Learning Outcomes

This article explains investor biases and behavioral investor types for the CFA Level 3 exam, including:

- distinguishing emotional biases from cognitive errors and assessing how each affects investor decision-making, risk tolerance, and portfolio adjustments

- classifying clients into the four core behavioral investor types (Passive Preserver, Friendly Follower, Independent Individualist, Active Accumulator) based on observed attitudes and dominant biases

- identifying the key diagnostic biases, typical behaviors, and communication needs associated with each behavioral type

- recognizing blended or shifting behavioral profiles and understanding the limitations of rigid investor-type classifications in real client situations

- applying behavioral profiling within the IPS process to refine risk objectives, constraints, and asset-allocation guidance

- integrating bias awareness into suitability analysis, portfolio recommendations, and ongoing monitoring so advice remains aligned with client psychology and exam-style case scenarios

- relating behavioral findings to communication strategies, expectation management, and exam vignette reasoning to justify recommended actions and constraints in constructed-response and item-set questions

- deciding when to try to moderate a client’s cognitive errors versus when to adjust portfolio design to accommodate persistent emotional biases

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand how investor biases affect client profiling, portfolio construction, and advisory recommendations, with a focus on the following syllabus points:

- The distinction between emotional biases and cognitive errors, and their impact on decision-making

- Classification and diagnostic features of key behavioral investor types (BITs)

- How behavioral profiles inform risk tolerance assessments and IPS construction

- The process of recognizing multiple or blended behavioral types

- How to tailor advice and communication styles according to behavioral profiles

- Uses and limitations of classifying investors into personality or behavioral types

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

What is the main difference between an emotional bias and a cognitive error in the context of portfolio advice?

- a) Emotional biases are always harmful, while cognitive errors can be beneficial.

- b) Emotional biases arise from feelings and are hard to change, while cognitive errors arise from faulty reasoning and can often be corrected with education.

- c) Emotional biases affect only risk tolerance, while cognitive errors affect only return expectations.

- d) Emotional biases apply only to retail clients, while cognitive errors apply only to institutional clients.

-

A retired client is very anxious about any change to her portfolio, focuses on preserving capital, and refuses to sell inherited stock despite extreme concentration risk. Which behavioral investor type (BIT) best fits this client?

- a) Friendly Follower

- b) Independent Individualist

- c) Passive Preserver

- d) Active Accumulator

-

A wealthy entrepreneur enjoys making her own investment decisions, has a high risk tolerance, trades frequently, and is convinced she can “time the market.” Which behavioral investor type will most likely benefit most from firm risk limits and strong monitoring rather than emotional reassurance?

- a) Passive Preserver

- b) Friendly Follower

- c) Independent Individualist

- d) Active Accumulator

-

An investor insists on holding a large, undiversified position in her employer’s stock, stating that she would “feel disloyal” selling and would regret it if the stock rose after she sold. Which category of bias most likely dominates?

- a) Cognitive errors such as anchoring

- b) Emotional biases such as endowment and regret aversion

- c) Purely rational risk–return considerations

- d) Random behavior not explained by behavioral finance

Introduction

Behavioral finance recognizes that investors are subject to consistent patterns of bias rooted in psychology. These patterns influence decisions, risk tolerances, and portfolio choices. Identifying individual biases and classifying investors by behavioral type is a key skill for CFA charterholders, especially in client-facing roles. This article outlines the common bias types, explains behavioral investor types (BITs) and their identification, and shows how these concepts are used in client profiling and portfolio recommendation.

Traditional finance assumes fully rational investors and efficient markets. Behavioral finance micro focuses instead on the biases of individual investors and how actual decisions systematically deviate from the rational benchmark.

Key Term: behavioral bias

A systematic deviation from rationality in decision making, driven by either faulty cognition or emotional responses, that can lead to suboptimal financial choices.

When advising private clients at Level 3, you must not only identify biases but also decide how far you can and should adjust portfolio design to accommodate them, while still meeting objectives and respecting constraints in the IPS.

Key Term: Behavioral Finance Micro (BFMI)

The branch of behavioral finance that studies how individual investors deviate from rational decision-making assumptions and how these deviations affect financial choices. Key Term: Behavioral Finance Macro (BFMA)

The branch of behavioral finance that examines how aggregate investor behavior and biases generate market-level anomalies relative to efficient market assumptions.Test Tip: When revising Behavioral investor types and profiling, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Emotional Biases and Cognitive Errors

Investor behavior is shaped by two broad categories of bias:

- Emotional biases: Decisions influenced by feelings, impulses, or intuitions. These biases are resistant to correction through information or reasoning and most often require adjustment in portfolio strategy rather than confrontation.

- Cognitive errors: Mistakes in information processing, memory, or statistical reasoning. These are more responsive to education and discussion.

Key Term: emotional bias

A decision pattern dominated by feelings or impulses rather than logic, typically difficult to correct through reasoning and more appropriate to accommodate than to “fix” outright. Key Term: cognitive error

A decision-making distortion caused by faulty reasoning, information processing, or memory, often correctable or moderatable through education, better information, or improved decision processes.

The curriculum also distinguishes two broad subcategories of cognitive errors:

- Belief perseverance biases: The tendency to cling to existing beliefs despite new information (for example, conservatism, confirmation, representativeness).

- Processing errors: Systematic mistakes in how information is analyzed or framed (for example, anchoring, mental accounting, framing, availability).

Key Term: belief perseverance bias

A cognitive error in which individuals irrationally maintain prior beliefs or forecasts by underweighting or misinterpreting new, contradictory information. Key Term: processing error

A cognitive error that arises from illogical or inconsistent information processing, such as misframing data, anchoring on irrelevant values, or relying on easily recalled but unrepresentative examples.

From an advisory standpoint, the distinction between emotional and cognitive is practical:

- Cognitive errors can often be moderated. For example, an investor anchoring on a purchase price can be shown total-return and risk data that highlight opportunity cost and downside risk, helping shift behavior toward a more rational benchmark.

- Emotional biases are harder to change. Loss-averse clients may continue to experience intense anxiety around drawdowns even after extensive education. For such clients, it is usually more effective to adjust the portfolio (for example, lower equity weight, more cash buffers) so they can stick with the plan through market stress.

On the exam, when you see a vignette describing a client ignoring statistical evidence or probabilities but being open to discussion, think “cognitive error—moderate with education.” When the vignette emphasizes anxiety, regret, or attachment (for example, to legacy holdings), think “emotional bias—adjust the portfolio and communication style.”

Behavioral Investor Types (BITs) and Profiling

Behavioral profiling aims to cluster investor personalities into “types” based on their dominant biases and likely behaviors toward risk, diversification, and portfolio change. Understanding these types supports the CFA syllabus requirement to recognize how behavioral biases influence both asset allocation and the client–adviser relationship.

Key Term: behavioral investor type (BIT)

An investor profile characterized by a dominant set of emotional or cognitive biases and a typical level of risk tolerance that together guide attitudes toward risk, change, and portfolio decisions.

Psychographic models pre-date BITs (for example, Barnewall’s active versus passive investors and the Bailard, Biehl & Kaiser five-way model). The BIT framework, however, is specifically designed to be a practical, top-down tool to link observable behavior to dominant biases and then to a behaviorally-informed asset allocation.

Behavioral profiling is not clinical psychology and cannot produce a perfect diagnosis. Its purpose is to:

- anticipate likely decision patterns and stress points,

- tailor communication and education,

- and build portfolios that clients can actually follow over time.

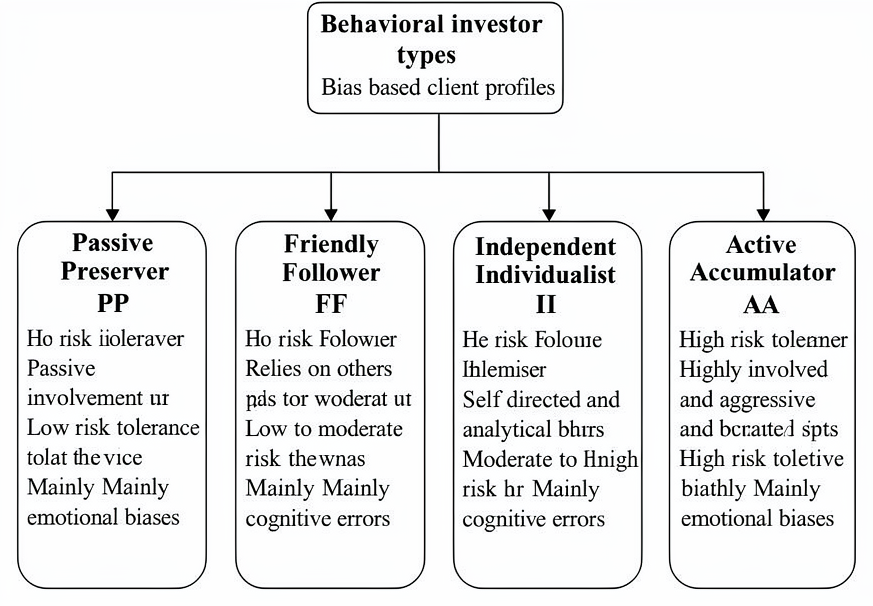

Four Core Behavioral Investor Types (BITs)

Behavioral finance literature defines four major BITs for practical profiling. They can be placed on two axes: active versus passive involvement and low versus high risk tolerance. Importantly, the two extreme types (PP and AA) are dominated by emotional biases, while the middle types (FF and II) are dominated by cognitive errors.

Passive Preserver (PP)

- Low risk tolerance.

- Generally passive; wealth often created passively (inheritance, executive compensation).

- Dominant biases: loss aversion, status quo, regret aversion, endowment; may also show anchoring and mental accounting.

- Seeks security, is slow to adjust, and emotionally attached to existing positions.

Key Term: Passive Preserver (PP)

A conservative, security-focused investor type with low risk tolerance and primarily emotional biases such as loss aversion and status quo bias, often anxious about portfolio change.

Typical manifestations:

- Large cash or money market balances despite low real returns.

- Concentrated legacy holdings (for example, inherited stock) maintained despite clear diversification benefits.

- Focus on short-term fluctuations and fear of “losing what I already have.”

Advisory implications:

- Advice approach: Focus on emotional reassurance and gradual, non-disruptive recommendations. Use “big-picture” explanations (meeting spending needs, preserving real wealth) rather than technical measures like standard deviation.

- Portfolio design: Adjust to biases by using lower-volatility allocations than a purely rational optimization might suggest, provided long-term objectives remain achievable. Build in cash buffers and high-quality fixed income to reduce drawdown anxiety.

- Exam angle: When a vignette emphasizes age, inheritance, low spending needs, and anxiety about losses, PP is a likely classification.

Friendly Follower (FF)

- Slightly higher risk tolerance than PP, but still low to medium.

- Passive in the sense of relying heavily on friends, media, or advisers for ideas.

- Dominant biases: regret aversion, herding, availability, framing, and hindsight.

Key Term: Friendly Follower (FF)

A follower-oriented investor type with low-to-moderate risk tolerance and mainly cognitive biases, prone to herding, trend following, and overestimating risk tolerance.

Typical manifestations:

- Likes “hot ideas” and popular funds, often chasing recent performance.

- Overestimates risk tolerance by wanting exposure to high-volatility assets because “everyone else is doing it.”

- Comfortable delegating decisions but may later suffer regret if peers outperform.

Advisory implications:

- Advice approach: Educate using peer comparisons (for example, diversified model portfolios) and clear, data-backed explanations. Encourage introspection about past episodes of regret and overreaction to trends.

- Portfolio design: Emphasize diversification and systematic rebalancing. Provide simple model portfolios instead of a long list of enticing ideas, to reduce the tendency to chase everything.

- Exam angle: When you see clients eager to invest in recent winners and heavily influenced by peers yet open to guidance and data, FF is likely.

Independent Individualist (II)

- Moderate to high risk tolerance.

- Active, self-directed, confident, and often contrarian.

- Dominant biases: conservatism, confirmation, representativeness, availability; emotional overconfidence and self-attribution can also appear.

Key Term: Independent Individualist (II)

An analytical, self-directed investor type with medium-to-high risk tolerance and mainly cognitive biases, including conservatism, confirmation, and representativeness, often combined with overconfidence.

Typical manifestations:

- Performs own research and enjoys investing, but may rely heavily on favored sources (websites, newsletters) and ignore contrary evidence.

- May hold idiosyncratic or contrarian positions and stick with them despite new information.

- Likes to “trust their own judgment” rather than follow advisers blindly.

Advisory implications:

- Advice approach: Use logical support and robust data. Respect their intelligence and independence; avoid paternalistic or purely emotional appeals.

- Portfolio design: Work collaboratively to codify a disciplined investment process (for example, rebalancing rules, diversification thresholds) that still allows room for independent ideas within a risk-controlled framework.

- Exam angle: When vignettes describe strong-willed, self-confident investors making independent decisions but willing to consider data, classify as II and focus on education and process improvements.

Active Accumulator (AA)

- Highest risk tolerance.

- Highly active, entrepreneurial, and action-oriented.

- Dominant biases: overconfidence, self-control issues, illusion of control.

Key Term: Active Accumulator (AA)

An aggressive, entrepreneurial investor type with high risk tolerance and primarily emotional biases, especially overconfidence and illusion of control, often trading frequently and stretching risk limits.

Typical manifestations:

- Heavy trading, use of leverage or margin, and concentrated speculative positions.

- Belief that they can control or predict outcomes (“I can get out before the market turns”).

- May neglect diversification and risk controls, viewing them as constraints on opportunity.

Advisory implications:

- Advice approach: Set robust guidelines and emphasize discipline. Establish clear risk limits, pre-agreed stop-loss or drawdown thresholds, and explicit constraints on leverage and concentration.

- Portfolio design: Segregate a “core” portfolio aligned with long-term objectives from a smaller “satellite” or “play” portion where the client can express strong views without jeopardizing primary goals.

- Exam angle: When vignettes mention entrepreneurs, leverage, frequent trading, and performance-chasing, AA is the likely BIT, and the recommended answer will emphasize tight risk control and monitoring rather than emotional reassurance.

Classification, Limitations, and Blended Types

No real client fits a pure BIT; most exhibit a mix of characteristics from adjacent types. Additionally, dominant biases may shift over time or in response to major life or market events. Behavioral profiling is a client management tool—not a rigid categorization.

Key limitations highlighted in the curriculum include:

- Overlap of cognitive and emotional biases: The same investor may display cognitive errors (for example, anchoring) and emotional biases (for example, loss aversion). You can rarely label a client as purely “emotional” or purely “cognitive.”

- Multiple BIT characteristics: An investor may resemble a Friendly Follower in bull markets (herding into hot sectors) but behave as a Passive Preserver after experiencing large losses. Judgment is required to decide which traits dominate at a given time.

- Behavior changes with age and circumstances: As investors age, experience changes in employment, or face new obligations (for example, elder care, education funding), risk tolerance and emotional sensitivity often shift. BITs must be reassessed periodically.

- Need for individualized treatment: Two Passive Preservers may require different responses. One may accept some equity exposure, while another may require an even more capital-preservation-oriented portfolio.

- Unpredictable timing of irrationality: Clients may behave rationally for long periods and then suddenly act in a strongly biased way during periods of stress. The BIT framework cannot predict exact timing, only likely patterns.

On exam questions, you are expected to recognize these limitations and avoid over-committing to a “type” when evidence is mixed. A good answer might explicitly note that a client is “primarily AA with some II traits” and explain how that affects recommended constraints and communication.

Worked Example 1.1

An adviser meets Kim, who refuses to sell inherited stock despite holding 70% of her portfolio in it. She is anxious about any change and ignores statistical evidence of risk.

Answer:

Kim fits the Passive Preserver BIT, with emotional biases (loss aversion, endowment, regret aversion, and status quo). Her primary concern is security and avoiding regret, not maximizing expected return. The recommended approach is gradual diversification (for example, staged sales or using new contributions to build other positions), emotional support, and a focus on how modest changes support her long-term security. Aggressive use of complex statistics is unlikely to change her behavior and may even increase anxiety.

Worked Example 1.2

A self-employed client regularly trades on economic speculation, uses margin, and rarely studies detailed reports. She wants to outperform her business rivals and is often “sure” of her market timing skills.

Answer:

She matches an Active Accumulator BIT. Overconfidence, self-control issues, and illusion of control are likely primary biases. A disciplined process, pre-set risk limits (for example, cap leverage and concentration), and strong monitoring are key. A practical approach is to ring-fence a limited “trading” allocation while preserving a core portfolio aligned with her long-term objectives. Education alone is unlikely to suffice; structural safeguards are needed.

Worked Example 1.3

A client enjoys researching investments, constructs his own spreadsheets, and often takes contrarian positions. He insists on keeping a value stock that has missed earnings several times because “the market will eventually recognize its true worth,” despite several negative analyst reports he has not read.

Answer:

This client is best classified as an Independent Individualist, dominated by cognitive biases such as conservatism (underreacting to new information), confirmation bias (seeking only supportive data), and possibly representativeness. The adviser should not challenge his independence directly but should introduce process improvements: require pre-trade investment theses, schedule periodic review of positions against predefined sell criteria, and encourage systematic consideration of disconfirming evidence. The IPS might include explicit diversification and review rules rather than relying solely on judgment.

Behavioral Profiling Process

Behavioral profiling for CFA purposes typically involves several stages, which mirror the “Behavioral Alpha” top-down process described in the curriculum.

Behavioral client classification presents four investor types with characteristic involvement, risk tolerance, and predominance of emotional biases or cognitive errors.

Key Term: behavioral profiling

The process of identifying an investor’s dominant behavior patterns and likely biases, used to guide portfolio design, suitability assessments, and adviser communication. Key Term: Behavioral Alpha (BA) approach

A top-down behavioral process that classifies clients into BITs by first identifying active/passive traits and risk tolerance, then testing for expected biases, with the goal of improving outcomes by aligning portfolios with investor psychology.

A practical four-step process:

-

Step 1 – Identify active/passive traits and risk tolerance: Through the initial client interview, the adviser gathers information on how the client created wealth (risking own capital versus more passive accumulation), how involved they want to be in investment decisions, and their willingness and ability to take risk. Simple questionnaires can be used to distinguish active from passive tendencies and approximate risk tolerance.

-

Step 2 – Place the client on the active/passive and risk axes: Client responses are used to locate them on a conceptual grid: passive-active on one axis and low-high risk tolerance on the other. Passive, low-risk clients are more likely to be PPs; passive with somewhat higher risk tolerance are likely FFs; active with medium–high risk tolerance are IIs; and active with high risk tolerance are AAs. If the active/passive classification conflicts with risk tolerance, risk tolerance should generally dominate.

-

Step 3 – Test for likely behavioral biases: Based on the provisional BIT indicated by Step 2, the adviser probes for the biases expected for that type (for example, loss aversion and endowment for PPs; overconfidence and illusion of control for AAs). Probing can include questions about past responses to market falls, attitudes to diversification, and reactions to missed gains or realized losses.

-

Step 4 – Confirm and assign BIT classification: If the client’s observed behavior and dominant biases match the profile suggested by their grid location, the adviser classifies them into that BIT. If there is significant inconsistency, the adviser either assigns a blended classification (for example, “PP/FF hybrid”) or returns to the earlier steps for clarification.

Behavioral profiling also involves:

- Reviewing client history, wealth source, and investment experience.

- Observing expressed attitudes toward gains, losses, and volatility.

- Considering client reactions to previous market declines or advice.

- Documenting dominant behavioral biases in the IPS and including tailored communication guidelines.

In exam questions, you may be asked to identify the BIT from a short vignette and then explain how that classification should influence risk objectives, constraints, and the recommended communication style.

Tailoring Portfolio Strategies to Behavioral Type

Once BITs and biases are identified, CFA candidates should be able to recommend:

- how to adjust the IPS and portfolio guidance to accommodate emotional biases,

- when to move forward with data-driven education (for cognitive error–dominated types),

- how to sequence or communicate change to minimize emotional resistance,

- and specific monitoring or review strategies based on client profile.

Key principles:

- Adjust for emotional biases: For PPs and AAs, portfolios will often deliberately deviate from the “optimal” mean–variance allocation to increase the probability that the client can follow the plan. For PPs, this may mean more capital preservation; for AAs, more guardrails and limits.

- Moderate cognitive errors: For FFs and IIs, emphasize investor education, quantitative evidence, and structured processes. Over time, you aim to move these clients closer to rational asset allocation, because their biases are more amenable to change.

- Align risk tolerance in the IPS: The IPS must reflect the client’s effective (behaviorally-adjusted) willingness to take risk, not just their theoretical ability. An apparently wealthy client with extreme loss aversion (PP) may warrant a lower-risk allocation than traditional finance alone would suggest, provided objectives are still feasible.

- Incorporate behavioral constraints explicitly: The IPS can note “legacy” holdings the client insists on retaining, maximum acceptable drawdowns for emotional clients, or explicit limits on leverage for AAs. These are behavioral constraints that shape feasible asset allocations.

Worked Example 1.4

A wealthy 45-year-old entrepreneur has significant financial ability to take risk. However, after a large loss in a previous market downturn, he is now very focused on avoiding further losses and becomes visibly anxious when equity volatility is discussed. He still wants to grow wealth but says, “I never want to go through that again.”

You must draft a risk objective and asset-allocation recommendation.

Answer:

Although his financial ability to take risk is high, his behavioral profile shows strong loss aversion and anxiety—Passive Preserver traits. The risk objective should emphasize capital preservation with modest real growth, acknowledging that his willingness to take risk is low. A behaviorally-modified asset allocation might include a relatively high allocation to high-quality bonds and cash, with a smaller, globally diversified equity allocation than a purely ability-based analysis would suggest. The justification in an exam answer should explicitly state that the portfolio intentionally sacrifices some expected return to increase the likelihood that he will follow the plan, given his emotional biases.Exam Warning: Over-relying on fixed investor “types” or expecting a profile to remain static may lead to poor advice and suitability errors. Always reassess BITs after major market moves or life changes, and explicitly acknowledge in written answers that classifications are approximations used to improve, not replace, traditional risk–return analysis.

Summary

Behavioral investor types provide a structured approach to identifying and addressing investor biases in practical portfolio management. Recognizing both emotional and cognitive components is essential. Proper client profiling improves suitability, communication, and portfolio recommendations. For the CFA exam, you should be able to diagnose primary BITs, recognize the blended nature of real-world clients, and tailor the IPS and asset allocation process accordingly, explaining when you are moderating cognitive errors and when you are adjusting for emotional biases.

Key Point Checklist

This article has covered the following key knowledge points:

- The difference between emotional biases and cognitive errors, and the practical consequences for portfolio management and communication.

- The two broad categories of cognitive errors: belief perseverance biases and processing errors.

- Four primary behavioral investor types (BITs): Passive Preserver, Friendly Follower, Independent Individualist, Active Accumulator, and their dominant biases.

- The Behavioral Alpha top-down process: identifying active/passive traits, risk tolerance, testing for biases, and assigning BITs.

- How to profile and recognize blended or changing behavioral types, and the limitations of rigid classifications.

- How behavioral profiling feeds into IPS design, including risk objectives, behavioral constraints, and asset-allocation guidance.

- How to tailor education, portfolio construction, and monitoring strategies to emotional versus cognitive bias dominance in exam-style vignettes.

Key Terms and Concepts

- behavioral bias

- Behavioral Finance Micro (BFMI)

- Behavioral Finance Macro (BFMA)

- emotional bias

- cognitive error

- belief perseverance bias

- processing error

- behavioral investor type (BIT)

- Passive Preserver (PP)

- Friendly Follower (FF)

- Independent Individualist (II)

- Active Accumulator (AA)

- behavioral profiling

- Behavioral Alpha (BA) approach