Learning Outcomes

This article explains how immunization and liability management are applied in fixed income portfolio management, emphasizing surplus-based performance evaluation relevant for CFA Level 3. It defines classical and contingent immunization, contrasts single-liability and multi-liability settings, and highlights the conditions required for an immunized position to remain effective. It outlines how to measure and interpret surplus, surplus volatility, and tracking error relative to liabilities, and how these differ from benchmark‑relative risk. It analyzes the main sources of surplus risk—duration and key rate mismatches, convexity differences, yield‑curve shifts, credit and spread risk, reinvestment risk, and model risk—and links each source to exam-style risk decomposition formulas. It details how performance attribution is carried out for liability‑driven mandates, separating the effects of market movements, liability characteristics, and active management decisions such as sector rotation, curve positioning, and security selection. It also reviews typical numerical tasks tested in the curriculum, including computing surplus volatility, decomposing risk contributions, and attributing surplus return to duration, curve, convexity, and credit factors for immunized portfolios.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand how immunization and liability management relate to performance attribution and risk decomposition, with a focus on the following syllabus points:

- Distinguish among immunization techniques and identify their limitations

- Describe risk measures relevant to liability-driven portfolio management

- Decompose surplus risk and interpret performance attribution for immunized portfolios

- Evaluate the impact of asset-liability mismatches on attribution and risk

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What are the three primary sources of surplus risk in a liability-relative fixed income portfolio?

- How does immunization seek to manage surplus volatility?

- Which risk factors are typically relevant in a performance attribution for a liability-driven mandate?

- Describe one limitation of classical single-duration immunization when applied in a multi-liability context.

Introduction

Immunization and liability management are central to fixed income portfolio strategy where cash flows must reliably meet future liabilities. For CFA Level 3, you must be comfortable with analysing how immunization effectiveness can be assessed using performance attribution, and with decomposing risk in terms of surplus volatility and sources of tracking error relative to liabilities. This article focuses on surplus risk decomposition for portfolios managed to hedge (or outperform) liability streams, and reviews core exam-relevant techniques for performance attribution in liability-driven mandates.

Key Term: immunization

A fixed income strategy that attempts to structure and manage a bond portfolio so the future value of its assets will satisfy known liability payments, typically by matching portfolio duration (and sometimes convexity) with the duration of the liabilities. Key Term: surplus

The difference between the market value of a portfolio’s assets and the present value of its liabilities; surplus risk refers to the volatility of this difference arising from asset and liability value changes. Key Term: surplus volatility

The standard deviation of periodic changes in the surplus; a measure of the risk that portfolio assets will not track liability value movements. Key Term: performance attribution

A technique used to decompose and analyse sources of active return (relative to liabilities or a benchmark), enabling identification of portfolio manager decisions and external market factors that contributed to surplus or tracking error. Key Term: risk decomposition

The process of breaking down overall portfolio risk (e.g., surplus volatility) into component risks arising from interest rate mismatches, yield curve changes, convexity differences, credit spreads, and other factors.Test Tip: When revising Performance attribution and risk decomposition, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Immunization and Liability Management: Core Principles

Immunization Techniques

Immunization is used by institutional investors—especially defined benefit pension schemes and insurance companies—to ensure that future payments (liabilities) are made as they fall due, regardless of interest rate fluctuations. Classical immunization matches the duration of assets and liabilities so that the present value of assets offsets the present value of liabilities for small parallel shifts in yields.

Immunization is most straightforward in the case of a single liability. For multiple liabilities, practitioners use duration-matching or cash flow matching (dedicated portfolio) approaches, but these are subject to interest rate and yield curve risk.

Surplus and Performance Risk

Immunized portfolios are not managed in absolute return terms, but relative to an evolving liability value. The difference between assets and liabilities is the surplus. For reporting and risk control, the key management metric is surplus volatility—that is, how much the assets’ value may diverge from liability value as market conditions change.

Risk Decomposition for Surplus Risk

Risk decomposition allows the analysis of what drives surplus volatility. For portfolios immunized to a single factor (e.g., parallel shift), surplus volatility may be low, but in multi-factor or non-parallel scenarios, mismatches in duration, convexity, or exposure to non-interest rate risk may dominate. The primary sources contributing to surplus volatility include:

- Interest rate risk (parallel shifts)

- Yield curve risk (twists/shape changes)

- Convexity mismatch

- Asset-specific risks (credit, currency, liquidity)

- Model and estimation risk

A risk decomposition should isolate how much surplus volatility is due to each of these risk exposures.

Performance Attribution in Liability Management

Performance attribution in a liability-driven context means decomposing the portfolio’s return (relative to liabilities) into contributions from market conditions (uncontrollable), active management (controllable), and mismatches between asset and liability sensitivities.

A typical performance attribution framework for immunized mandates will include:

- Contribution of interest rate movements (via matched or unmatched durations)

- Yield curve movements (if duration is matched, but curve is not)

- Active return from credit or sector allocation (if permitted)

- Decisions related to cash flow or convexity mismatch

Practical Risk Decomposition and Attribution Methods

Present values of assets and discounted liabilities determine surplus, whose volatility links to the objective of surplus stability.

Decomposing Surplus Volatility

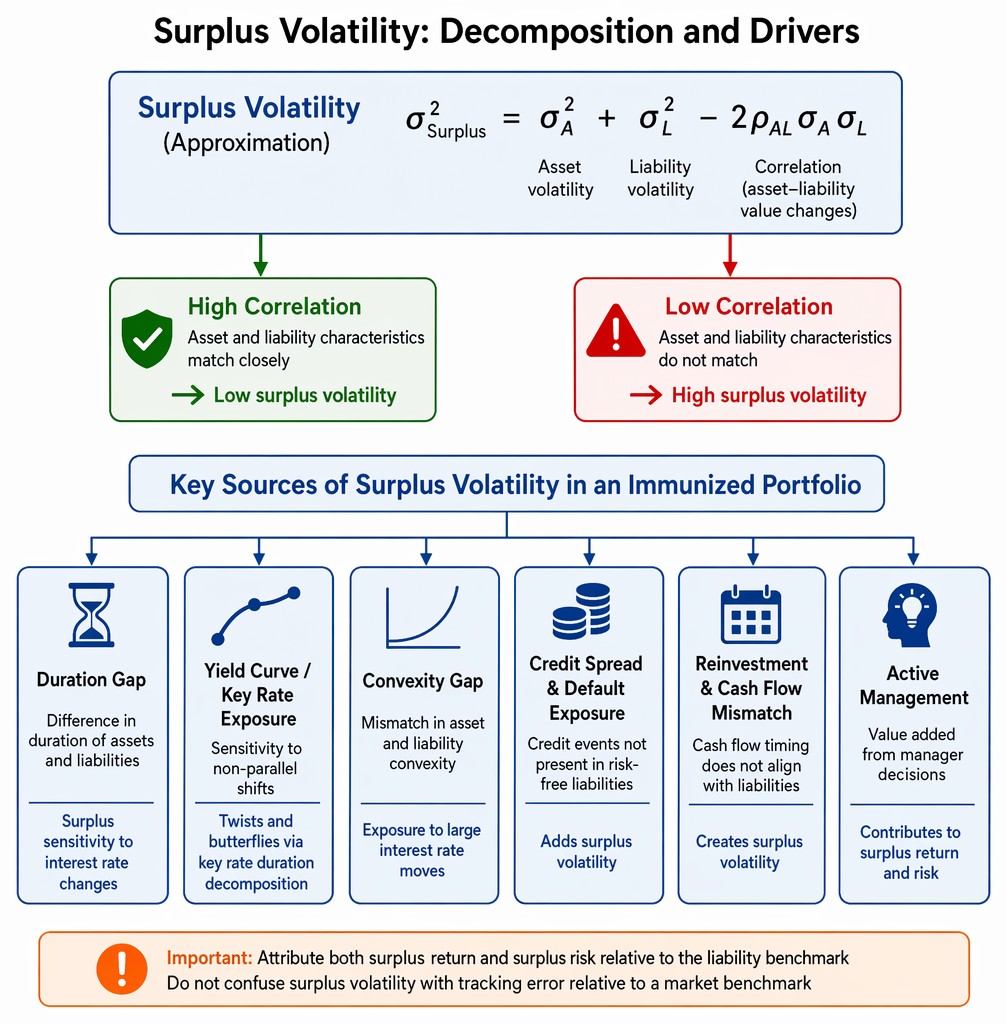

Surplus volatility can be approximated by:

Where:

- = asset volatility

- = liability volatility

- = correlation between asset and liability value changes

If the asset and liability characteristics match closely, correlation is high and surplus volatility is low. If not, surplus volatility rises due to risk mismatches.

Attribution Sources for an Immunized Portfolio

A full risk and return attribution for an immunized portfolio typically analyses:

- Duration gap: Difference in duration of assets and liabilities. This leads to surplus sensitivity to interest rate changes.

- Yield curve/Key rate exposure: Sensitivity of surplus to non-parallel shifts (e.g., twists, butterflies), assessed via key rate duration decomposition.

- Convexity gap: Mismatch in asset and liability convexity creates exposure to large rate moves.

- Credit spread and default exposure: Non-govt portfolios may have surplus volatility from credit events not reflected in risk-free liabilities.

- Reinvestment and cash flow mismatch: Occurs if timing of portfolio cash flows does not align perfectly with liabilities.

- Active management (value added from manager decisions)

Worked Example 1.1

A pension fund immunizes its liabilities by constructing a bond portfolio matched in duration but not in key rate exposure. The value of assets and liabilities each has a volatility of 8%, with a correlation between their value changes of 0.8.

Question: What is the surplus volatility as a percentage?

Answer:

Surplus volatility

This reflects the reduction in surplus risk due to the high correlation between asset and liability value changes.

Performance Attribution Example for an Immunized Portfolio

Performance attribution for a liability-matched portfolio decomposes return sources relative to the liability benchmark. Typical factors include:

- Effect of parallel shifts (if duration matched, impact is minimal)

- Effect of curve steepening or flattening (exposure if key rate risk is not neutralized)

- Impact of credit spread widening (if permitted in portfolio, but not present in liabilities)

- Active management decisions (e.g., sector overweights, security selection)

Effective attribution quantifies surplus return and surplus risk from each source.

Worked Example 1.2

Suppose a liability has duration of 12 and convexity of 147, while a portfolio has duration 12 and convexity 120. Parallel shifts in rates have no surplus impact, but a 50bp change in curve steepness (2s/30s) occurs. The asset's key rate duration for 2y is 2, for 30y is 10; the liability's are 3 and 9. What is the net surplus effect?

Answer:

The change in surplus value is approximately:

In this case, opposite mismatches in key rate exposures cancel. If mismatches coincided, surplus value would be sensitive to yield curve shifts.

Exam Warning: On the exam, do not confuse “tracking error” (relative to a market benchmark) with surplus volatility (tracking error relative to the liability value). Always interpret risk decomposition and attribution relative to the liability benchmark for immunized portfolios.

Summary

Immunization techniques are used to ensure that a portfolio’s value tracks liability outflows despite changes in interest rates. Surplus volatility measures the risk that assets and liabilities will move independently due to duration, curve, or convexity mismatches, as well as asset-specific risks. Performance attribution in liability-driven mandates evaluates contributions to surplus return and risk from market movements, key rate mismatches, convexity differences, and manager decisions. Effective attribution and risk decomposition are essential for managing and reporting results accurately for liability-based portfolios.

Key Point Checklist

This article has covered the following key knowledge points:

- Define immunization, surplus risk, surplus volatility, and liability-driven performance attribution

- Identify and explain surplus risk decomposition for liability-matched portfolios

- Attribute performance in immunized portfolios to duration, curve, convexity, credit, and active management factors

- Apply concepts in CFA exam-style calculations and scenario analysis

Key Terms and Concepts

- immunization

- surplus

- surplus volatility

- performance attribution

- risk decomposition