Learning Outcomes

This article explains hedge fund and liquid alternative performance evaluation and replication, including:

- Decomposing hedge fund and liquid alternative returns into traditional market betas, alternative risk premia, manager-specific alpha, leverage effects, and layered fees, and relating each component to observed performance statistics

- Measuring and interpreting risk when returns are non-normal, autocorrelated, and affected by illiquidity, and recognizing when standard deviation, tracking error, and VaR understate true downside and tail risk

- Evaluating the suitability, interpretation, and limitations of traditional and alternative performance metrics—Sharpe, Sortino, maximum drawdown, drawdown duration, and upside/downside capture ratios—for different hedge fund and liquid alternative strategies

- Identifying and assessing hedge fund and liquid alternative benchmarks, including how index construction, survivorship and backfill biases, and investability constraints can distort peer comparisons and manager appraisal

- Explaining factor-based (direct) and holding-based (indirect) replication approaches, including their mechanics, data requirements, model risks, and reasons replication may diverge from actual hedge fund or index performance

- Applying these concepts to CFA Level 3–style vignettes to interpret reported results, question benchmark and replication choices, and justify conclusions about manager skill, risk, and suitability for client objectives

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand hedge fund and liquid alternative performance evaluation and replication, with a focus on the following syllabus points:

- Assess the composition and drivers of hedge fund and liquid alternative returns

- Measure and interpret risk and performance accurately for these strategies, given non-normal and autocorrelated returns

- Explain and evaluate returns-based and holdings-based performance attribution when applied to hedge funds

- Explain common and advanced replication methods for hedge fund returns

- Identify the challenges and limitations of benchmarking and replication for alternative investments

- Evaluate manager skill, benchmark choice, and replication claims in an integrated, portfolio-level context

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which feature most often makes hedge fund performance measurement more challenging than for traditional long-only equity funds?

- a) Use of broad equity benchmarks such as the S&P 500

- b) High turnover in highly liquid listed securities

- c) Non-normal, serially correlated returns arising from illiquidity and derivatives

- d) Lower management fees relative to mutual funds

-

What is the primary risk when using a self-reported hedge fund index as a benchmark for an individual hedge fund?

- a) The index return will always exceed the fund’s return

- b) The index may be subject to survivorship, backfill, and selection biases

- c) The index is too diversified across strategies

- d) The index is fully investable and therefore understates realistic costs

-

Which statement best distinguishes direct and indirect hedge fund replication and correctly identifies one limitation of each?

- a) Direct = holding-based, limited by reporting lags; Indirect = factor-based, limited by model risk

- b) Direct = investing in hedge funds, limited by capacity; Indirect = buying ETFs, limited by liquidity

- c) Direct = factor-based, limited by inability to capture manager-specific alpha; Indirect = holding-based, limited by stale and incomplete position data

- d) Direct = using swaps, limited by counterparty risk; Indirect = using futures, limited by margin requirements

-

A liquid alternative fund claims to replicate a broad hedge fund index using liquid, transparent instruments. Which pair of methods is it most likely to employ?

- a) Bottom-up fundamental security analysis and activist engagement

- b) Factor-based regressions on hedge fund index returns and rules-based portfolios of futures/ETFs

- c) Private equity co-investments and leveraged bank loans

- d) Long-only value and growth tilts within a developed equity index

Introduction

Hedge funds and liquid alternatives require special attention in performance analysis. Unlike traditional funds, these vehicles often use diverse asset classes, active timing, borrowing, short selling, and illiquid or difficult-to-value holdings. As a result, standard risk and return metrics may not provide a full picture. CFA Level 3 questions focus on return drivers, risk measures, replication, and the use of benchmarks, often requiring you to integrate these elements when judging whether results are consistent with a manager’s stated strategy and objectives.

Key Term: hedge fund

An actively managed investment fund using broad mandates, with the flexibility to take long and short positions, use derivatives, and apply borrowed funds, typically in pursuit of absolute or risk-adjusted return targets. Key Term: liquid alternative

An investment product, often structured as a mutual fund or ETF, designed to offer hedge fund–like strategies and risk exposures but with higher liquidity, tighter leverage limits, and greater regulatory transparency. Key Term: hedge fund replication

The process or strategy of recreating the risk/return characteristics of a hedge fund or hedge fund strategy using rules-based, investable portfolios (often of liquid instruments) rather than direct investment in actual hedge funds.Test Tip: When revising Performance evaluation and replication, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Why performance evaluation is different

Several features distinguish hedge funds and liquid alternatives from traditional long-only funds:

- Use of short positions and derivatives to create non-linear payoffs (e.g., option-writing strategies)

- Heavy reliance on leverage to increase modest base premia

- Exposure to illiquid and infrequently priced securities, leading to smoothed returns

- Broad, dynamic opportunity sets across asset classes, geographies, and instruments

- Layered fee structures, often including performance-based incentive fees with high-water marks

These features:

- Complicate risk measurement (because return distributions are often non-normal and path-dependent)

- Make benchmark selection more subjective and prone to bias

- Create scope for replication using more transparent, liquid building blocks

Level 3 questions typically present you with partial information about a fund’s strategy and track record, then ask you to identify what the reported statistics do and do not reveal, whether the benchmark or replication approach is appropriate, and how to adjust your judgment accordingly.

Key Term: non-normal return distribution

A return distribution that is skewed or exhibits fat tails relative to the normal distribution. For hedge funds and liquid alternatives, non-normality often arises from option-like strategies, leverage, and return smoothing from illiquid holdings. Key Term: autocorrelation

The correlation of a return series with its own lagged values (e.g., this month’s return with last month’s return). Positive autocorrelation often signals return smoothing due to illiquidity, stale prices, or subjective valuations.

Drivers and Measurement of Hedge Fund and Liquid Alternative Returns

Hedge fund and liquid alternative strategies are heterogeneous, but several return drivers are common:

- Traditional equity and bond betas, often with reduced or dynamically managed exposure relative to standard funds

- Alternative risk premia, such as volatility, merger arbitrage, event, illiquidity, or credit spreads

- Alpha from manager skill in security selection, trading, or style timing

- Use of borrowing and derivatives for risk or return amplification

- Fee structures, including management fees and performance-based incentive fees

Key Term: alternative risk premia

Systematic sources of return beyond traditional equity and bond market betas, such as value, momentum, carry, volatility, merger arbitrage, and credit premia, that can often be harvested through rules-based long–short strategies.A useful decomposition for exam purposes is:

where:

- is the risk-free rate

- is traditional market beta exposure

- are exposures to alternative risk premia factors

- is manager-specific skill (idiosyncratic alpha)

- fees reflect management and incentive charges

In practice, much of what is labelled “hedge fund alpha” is explained by alternative premia and dynamic beta management rather than pure stock-picking skill.

Key Term: high-water mark

A provision in many hedge fund incentive fee arrangements under which performance fees are charged only on new net profits above the previous peak in net asset value. Key Term: hurdle rate

The minimum return (often a cash rate or cash plus a spread) that a hedge fund must earn before charging a performance fee. High-water marks and hurdles affect the time pattern and optionality of incentive fees and can create incentives for risk-taking after drawdowns—issues that may be explored in exam vignettes.

Because of these complexities, superficial application of traditional evaluation metrics (Sharpe ratio, standard deviation, tracking error, etc.) may mislead.

Performance Measurement Considerations

Assessing hedge fund and liquid alternative performance requires adaptation beyond the standard long-only toolkit.

Volatility and smoothing

-

Standard deviation of monthly returns often understates true economic risk because:

- Illiquid positions may be priced infrequently or using models, leading to stale or smoothed valuations.

- Managers may be conservative in marking down positions during stress, resulting in artificially low volatility and positive autocorrelation.

-

Positive autocorrelation implies that simple standard deviation understates the variability that would be observed if prices were marked to market continuously. For the exam, serial correlation in returns is a strong cue to question reported risk metrics.

Sharpe versus downside-focused measures

The Sharpe ratio remains a central appraisal measure:

But for hedge funds and liquid alternatives:

- Smoothed returns can overstate Sharpe ratios by depressing without reducing true downside risk.

- Symmetric volatility penalizes upside and downside equally, which is inconsistent with most investors’ preferences when distributions are skewed.

The Sortino ratio is sometimes more informative:

where is the standard deviation of downside returns only (returns below a target such as or zero). Strategies such as option-writing may show high Sharpe ratios but low Sortino ratios once large drawdowns are included.

Key Term: maximum drawdown

The largest peak-to-trough decline in portfolio value over a given period, expressed as a percentage of the peak. Key Term: drawdown duration

The time elapsed from a portfolio peak until the value fully recovers to that peak. For path-dependent, capital-preservation-oriented strategies, maximum drawdown and drawdown duration often convey more about investor experience and risk tolerance than annualized volatility. Level 3 questions may ask you to reconcile a modest standard deviation with an unacceptably deep or prolonged drawdown.

Other useful measures include:

- Upside and downside capture ratios relative to an equity index (e.g., how much of the market’s up/down moves the strategy participates in)

- Value at Risk (VaR) and expected shortfall for tail risk, acknowledging model limitations under non-normality

Key Term: upside/downside capture ratio

A metric comparing a strategy’s average return in periods when a benchmark is up (or down) to the benchmark’s average return in those periods.

Fees and layers of costs

Hedge funds and some liquid alternatives charge:

- An annual management fee on assets (e.g., 1%–2%)

- A performance or incentive fee (e.g., 15%–20% of profits over a hurdle, subject to a high-water mark)

Funds of hedge funds and some multi-manager liquid alts add an extra layer of fees on top of constituent managers. For exam purposes:

- Always interpret returns net-of-fees for the investor.

- Be prepared to compare a high-fee hedge fund versus a lower-cost replication or liquid alternative, discussing whether any observed outperformance appears sufficient and consistent with genuine skill.

Worked Example 1.1

A candidate is asked to assess the quality of a hedge fund manager's performance relative to an index. The manager reports a Sharpe ratio of 1.2, a standard deviation of 5%, and a maximum drawdown of 11%, with returns showing significant serial correlation.

Answer:

The Sharpe ratio and standard deviation may understate economic risk because positive autocorrelation suggests smoothed returns, likely due to illiquid or difficult-to-value assets. A relatively low maximum drawdown is positive, but the serial correlation implies that shocks may be underrepresented in the sample. For CFA Level 3, you should:

- Highlight that non-normal, autocorrelated returns make volatility-based measures less reliable.

- Emphasize the role of maximum drawdown and drawdown duration as additional risk metrics.

- Question whether the benchmark appropriately reflects the fund’s factor exposures and illiquidity risk.

Benchmarking and Its Pitfalls

Hedge fund and liquid alternative benchmarks are difficult to construct and interpret.

Key Term: survivorship bias

Bias introduced when poorly performing funds that close or stop reporting are dropped from an index, causing historical returns to be overstated. Key Term: backfill bias

Bias that occurs when successful funds join a database and add their attractive prior track records (instant history), inflating historical index performance.

Index construction issues

Most hedge fund indexes rely on manager self-reporting, with common consequences:

- Self-selection: Managers choose whether to report, and often stop reporting after poor performance.

- Survivorship bias: Defunct or liquidated funds fall out of the index, making past returns look better than a truly investable universe.

- Backfill bias: New entrants may contribute only successful prior histories.

- Heterogeneity: Broad “hedge fund” indexes combine strategies with very different risk profiles (e.g., market-neutral, macro, distressed).

Moreover, many hedge fund indexes are not fully investable (no index fund or investable vehicle exists that perfectly tracks them net of realistic fees and capacity limits). This violates a key property of a good benchmark.

When evaluating benchmark quality, you should recall that effective benchmarks for performance evaluation should be:

- Unambiguous and clearly defined

- Investable

- Measurable

- Appropriate to the manager’s style and process

- Specified in advance

- Owned (accepted) by both sponsor and manager

Hedge fund databases and style indexes often fail on investability and, at times, on appropriateness and clarity.

Style and misfit risk

If a long–short equity hedge fund is evaluated against a broad equity index such as the MSCI World, the benchmark will:

- Ignore the fund’s ability to profit from both longs and shorts

- Confound style effects (e.g., value, momentum, small-cap tilts) with active management

Using the notation from performance evaluation:

where:

- is the portfolio return

- is the market index return

- is the style return (benchmark minus market)

- is the active management return (portfolio minus benchmark)

If the benchmark does not match the fund’s actual style (e.g., it uses a broad market index when the fund is equity market–neutral value), and become conflated, and appraisal of true skill is distorted. In the hedge fund context, this misfit is common and must be explicitly recognized in exam answers.

Worked Example 1.2

An investor compares a market-neutral hedge fund’s performance to a broad equity index. Over three years, the hedge fund earns 6% annually with 4% volatility, while the equity index earns 10% with 16% volatility. The investor concludes that the hedge fund manager exhibits poor skill because of underperformance versus the equity index.

Answer:

The conclusion is inappropriate because the benchmark does not reflect the fund’s style. The market-neutral fund is designed to deliver low-volatility, low-correlation returns, not to track equity upside. Using a long-only equity index: Misclassifies the fund's style (

is non-zero but ignored). Attributes the fund's lower return to poor active management (

), when it largely reflects intentional beta reduction. In an exam response, you should recommend a benchmark that reflects the fund’s mandate—such as cash plus a spread or a market-neutral style index—and reframe performance in risk-adjusted terms (e.g., Sharpe, downside capture, drawdowns) rather than simple excess return over an equity index.

Hedge Fund and Liquid Alternative Replication

Replicating hedge fund performance aims to deliver similar return/risk characteristics using transparent, liquid, rules-based approaches. Replication can serve two main roles:

Infrequently priced positions can induce serially correlated reported returns that mask drawdown risk and bias risk-adjusted performance metrics upward.

- As a cheaper, more liquid investment alternative for investors seeking exposure to broad hedge fund–like risk premia

- As an analytic tool to decompose hedge fund returns into factor exposures and potential alpha

There are two primary methods:

Key Term: factor-based replication

A replication approach that builds a portfolio whose exposures to tradable risk factors (e.g., equity beta, credit spreads, volatility, trend) mimic those historically observed for an aggregate hedge fund or liquid alternative strategy, often using regression-based estimates. Key Term: holding-based replication

A replication approach that attempts to mimic hedge fund returns by reproducing actual holdings or disclosed positions, with adjustments for liquidity, regulatory constraints, and incomplete information.

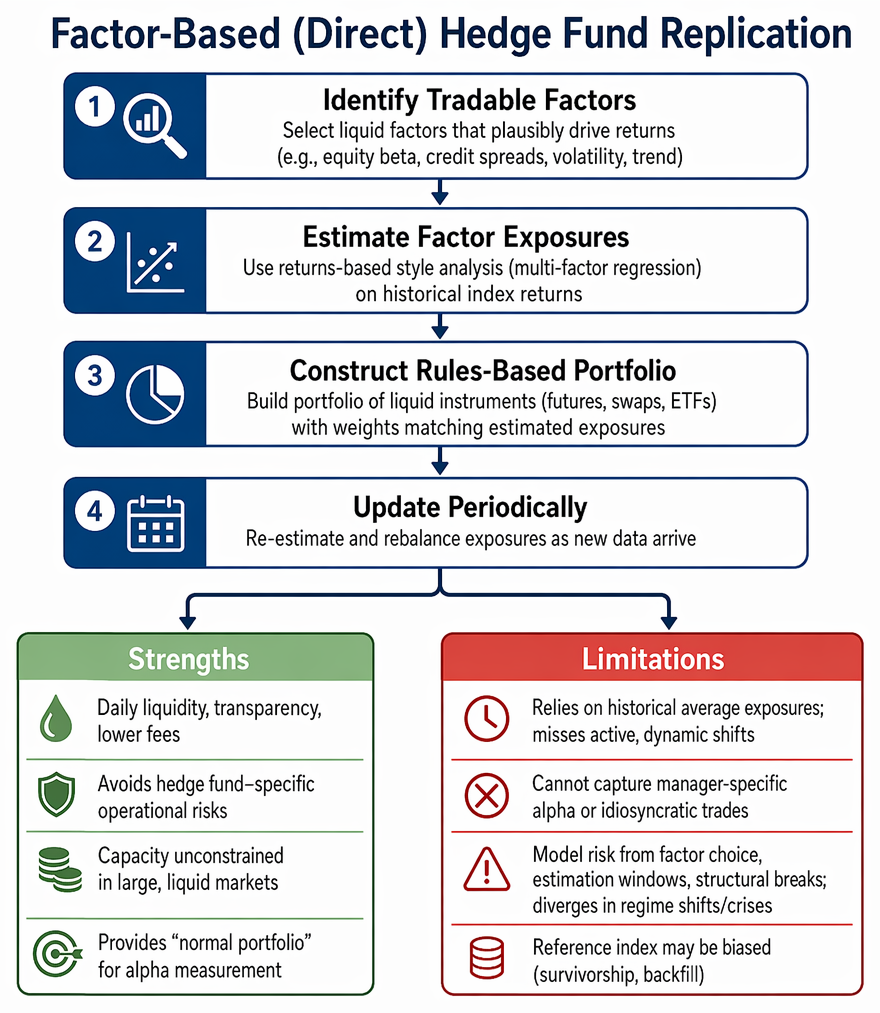

Direct (factor-based) replication

Factor-based replication is often called direct replication because it directly targets the statistical relation between hedge fund returns and observed factors.

Mechanics:

- Identify a set of tradable factors (e.g., equity indexes, bond indexes, credit spread indexes, volatility futures, trend-following strategies) that plausibly drive returns of a given hedge fund index or style.

- Use returns-based style analysis (typically multi-factor regression) on historical index returns to estimate factor sensitivities.

- Construct a rules-based portfolio of liquid instruments (futures, swaps, ETFs) whose weights approximate the estimated factor exposures.

- Update exposures periodically as new data arrive.

Strengths:

- Offers daily liquidity, transparency, and potentially lower fees compared with direct hedge fund investments.

- Avoids hedge fund–specific operational risks (gating, side pockets, key-person risk).

- Can be capacity unconstrained relative to individual hedge funds, since it trades in large, liquid markets.

- Provides a useful “normal portfolio” against which to measure individual hedge fund alpha.

Limitations:

- Relies on historical average exposures; it does not capture active, dynamic shifts in positioning or idiosyncratic trades.

- Cannot replicate true manager-specific alpha, such as superior event analysis or security selection.

- Model risk: factor choices, estimation windows, and structural breaks can cause replication to diverge from actual hedge fund performance, especially around regime shifts or crises.

- The reference index being replicated may itself be biased (survivorship, backfill), so “successful” replication of a biased index is not necessarily desirable.

Indirect (holding-based) replication

Holding-based replication is sometimes labelled indirect replication because it uses inferred holdings to approximate trades.

Mechanics:

- Use publicly disclosed holdings (e.g., regulatory filings, reports from liquid alternative funds with hedge fund–like styles) to estimate the hedge fund’s portfolio.

- Recreate a similar portfolio, possibly adjusting for position size limits, liquidity constraints, or regulatory rules.

- Rebalance as new holdings data become available.

Strengths:

- Can target specific strategies or high-profile funds when position transparency is sufficient (most often in long-only or constrained strategies).

- Potentially captures some security-selection alpha embedded in disclosed positions, at least on the long side.

Limitations:

- Reporting lags mean that disclosed holdings may be weeks or months out of date, missing tactical trades and short-term opportunities.

- Short positions and derivative exposures are often not disclosed, so replication based on long disclosures may materially misrepresent net exposures.

- High turnover strategies or those using complex derivatives are poorly suited to holdings-based cloning.

- Managers may deliberately “window dress” holdings at reporting dates, reducing the informativeness of disclosures.

Holding-based replication therefore tends to be more credible for relatively transparent, lower-turnover, long-biased strategies (e.g., some equity long–short with low turnover) and less so for macro, high-frequency, or heavily derivative-based funds.

Worked Example 1.3

A liquid alternative mutual fund claims to "replicate" a leading multistrategy hedge fund index. The manager explains that the replication engine uses factor-based exposures to equities (beta), credit spreads, trend-following commodities, and implied volatility from liquid indices.

You are asked to:

- Identify two potential risks in this replication approach.

- Explain how you would interpret persistent performance differences between the replicator and the reference hedge fund index.

Answer:

Potential risks include:

- Model risk and regime shifts: The factor model is calibrated on historical relationships. If hedge fund managers change styles, add new strategies, or significantly alter leverage in response to market conditions, the historical factor loadings may no longer describe future behaviour. Replication is likely to diverge during such transitions.

- Missing alpha and strategy heterogeneity: The replicator cannot capture idiosyncratic opportunities (e.g., complex restructurings, private deals, off-the-run securities) that contribute to true hedge fund alpha. It also assumes that an aggregate index can be represented by a relatively small set of liquid factors, which may be overly simplistic. When interpreting performance differences, you should:

- Distinguish between periods when the replicator tracks broad risk premia well (suggesting limited incremental alpha in the index) and periods when large deviations arise (which might reflect manager skill, strategy dispersion, or model failure).

- Avoid concluding that close tracking implies “no value in active management” or that the replicator is “equivalent” to a diversified hedge fund portfolio. Instead, emphasize that replication captures long-run factor exposures but will likely underperform in tail events and miss manager-specific alpha.

Replication and liquid alternatives

Many liquid alternative funds marketed to retail investors effectively implement hedge fund replication:

- Some pursue factor-based replication of hedge fund indexes (e.g., “hedge fund beta” products).

- Others use rules-based alternative premia strategies (e.g., long–short value, momentum, carry, volatility) that resemble building blocks of hedge fund returns.

- A smaller subset attempts holding-based replication, particularly of large, relatively transparent equity long–short funds, using regulatory filings.

Relative to traditional hedge funds, these vehicles:

- Offer daily liquidity and UCITS or ’40 Act–style oversight.

- Are subject to leverage, concentration, and illiquidity constraints that may prevent full replication of hedge fund risk profiles.

- Typically charge lower and simpler fees (no incentive fee), which is an important consideration in net performance comparisons.

Exam Warning: Replication strategies may appear attractive due to liquidity and cost, but for the exam you should always identify major limitations:

- Replicators capture long-run average exposures, not active or unique trades that drive true alpha.

- Replication quality depends critically on the quality of the benchmark index and the stability of factor relationships.

- Most replication strategies are likely to diverge from hedge fund indexes during tail events, crises, or periods of high manager discretion.

- Liquid alternative implementations may be unable to use leverage, illiquid instruments, or concentrated positions to the same extent as the original hedge funds, limiting the comparability of risk and return.

Summary

Hedge fund and liquid alternative performance cannot be evaluated or replicated effectively with standard tools alone. You need to:

- Decompose returns into traditional market betas, alternative risk premia, and potential alpha, recognizing the significant role of leverage and fees.

- Recognize that non-normal, autocorrelated return distributions undermine naïve interpretations of volatility, Sharpe ratios, and tracking error.

- Supplement traditional metrics with drawdown measures, downside-focused statistics, and capture ratios that better reflect investor objectives and risk tolerance.

- Be skeptical about benchmarks and indexes for hedge funds and liquid alternatives, explicitly discussing survivorship, backfill, and investability issues.

- Understand factor-based and holding-based replication approaches, being ready to articulate their mechanics, advantages, and limitations in exam scenarios.

In Level 3 questions, you will often be asked not just to compute measures, but to judge whether a manager’s results are consistent with their stated process, whether a benchmark is appropriate, and whether a replication claim is credible given the specific risks and constraints.

Key Point Checklist

This article has covered the following key knowledge points:

- Main drivers of hedge fund and liquid alternative returns: traditional betas, alternative risk premia, alpha, leverage, and fees

- Why traditional performance metrics frequently understate risk when returns are non-normal and autocorrelated

- Use and interpretation of Sharpe, Sortino, maximum drawdown, drawdown duration, and upside/downside capture for these strategies

- Benchmarking challenges for hedge funds and liquid alternatives, including survivorship and backfill biases and investability concerns

- Principles, strengths, and weaknesses of factor-based and holding-based hedge fund replication

- How to interpret and evaluate replication claims and benchmark choices in CFA Level 3 exam vignettes

Key Terms and Concepts

- hedge fund

- liquid alternative

- hedge fund replication

- non-normal return distribution

- autocorrelation

- alternative risk premia

- high-water mark

- hurdle rate

- maximum drawdown

- drawdown duration

- upside/downside capture ratio

- survivorship bias

- backfill bias

- factor-based replication

- holding-based replication