Learning Outcomes

This article explains hedge fund and liquid alternative strategy taxonomy and associated risk exposures, including:

- Classifying major hedge fund and liquid alternative strategies into equity-related, event-driven, relative value, opportunistic, specialist, and multi‑manager categories used in the CFA Level 3 curriculum.

- Distinguishing the primary sources of return and typical factor risk exposures (equity, credit, interest-rate, currency, volatility, liquidity) for each strategy group.

- Interpreting linear factor risk model outputs to attribute hedge fund performance to systematic and idiosyncratic drivers.

- Applying conditional or crisis-period factor models to detect nonlinear, time-varying, or hidden risk exposures that emerge during market stress.

- Assessing how hedge fund and liquid alternative allocations affect portfolio-level volatility, drawdowns, and risk-adjusted performance metrics.

- Comparing traditional hedge fund vehicles with liquid alternatives in terms of liquidity terms, fee structures, regulatory oversight, transparency, and operational risk.

- Evaluating the suitability of specific strategies for different investor objectives, risk tolerances, and liquidity needs in an exam case-study context.

- Identifying common CFA Level 3 exam traps related to strategy misclassification, misunderstanding of factor model results, and overestimation of diversification benefits.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand hedge fund and liquid alternative strategies, their main risk exposures, and their role within a diversified portfolio, with a focus on the following syllabus points:

- Classifying hedge fund and liquid alternative investment strategies

- Identifying typical risk exposures (equity, market, credit, volatility, liquidity) for major hedge fund and liquid alternative strategies

- Explaining the use of linear and conditional factor risk models for assessing hedge fund strategy risks

- Evaluating the impact of hedge fund allocations on traditional portfolio return and risk metrics

- Recognizing the operational, legal, and fee differences between traditional hedge funds and liquid alternatives

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which hedge fund strategy typically aims for market-neutral exposure and relies on mean reversion between paired securities?

- Identify two main risk factor exposures for global macro strategies.

- What are the primary liquidity differences between traditional hedge funds and liquid alternatives?

- True or false? A conditional factor risk model can highlight risk exposures that emerge only during periods of market turbulence.

Introduction

Hedge funds and liquid alternatives are central to the CFA Level 3 syllabus as key components of institutional and private portfolios. Effective exam preparation requires a structured approach to hedge fund strategy classification, understanding key risk exposures, and recognizing how liquid alternative vehicles differ in regulatory and operational aspects.

Major Hedge Fund and Liquid Alternative Strategy Groups

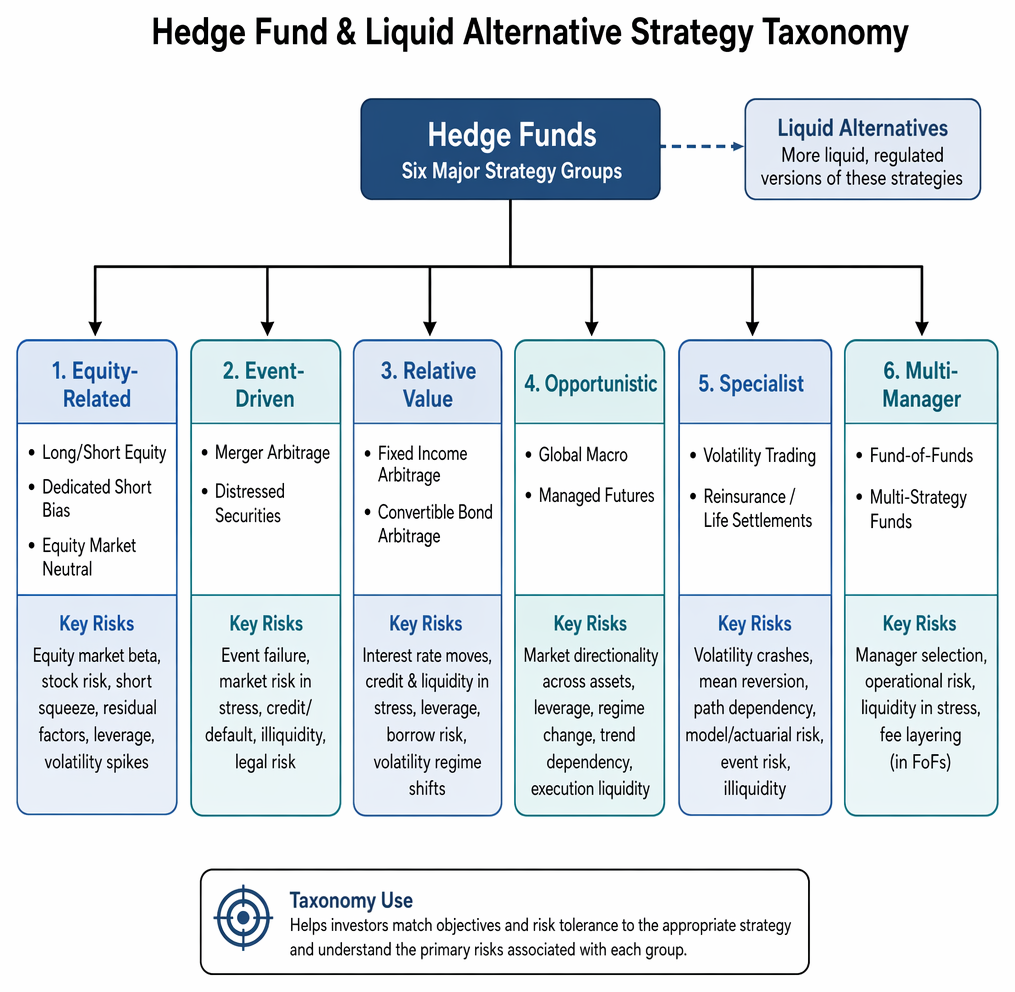

Hedge funds are often grouped into six main strategy categories: equity-related, event-driven, relative value, opportunistic, specialist, and multi-manager. Liquid alternatives are pooled vehicles that implement similar, but usually more liquid and regulated, versions of these strategies.

Hedge fund risk analysis progresses from historical returns and factor identification to conditional stress attribution and revised strategy risk limits.> Key Term: Hedge fund> A private investment fund with a flexible mandate, often employing borrowed capital, short selling, and derivatives to pursue absolute or risk-adjusted returns.

Key Term: Liquid alternative

A regulated, pooled investment vehicle (e.g., mutual fund or UCITS) that offers hedge-fund-like strategies, typically with daily liquidity and stronger regulatory oversight. Key Term: Factor risk model

A quantitative model used to attribute portfolio returns to common market risk factors (e.g., equity, credit, volatility), often extended to examine crisis or conditional effects.

Equity-Related Strategies Long/Short Equity: These managers combine long positions in undervalued stocks with short positions in overvalued stocks. Most maintain a net long bias, but exposures vary over time. Stock selection is the most important source of alpha; managers may be fundamental or quantitative in approach

-

Key risks: equity market beta, stock-specific risk, moderate liquidity risk.Dedicated Short Bias: Managers who operate primarily with net short equity market exposure aim to profit from declining securities. These strategies are rare due to the historic upward trend in equities and exceptional operational demands.

-

Key risks: high volatility, short squeeze risk, negative correlation with equities.Equity Market Neutral: These managers build portfolios with balanced long and short equity exposures with close to zero net market beta. Pairs trading, stub trades, and multi-factor portfolios are common implementations.

-

Key risks: residual factor exposures, risk from the use of borrowed funds, potential exposure to volatility spikes.

Event-Driven Strategies Merger Arbitrage: Managers profit from announced mergers by going long the target and, in stock-for-stock deals, short the acquirer. Payoff resembles selling event risk insurance

-

Key risks: event-specific risk (deal failure), market risk (if correlations rise during stress), moderate liquidity risk.Distressed Securities: These strategies invest in securities of companies in or near bankruptcy, often with a long bias and longer holding periods.

-

Key risks: credit/default risk, low liquidity, event risk, sometimes legal risk.

Relative Value Strategies Fixed Income Arbitrage: Exploits pricing discrepancies between bonds or derivatives in similar markets, typically using leveraged, duration-neutral portfolios

-

Key risks: interest rate moves, credit and liquidity risk during market stress, the use of borrowed funds.Convertible Bond Arbitrage: Long convertibles, short the reference equity, extracting value from option mispricing. Delta and gamma hedging are key.

-

Key risks: credit risk, short borrow risk, volatility regime shifts.

Opportunistic Strategies Global Macro: Top-down strategies based on macroeconomic trends, using discretionary or systematic methods across asset classes

-

Key risks: market directionality (equity/currency/bond/commodity), use of borrowed capital, regime change.Managed Futures: Systematic trading of futures (often time-series momentum or cross-sectional momentum).

-

Key risks: trend regime dependency, significant use of borrowed funds, execution liquidity.

Specialist and Multi-Manager Strategies Volatility Trading: Specializes in buying/selling volatility via options, volatility swaps, or variance swaps, often for portfolio hedging or premium collection

-

Key risks: volatility crashes (for sellers), mean reversion, path dependency, liquidity.Reinsurance/Life Settlements: Provides insurance risk capital or invests in longevity products, seeking uncorrelated returns.

-

Key risks: model/actuarial risk, event risk, illiquidity.Multi-Manager (Fund-of-Funds, Multi-Strategy Funds): Allocates to multiple strategies for diversification and central risk management. Multi-strategy funds usually have better fee netting and tactical flexibility than fund-of-funds.

-

Key risks: manager selection, operational risk, liquidity in stressed markets, fee layering (in FoFs).

Worked Example 1.1

Question: An investor wants steady risk-adjusted returns, minimal market exposure, and diversification during equity downturns. Which hedge fund strategy and key risks should be considered?

Answer:

Equity market-neutral strategies are typically used. They seek to neutralize market beta via balanced long and short positions. Key risks include amplification from the use of borrowed funds, hidden factor (style/sector) exposures, and losses if correlations spike in stress periods.

Liquidity, Fees, and Operational Risk: Hedge Funds vs. Liquid Alternatives

Traditional hedge funds are typically organized as limited partnerships with lock-ups, redemption gates, and high manager/incentive fees. Liquid alternatives, such as mutual fund-based products, provide daily liquidity, transparent holdings, and are subject to stricter regulation and lower fees (no performance fees in some jurisdictions). However, liquid alternatives often cannot fully replicate hedge fund strategies reliant on illiquidity premia.

Exam Warning: Many candidates overlook the operational and liquidity risk implications of different vehicle types. Exam questions often test your knowledge of the impact of lock-up periods, redemption gates, and the regulatory obligations attached to liquid alternative structures.

Risk Factor Models for Hedge Fund Strategy Assessment

A factor risk model attributes strategy or fund returns to broad market risk factors (e.g., equity, credit, currency, volatility). Conditional or crisis-period models reveal risk exposures that may only appear during market stress. This helps to identify when apparent diversification fails.

Key Term: Conditional risk model

A type of factor risk model that estimates changes in risk exposures in normal versus stress or crisis periods, revealing hidden vulnerabilities not captured in average estimates.

Worked Example 1.2

Question: How might a conditional factor risk model inform risk management for a portfolio allocating to multiple hedge fund strategies, including long/short equity, event-driven, and global macro?

Answer:

A conditional factor risk model could reveal that long/short equity and event-driven strategies unexpectedly increase equity beta or credit spread sensitivity during crisis periods, reducing diversification. Conversely, global macro may add value during such periods through defensive or contrarian exposures. Identifying these shifts helps the portfolio manager avoid concentration in strategies prone to co-movement under stress.

Portfolio Impact of Hedge Fund Allocations

A diversified portfolio that includes hedge funds or liquid alternatives can reduce overall volatility and improve risk-adjusted returns (Sharpe and Sortino ratios), especially if the strategies display low or negative correlation with equities, or positive returns during market stress. However, correlation and risk exposures during crises must be carefully assessed, as diversification benefits may disappear under extreme stress.

Worked Example 1.2 Details

Question: A traditional 60/40 portfolio is considering adding a 20% allocation to event-driven and relative value hedge fund strategies. What effects should an analyst expect on return, risk, and maximum drawdown?

Answer:

Such an allocation would typically modestly improve expected returns and reduce portfolio standard deviation and drawdown, provided the hedge fund strategies have low correlation with both stocks and bonds and maintain their diversification profile in stress scenarios. However, illiquidity, fee, and manager selection risks may dampen, or in some periods even reverse, the expected benefits.Revision Tip: Practice classifying strategies and their main risk exposures from short scenario descriptions, as exam questions may focus on concise scenario classification and factor model interpretation.

Key Point Checklist

This article has covered the following key knowledge points:

- Classify hedge fund and liquid alternative strategies into major strategy groups

- Identify typical risk exposures (equity, credit, volatility, liquidity) for each group

- Distinguish between traditional hedge funds and liquid alternatives in liquidity, fees, and regulation

- Understand and apply linear and conditional factor risk models for assessing strategy risks

- Evaluate how hedge fund allocations affect portfolio return, risk, and drawdown

Key Terms and Concepts

- Hedge fund

- Liquid alternative

- Factor risk model

- Conditional risk model