Learning Outcomes

This article explains how to design and evaluate currency risk management policies for globally invested portfolios, including:

- Differentiating core exam definitions of strategic (policy) hedging, tactical overlays, passive/discretionary/active currency management, and recognizing them in vignette descriptions.

- Linking stated investor objectives, risk tolerance, time horizon, and liability structure to appropriate benchmark hedge ratios by asset class and overall portfolio.

- Interpreting IPS language on policy hedges, permitted ranges, and overlay mandates, and determining whether proposed manager actions are compliant or represent policy breaches.

- Comparing full, partial, and unhedged policy choices using risk, return, cost, and behavioral “regret” arguments that commonly appear in CFA Level III questions.

- Evaluating the design of tactical FX programs, including alpha objectives, tracking‑error limits, rebalancing rules, and the choice of derivatives (forwards, futures, options).

- Identifying key implementation risks—transaction costs, cash‑flow and margin implications, counterparty and operational risk—and explaining how they affect net results.

- Working through exam-style numerical and qualitative scenarios that combine hedge benchmarks, ranges, and overlay trades to judge appropriateness and recommend adjustments.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand currency risk management within multi-asset portfolios, with a focus on the following syllabus points:

- Distinction between strategic currency policy and tactical/active currency management.

- Role of the IPS in specifying benchmark hedge ratios, ranges, and overlay authority.

- Spectrum of currency management approaches from passive hedging to active trading.

- Cost–benefit trade-offs of hedging, including transaction, funding, and opportunity costs.

- Rebalancing and monitoring of currency hedges and their impact on portfolio risk and return.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which statement best describes a strategic currency hedge?

- a) A short-term FX position based on a manager’s macro view.

- b) A long-term hedge ratio set in the IPS, largely independent of short-term views.

- c) Any hedge implemented with FX forwards.

- d) An overlay that always fully hedges all foreign currency exposures.

-

An IPS specifies a 60% policy hedge ratio for foreign bonds with a permitted range of 40%–80%. The overlay manager reduces the hedge to 20% after a large currency sell-off. From a governance standpoint, this is:

- a) Acceptable if the manager documents a strong conviction.

- b) Acceptable if the position is reversed within one month.

- c) A breach of the policy hedge range, even if it adds value ex post.

- d) Acceptable if it improves the portfolio’s Sharpe ratio.

-

Which factor most directly argues for a wider tactical hedging range around the policy hedge?

- a) Very low transaction costs and strong belief in mean reversion.

- b) High FX volatility and low tracking-error tolerance.

- c) High transaction costs and belief in momentum in currency markets.

- d) Currency risk viewed solely as a diversifier with no alpha potential.

Introduction

Currency risk arises whenever the base currency of the investor differs from the currency in which assets or liabilities are denominated. In a multi-currency portfolio, the domestic-currency return combines both the foreign asset return and the FX movement. For a portfolio of foreign assets, the domestic-currency return can be written as:

where is the return on asset in its own currency, and is the return from the change in the exchange rate for that currency versus the investor’s base currency.

Because FX movements can materially affect short- and medium-term returns, currency risk management becomes a central portfolio design decision. At Level 3, the key is to separate:

- Long-term strategic decisions embedded in the investment policy statement (IPS), such as the benchmark hedge ratio and allowed ranges.

- Short-term tactical or active decisions, often delegated to a specialist overlay manager, that vary currency exposure within those policy limits.

Key Term: strategic currency hedge

A long-term or “default” hedge ratio for foreign currency exposures set in policy (often in the IPS), reviewed infrequently, and intended to anchor FX risk regardless of short-term views. Key Term: tactical currency overlay

An active, usually shorter-horizon program that adjusts currency exposure around the strategic hedge to seek alpha or manage near-term risks, subject to IPS-defined limits.

The IPS for an institutional or private client will usually specify:

- Whether currency risk is to be hedged and at what benchmark hedge ratio.

- How much discretion managers have to deviate from this benchmark.

- Which instruments are permitted (forwards, futures, options, swaps).

- How performance will be measured and against which currency benchmark.

Exam questions often combine these elements: you may be given an IPS, a policy hedge and range, and a manager’s proposed or actual FX trades. Your task is to decide whether the actions are consistent with policy, appropriate given the investor’s objectives, and well implemented.

STRATEGIC HEDGING POLICIES

Strategic currency hedging, often termed a benchmark hedge, defines a portfolio’s neutral or standard hedge ratio for managing FX risk. For example, an institutional investor might declare a 50% hedge benchmark for all developed market currencies and a 100% hedge benchmark for high-volatility minor currencies.

The strategic hedge is chosen to reflect investor objectives, risk tolerance, asset–liability needs, and long-term beliefs about currency markets. It is not a short-term view on where a particular currency is heading; it is a structural risk decision within the overall strategic asset allocation.

Key Term: policy hedge ratio

The benchmark percentage of foreign currency exposure to be hedged, specified in the IPS as a long-term target (e.g., 0%, 50%, or 100%) for the portfolio or for specific asset classes.

Strategic hedges seek to anchor FX exposures over time and minimize the need for constant re-evaluation. They are analogous to the strategic asset allocation in that they define the long-term risk profile of the portfolio.

Choosing the Strategic Hedge Ratio

Strategic hedge ratios may be set at 0% (fully unhedged), partial (e.g., 50%), or 100% (fully hedged). The choice reflects a combination of:

-

Investor objectives and risk tolerance:

- Liability-relative investors, like defined benefit plans with domestic-currency liabilities, often favor higher hedge ratios to stabilize funded status.

- Total-return or goals-based investors may accept more FX volatility for potential diversification or alpha.

-

Time horizon:

- Over long horizons, some believe currency returns mean revert and net to roughly zero. This view supports lower hedge ratios, especially for equities.

- Over shorter horizons, FX volatility is large relative to asset returns, supporting more hedging, especially for fixed income.

-

Asset–liability characteristics:

- If liabilities are in domestic currency, hedging reduces mismatch risk between foreign assets and domestic liabilities.

- If liabilities are in multiple currencies, the policy may match liability currency weights rather than fully hedge into a single base currency.

-

Beliefs about currency markets:

- If the institution believes currency markets are efficient and alpha is hard to capture, it may adopt a simple, stable hedge rule (e.g., 100% for bonds, 50% for equities).

- If it believes there are exploitable anomalies, it may set a moderate strategic hedge and rely more on tactical overlays.

-

Cost and operational capacity:

- Hedging requires infrastructure (front/middle/back office, settlement accounts, systems). Investors with limited resources may adopt simpler or lower-frequency hedge programs.

The policy may specify different hedge ratios by asset class. A common pattern in practice:

- 0–50% hedged for foreign equities (accepting some FX risk as part of growth risk).

- 50–100% hedged for foreign bonds (FX volatility can dominate bond volatility).

- Higher hedges for currencies with extreme volatility or limited convertibility.

Strategic Hedge Bands

Strategic hedging is not just a single number. Policy typically defines not only the benchmark hedge but also a permitted deviation range (e.g., 50% hedge ±20%). This creates a governance framework within which tactical decisions can be made.

Key Term: rebalancing corridor

A range of allowed deviation around a target allocation or hedge ratio (for example, a 40%–60% permitted band around a 50% policy hedge), within which no rebalancing is required.

These bands are analogous to rebalancing corridors in strategic asset allocation:

- Tighter bands (e.g., 60% ±10%) keep FX risk closely aligned with strategic intent but reduce tactical flexibility and may increase trading costs.

- Wider bands (e.g., 60% ±25%) allow greater active risk and potential alpha but can generate larger tracking error versus the policy hedge and more pronounced FX-driven performance swings.

Factors influencing band width include:

- Transaction and implementation costs.

- FX volatility and correlation with other portfolio risks.

- Investor risk tolerance and tracking-error limits.

- Beliefs about momentum vs mean reversion in FX markets.

Exam Warning: A common CFA exam error is confusing a currency overlay mandate (which can be delegated to an active manager) with the IPS-defined hedge range. The range sets hard limits regardless of manager view. If a manager moves outside the range, it is a policy breach even if the trade is profitable ex post.

TACTICAL HEDGING POLICIES

Tactical (or active) currency overlays allow managers to adjust currency exposure opportunistically within the limits set by policy. The goal is to add value by increasing or decreasing the FX hedge ratio when forward rates, carry, or macro views are viewed as especially favorable or unfavorable.

Key Term: discretionary hedging

A hedging approach in which the manager may vary the hedge ratio around a neutral policy level within defined limits, based on judgment or signals, rather than fully neutralizing currency risk at all times.

Tactical hedging is usually implemented using short-dated forwards, futures, or options. The overlay manager may take views based on interest rate differentials (carry), valuation metrics, trend-following signals, or macroeconomic factors, typically within a range (e.g., permitted deviation from the benchmark of ±10% or ±20%).

Active overlays aim to capture incremental alpha from:

- Misalignments between spot and forward rates.

- Mean reversion in over- or undervalued currencies.

- Macro themes (e.g., policy divergence, current account trends).

- Short-term regime changes (risk-on vs risk-off).

But they also introduce:

- Model risk (signals may fail or regimes may change).

- Implementation and slippage costs.

- Operational risk from more frequent trading and complex positions.

Key Term: active currency management

A strategy that intentionally takes non-neutral currency positions, within risk limits, to generate alpha relative to a currency benchmark or policy hedge.

Tactical Hedging Constraints and Risk Budgets

Within the IPS, tactical currency overlays are usually constrained by:

- Maximum deviation from the policy hedge ratio for each currency or for the aggregate FX exposure.

- Overall FX active risk or tracking-error limits versus the currency benchmark.

- Limits on leverage, short positions, and use of options or complex structures.

- Concentration limits by currency or strategy (e.g., trend, carry, value).

These constraints define the overlay manager’s risk budget. An effective derivative of this for exam analysis:

- Start from the policy hedge and permitted ranges.

- Identify the proposed tactical position and its impact on the hedge ratio.

- Compare the resulting hedge ratio with the allowed corridor.

- Comment on whether the action fits the investor’s risk tolerance and objectives.

Key Implementation Features:

- Deviation from the benchmark (policy) FX hedge must remain within permitted bounds.

- Execution tactics, choice of instruments, and trade frequency all require monitoring for transaction and slippage costs.

- Overlay positions are monitored, marked to market, and require tight controls to avoid policy breaches and counterparty risk exposures.

Worked Example 1.1

A global endowment holds €100 million in USD and JPY assets. Its policy FX hedge benchmark is 50%, with a range of 30% to 70%. In mid-year, the portfolio manager believes the US dollar will strengthen and decides to lower the USD hedge ratio to 30%. What is allowed, and what steps should the manager take?

Answer:

The manager may tactically lower the USD hedge to 30%—the lower limit of the policy range. The change must be documented, justified using the manager’s process and market views, implemented using approved FX instruments, and closely monitored. The manager must maintain the actual hedge ratio within the 30%–70% range and have a plan either to revert gradually toward the 50% benchmark or to reassess the position as conditions change.

Passive vs Discretionary vs Active Overlays

The curriculum describes a spectrum of currency management approaches:

Key Term: passive currency hedge

A rules-based hedge that aims to keep currency exposure close to a neutral benchmark (often fully hedged) with minimal discretion, primarily to control risk and tracking error.

-

Passive hedging:

- Objective: Minimize currency risk and tracking error.

- Manager duty: Keep hedge ratio close to benchmark; limited or no directional views.

- Typical for: Fixed-income portfolios where currency risk is not desired.

-

Discretionary hedging:

- Objective: Primarily risk control, with some room to express views.

- Manager duty: Keep hedge ratio within a narrow corridor around the benchmark, occasionally leaning against or with FX moves.

- Typical for: Investors who believe some value can be added but wish to limit active risk.

-

Active currency management:

- Objective: Harvest alpha from FX markets.

- Manager duty: Use the full allowed deviation range; maintain meaningful active positions most of the time.

- Typical for: Investors granting a dedicated currency risk budget and overlay benchmark.

In exam questions, you may be asked to identify which approach is being used and whether it is consistent with the IPS language and investor preferences.

BENCHMARK HEDGE RATIOS AND RANGE POLICIES

The benchmark hedge ratio—the percentage of FX exposure to be hedged as policy—is set to balance long-term risk and return objectives. It determines the default level of FX risk, and typically a formal deviation policy is also established for permitted tactical activity.

Policy hedge selection depends on objectives, horizon, asset-liability exposures, currency views, and operational constraints to produce the benchmark hedge ratio.

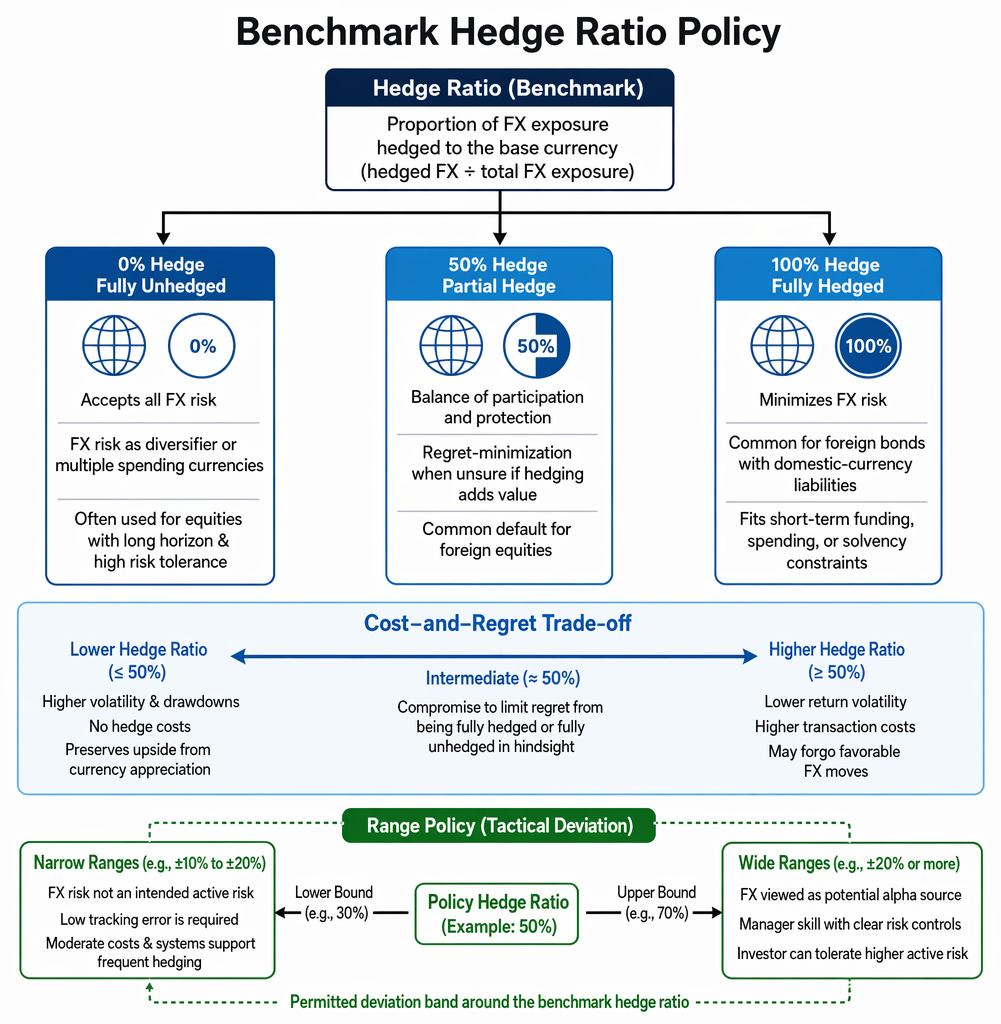

Key Term: hedge ratio

The proportion of foreign currency exposure that is hedged back into the base currency, often expressed as hedged FX exposure divided by total FX exposure for a given currency or portfolio.

Main Policy Approaches

-

Fully unhedged (0% hedge):

- Accepts all FX risk.

- Appropriate when currency risk is considered a diversifier or when the investor has multiple spending currencies.

- Often used for equity allocations by investors with very long horizons and high risk tolerance.

-

Partial hedge (e.g., 50%):

- Balances participation in currency moves with some protection from adverse FX moves.

- Common “regret-minimization” solution when the investor is unsure whether hedging will add value.

- Often used as a default for foreign equities.

-

Fully hedged (100% hedge):

- Minimizes FX risk relative to the base currency.

- Common for foreign bonds held by investors with domestic-currency liabilities, because FX volatility can dominate bond volatility.

- Appropriate when short-term funding, spending, or solvency constraints require stable domestic-currency asset values.

From a cost-and-regret standpoint:

- High hedge ratios reduce return volatility but incur higher transaction costs and may forgo favorable FX moves.

- Low hedge ratios may raise volatility and potential drawdowns, but avoid hedge costs and preserve upside from currency appreciation.

- Many institutions compromise at intermediate hedge ratios (e.g., 50%) to mitigate the risk of extreme regret from being either fully hedged or fully unhedged in hindsight.

Key Term: currency overlay benchmark

The reference hedge position (and sometimes return index) against which active currency management performance is evaluated, typically aligned with the policy hedge ratio.

Setting Range Policies

The permitted deviation or tactical range (e.g., ±20%) is essential to set clear risk boundaries and avoid over-reliance on manager market timing. It also reflects a cost–benefit analysis similar to rebalancing corridors in asset allocation:

-

Narrow ranges are favored when:

- FX risk is not a source of intended active risk.

- Tracking error relative to a reference index must be low.

- Transaction costs are moderate and systems support frequent hedging.

-

Wide ranges are favored when:

- FX is viewed as a potential alpha source.

- The overlay manager has skill and clear risk controls.

- The investor can tolerate higher active risk and episodic FX-driven underperformance.

Worked Example 1.2

A pension fund’s IPS specifies that FX overlay managers may vary the EUR hedge between 20% and 80% of non-base assets. The current hedge is 60%. If the overlay manager wishes to exploit an expected EUR rally, what is their minimum permitted hedge?

Answer:

The lowest the manager can set the EUR hedge is 20%—the lower policy bound. Reducing the hedge to 20% increases the unhedged EUR exposure and allows the portfolio to benefit if the EUR appreciates. The overlay manager must document the rationale, implement the change using permitted derivatives, and ensure that the hedge ratio does not fall below 20% at any time, even if FX movements change the actual exposure.

HEDGING IMPLEMENTATION AND OPERATIONAL CONSIDERATIONS

Strategic and tactical hedges are executed using instruments such as FX forwards, futures, and options. The choice of instrument, hedge horizon, and rebalancing frequency depend on liquidity, transaction costs, operational capabilities, and policy limits.

Key Term: currency overlay

A dedicated mandate or program, often managed by a specialist, that implements the portfolio’s currency policy and any active deviations, separate from the core asset management. Key Term: currency overlay benchmark

As defined earlier, the reference hedge position or index used to measure the overlay’s performance relative to the policy hedge.

Instruments and Mechanics

-

FX forwards:

- Most common tool for institutional hedging.

- Customized notionals and maturities.

- No initial premium; but contracts settle at maturity, causing cash inflows/outflows.

-

FX futures:

- Standardized contracts traded on exchanges.

- Marked to market daily with margin requirements.

- Useful for smaller or more standardized hedges; less flexible for specific exposure sizes.

-

Options (plain vanilla and structured):

- Provide asymmetric protection (e.g., downside protection with upside participation).

- Require upfront premium and careful cost–benefit analysis, especially for frequent tactical use.

Operationally, the manager must:

- Measure current FX exposure accurately by currency, including cash, securities, and derivatives.

- Determine target exposures (based on policy hedge and tactical positions).

- Size and execute derivative trades to move from current to target.

- Roll maturing contracts and adjust notionals for changes in portfolio value or policy.

Rebalancing: Both strategic and tactical overlays must be monitored for drift due to market moves (in asset values and exchange rates). Regular rebalancing is required to keep the hedge ratio near the policy or tactical target.

The rebalancing framework parallels that for asset allocation:

-

Calendar-based hedging: Roll and rebalance at fixed intervals (e.g., monthly or quarterly). Simple and predictable but may allow larger interim deviations.

-

Threshold-based hedging: Rebalance when the hedge ratio or FX exposure moves outside a specified corridor (e.g., plus or minus 5 percentage points). More responsive but operationally more demanding.

Key factors in setting hedge rebalancing policy include:

- FX volatility and correlation with the rest of the portfolio.

- Transaction costs and bid–ask spreads.

- Operational capacity and governance (how often can committees review and approve changes).

- Beliefs about momentum vs mean reversion (similar to the rebalancing framework in asset allocation).

Worked Example 1.3

A fund holds $200 million of foreign equities with 100% policy FX hedges. Forward contracts are rolled monthly, but a sharp equity rally causes the FX exposure to increase to $250 million before the next scheduled rebalance. What is the risk?

Answer:

Until the hedge is adjusted, the fund is under-hedged relative to its 100% policy: only $200 million of exposure is hedged, leaving $50 million unhedged. This creates unintended FX risk and potential tracking error versus the fully hedged policy benchmark. To maintain policy alignment, the manager should monitor exposures more frequently and either increase the forward notional intra-month when deviations exceed a threshold or reduce the equity exposure.

Costs, Cash Flows, and Operational Infrastructure

The costs of hedging are both explicit and implicit:

-

Trading and infrastructure costs:

- Bid–ask spreads, brokerage commissions, and market impact.

- Costs of setting up and maintaining FX trading, risk systems, and settlement processes.

- Cost of managing margin and collateral for derivatives.

-

Cash-flow volatility:

- Hedging may reduce the volatility of the domestic-currency value of assets but increase volatility of cash accounts because forward contracts settle periodically.

- This can matter for institutions with tight liquidity constraints.

-

Opportunity cost:

- A fully hedged position forgoes gains from favorable currency movements.

- Policies with partial hedges often reflect a compromise between risk reduction and maintaining upside potential.

Because of these costs, the policy typically does not aim to hedge every minor FX fluctuation. Instead, it seeks to mitigate economically meaningful risk while avoiding excessive trading.

Worked Example 1.4

A domestic investor holds £100 million of UK gilts. The IPS requires a 100% hedge of foreign-currency assets but says nothing about domestic-currency assets. The overlay manager proposes selling GBP forwards against the base currency to exploit an expected GBP depreciation. Is this consistent with a pure hedging mandate?

Answer:

No. The policy hedge applies to foreign-currency assets. Selling GBP forwards against the base currency when the asset itself is already in the base currency amounts to taking a speculative FX position unrelated to hedging. Unless the IPS explicitly allows leverage and active currency positions beyond hedging foreign exposures, this would exceed a pure hedging mandate and violate the spirit (and likely the letter) of the IPS.

Exam Warning (Implementation)

In the CFA exam, expect scenarios where benchmark and tactical hedge ratios, allowable ranges, and overlay execution policies are tested together. Always identify:

- The IPS-specified policy hedge and allowed corridor.

- What the actual or proposed hedge ratio is after trades.

- Whether that ratio is inside or outside the corridor.

- Whether the type of trade (risk-reducing vs speculative) is consistent with the mandate.

POLICY TRADE-OFFS AND PRACTICAL LIMITATIONS

Strategic and tactical currency policies must not be evaluated in isolation; they interact with the overall asset allocation, liability structure, and governance framework.

Strategic vs Tactical Approach—Checklist:

-

Strategic (policy) hedging is appropriate where:

- Risk budgets are tight and tracking error versus a domestic index must be low.

- Funding or obligations are in the base currency, as for many DB plans and insurers.

- The investor seeks stable real portfolio values and wants FX risk to be minimized or at least controlled.

-

Tactical overlays are appropriate where:

- The investor can tolerate some FX volatility and tracking error.

- There is a belief in exploitable inefficiencies in currency markets.

- Governance permits active risk-taking and performance assessment of overlay managers.

Range selection and rebalancing:

- Tighter bands (e.g., ±10%) reduce deviation risk but also limit opportunity and may raise trading frequency.

- Wider bands (e.g., ±25%) permit more alpha seeking but risk greater tracking error and larger temporary departures from the policy hedge.

- As with rebalancing asset allocations, ranges should reflect transaction costs, asset/FX volatility, correlations, and investor risk aversion.

Operational Challenges:

- Overlays add transaction, governance, and monitoring costs.

- Slippage, roll risk, and option premium costs can erode any tactical alpha.

- Systems must track exposures, reset dates, margin, and policy compliance across multiple FX instruments and counterparties.

- Illiquid or frontier currencies can be costly or difficult to hedge; proxy hedging introduces basis risk.

Currency Policy and Different Investor Types

-

Liability-driven investors (e.g., DB plans, insurers):

- Emphasis on high hedge ratios for assets supporting domestic-currency liabilities.

- Currency policy integrated with liability-hedging portfolios (e.g., high hedges for foreign bonds in the LDI bucket).

- Tactical overlays usually tightly constrained to avoid jeopardizing funded status.

-

Total-return institutions (e.g., endowments, charitable organizations):

- More flexibility to balance hedging with diversification and alpha.

- May differentiate hedging by asset class (e.g., fully hedged bonds, partially hedged equities).

- Tactical overlays can be a distinct source of active risk if governance permits.

-

Private wealth clients:

- IPS must balance behavioral preferences (e.g., discomfort with FX losses) against objectives.

- Goals-based structures may hedge currency risk differently across goal sub-portfolios (for example, lifestyle vs aspirational).

Worked Example 1.5

A charitable organization's IPS specifies:

- Base currency: USD.

- Foreign equities: 50% policy hedge, allowed range 25%–75%.

- Foreign bonds: 100% policy hedge, allowed range 90%–110%.

The current allocations and hedge ratios are:

- Foreign equities: $80 million, hedge ratio 20%.

- Foreign bonds: $40 million, hedge ratio 95%.

Evaluate compliance with policy and recommend adjustments.

Answer:

For foreign equities, the hedge ratio of 20% is below the allowed range of 25%–75%, so the position is out of compliance. The overlay manager should increase the equity FX hedge to at least 25% (and ideally back toward the 50% policy level). For foreign bonds, the 95% hedge is within the allowed 90%–110% range and is consistent with the policy objective of almost fully eliminating FX risk for bonds. The recommended action is to adjust only the equity hedge, increasing it by at least 5 percentage points of FX exposure.Revision Tip: When answering CFA questions, explicitly reference:

- The IPS policy hedge ratio and permitted range.

- The investor’s objectives and risk tolerance.

- How the proposed hedge change affects those objectives and constraints.

- The implementation and monitoring implications (costs, rebalancing, governance).

This demonstrates synthesis of policy, portfolio construction, and implementation considerations.

Summary

Effective currency risk management for global portfolios requires clear separation and integration of:

-

Strategic policy hedges:

- Long-term decisions embedded in the IPS.

- Defined benchmark hedge ratios by asset class or overall portfolio.

- Permitted ranges that reflect risk tolerance, costs, and governance.

-

Tactical overlays:

- Short-term, alpha-seeking or risk-managing deviations within policy bands.

- Use of forwards, futures, and options to adjust exposures.

- Explicit risk budgets, performance benchmarks, and monitoring.

Managers must implement hedges through approved instruments, monitor exposures and hedge ratios in real time or at agreed frequencies, and strictly conform to policy ranges to manage portfolio risk and compliance. For Level 3, the emphasis is on evaluating whether currency management choices are consistent with the IPS, investor profile, and stated risk–return objectives, and on recognizing implementation frictions that can affect net performance.

Key Point Checklist

This article has covered the following key knowledge points:

- Strategic currency hedging sets long-term policy hedge ratios that define the default level of FX risk.

- Tactical currency overlays adjust hedge ratios around the policy within IPS-defined ranges to seek alpha or manage near-term risks.

- Benchmark hedge ratios (0%, partial, 100%) and their ranges depend on investor objectives, liabilities, risk tolerance, costs, and beliefs about FX markets.

- Passive, discretionary, and active currency approaches lie on a spectrum from pure risk control to explicit alpha-seeking programs.

- Currency overlays require careful implementation using forwards, futures, and options, with ongoing monitoring, rebalancing, and cost control.

- Policy ranges and rebalancing corridors for hedges mirror asset allocation rebalancing decisions and are influenced by transaction costs and risk preferences.

- Exam analysis must always tie proposed FX actions back to the IPS, hedge ratio ranges, and the investor’s overall risk and return objectives.

Key Terms and Concepts

- strategic currency hedge

- tactical currency overlay

- policy hedge ratio

- rebalancing corridor

- discretionary hedging

- active currency management

- passive currency hedge

- hedge ratio

- currency overlay benchmark

- currency overlay