Learning Outcomes

This article explains currency risk management using forwards, options, and non-deliverable forwards (NDFs), including:

- Identifying and classifying transaction, translation, and economic currency exposures in global portfolios, and determining their direction.

- Explaining the mechanics, payoff diagrams, and settlement conventions of deliverable forwards and NDFs, including fixing and cash-settlement.

- Comparing symmetric forward and NDF payoffs with the asymmetric, premium-funded payoffs of currency options and option-based collars.

- Designing full, partial, and options-based hedges that align with client objectives, risk tolerance, investment horizon, and liability structure.

- Quantifying how forward points, interest rate differentials, and option premiums alter expected hedged returns versus unhedged returns.

- Calculating and interpreting hedged and unhedged domestic-currency returns, effective option hedge rates, and NDF cash-settlement amounts.

- Evaluating when NDFs are preferable to deliverable forwards for restricted or illiquid currencies subject to capital controls.

- Selecting between forwards, options, and NDFs for specific exam vignettes, and justifying hedge ratios and instrument choices in concise CFA Level 3–style answers.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand currency risk management for multi-currency portfolios, with a focus on the following syllabus points:

- Describing and comparing currency hedging instruments: forwards, futures, options, swaps, and NDFs

- Determining when to hedge FX risk, and selecting full, partial, or no hedging

- Explaining how forward rates and forward points relate to interest rate differentials

- Calculating hedged and unhedged portfolio returns and cash flows

- Designing and evaluating option-based currency hedges, including collars

- Explaining the role of NDFs where capital controls prevent physical delivery

- Integrating currency views, risk tolerance, and constraints into portfolio recommendations

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

A euro-based investor holds USD assets and wants to lock in the EUR value in six months with no upside participation. Which instrument is most consistent with this objective?

- a) Buy a EUR call (USD put) option

- b) Sell a EUR put (USD call) option

- c) Enter a six-month EUR/USD forward contract

- d) Enter a six-month EUR/USD NDF

-

A vignette states that a fund has exposure to an emerging-market currency that is non-convertible and subject to capital controls. Which hedge is most appropriate?

- a) Deliverable FX forward

- b) Currency swap

- c) Non-deliverable forward (NDF)

- d) Exchange-traded FX option

-

A client wants to “protect against a sharp depreciation of the foreign currency but still benefit if it appreciates.” Which instrument best fits this need?

- a) Forward contract

- b) Long put option on the foreign currency

- c) Short call option on the foreign currency

- d) NDF

-

A manager believes the foreign currency will appreciate, but the client has low risk tolerance and wants to reduce downside volatility. Which approach best reflects a compromise?

- a) Fully hedge the currency with forwards

- b) Leave the currency completely unhedged

- c) Implement a partial forward hedge

- d) Implement a full hedge using NDFs

Introduction

Currency fluctuations can materially alter the value and volatility of international investments when measured in an investor’s home currency. At Level 3, you must not only understand the mechanics of hedging instruments, but also be able to combine them into appropriate, client-specific recommendations.

Key Term: currency risk

Currency risk is the risk that changes in exchange rates will affect the domestic-currency value or returns of assets or liabilities denominated in a foreign currency.

A global equity or bond portfolio typically involves:

- Local-currency asset returns (e.g., the stock market in EUR)

- Currency returns from movements in the exchange rate (e.g., EUR/USD)

- The interaction between asset and currency returns

Unhedged domestic-currency return is approximately:

where is the percentage change in the foreign currency relative to the home currency. A hedge modifies or removes .

Three main tools for managing this risk are deliverable forwards, currency options, and non-deliverable forwards (NDFs). Each has distinct payoff patterns, cash-flow implications, and suitability depending on client preferences, market liquidity, and regulatory constraints.

Key Term: forward contract

A forward contract is an over-the-counter (OTC) agreement to exchange two currencies at a fixed rate on a specific future date; settlement is typically by physical delivery of both currencies. Key Term: currency option

A currency option is a contract granting the right, but not the obligation, to buy or sell a specified amount of currency at a pre-agreed exchange rate (the strike) on or before a specific date, in exchange for an upfront premium. Key Term: non-deliverable forward (NDF)

A non-deliverable forward is a cash-settled forward contract, usually settled in a hard currency (e.g., USD), that nets the difference between the agreed NDF rate and the fixing spot rate at maturity, without exchanging the notional of the referenced (often non-convertible) currency. Key Term: capital controls

Capital controls are government-imposed restrictions on currency convertibility and cross-border capital flows; they often prevent physical delivery of local currency to foreign counterparties.

This article focuses on how these instruments are combined with portfolio objectives, constraints, and views to construct robust currency risk management strategies.

Test Tip: When revising Forwards options and NDFs, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Exam Warning: Do not rely on keyword recognition alone; check the precise condition, exception, calculation step, or evidence the question requires.

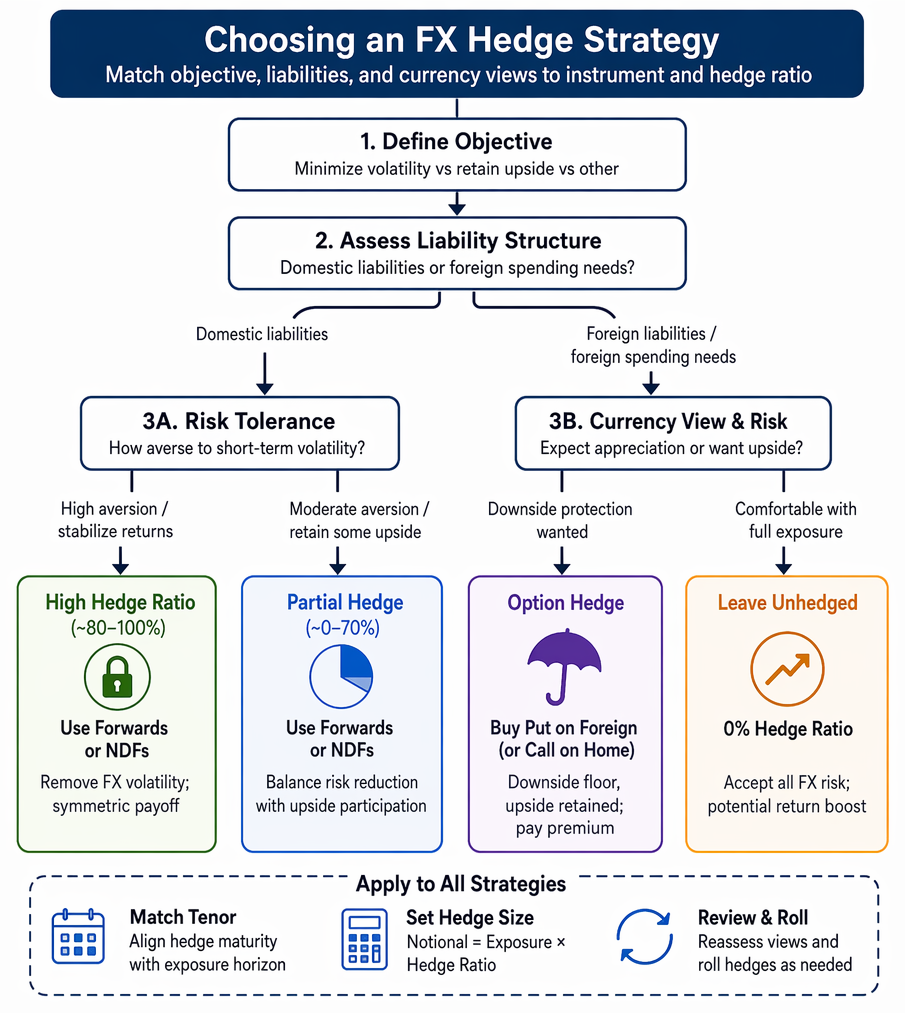

Forwards, Options, and NDFs in Currency Risk Management

Currency risk management decision tree links restricted currencies to cash-settled NDFs and tradable currencies to forwards or option-based hedges.

Why Hedge Currency Risk

Currency fluctuations can both increase volatility and alter expected return. Hedging decisions therefore involve a trade-off between risk reduction and potential reward.

Common strategic approaches include:

-

Passive (full) hedging: Fully hedge foreign-currency exposures to stabilize domestic-currency returns. Often implemented via rolling forward contracts or NDFs.

-

Active (partial) hedging: Set a hedge ratio between 0% and 100%, and adjust tactically based on currency views and risk budget.

-

Leave unhedged: Accept all FX risk, sometimes for diversification or return-seeking reasons, especially when currencies are expected to appreciate or provide a hedge against domestic shocks.

Key Term: hedge ratio

The hedge ratio is the proportion of a currency exposure that is hedged using derivatives (e.g., a 60% hedge ratio means 60% of the foreign-currency exposure is hedged, 40% remains unhedged).

Your task in a Level 3 vignette is to infer the appropriate hedge ratio and instrument choice from information about:

- Risk tolerance and aversion to short-term volatility

- Investment horizon (short-term vs very long-term)

- Liability structure (e.g., domestic liabilities vs foreign liabilities)

- Views on currency direction

- Constraints such as capital controls, liquidity, and derivatives policy

If the objective is to minimize short-term volatility and the client has domestic liabilities, a high hedge ratio using forwards or NDFs is often justified. If the client has foreign-currency spending needs (e.g., a retiree living in EUR with USD base currency), leaving some exposure unhedged may better match liabilities.

When to Use Forwards, Options, and NDFs

Currency Forwards

Deliverable forwards are widely used where both currencies are freely traded and physical delivery is feasible. They:

- Lock in an exchange rate for a future date

- Eliminate uncertainty about the domestic-currency value of a foreign asset or liability

- Create a linear, symmetric payoff: gains and losses are equal in magnitude for equal-sized FX movements

Typical Uses

- Fully hedging bond portfolios where stable income in the base currency is a priority

- Hedging known, dated cash flows (e.g., a known foreign-currency dividend or bond redemption)

- Implementing active currency views (over- or under-hedging)

Options

Options provide downside protection while retaining upside potential, with an asymmetric payoff. The cost is an upfront option premium.

- A put on the foreign currency (or equivalently a call on the home currency) protects against foreign-currency depreciation while allowing participation in appreciation.

- A call on the foreign currency protects against appreciation when you need to buy foreign currency in the future.

Options are particularly appropriate when:

- The client is risk averse but unwilling to give up favorable currency moves

- Volatility is high and the distribution of FX outcomes is skewed or uncertain

- The manager has a directional view but wants to cap losses

Key Term: moneyness

Moneyness describes the relationship between the current spot rate and an option’s strike: at-the-money (ATM), in-the-money (ITM), or out-of-the-money (OTM). It strongly affects premium and hedge behavior. Key Term: collar

A collar is an options strategy that combines a long option (e.g., a protective put) with a short option (e.g., a written call) on the same notional and maturity, designed to limit both upside and downside within a band, often at reduced or zero net premium.

Non-Deliverable Forwards (NDFs)

NDFs are used when the referenced currency is non-convertible, tightly controlled, or lacks a liquid forward market.

No physical exchange of the local currency occurs. Instead:

- The contract references an “offshore” forward rate on a restricted currency

- At fixing, the agreed NDF rate is compared to a published spot reference rate

- The net difference is settled in a hard currency such as USD

Key Term: settlement currency

The settlement currency is the currency used for cash settlement of an NDF; it is typically a hard currency such as $, EUR, or GBP.

NDFs replicate the economic effect of deliverable forwards on the domestic-currency value of the exposure, but are compatible with capital controls.

Types of FX Exposure (Exam-Relevant Distinction)

Before designing a hedge, identify the nature and direction of exposure:

-

Asset exposure: A home-currency investor holds foreign-currency assets. If the foreign currency depreciates, domestic-currency value falls.

-

Liability exposure: A home-currency investor owes payments in foreign currency. If the foreign currency appreciates, the domestic cost rises.

-

Anticipated vs existing exposures: Existing holdings (e.g., foreign bonds already owned) vs future planned transactions (e.g., planned purchase of EUR in three months).

The hedge direction reverses for assets vs liabilities:

- Foreign asset: typically sell foreign / buy home in the forward or NDF

- Foreign liability: typically buy foreign / sell home in the forward or NDF

Failure to get the direction correct is a common exam error.

Worked Example 1.1

A US-based portfolio manager holds a large position in bonds denominated in MXN. Because of capital controls and an illiquid onshore forward market, she cannot find deliverable forward contracts on the Mexican peso. She wants to hedge the USD value of her MXN exposure over the next six months.

Answer:

She should use a USD-settled MXN NDF. She enters into a contract to sell MXN (and receive USD) at an agreed NDF rate in six months. At fixing, the NDF provider compares the agreed rate to the official MXN/USD spot rate and pays or receives the USD cash difference. No pesos are delivered, so the hedge is feasible despite capital controls. This is the standard solution when the exposure currency is restricted or non-convertible.

Mechanics of a Currency Forward

At inception, two parties agree:

- Notional amounts in the two currencies

- The forward exchange rate

- The maturity date and settlement convention

Key Term: base currency

The base currency is the second currency in an FX quote when expressed as price/base in CFA notation; it is the currency in which the asset may be denominated. Key Term: price currency

The price currency is the first currency in an FX quote; it is the currency in which the exchange rate is expressed and usually the investor’s domestic currency in Level 3 problems.

If the spot exchange rate is quoted as and annualized interest rates for price and base currencies are and for maturity (in years), then under covered interest rate parity the theoretical forward rate is:

Key Term: covered interest parity (CIP)

Covered interest parity is the no-arbitrage relationship linking spot and forward FX rates to domestic and foreign interest rates, assuming fully hedged positions and no capital controls.

The difference between forward and spot, often quoted in pips, is referred to as forward points:

Key Term: forward points

Forward points are the arithmetic difference between the forward rate and the spot rate, quoted in pips. A positive value means the price currency trades at a forward premium; a negative value implies a forward discount.

Important exam implications:

- If the price currency interest rate is higher than the base currency’s, the price currency typically trades at a forward discount (negative forward points).

- Hedging currency risk with forwards effectively transforms foreign-currency cash flows into domestic-currency cash flows that reflect the interest rate differential embedded in the forward.

Key Term: notional principal

Notional principal is the reference amount of currency on which payments in forwards, options, and NDFs are based. It is not usually exchanged in NDFs but is exchanged in deliverable forwards.

Worked Example 1.2

You manage a portfolio with significant EUR exposure. Your base currency is USD. You are concerned about short-term downside risk in EUR over the next three months but want to retain some upside potential if EUR appreciates.

Which instrument best aligns with this objective?

Answer:

A USD/EUR currency put option on EUR (equivalently, a EUR/USD call on USD) is appropriate. By buying a put on EUR, you secure a minimum EUR/USD rate (the strike), limiting the downside if EUR weakens. If EUR strengthens, you simply let the option expire and benefit fully from the favorable FX move. The trade-off is the upfront option premium, which reduces expected return. In contrast, a forward would hedge fully but eliminate upside.

Mechanics of a Currency Option

An FX option is defined by:

- Reference currency pair

- Strike exchange rate

- Expiration date

- Option type: call or put, European or American style

- Notional amount

- Premium paid or received

The payoff is asymmetric:

- Long call on foreign currency: benefits from foreign appreciation above the strike; loss is limited to premium.

- Long put on foreign currency: benefits from foreign depreciation below the strike; loss is limited to premium.

The key design variables are:

- Strike choice (ATM, OTM, ITM)

- Maturity relative to the horizon of the exposure

- Whether to offset premium via strategies like collars

Option premia are higher when:

- Volatility of the currency pair is high

- Time to expiration is longer

- Interest rate differentials are large

An important Level 3 synthesis skill is to articulate how option premium payments lower expected returns but may improve risk-adjusted performance when downside tails are a concern.

Non-Deliverable Forwards (NDFs) Details

NDFs work like forwards in economic terms but differ in settlement.

Key Term: fixing date

The fixing date is the date on which the spot reference rate is observed to calculate the NDF cash settlement. Key Term: settlement date

The settlement date is the date on which the NDF cash payment is exchanged in the settlement currency, typically a few business days after fixing.

On the fixing date:

- A pre-agreed reference spot rate (e.g., official central bank fixing) is compared to the NDF rate.

- The difference is applied to the notional to determine a gain or loss.

- On the settlement date, the net amount is paid in the settlement currency (e.g., USD).

Key characteristics:

- No delivery of the restricted currency

- Usually short-term (1–12 months) but can be longer

- Quoted and settled offshore

- Used extensively for currencies with capital controls (e.g., CNY, INR, BRL in various regimes)

NDF pricing reflects:

- Offshore interest rate differentials

- Market expectations of onshore vs offshore rates

- Credit and liquidity premia

Worked Example 1.3

Suppose a BRL/USD NDF contract has:

- Notional: BRL 1,000,000

- NDF rate: 5.0000 BRL/USD

- Fixing spot rate at maturity: 5.2500 BRL/USD

- Settlement currency: USD

How much is paid, and by whom?

Answer:

The NDF references the BRL value of $1. At 5.0000 BRL/USD, the implied USD value of the notional is BRL 1,000,000 ÷ 5.0000 = $200,000. At the fixing rate 5.2500, that same BRL notional is worth BRL 1,000,000 ÷ 5.2500 ≈ $190,476. The party who agreed to sell BRL and receive USD at 5.0000 is now worse off, because the market would deliver fewer USD for BRL (5.2500). The USD cash settlement equals:

The BRL seller (USD receiver under the NDF) pays $9,524 to the counterparty. This payment offsets the mark-to-market loss on the notional position, effectively locking in the agreed NDF rate. Revision tip: In exam vignettes, references to “restricted market”, “capital controls”, “non-convertible currency”, or “offshore hedge settled in USD” are strong cues to recommend an NDF rather than a deliverable forward. Exam warning: Clearly distinguish between physical delivery (deliverable forward) and cash settlement (NDF or option). Misstating settlement mechanics is a frequent source of lost marks.

Designing a Forward Hedge: Direction, Size, and Horizon

When using forwards or NDFs to hedge:

-

Identify direction: For a foreign asset, you are long the foreign currency; hedge by selling foreign (buying domestic) in the derivative.

-

Determine hedge size (notional): For a full hedge, the notional equals the current market value of the foreign exposure. For a partial hedge, multiply by the hedge ratio.

-

Align tenor with horizon: If the investment horizon exceeds hedge tenor, rolling the hedge will be required, potentially affecting performance due to changing forward points.

Worked Example 1.4

A UK investor (base currency GBP) holds $10 million of US equities, valued at GBP 8 million at the current spot rate of 0.8000 GBP/USD. She wants to fully hedge the next three months of USD exposure using a deliverable forward. What notional should she use and in which direction?

Answer:

She is long USD assets and concerned about GBP value. To hedge, she should sell USD and buy GBP in the forward market. For a full hedge, she sets the forward notional equal to the USD exposure: sell $10 million forward (and receive GBP at the forward rate). The GBP notional will be determined by the forward rate quoted by the dealer. This will immunize the GBP value of her US equity holdings against USD/GBP moves over the hedge period (ignoring basis risk from equity price changes).

Partial Hedges and Active Currency Views

You may be asked to justify a partial hedge, for example 50% of the exposure, when:

- The client wants some currency diversification

- The manager has a moderate view on currency direction

- The client’s liabilities are partly in foreign currency

Key Term: hedge ratio (revisited)

At Level 3, the hedge ratio is often a judgmental parameter balancing risk reduction and expected return, not just a statistical minimum-variance parameter.

A partial forward hedge can be interpreted as:

- A combination of a fully hedged position and an unhedged position

- Equivalent to consciously maintaining some open FX exposure

Worked Example 1.5

A Swiss-based endowment (CHF base) holds $20 million in global bonds. Its investment committee is moderately optimistic on USD but concerned about downside risk. Risk tolerance is low to moderate. Suggest an appropriate hedge ratio and instrument, and justify your choice.

Answer:

A plausible recommendation is a 50–70% hedge ratio using CHF/USD deliverable forwards. This reduces FX volatility significantly (aligning with low-to-moderate risk tolerance) while preserving some upside from potential USD appreciation. The endowment does not have USD liabilities, so there is no compelling liability-matching reason to stay fully unhedged. A full hedge might be too conservative given their positive USD view; leaving it fully unhedged could be inconsistent with their risk profile. A partial forward hedge appropriately integrates views and risk tolerance.

Comparing Forwards and Options in a Hedging Mandate

When choosing between forwards (or NDFs) and options, consider:

-

Risk profile: Forwards remove both downside and upside currency risk; options mainly remove downside, at a cost.

-

Cost and cash-flow impact: Forwards typically require no upfront premium but may involve credit support or margin. Options require premium outlay, reducing current income or capital.

-

Client objectives: A total-return–oriented, risk-neutral client may prefer forwards; a capital-preservation–oriented client may favor options.

Key Term: strike price

The strike price is the exchange rate specified in an option contract at which the holder can buy or sell the referenced currency.

Worked Example 1.6

A Canadian pension fund (CAD base) has a large allocation to EUR-denominated infrastructure assets. The board is very sensitive to downside risk in CAD terms but has a long horizon and is reluctant to “give away” upside from EUR appreciation. Funding ratio is healthy.

Which hedging approach is most appropriate?

a) Fully hedge with EUR/CAD forwards b) Fully hedge with EUR put options (CAD call options) c) Leave the currency completely unhedged d) Implement a 50% forward hedge

Answer:

Option (b) is most consistent. Protective EUR put options (CAD calls) provide a floor to the CAD value of the EUR exposure, addressing downside risk sensitivity, while preserving upside if EUR strengthens. The costs (option premiums) are acceptable given the healthy funding ratio and long horizon. A full forward hedge (a) would eliminate both downside and upside currency risk, conflicting with the desire to retain upside. Leaving the exposure unhedged (c) ignores the stated risk aversion. A partial forward hedge (d) reduces volatility but still exposes half the position to potentially large EUR depreciation.

Hedged vs Unhedged Returns and Forward Points

For a foreign asset with local-currency return and currency return :

-

Unhedged domestic return:

-

Fully forward-hedged domestic return (assuming CIP holds):

Over the hedge horizon, you are effectively:

- Long the foreign asset

- Short the foreign currency via forward

- Long the domestic money market

The domestic return approximates:

where is the domestic risk-free rate and is the horizon in years. FX volatility is largely removed; currency exposure is replaced by domestic interest rate exposure.

The forward premium/discount embedded in relative to reflects the interest rate differential:

- Positive forward points: price currency at a forward premium

- Negative forward points: price currency at a forward discount

An important exam detail:

- Hedging high-yield foreign currencies (where foreign rates > domestic) typically gives up some expected return because the foreign currency tends to trade at a forward discount.

- Hedging low-yield foreign currencies may increase expected return, because the foreign currency trades at a forward premium.

You should be able to explain in words how forward points alter expected hedged returns, even if not asked for exact calculations.

Options and Effective Hedge Cost

Option hedges alter expected return through:

- Upfront premium (certain cost)

- Potential exercise gain (conditional benefit)

- Participation in favorable FX moves beyond the strike

The effective exchange rate when using a call option to buy EUR (for example) is:

where is the strike rate. If the spot rate at expiration is below , the option is not exercised, and the effective rate is the spot rate plus sunk premium.

At Level 3, commentary should reflect both quantitative impact (premium drag on return) and qualitative impact (better downside protection, convexity of payoffs).

Worked Example 1.7

A US-based company plans to purchase EUR 1,000,000 in three months. Data:

- Spot: 1.20 USD/EUR

- Three-month EUR call (USD put) with strike 1.25 USD/EUR costs 0.02 USD per EUR

- Three-month forward: 1.205 USD/EUR

a) If spot in three months is 1.29 USD/EUR, what is the effective purchase rate under the call option hedge? b) If spot in three months is 1.10 USD/EUR, compare the cost under the call and forward hedges.

Answer:

a) At 1.29, the call is in the money. The company exercises the call, buying EUR at 1.25. Including the premium of 0.02, the effective rate is:

The total USD cost is 1.27 × 1,000,000 = $1,270,000. b) At 1.10, the call expires worthless, and the company buys EUR at spot: 1.10. The total USD cost is:

- With call: 1.10 × 1,000,000 + (0.02 × 1,000,000) = 1,100,000 + 20,000 = $1,120,000

- With forward: 1.205 × 1,000,000 = $1,205,000

The option hedge costs $85,000 less than the forward in this scenario, because the company benefits from favorable spot movement (1.10) but pays the premium. The forward locks in certainty at 1.205, regardless of spot. This illustrates the asymmetric payoff of options versus the symmetric payoff of forwards.

From an exam standpoint, you should be able to:

- Compute effective purchase/sale rates under both hedges

- Comment on trade-offs between certainty, cost, and upside participation

Summary

Currency risk management is a central topic in CFA Level 3 portfolio management. Forwards, options, and NDFs are the core instruments.

- Deliverable forwards lock in future FX rates with symmetric payoffs and typically no upfront premium, but require physical delivery and may be constrained by capital controls.

- Options provide asymmetric protection: they cap downside risk but allow upside participation at the cost of a premium, and can be structured into collars to reduce cost.

- NDFs replicate forward hedging economics for non-convertible or restricted currencies, using cash settlement in a hard currency.

At Level 3, you must go beyond mechanics and quantify and justify hedging choices in the context of:

- Client objectives and constraints

- Risk tolerance and horizon

- Currency views and diversification benefits

- Market features such as capital controls and liquidity

Key Point Checklist

This article has covered the following key knowledge points:

- The risk–return impact of currency exposure on global portfolios

- The main currency hedging instruments (forwards, options, NDFs) and their payoff profiles

- When to use deliverable forwards versus NDFs, given capital controls and convertibility

- How forward points relate to interest rate differentials through covered interest parity

- How to size and directionally set up forward and NDF hedges for assets and liabilities

- The role of partial hedging and how hedge ratios reflect views and risk tolerance

- The use of options (and collars) to protect downside while retaining upside, and how premiums affect expected returns

- The mechanics of NDF fixing and cash settlement in a hard currency

- Common exam cues and pitfalls: settlement type, hedge direction, and aligning hedges with client constraints

Key Terms and Concepts

- currency risk

- forward contract

- currency option

- non-deliverable forward (NDF)

- capital controls

- hedge ratio

- moneyness

- collar

- settlement currency

- base currency

- price currency

- covered interest parity (CIP)

- forward points

- notional principal

- fixing date

- settlement date

- strike price