepayment risk

The risk that principal will be repaid earlier than scheduled, typically due to borrowers refinancing or moving. Key Term: PSA (Public Securities Association) prepayment model

A standardized convention for expressing expected prepayment rates, where 100 PSA represents a defined monthly prepayment pattern. Key Term: conditional prepayment rate (CPR)

The annualized percentage of the remaining mortgage pool expected to prepay in a given period. Key Term: option-adjusted spread (OAS)

The spread over a benchmark yield curve that, when added to all short rates in a path-dependent model, produces a model price equal to the market price of a security with embedded options.Test Tip: When revising MBS prepayment modeling and oas, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Prepayment Modeling for MBS

Mortgage pool prepayment modeling maps PSA or CPR assumptions into SMM and estimated monthly prepayments on the outstanding balance.

Overview of MBS Prepayment Risks

MBS holders receive periodic principal and interest payments but are exposed to early repayments. Borrowers prepay for numerous reasons—rate declines (refinancing), home sales, or curtailments. Unlike traditional bonds, the timing and amount of principal cash flows are uncertain.

Prepayment Conventions: PSA and CPR

Market participants typically quote prepayment assumptions using PSA (for standardized agency pools) or CPR (annualized). For US MBS:

- 100 PSA: Assumes prepayments begin at 0.2% CPR in the first month, increasing by 0.2% per month until reaching 6% CPR at month 30, then level.

- CPR: Represents the annualized percentage of the mortgage pool expected to prepay, assuming a constant rate (e.g., 8% CPR).

For custom or non-agency pools, CPR can be specified directly.

Key Term: average life

The weighted average time until principal is repaid, considering both scheduled amortization and expected prepayments.

Static vs. Stochastic Prepayment Models

- Static models assume a constant prepayment rate (e.g., 100 PSA or 6% CPR) over the entire horizon—simple but inflexible.

- Stochastic models link prepayments to assumed interest rate paths, reflecting the economic incentives borrowers have to refinance as rates fluctuate.

Sophisticated models may include borrower burnout, seasonality, loan seasoning, home price effects, and macroeconomic variables.

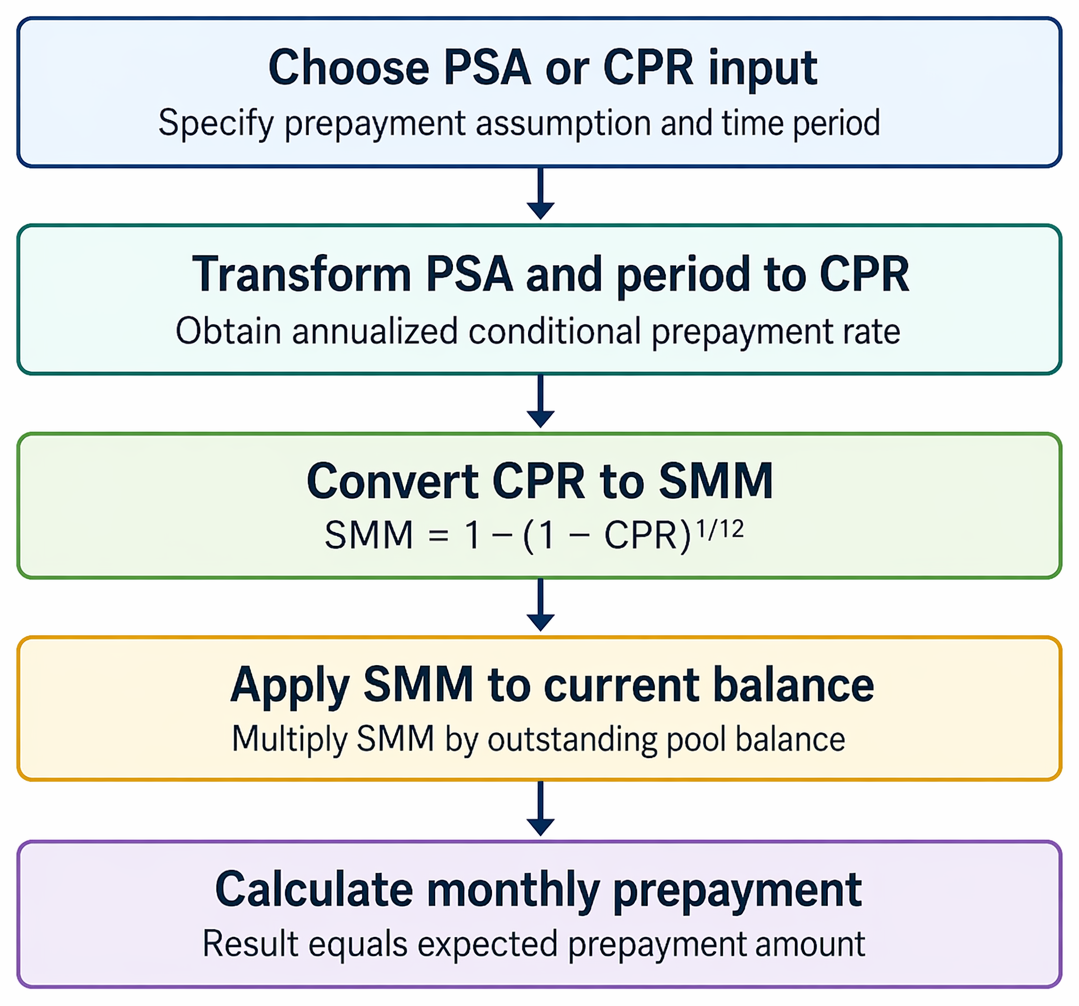

Worked Example 1.1

Question: A GNMA pass-through has a pool factor of 0.95, a coupon of 5.5%, and an original balance of $50 million. If you assume a 100 PSA prepayment assumption, what is the approximate monthly prepayment in month 6?

Answer:

100 PSA at month 6 is 1.2% CPR (0.2% x 6). The monthly SMM (single monthly mortality rate) ≈ 1 – (1 – 0.012)^(1/12) ≈ 0.0010048, or ≈ 0.10% per month. The outstanding balance at month 6 is $47.5 million. Monthly prepayment ≈ $47,500,000 x 0.10% ≈ $47,500.

Modelling Effect on MBS Price, Yield, and Average Life

- Faster prepayments (from lower rates) shorten the average life, increasing reinvestment risk.

- Slower prepayments (from higher rates) extend average life, increasing price sensitivity to rate movements.

- Large prepayment variability distorts traditional duration and convexity measures, making OAS analysis essential.

Option-Adjusted Spread (OAS) and Its Use in MBS

OAS is the market-standard metric for risk-adjusted valuation and comparison of bonds with embedded options, such as callable bonds and MBS.

- OAS strips out the value of any borrower option implicitly sold by the investor (callability due to prepayment).

- OAS is derived by adjusting the modelled yield curve in a Monte Carlo framework until the discounted average expected cash flows equate the security’s price to market.

- OAS is compared across securities to establish relative value, since it represents compensation per unit of option risk, after removing the expected cost of the borrower option.

Key Term: Monte Carlo simulation (for prepayment modeling)

A method that generates a large number of possible interest rate and prepayment paths to value the expected cash flows from securities with embedded options.

Worked Example 1.2

Question: Suppose an MBS has a market price of 102, and a stochastic prepayment model suggests its value equals 102 when a 50 bps OAS is added to each path in the interest rate model. If volatility is increased in the prepayment model’s assumptions, what generally happens to the OAS for a highly optioned (neg-convex) MBS?

Answer:

Increasing volatility raises the value of the borrower’s prepayment option, which the investor is short. The higher option cost reduces the OAS, all else equal.Exam Warning: Option-adjusted spread analysis is only meaningful if the prepayment model accurately fits real-world borrower behavior. Overly simplistic models risk mispricing prepayment and thus OAS, leading to incorrect relative value conclusions.

Key Drivers and Limitations of OAS and MBS Prepayment Models

- OAS depends on reliable modeling of both interest rates and borrower behavior; models are always imperfect.

- OAS is most useful for comparing securities with similar types of embedded options under identical modeling assumptions.

- Prepayment model calibration to recent market experience is essential for accurate MBS pricing and risk assessment.

Worked Example 1.3

Question: A portfolio manager compares a 30-year agency MBS with a callable corporate bond—both trade at par and have an OAS of 80 bps and 100 bps, respectively, using the same model assumptions. Which is more attractive, holding prepayment and call option models as equally accurate?

Answer:

The callable corporate bond with a higher OAS offers greater risk compensation, assuming comparable model reliability and fundamental credit risk.

Summary

Prepayment modeling is essential for analyzing, pricing, and managing MBS and option-embedded asset-backed securities. Prepayment rates are commonly specified using PSA or CPR conventions, and robust models can incorporate stochastic interest rate paths and borrower behavior. The option-adjusted spread (OAS) isolates spread compensation for risks excluding the explicit value of the prepayment option. OAS provides a critical comparative tool for portfolio managers seeking relative value among option-impacted fixed-income alternatives.

Key Point Checklist

This article has covered the following key knowledge points:

- Understand PSA and CPR conventions for prepayment assumptions

- Distinguish static and stochastic prepayment models and main model drivers

- Identify how prepayment variability affects MBS cash flows, average life, and price risk

- Define, interpret, and practically apply OAS for evaluating relative value among option-embedded securities

- Recognize modeling limitations that affect OAS reliability

Key Terms and Concepts

- prepayment risk

- PSA (Public Securities Association) prepayment model

- conditional prepayment rate (CPR)

- option-adjusted spread (OAS)

- average life

- Monte Carlo simulation (for prepayment modeling)