Learning Outcomes

This article explains currency risk management in FX with a focus on carry value and momentum, including:

- Describing the mechanics of FX carry trades, including how interest rate differentials translate into expected returns and forward pricing.

- Analyzing how adverse spot moves generate negative carry events and asymmetric, negatively skewed loss profiles in crisis periods.

- Contrasting carry with momentum-based FX strategies that buy recent winners and sell recent losers using trailing return signals.

- Evaluating empirical evidence on the performance, cyclicality, and drawdown characteristics of currency carry and momentum factors.

- Assessing how portfolio managers implement standalone and combined carry–momentum overlays within institutional multi-asset portfolios.

- Identifying key risk controls, including position sizing, leverage limits, liquidity management, and stress-testing of overlay strategies.

- Diagnosing common exam pitfalls, such as assuming stable factor premia or ignoring correlation spikes during risk-off environments.

- Applying worked examples that calculate carry-based returns, momentum overlay outcomes, and the impact of factor diversification on portfolio losses.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the practical challenges of currency risk management, specifically how carry and momentum strategies operate in FX markets and their incorporation into investment policy and active overlays, with a focus on the following syllabus points:

- Explaining the mechanics and risk exposures of currency carry trades.

- Analyzing the role of momentum in currency selection and overlay strategies.

- Assessing risks, diversification limits, and pitfalls for portfolio managers employing carry and momentum FX strategies.

- Identifying and justifying the inclusion or exclusion of carry- or momentum-based overlays in multi-asset portfolios.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What primary risk is associated with currency carry trades and how can it impact portfolio returns in crisis periods?

- How does momentum differ from carry value in the context of FX trading?

- Explain why a carry strategy may underperform or experience large losses during market stress.

- What portfolio construction considerations arise when using momentum as a currency overlay?

Introduction

Currency risk management is critical for globally diversified portfolios at CFA Level 3. This article examines two empirical FX phenomena: carry value (carry trade) and momentum effects. Both have been found to offer positive returns over time, yet each comes with specific risk profiles and practical implementation difficulties. Thorough understanding of these concepts is essential for assessing and managing currency overlay strategies and for mitigating unintended risk exposures within institutional investment policies.

Key Term: carry trade

A trading strategy in FX that seeks to profit by borrowing in currencies with low interest rates and investing in those with higher yields, typically targeting the interest rate differential. Key Term: momentum (in FX)

The tendency for a currency's past relative performance to continue in the short term, such that recent “winner” currencies are likely to keep outperforming “loser” currencies.

FX CARRY VALUE: MECHANICS AND RISKS

Carry trades in FX exploit the difference between short-term interest rates (the "carry") by holding high-yielding currencies funded by borrowing in low-yielding ones. Investors anticipate profit equal to the interest rate differential, assuming the spot rate remains unchanged. However, exchange rates are volatile, and during market disruptions, high-yield currencies often experience sharp depreciations, leading to sudden, severe carry trade losses.

Worked Example 1.1

Question: A manager notices USD/JPY offers a 3% annualized carry in favor of the dollar, with USD short rates at 3% and JPY near zero. Over one year, the USD depreciates by 4% relative to JPY. What is the net return to a carry trade that was long USD/short JPY?

Answer:

The carry is +3%, but the 4% depreciation in USD erases all carry gains and results in a 1% net loss: 3% carry – 4% depreciation = –1%. This illustrates how FX moves can outweigh interest rate differentials, especially during market volatility. Key Term: negative carry event

A scenario where adverse currency moves offset or overwhelm the positive carry earned from the interest rate differential.Exam Warning: A common CFA exam mistake is to assume carry strategies outperform in all market conditions. In crises, “risk-off” trading often triggers sharp depreciations in high-carry currencies. Always recognize the asymmetric (negatively skewed) risk profile of these trades.

FX MOMENTUM: DETECTING AND DEPLOYING THE TREND

FX momentum strategies buy recent outperforming ("winner") currencies and sell recent underperformers ("losers"), typically based on trailing 3-to-12-month returns. Academic and practitioner evidence shows outperformance of this approach even after costs, albeit with periods of sharp reversal risk.

Momentum in FX can be exploited using long/short baskets based on cumulative past returns. However, returns are not persistent forever; at turning points, momentum positions may suffer substantial drawdowns.

Worked Example 1.2

Question: A portfolio manager reviews the past 6 months: GBP and AUD have appreciated 5%, while SEK and CAD are down 4%. If she applies a momentum overlay by going long GBP/AUD and short SEK/CAD, what is the risk if the trend reverses abruptly?

Answer:

If market conditions reverse (e.g., SEK and CAD suddenly recover and GBP/AUD lag), the momentum overlay may incur rapid and significant losses as persistent trends break. These drawdowns are often observed around shifts in global risk appetite or macroeconomic surprises.

DESIGNING CURRENCY OVERLAYS: COMBINING CARRY AND MOMENTUM

Currency overlay mandates may use carry, momentum, or both factor signals. While carry is related to differences in interest rates, momentum is strictly price-based. Diversifying across these styles can help: their return streams are only moderately correlated, and their drawdowns often occur at different times.

Currency carry mechanics link interest differentials and subsequent spot movements to total FX return and the detection of loss-making carry outcomes.

However, mis-specification or excessive reliance on a single factor can increase portfolio risk, especially under extreme market conditions. Risk controls, appropriate gearing levels, and robustness testing are mandated.

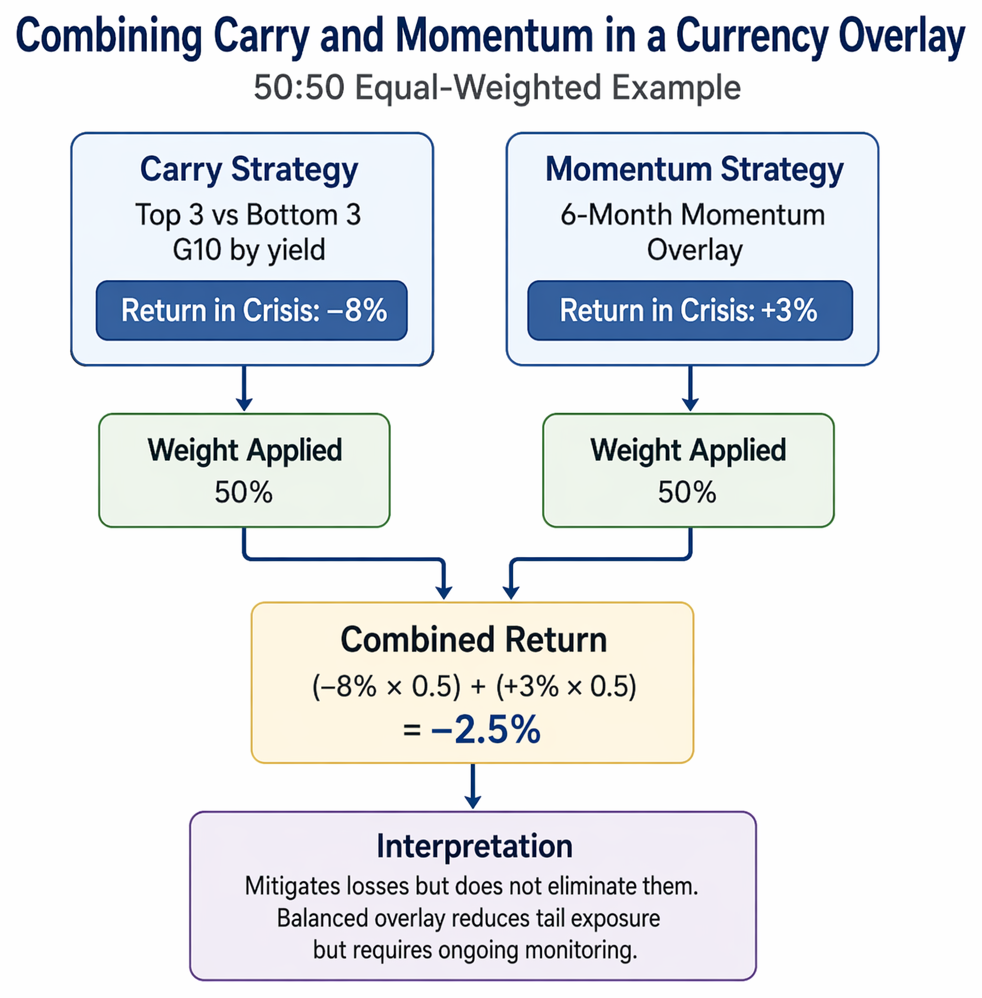

Worked Example 1.3

Question: An endowment considers a currency overlay combining a carry strategy (top 3 vs bottom 3 G10 currencies by yield) and a 6-month momentum overlay with equal weights. If carry exposure loses 8% during a crisis but momentum gains 3%, what is the overall impact for a 50:50 combination?

Answer:

The overall return is half of each: (–8% × 0.5) + (+3% × 0.5) = –2.5%. Combining mitigates but does not eliminate losses in extreme events. Balanced overlay reduces tail exposure but requires ongoing monitoring.

PORTFOLIO RISKS, PREDICTABILITY, AND PRACTICAL CONSTRAINTS

Carry and momentum exposures produce attractive average returns, but their risk profiles are highly non-normal, showing fat tails and episodes of rapid reversal. Risk factors include:

- Correlation spikes during market shocks (“risk-off” sells high-carry and high-momentum currencies).

- Hidden gearing through derivatives and forwards.

- Liquidity gaps if positions need rapid unwinding.

- Model decay—return premia are diminished if too many market participants crowd into the same trades.

Exam Warning (Overlays)

Do not rely on historical backtests alone—factor returns are unstable and vulnerable to alpha decay and crowding, especially in stressed environments. Always stress-test overlay portfolios and model funding and operational constraints.

Revision Tip: For the CFA exam, know how to explain the difference in risk/return drivers between carry and momentum, and be able to enumerate major pitfalls of each. Always integrate these in your assessment of currency risk management strategies.

Summary

FX carry and momentum strategies are widely used in institutional currency overlays. Carry trades profit from positive rate differentials but face abrupt losses if market trends reverse. Momentum overlays exploit short-term price trends but may lag in choppy or mean-reverting environments. Both strategies display non-normal risk, and both must be combined with robust risk controls and an understanding of correlation breakdowns and extreme market events.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain mechanics and risk of currency carry trades.

- Describe the implementation and risk profile of FX momentum overlays.

- Recognize negative skew and non-normal risk in currency factor strategies.

- Assess when to include or limit carry/momentum overlays in currency risk management.

- Identify diversified and risk-managed approaches for currency overlay design.

Key Terms and Concepts

- carry trade

- momentum (in FX)

- negative carry event