Learning Outcomes

This article explains how to formulate an individual investment policy statement (IPS) with explicit reference to liquidity, time horizon, tax, legal, and unique constraints in the CFA Level 3 context. It clarifies the role of each constraint within the overall IPS, emphasizing how they interact with client objectives and risk tolerance. The article highlights how to identify realistic liquidity needs, distinguish immediate from ongoing or contingent cash flows, and translate them into precise, exam‑quality constraint statements. It explains when and how to segment an investment horizon into stages, and how horizon changes affect portfolio risk, return, and spending assumptions. It details how to frame a tax constraint using the client’s jurisdiction, account types, and marginal tax rates, and how to avoid common mistakes such as ignoring tax‑advantaged accounts or embedded gains. The article also reviews typical legal and regulatory issues, plus genuinely unique client circumstances, and shows how to express them succinctly. Throughout, it focuses on structuring answers in CFA exam format, using clear rationales tied directly to the case facts and maximizing the likelihood of earning full credit.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand not only the qualitative and quantitative formulation of IPS constraints, but also how to tailor these to the specific context of an individual client, with a focus on the following syllabus points:

- Recognizing and applying the IPS liquidity, horizon, tax, legal/regulatory, and unique constraint definitions for private clients

- Formulating precise, CFA-level IPS constraint statements and rationales

- Structuring and evaluating IPSs that match CFA exam scenarios, especially distinguishing between immediate and future liquidity requirements and identifying critical legal/tax issues

- Incorporating and justifying unique personal factors in IPS construction

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What are the main elements included in the liquidity constraint for an individual IPS, and how do you distinguish between short-term and ongoing liquidity needs?

- When should an investment horizon for a private client be segmented into multiple stages within the IPS?

- Which tax factors are essential for the IPS, and how should tax-advantaged accounts be addressed?

- Identify two examples of legal or regulatory issues that must be included in an individual's IPS, and explain why they are relevant.

Introduction

Formulating an individual IPS constraint section is a core CFA Level 3 skill. The effective IPS must clearly identify and justify the client’s liquidity needs, investment horizon, tax position, legal and regulatory circumstances, and unique constraints. CFA exam questions will require you to apply these concepts concisely, avoid common misstatements, and present rationale matched to client fact patterns.

Liquidity Constraint

A correct liquidity constraint specifies both immediate and foreseeable short-term cash needs that must be met from the portfolio, as well as an allowance for unexpected expenses or a cash reserve if relevant. Liquidity events are often stated as a currency amount or percentage of the portfolio, and the timing of each withdrawal should be specified in the IPS.

Common liquidity items in an individual IPS include:

- Upcoming portfolio withdrawals for consumption, education, home purchase, taxes due, or large one-time purchases

- Planned charitable donations payable from assets under management

- Any required minimum cash balances maintained in the portfolio

Key Term: Liquidity Constraint

The explicit identification of cash demands on the portfolio (immediate and ongoing), specifying both magnitude and timing for withdrawals.

Worked Example 1.1

Question: A 58-year-old client is retiring in two months. She requires $150,000 for a mortgage payoff from her $3 million portfolio, and annual living expenses of $80,000 to be drawn from portfolio assets until social security starts in four years. State her liquidity constraint.

Answer:

The IPS liquidity constraint should state that $150,000 is required immediately to pay off the mortgage. Additionally, the portfolio must provide $80,000 annually for living expenses over the next four years, until social security commences.Exam Warning: Many candidates fail to distinguish between immediate, one-off liquidity needs and ongoing withdrawals. Always specify both and avoid listing anticipated, but unfunded, goals as "liquidity" unless required within 12 months.

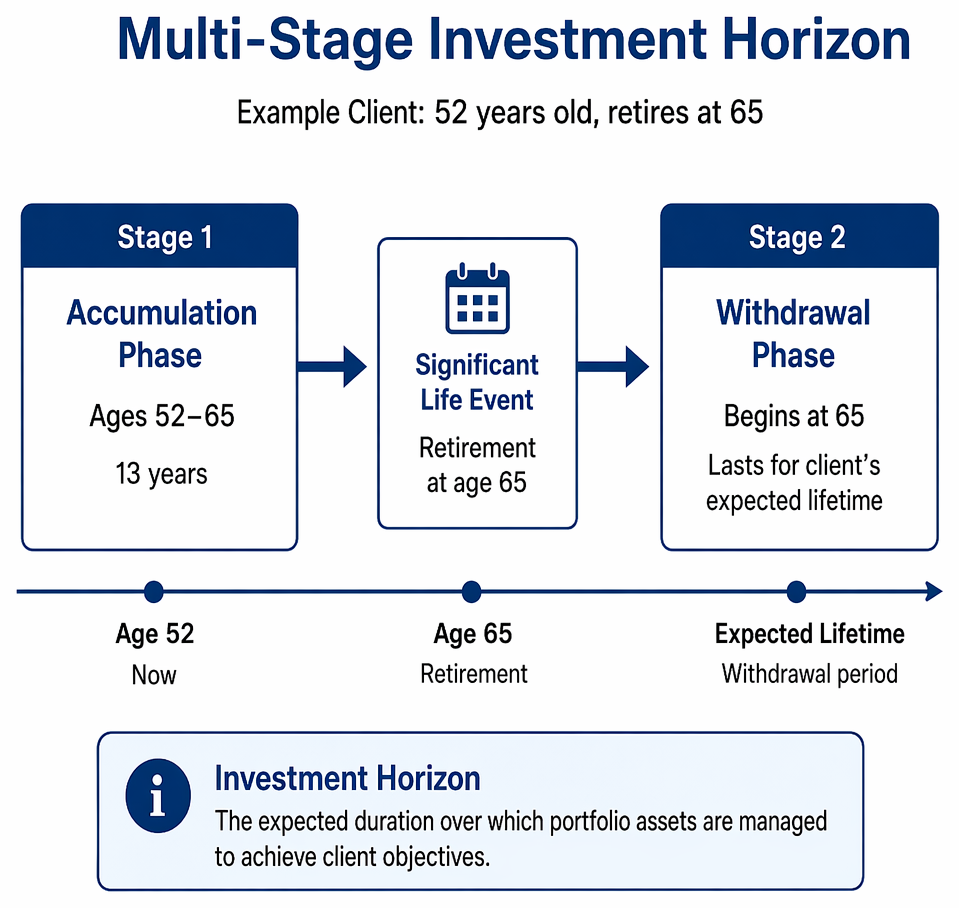

Investment Horizon Constraint

The investment horizon defines the time period over which the portfolio is to be managed. For individuals, it is typically multi-stage if a major event (such as retirement, sale of a business, or inheritance) will substantially alter cash flows or risk tolerance. Each stage should be clearly identified (e.g., pre-retirement and post-retirement).

Liquidity constraint workflow identifies funded cash needs, separates immediate and ongoing requirements, quantifies timing, and states required cash balances in the IPS.

Key Term: Investment Horizon

The expected duration over which portfolio assets will be managed to achieve client objectives, often divided into stages by significant life events.

Worked Example 1.2

Question: A 52-year-old client plans to work for 13 more years, with retirement at 65. At retirement, her portfolio will provide the majority of living expenses.

Answer:

The IPS investment horizon constraint should note a two-stage horizon: Stage 1 is from now until age 65 (13 years, accumulation phase); Stage 2 is withdrawal phase beginning at retirement and lasting for the client’s expected lifetime. Key Term: Multi-Stage Horizon

An investment horizon articulated as distinct periods separated by events that change cash flows or risk tolerance.

Tax Constraint

Taxation affects investment selection, return expectations, and asset location. Clearly state tax status (e.g., taxable, tax-deferred, tax-exempt), noting whether the portfolio is subject to ongoing income tax, capital gains tax, or other specific tax treatments. Mention any portfolio structuring around tax-advantaged accounts (e.g., ISAs, 401(k), pension, etc.). Highlight potential for realization of gain/loss, especially where a position has large unrealized capital gains.

Key Term: Tax Constraint

The specification of tax circumstances influencing the portfolio, including income and capital gains tax rates, tax-advantaged accounts, and any other tax issues impacting investment strategy.

Worked Example 1.3

Question: A client holds a tax-deferred retirement account and a taxable investment account. He is in the 40% marginal income tax bracket; long-term capital gains are taxed at 20%.

Answer:

The IPS tax constraint should state that portfolio returns in the taxable account are subject to 40% income tax on interest/dividends and 20% on long-term capital gains. The tax-deferred account allows deferral of tax until withdrawal, at which point withdrawals are taxed as ordinary income.

Legal and Regulatory Constraint

Legal and regulatory constraints refer to client-specific legal circumstances or restrictions that affect portfolio management. Common examples for individuals include: residency or citizenship restrictions, beneficiary designations, trust documents, legal proceedings, or employment agreements that impose investment restrictions (e.g., blackout periods, insider trading restrictions). These must be described if they materially impact how assets may be managed, transferred, withdrawn, or invested.

Key Term: Legal and Regulatory Constraint

Any client-specific law, rule, court order, or regulation that limits or directs portfolio transactions, withdrawals, or investment choices. Key Term: Unique Constraint

Any client-specific circumstance (not captured in other constraints) that has a direct bearing on investment strategy—such as social, ethical, employment, or personal preferences.

Worked Example 1.4

Question: A client is a US citizen residing in Europe, subject to FATCA reporting, and is a director of a public company with blackout trading periods on company stock.

Answer:

The IPS must specify the client’s legal constraints: US citizenship subjects worldwide income to US tax and reporting (FATCA/CRS). As a company director, she is subject to trading blackouts and insider trading rules, restricting purchase or sale of company stock during specified periods.

Unique Circumstances Constraint

The unique circumstances section covers any remaining constraints not covered above. These might include specific personal or familial issues, social investment policies (e.g., ESG, SRI, faith-based screening), concentrated stock holdings, low basis asset considerations, employment-related investment restrictions, ethical preferences, or any other client instruction (e.g., no investment in specific assets or sectors). Clearly state only if material and relevant to portfolio management.

Revision Tip: Avoid listing "none" for unique constraints unless you have explicitly checked the client scenario. If a concentrated position, inheritance expectation, or ethical/sustainable investing preference exists, spell this out precisely in the IPS.

Summary

For CFA Level 3, IPS formulation for individuals demands precise, concise articulation of the constraints—in particular, liquidity, horizon, tax, legal and unique circumstances. Use clear, CFA-style structure. Specify amounts and timing for liquidity. Identify all relevant stages for the investment horizon. State tax, legal, and unique constraints as they arise from the client’s factual scenario. Base every statement on information provided.

Key Point Checklist

This article has covered the following key knowledge points:

- Liquidity constraints should specify all immediate and planned portfolio withdrawals and required cash balances.

- Investment horizon is defined by total portfolio time frame, often with stage breakdowns when appropriate.

- Tax constraints must state relevant tax rates and account types affecting portfolio returns and asset selection.

- Legal and regulatory constraints include all binding laws, regulations, or agreements impacting investments.

- Unique constraints summarize any material special client instructions, preferences, or restrictions not covered elsewhere.

Key Terms and Concepts

- Liquidity Constraint

- Investment Horizon

- Multi-Stage Horizon

- Tax Constraint

- Legal and Regulatory Constraint

- Unique Constraint