Learning Outcomes

This article explains how to evaluate the risk tolerance, governance, and investment policy of endowments, foundations, and sovereign wealth funds (SWFs) in an exam setting. It clarifies the distinguishing objectives, time horizons, and liability structures of each institution type so you can infer appropriate levels of risk, liquidity, and diversification from a vignette. It details how governance frameworks—boards, investment committees, policy documents, and delegation arrangements—shape the construction and monitoring of institutional portfolios. It outlines the essential components of an institutional investment policy statement (IPS), including return and risk objectives, constraints, strategic asset allocation, and reporting requirements, with emphasis on wording suitable for CFA Level 3 constructed-response answers. It analyzes the impact of legal, regulatory, tax, and donor or sovereign-imposed restrictions on feasible investment strategies, spending rules, and rebalancing flexibility. It further examines how differing institutional missions, payout requirements, and intergenerational equity considerations drive choices among public equities, fixed income, real assets, and alternative investments. Finally, it applies these concepts to typical CFA-style scenarios so you can justify recommended changes to risk tolerance, governance provisions, or asset allocation when institutional circumstances or objectives change.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand the unique challenges and policies of endowments, foundations, and SWFs as institutional investors, with a focus on the following syllabus points:

- Defining and contrasting the risk tolerance of endowments, foundations, and SWFs

- Recognizing the role of governance including oversight bodies, stakeholders, and fiduciary responsibilities

- Analyzing and structuring the investment policy statement (IPS) for these institutions, including objectives, constraints, asset allocation, and reporting requirements

- Evaluating the impact of external (legal, regulatory, tax) and internal (spending rules, payout requirements, legacy gifts) constraints on investment decisions

- Assessing liquidity needs, time horizons, and liability structures relevant to these institutions

- Relating investment approaches (e.g., “Norway” vs “endowment” models) to institutional objectives, scale, and governance capacity

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Compared with a typical defined benefit pension fund, which statement best describes the risk tolerance of a large, well-funded university endowment with a 4% spending rate and limited reliance on endowment income for operations?

- a) Lower risk tolerance because the endowment has no contractual liabilities

- b) Similar risk tolerance because both are perpetual institutions

- c) Higher risk tolerance because of long horizon and limited explicit liabilities

- d) Lower risk tolerance because donors are risk-averse

-

For a sovereign wealth fund mandated to stabilize government revenues from volatile commodity exports, which factor most likely reduces its risk tolerance?

- a) Weak short-term liquidity needs

- b) Low correlation between domestic economy and commodity prices

- c) High political pressure to maintain nominal fund value over short horizons

- d) Absence of any formal spending rule

-

In assessing governance quality for a large foundation planning to increase its allocation to private equity, which feature most strongly supports this strategic change?

- a) Infrequent board meetings and full board approval required for all trades

- b) A concise but regularly reviewed IPS, clear delegation to a professional investment office, and use of specialist consultants

- c) Reliance solely on volunteer trustees with limited investment experience

- d) Absence of any performance benchmarks to avoid “short-termism”

Introduction

Endowments, private foundations, and sovereign wealth funds (SWFs) are important institutional investors with distinct purposes, governance structures, and investment policy considerations. Success in managing these institutions’ portfolios hinges on clear articulation of risk tolerance, transparent governance models, and robust investment policy, all of which are core CFA Level 3 topics.

A key skill at Level 3 is to read a vignette, infer each institution’s ability and willingness to bear risk, and translate that into an IPS-style statement that is coherent with its mission, liabilities, and constraints. You are frequently required to:

- Diagnose whether risk tolerance is high, moderate, or low and justify this using specific case facts

- Evaluate governance arrangements (e.g., board structure, delegation, use of external managers) for strengths and weaknesses

- Design or amend an IPS, including strategic asset allocation and spending rules, consistent with institutional objectives

Key Term: Risk Tolerance

Risk tolerance is the maximum level of investment risk an institution is willing and able to assume to achieve its objectives, considering its mission, obligations, liquidity needs, and capacity to absorb adverse outcomes without compromising its purpose. Key Term: Investment Policy Statement (IPS)

An investment policy statement is a written policy document that formalizes an institution’s mission, investment objectives, risk tolerance, constraints, implementation guidelines, and monitoring/reporting protocol. Key Term: Mission-Driven Investing

Mission-driven investing means structuring portfolio decisions so that risk and return choices are explicitly aligned with the institution’s articulated mission and are periodically reviewed to ensure continued alignment. Key Term: Intergenerational Equity

Intergenerational equity is the principle that current and future beneficiaries should receive comparable real economic benefits from an institution’s assets, implying a focus on preserving or growing real purchasing power over time.Test Tip: When revising Risk tolerance governance and investment policy, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Institutional Overview

Endowments and foundations generally represent pools of capital accumulated through charitable donation. Their primary goal is supporting the long-term missions of entities such as universities, hospitals, museums, or social organizations, with a strong focus on intergenerational equity. They typically seek to:

- Provide a relatively stable, inflation-adjusted stream of support for operations or grants

- Preserve, and ideally grow, the real value of capital over the long run

- Reflect donor intent and legal restrictions on the use of funds

Within this group:

- Endowments are usually attached to an operating institution (e.g., a university or hospital). Spending often directly supports the operating budget.

- Private foundations are often stand-alone grant-making entities. Some are intended to exist in perpetuity; others are “spend-down” entities with a finite life.

SWFs, in contrast, are government-owned funds aiming to steward public wealth—often derived from commodity surpluses or foreign exchange reserves—for national priorities. Common SWF types include:

- Stabilization funds: Smooth government revenues and support budgets during downturns

- Savings or intergenerational funds: Transform non-renewable resource wealth into diversified financial assets for future generations

- Development funds: Finance domestic infrastructure or strategic sectors

- Reserve investment or pension reserve funds: Increase returns on excess reserves or pre-fund future pension obligations

Key Term: Sovereign Wealth Fund (SWF)

A sovereign wealth fund is a state-owned investment fund, typically funded by fiscal surpluses, commodity revenues, or foreign exchange reserves, managed for long-term national objectives such as stabilization, savings, or development.

Despite this diversity, all three institutional types must formalize how they balance risk, return, liquidity, time horizon, and external constraints within a governance framework capable of implementing and monitoring their chosen strategy.

Risk Tolerance

Institutional risk tolerance is the level of investment risk an institution is willing and able to undertake, determined by its mission, liability profile, cash flow needs, spending policies, and stakeholders’ preferences.

The exam will often require you to integrate multiple case details to judge whether risk tolerance is above average, average, or below average, and to defend that judgment.

Endowments

Generally, large university endowments exhibit high risk tolerance because:

- They have very long, often perpetual time horizons

- They typically have no contractual liabilities; spending is policy-driven, not legally fixed

- Many have diversified donor bases and ongoing fundraising, which can supplement investment returns

- They often face modest short-term liquidity needs relative to their asset base

However, risk tolerance can be materially lower if:

- The endowment funds a large share of operating budgets (e.g., 40% of university expenses)

- The sponsoring institution is financially weak or heavily reliant on stable distributions

- Spending rules or state laws impose effective minimum payouts that cannot be reduced in downturns

- Donor restrictions significantly reduce diversification (e.g., many restricted funds or large illiquid legacy holdings)

In the IPS, risk tolerance for an endowment is usually expressed as tolerance for total return volatility, sometimes with qualitative constraints such as “avoid more than a 20% decline in real value over any five-year period.”

Private Foundations

Private foundations are heterogeneous, so you must read the vignette carefully.

Factors increasing risk tolerance:

- Perpetual existence with a mission similar to an endowment

- Substantial asset base relative to annual grant-making

- Highly diversified sources of future donations (if any)

Factors reducing risk tolerance:

- Mandatory payout rules (e.g., 5% of assets annually in some jurisdictions) that must be met regardless of markets

- Finite life (“spend-down”) mandates, which create a shorter effective horizon

- Heavy reliance of grantees on stable annual funding, creating reputational and mission risk if grants must be cut

- Concentrated or illiquid positions that are difficult to reduce without major tax or reputational costs

Thus, while a perpetual grant-making foundation may resemble an endowment with medium-to-high risk tolerance, a foundation with a high statutory payout and a planned 20-year life will have lower risk tolerance and will likely hold more liquid, lower-volatility assets.

Sovereign Wealth Funds (SWFs)

SWFs are highly diverse. Their mandate is the dominant driver of risk tolerance.

-

Stabilization SWFs:

- Objective is to smooth fiscal revenues and support the budget in downturns.

- Require high liquidity and low short-term volatility because withdrawals typically occur when markets are stressed.

- Risk tolerance is therefore low-to-moderate, with a bias toward high-quality, short- to intermediate-term fixed income and cash-like assets.

-

Savings or intergenerational SWFs:

- Objective is to transform temporary resource income into a diversified, long-horizon portfolio.

- Have long investment horizons and usually no explicit short-term payout requirements.

- Can tolerate higher volatility and illiquidity, with substantial allocations to global equities, real estate, and private markets.

- Risk tolerance is typically high, subject to political and reputational considerations.

-

Development and strategic SWFs:

- Often invest domestically in infrastructure or strategic industries.

- Risk tolerance depends on the national development strategy and may be constrained by concentration and governance issues.

Reading 24 notes that SWF risk tolerance is often articulated in terms of probabilities of loss or failure to maintain purchasing power over a specified horizon (e.g., “no more than a 10% probability of real loss over five years”).

Key Term: Policy Portfolio

A policy portfolio is the institution’s strategic asset allocation—target weights to asset classes and benchmarks—designed to meet long-term return and risk objectives, usually specified in the IPS.

Across all institutional investors, risk tolerance should be reviewed regularly using scenario analysis and stress testing against spending needs, legal requirements, and reputational concerns.

Key Term: Liquidity Stress Test

A liquidity stress test is a forward-looking analysis that assesses whether the institution could meet all expected and plausible unplanned outflows in adverse markets without impairing its mission or being forced to liquidate assets at depressed prices.

Exam Focus: Integrating Risk Tolerance

When writing an IPS risk objective:

- State whether risk tolerance is above average, average, or below average

- Support this judgment with specific case facts (time horizon, spending rate, reliance on assets, size, legal requirements)

- Acknowledge offsetting factors (e.g., long horizon but high spending reliance) and conclude which dominates

Avoid generic statements that do not explicitly refer to the vignette.

Governance

Effective governance is essential for these institutions. Good governance ensures prudent fiduciary oversight, manages principal–agent problems, and clarifies decision rights. Poor governance can make even a sound policy portfolio unworkable.

Key Term: Governance Framework

A governance framework is the set of structures, roles, processes, and policies through which an institution sets investment objectives, allocates responsibilities, makes decisions, and oversees performance and risk. Key Term: Principal–Agent Problem

The principal–agent problem arises when decision-makers (agents) such as boards, investment staff, or external managers do not have perfectly aligned interests with the asset owner (principal), creating incentives for actions that may not maximize the principal’s welfare.

Key Elements of Governance

Key governance components typically include:

-

Oversight bodies:

- A board of directors or trustees with ultimate fiduciary responsibility

- An investment committee, often a subcommittee of the board, with delegated authority over investment policy

-

Documented policies:

- A comprehensive IPS capturing mission, objectives, risk appetite, and asset allocation policy

- Supporting policies on conflicts of interest, use of derivatives, ESG, and liquidity management

-

Delegation and implementation:

- Clear division of roles between board, investment committee, internal investment office, and external managers

- Delegation of day-to-day decisions (e.g., manager selection, rebalancing) to investment staff or external CIOs, while the board focuses on strategy and oversight

-

Use of external agents:

- External asset managers, consultants, and custodians

- Outsourced CIO models for smaller institutions lacking internal scale

-

Transparency and accountability:

- Regular performance and risk reporting, including benchmarks and attribution

- Clear lines of reporting and review cycles for IPS and strategy (e.g., annual review, ad hoc review after major changes)

Reading 24 emphasizes that institutional investors should avoid having boards directly manage manager hiring/firing; instead, they should focus on governance, investment policy, and strategic asset allocation, delegating implementation to an investment office or external providers.

Endowments and foundations must also handle donor-imposed restrictions, conflict-of-interest policies, and, for larger entities, often maintain a professional investment office. Governance quality partly determines how complex an investment program they can credibly undertake (for example, a small foundation with a part-time board and no staff is unlikely to manage a large alternatives program effectively).

SWFs vary: Governance structures may be embedded within ministries of finance, central banks, or stand-alone professional entities. Best practice involves:

- A clear separation between owner (the state), governing body (board), and manager (investment office)

- Explicit statements of objectives and risk appetite

- High transparency and public reporting to support legitimacy and reduce political interference

Worked Example 1.1

A mid-sized foundation has a volunteer board that meets twice per year. There is no dedicated investment staff; an external consultant provides advice, and managers invest in commingled funds. The foundation is considering a 40% allocation to private equity and hedge funds, requiring complex due diligence and ongoing monitoring.

Should the governance structure be considered adequate for this strategy?

Answer:

Governance appears weak relative to the proposed complexity. A volunteer board meeting infrequently, with no internal investment office, is unlikely to oversee a large alternatives allocation effectively. The principal–agent problem is amplified because external managers would exercise considerable discretion with limited oversight. Before increasing allocation to complex illiquid strategies, the foundation should strengthen governance—e.g., establish an investment committee with relevant investment experience, increase meeting frequency, possibly hire staff, and formalize due diligence and monitoring procedures in the IPS.

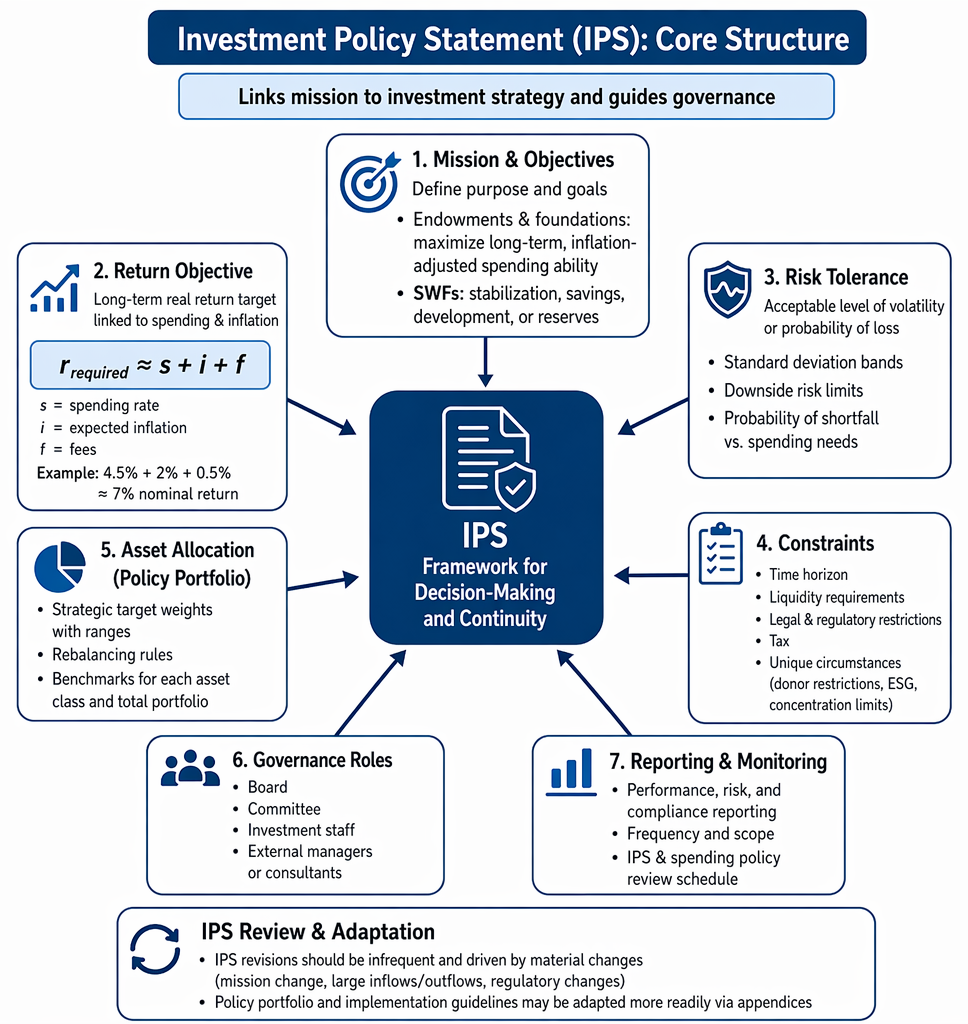

Investment Policy Statement (IPS): Structure and Objectives

The IPS provides a framework for sound decision-making and continuity across generations. It is the central governance document that links the institution’s mission to its investment strategy.

Risk tolerance determination incorporates mission, time horizon, portfolio reliance, funding flexibility, and legal, donor, or sovereign constraints.

Key IPS elements for endowments, foundations, and SWFs include:

-

Mission and objectives:

- For endowments and foundations, typically maximizing long-term, inflation-adjusted spending ability (intergenerational equity), net of fees and inflation

- For SWFs, objectives may include stabilization, savings, development, or reserve management

-

Return objective:

- Often expressed as a long-term real return target linked to spending and inflation

A common approximation is:

where:

- = long-run spending rate (including any mandatory payout)

- = expected long-run inflation for relevant costs

- = investment management and administrative fees (if charged to the fund)

For example, a university endowment with a 4.5% spending rate, 2% expected inflation, and 0.5% fees would require approximately a 7% nominal return.

-

Risk tolerance:

- Explicit statement of the acceptable level of volatility or probability of loss (e.g., standard deviation bands, downside risk limits, or probability of shortfall relative to spending needs)

-

Constraints:

- Time horizon, liquidity requirements, legal and regulatory restrictions, tax, and unique circumstances (donor restrictions, ESG preferences, concentration limits)

-

Asset allocation (policy portfolio):

- Strategic target weights and rebalancing rules, with clearly defined ranges for each asset class

- Benchmarks for each asset class and for total portfolio performance

-

Governance roles:

- Roles and responsibilities for board, committee, investment staff, and external managers or consultants

-

Reporting and monitoring:

- Frequency and scope of performance, risk, and compliance reporting

- Schedule for reviewing the IPS and spending policy

Reading 24 emphasizes that IPS revisions should be infrequent and driven by material changes in circumstances (e.g., mission change, large inflows/outflows, or regulatory changes), whereas the policy portfolio and implementation guidelines may be adapted more readily via appendices.

Worked Example 1.2

A private university endowment has a 2 billion portfolio, a 10-year-plus time horizon, and a goal to maintain purchasing power while spending 4.5% per year. Trustees are considering a major shift to private equity and infrastructure assets after recent strong public equity returns. Should they increase their risk tolerance?

Answer:

The endowment enjoys a long time horizon, perpetual mission, and flexible (non-mandatory) spending. Its ability to bear risk is high, especially if the university’s operating budget is not overly dependent on endowment distributions. Provided that liquidity is managed (e.g., limiting illiquid commitments relative to total assets and anticipated cash needs), increasing risk tolerance and allocating more to growth and illiquid assets may be justified. IPS amendments should:

- Document the higher risk tolerance and rationale

- Define target ranges and limits for illiquid assets

- Trigger updated stress tests of spending under adverse scenarios

- Ensure the board understands and accepts greater portfolio volatility and potential short-term drawdowns

Worked Example 1.3

A SWF in a commodity-exporting country is mandated mainly for budget stabilization but, after several years of surplus, wishes to diversify into equities. How should governance address this transition?

Answer:

Governance must first clarify whether the fund’s primary purpose remains stabilization or whether a dual stabilization–savings mandate is now intended. If stabilization remains primary, the IPS should keep the majority in liquid, low-volatility assets and strictly limit equity exposure. If a dual mandate is adopted, a sensible approach is to create separate sub-portfolios:

- A stabilization tranche invested conservatively (short-term government bonds, high-grade credits) with clear rules for withdrawals and replenishment

- A savings tranche with a higher allocation to global equities and alternatives, managed to a long-term real return target The IPS should define objectives, risk tolerance, benchmarks, and governance arrangements for each tranche, with separate reporting to improve transparency and accountability.

Exam Warning: In CFA Level 3, do not assume all endowments and foundations share identical risk tolerance or liquidity. Assess the specifics—payout rules, donor restrictions, reliance on distributions, and legal requirements may lead to very different constraints and attitudes toward risk. Similarly, SWF risk tolerance is determined by its mandate (stabilization versus savings), the volatility of funding sources, and political tolerance for losses.

Spending Policy and Constraints

Endowments and most private foundations use a payout or spending policy—often a percentage of trailing average market value—to balance current support with intergenerational equity.

Key Term: Spending Rule

A spending rule is a policy defining how much of an endowment or charitable organization’s assets may be distributed each year, typically as a percentage of market value, aimed at balancing current needs with preservation of real capital.

In some jurisdictions, private foundations are legally required to spend at least a certain percentage of assets each year (e.g., 5% in the United States). Endowments usually set spending in the 3–5% range but often have flexibility to adjust.

Common spending rules:

- Simple spending rule: Fixed percentage of beginning-of-year market value (e.g., 4% of MV at prior year-end). Simple and responsive to changes in asset value but produces volatile spending.

- Moving-average rule: Percentage applied to a multi-year average market value (e.g., 4% of average MV over the prior three years), smoothing payouts but introducing a lag.

- Hybrid rule: Weighted average of last year’s spending (with an inflation adjustment) and a percentage of current market value (e.g., 70% last year’s spending plus inflation, 30% of 4% of current MV). This combines stability and responsiveness.

Higher mandatory payouts or defined lifespans:

- Reduce risk tolerance (less ability to absorb volatility without jeopardizing mission)

- Require higher allocations to liquid assets to fund distributions, rebalancing, and contingency needs

- Limit the feasible allocation to illiquid alternatives, especially for smaller funds

Donor-imposed restrictions, state laws, or government policies further influence the investible universe and rebalancing flexibility (e.g., prohibiting certain asset classes or imposing minimum quality standards).

Liquidity constraints should be mapped to:

- Expected and potential spending (including stressed scenarios)

- Expected contributions or inflows (donations, tax transfers, commodity revenues)

- Rebalancing and collateral needs (especially when derivatives are used)

- Contingent obligations (e.g., guarantees or backstop commitments)

SWFs aimed at stabilization must maintain significant liquidity—often in government bonds and cash—to meet fiscal needs when commodity prices or economic activity fall. Savings-focused SWFs and perpetual endowments, by contrast, can accept more illiquidity to capture long-run growth.

Worked Example 1.4

A private charitable foundation has 200 million in assets and must, by law, distribute at least 5% of assets each year. It has adopted a moving-average spending rule of 5% of the prior three-year average market value. Donors have placed restrictions on 30% of assets, requiring investment only in investment-grade bonds. How do these factors affect risk tolerance and liquidity?

Answer:

The statutory minimum 5% payout and the moving-average rule create a relatively predictable but non-discretionary cash outflow, reducing risk tolerance and increasing liquidity needs. The foundation must maintain sufficient liquid assets (e.g., investment-grade bonds, listed equities) to meet spending even in downturns. Donor restrictions on 30% of assets further constrain the investible universe, limiting diversification and forcing a sizable high-quality bond allocation. Overall, risk tolerance is likely moderate at best, not high, despite the absence of explicit liabilities. The IPS should reflect:

- A conservative liquidity buffer to cover at least one to two years of spending

- Asset allocation ranges that ensure sufficient high-quality fixed income and cash

- A statement that donor-restricted assets are managed according to their specific constraints and cannot be used to increase overall portfolio risk unduly

Asset Allocation

Strategic asset allocation (SAA) is the primary determinant of long-term risk and return for institutional portfolios. It must be consistent with the institution’s risk tolerance, spending rules, and liquidity needs.

For endowments, foundations, and SWFs, common patterns include:

-

Long-horizon, perpetual funds (large endowments, savings SWFs):

- Can hold large allocations to equities, private markets, real assets, and other return-seeking assets

- Often follow an “endowment model” with high allocations to alternatives and significant active management

-

Shorter-horizon, development, or mandatory-payout foundations:

- Need to balance growth with capital preservation and liquidity

- May lean toward a “Norway model” (heavier use of public markets, often passive) to keep costs low and governance simpler

-

Stabilization SWFs:

- Focus on liquid, low-volatility assets; equities and illiquid alternatives play a limited role

- Asset allocation is often heavily skewed to high-quality sovereign bonds and cash

Key Term: Endowment Model

The endowment model is an investment approach characterized by high allocations to alternative investments (private equity, hedge funds, real estate), significant use of active management, and externally managed assets, suited to institutions with long horizons, high risk tolerance, and strong governance capabilities. Key Term: Norway Model

The Norway model is an investment approach emphasizing broad exposure to public equities and bonds, primarily through low-cost, passively managed portfolios with tight tracking error limits and modest use of alternatives.

Reading 24 highlights that scale, investment horizon, and governance capability are critical in determining whether an institution can successfully implement an endowment-style or Norway-style approach.

Governance should specify:

- Strategic target weights to each asset class

- Allowable ranges and any constraints on illiquidity, leverage, or concentration

- Rebalancing rules (time-based or threshold-based) and how cash flows are used to rebalance

- Benchmarks for each asset class and the total portfolio

Worked Example 1.5

A university endowment currently follows a Norway-style approach: 55% public equities, 40% investment-grade bonds, 5% private real estate, largely passively managed. The CIO argues that this approach will not preserve purchasing power given a 4.5% spending rule, 2% inflation, and 0.5% fees. He proposes moving to an endowment model with a higher allocation to private equity and other alternatives, managed by external specialists.

What institutional characteristics would support this shift?

Answer:

An effective shift toward the endowment model requires:

- Scale: A 12 billion endowment (as in the Janson University example in Reading 24) has sufficient capital to access top-tier alternative managers and diversify across strategies.

- Investment horizon: A perpetual horizon and relatively low short-term liquidity needs support higher allocations to illiquid assets.

- Governance framework: A robust governance structure with a dedicated investment office, an experienced investment committee, and the ability to hire and monitor external managers and consultants. If these conditions are met, increasing allocations to private investments may raise expected returns to meet the required nominal return (approximately 7% in this case). The IPS should be updated to reflect:

- A revised strategic asset allocation with explicit ranges for alternatives

- Illiquidity limits (e.g., maximum percentage committed to private investments)

- Stronger governance and reporting requirements for alternative portfolios

Worked Example 1.6

A stabilization SWF holds 80% in short-term government securities and 20% in global equities. The ministry of finance wants to increase equity exposure to 40% to “chase higher returns,” despite frequent drawdowns during commodity downturns. How should the fund’s risk tolerance and asset allocation be evaluated?

Answer:

A stabilization SWF’s primary role is to support the budget when commodity prices fall—precisely when global equities and risk assets also tend to perform poorly. Its ability to take equity risk is therefore limited by:

- High and unpredictable liquidity needs during downturns

- Political and social intolerance for losses at times of fiscal stress

- The correlation between commodity revenues and market returns Increasing equity exposure could materially impair its ability to perform its stabilization role. The IPS should reaffirm a conservative risk tolerance and clarify that:

- The stabilization tranche must prioritize capital preservation and liquidity

- Any higher-risk, return-seeking investments should be placed in a separate savings tranche with a distinct mandate and governance The proposed 40% equity allocation may be suitable for a savings tranche but not for the stabilization fund itself.

Summary: Institutional Characteristics

Instead of memorizing a table, it is more useful to internalize the patterns across key dimensions.

-

University endowment:

- Risk tolerance: Generally high, due to long horizon, limited explicit liabilities, and ability to accept volatility; moderated if the university is heavily dependent on endowment income.

- Governance: Board of trustees and investment committee; larger endowments often have professional investment offices and can adopt complex endowment-model strategies.

- IPS focus: Perpetual mission, real-return objective linked to spending (e.g., inflation plus 3–5%), emphasis on growth assets and alternatives, intergenerational equity.

-

Private charitable foundation:

- Risk tolerance: Medium to high for perpetual foundations with modest payout; lower for spend-down or high-mandatory-payout foundations.

- Governance: Board, often with legal and regulatory oversight; governance quality and scale vary widely. Heavy influence of donor wishes.

- IPS focus: Grant-making or operating support, payout constraints, donor restrictions, legal minimum spending, appropriate asset allocation balancing growth with liquidity and capital preservation.

-

Sovereign wealth fund (SWF):

- Risk tolerance: Highly variable; low to moderate for stabilization funds, high for savings funds, mandate-dependent for development funds.

- Governance: State owner (parliament/government), board or council, and investment office; must manage political influence and ensure transparency.

- IPS focus: Explicit mandate (stabilization, savings, development), asset–liability or asset–fiscal alignment, public accountability, risk measures (probability of loss, tracking to real return objectives).

Key Point Checklist

This article has covered the following key knowledge points:

- Compare the risk tolerance, liquidity, and horizon of endowments, foundations, and different types of SWFs, using case facts to justify your conclusions

- Identify governance structures and documentation (IPS, committees, roles, delegation) that support or undermine complex investment strategies

- Structure clear IPS statements for institutional investors, including mission, return objective, risk tolerance, constraints, strategic asset allocation, and monitoring/reporting provisions

- Distinguish the differing legal, regulatory, tax, and donor or sovereign constraints impacting each institution type and how these shape asset allocation and spending policy

- Assess how spending rules, payout requirements, and liquidity needs influence portfolio construction, use of alternatives, and risk management tools such as stress testing

- Relate investment approaches such as the Norway and endowment models to institutional characteristics like scale, horizon, and governance capacity

Key Terms and Concepts

- Risk Tolerance

- Investment Policy Statement (IPS)

- Mission-Driven Investing

- Intergenerational Equity

- Sovereign Wealth Fund (SWF)

- Policy Portfolio

- Liquidity Stress Test

- Governance Framework

- Principal–Agent Problem

- Spending Rule

- Endowment Model

- Norway Model