Learning Outcomes

This article explains investor biases and behavioural error types in a CFA Level 3 context, including:

- Distinguishing cognitive errors from emotional biases in client vignettes.

- Linking specific biases to portfolio construction, risk tolerance, and behavioural investor types.

- Evaluating when a bias can be moderated versus when it should be adapted to.

- Recommending realistic mitigation techniques that improve client outcomes and exam responses.

This article explains investor biases and behavioural error types in a CFA Level 3 context, focusing on the distinction between cognitive errors and emotional biases in real-world investment decisions. It clarifies how faulty information processing leads to specific cognitive errors, how emotions and impulses generate distinct emotional biases, and why this difference determines whether an adviser should attempt to moderate or instead accommodate the bias. The article details major categories and examples in each group, links them to typical exam vignettes, and highlights how biases influence portfolio construction, risk tolerance assessment, and client communication. It also emphasizes practical diagnostic cues for identifying the bias described in a case, guides the choice of appropriate mitigation techniques, and demonstrates their application through worked examples that mirror exam-style item sets. Overall, the article reinforces the conceptual framework, vocabulary, and exam-ready reasoning needed to accurately classify investor biases, evaluate their impact on wealth management recommendations, and select responses that align both with behavioural finance theory and CFA Institute expectations.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand the difference between cognitive errors and emotional biases, identify examples of each, and explain their implications for portfolio construction and behavioural investor types, with a focus on the following syllabus points:

- Defining cognitive errors and emotional biases, with examples of each.

- Explaining how each bias impacts investment decisions and client risk tolerance.

- Assessing whether a bias can be moderated (reduced) or only accommodated.

- Recommending strategies for managing or accommodating investor biases in private wealth and institutional contexts.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which type of investor bias is generally more amenable to improvement through education, better information, and structured decision processes?

- a) Cognitive error

- b) Emotional bias

- c) Both are equally amenable

- d) Neither type can be improved in practice

-

Which combination correctly matches three cognitive errors and three emotional biases relevant to financial decisions?

- a) Anchoring, confirmation, loss aversion; framing, status quo, regret aversion

- b) Representativeness, mental accounting, hindsight; loss aversion, status quo, endowment

- c) Loss aversion, overconfidence, availability; anchoring, endowment, regret aversion

- d) Illusion of control, self-control, framing; confirmation, endowment, regret aversion

-

An investor refuses to sell a large, undiversified stock position inherited from a parent, despite clear evidence of concentration risk and overvaluation. Which bias best explains this behaviour?

- a) Representativeness bias

- b) Endowment bias

- c) Anchoring and adjustment bias

- d) Conservatism bias

Introduction

Investor behaviour often diverges from the fully rational, utility-maximising decision maker assumed in traditional finance. Faced with uncertainty, limited time, and complex information, people rely on shortcuts and are influenced by emotions, leading to systematic deviations from rational choices.

Behavioural finance distinguishes between:

- How individual investors behave relative to the rational benchmark, often called behavioural finance micro.

- How markets as a whole sometimes display anomalies relative to efficient markets, called behavioural finance macro.

In this article the focus is on behavioural finance micro — the biases that individual clients and professionals bring to financial decisions.

Key Term: cognitive error

A decision-making flaw rooted in faulty information processing, memory, or statistical reasoning, rather than emotion. Key Term: emotional bias

A judgemental error arising from intuition, impulse, or personal feelings, rather than from rational analysis.

When building or reviewing an IPS at Level 3, you are expected to:

- Identify which type of bias is present in a vignette.

- Explain how it affects the client’s risk perception, constraints, and willingness to follow recommendations.

- Recommend whether to attempt to correct the bias or instead design the portfolio around it.

A useful mental model is to view decisions along a spectrum from “cold” rational analysis to “hot” emotion-driven reactions. Cognitive errors are closer to the rational end — they arise because people mis-handle information or probabilities. Emotional biases are closer to the emotional end — they arise because people want to avoid psychological pain or seek emotional comfort.

Recognising where on this spectrum a client’s behaviour lies is often the key to answering “moderate versus accommodate” questions correctly in essay and item-set formats.

Test Tip: When revising Cognitive errors vs emotional biases, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

TYPES OF INVESTOR BIASES

Investor biases fall into two broad groups: cognitive errors and emotional biases. This distinction determines whether it is more effective to try to correct the bias, or simply adjust to it when managing portfolios.

Cognitive Errors

Cognitive errors stem from faulty reasoning and statistical misjudgement. Investors commit these mistakes because of limited attention, improper weighting of information, misunderstanding probabilities, or inappropriate application of decision rules (heuristics). Cognitive errors are mostly unintentional and can affect both laypeople and professionals.

Key Term: belief perseverance bias

A category of cognitive errors in which individuals irrationally cling to existing beliefs or forecasts, despite new information that should logically change those beliefs. Key Term: information-processing bias

A category of cognitive errors in which individuals mis-handle or misuse information when forming estimates or decisions.

Categories of Cognitive Errors

Cognitive errors commonly fall into two further groups:

-

Belief perseverance biases: Clinging to existing beliefs or forecasts and wrongly interpreting new information.

- Examples: Conservatism, Confirmation bias, Representativeness, Illusion of control, Hindsight bias

-

Information processing biases: Flawed use of information in making estimates or decisions.

- Examples: Anchoring and adjustment, Mental accounting, Framing, Availability bias

Below we expand on the major cognitive errors most likely to appear in Level 3 vignettes.

Belief perseverance biases

Key Term: conservatism bias

A belief perseverance bias in which people underreact to new information and overweight their prior views, adjusting beliefs too slowly.

Conservatism often shows up when analysts or clients stick to outdated forecasts despite clear changes in fundamentals (for example, refusing to cut an earnings forecast after a series of negative surprises). Consequences include delayed trades and persistent misallocations. Moderation involves explicitly updating forecasts using structured processes (for example, Bayesian updating or formal models) and challenging “house views”.

Key Term: confirmation bias

A belief perseverance bias in which people seek, notice, and overweight information that confirms existing beliefs, while ignoring or discounting contradictory evidence.

Typical exam cues include a client who “only reads reports that support her belief” or an analyst who “screens out” data that would invalidate a thesis. Confirmation bias often results in under-diversification and failure to sell losers. Moderation calls for deliberately seeking disconfirming evidence and using devil’s advocate or investment-committee challenges.

Key Term: representativeness bias

A belief perseverance bias in which people classify new information based on superficial similarity to existing categories, ignoring base rates or sample size.

Investors overweight recent performance of a fund manager or “hot” sector, assuming it is representative of long-run skill or growth, while neglecting objective probabilities. This can drive return-chasing and frequent manager turnover.

Key Term: illusion of control bias

A belief perseverance bias in which people overestimate their ability to control or influence outcomes that are largely random.

Illusion of control is common among active traders who believe their monitoring or “hands-on” trading gives them control over returns. Consequences include excessive trading and concentrated positions in familiar companies (e.g., employer stock). Moderation requires emphasising the probabilistic nature of markets, tracking trading performance, and documenting ex ante rationales for decisions.

Key Term: hindsight bias

A belief perseverance bias in which people perceive past events as having been more predictable than they really were and misremember their own predictions as more accurate.

Hindsight bias leads investors to overestimate their forecasting skill and become overconfident, often raising risk to unjustified levels. It also leads to unfair evaluations of managers (“we should have seen this coming”) despite decisions being reasonable ex ante. Maintaining an investment diary with dated forecasts is an effective moderation tool.

Information-processing biases

Key Term: anchoring and adjustment bias

An information-processing bias in which people rely too heavily on an initial value (the anchor) and make insufficient adjustments when new information arrives.

Common anchors include purchase price, recent high, or a round-number index level. Investors might refuse to sell until a stock “gets back to” its purchase price, even when fundamentals have deteriorated. Moderation involves explicitly justifying valuations from current fundamentals and asking whether an anchor is economically relevant.

Key Term: mental accounting bias

An information-processing bias in which people treat identical sums of money differently depending on the mental “account” to which they assign them.

Investors might separate “safe retirement money” and “vegas money”, ignoring correlations across accounts and overall risk. Mental accounting can sometimes be used constructively in goal-based planning, but unmanaged it leads to inefficient portfolios. Moderation includes aggregating all holdings into a single balance sheet and emphasising total-return rather than “income only” thinking.

Key Term: framing bias

An information-processing bias in which people’s choices are affected by how information or questions are presented, such as gain versus loss framing.

For example, a client may prefer a portfolio when told “70% chance of meeting your goal” but reject a statistically equivalent portfolio described as “30% chance of falling short”. Framing distorts perceived risk tolerance. Moderation involves presenting options in multiple frames (percentages, ranges, scenarios) and checking for consistency of preferences.

Key Term: availability bias

An information-processing bias in which people estimate the likelihood of an outcome based on how easily examples come to mind, rather than on objective probabilities.

Heavily advertised mutual funds, recent market headlines, or familiar domestic companies get overweighted. Consequences include home bias, concentration in popular sectors, and under-diversification. Moderation relies on disciplined screening of the full opportunity set and clear investment policy statements that limit ad hoc idea selection.

Emotional Biases

Emotional biases are driven by personal feelings, impulses, or the desire to avoid pain and seek pleasure. These biases are more difficult to correct because they often operate below the level of conscious awareness.

Key Term: bias adaptation

The process of recognising an emotional bias, accepting its influence, and structuring decisions to limit its impact, rather than striving to eliminate it.

From a Level 3 exam standpoint, the key is recognising that with emotional biases, pushing too hard on “rational” arguments can damage the adviser–client relationship and reduce long-term adherence to the plan. Designing the portfolio around the bias is usually more realistic.

Common Emotional Bias Examples

Key Term: loss-aversion bias

An emotional bias in which people experience the pain of losses more intensely than the pleasure of equal-sized gains, leading to asymmetric risk attitudes.

Loss aversion helps explain the disposition effect — the tendency to hold losers too long and sell winners too early — and myopic loss aversion, where investors focus excessively on short-term losses.

Key Term: overconfidence bias

An emotional bias in which people place unwarranted faith in their own skill, knowledge, or forecasts, often reinforced by self-attribution of past successes.

Overconfident investors underestimate risk, trade too frequently, and hold undiversified portfolios. Unlike illusion of control (a cognitive error about causality), overconfidence reflects an emotionally driven self-perception. Moderation is challenging but can be partly achieved by performance reviews and setting trading constraints.

Key Term: self-control bias

An emotional bias in which people struggle to act in accordance with long-term goals because short-term gratification dominates their decisions.

Hyperbolic discounting — placing disproportionate weight on immediate consumption — is a related concept. Self-control bias leads to under-saving and inappropriate risk-taking later in life in an attempt to “catch up”. Adaptation often means automating savings and using commitment devices.

Key Term: status quo bias

An emotional bias in which people prefer maintaining their current situation and avoid change, even when change is objectively beneficial.

Status quo bias explains reluctance to rebalance, update asset allocations, or change managers. Adaptation might involve gradual transitions or default options consistent with the IPS.

Key Term: endowment bias

An emotional bias in which people assign higher value to assets they already own than to identical assets they do not own.

Endowment bias is especially strong for inherited or employer-related assets. It differs from status quo bias in that the attachment is to the asset itself, not just to “no change”. Adaptation often involves building diversification around the endowed asset or using hedging strategies rather than outright sale.

Key Term: regret-aversion bias

An emotional bias in which people avoid decisions that could lead to future regret, often preferring inaction or consensus choices.

Clients may avoid selling losers to avoid admitting a mistake, or may herd into popular funds to ensure they are “wrong with everyone else” rather than “wrong alone”. This bias is related to patterns seen in manager selection, where committees fear Type I errors (hiring a poor manager) more than Type II errors (failing to hire a good one).

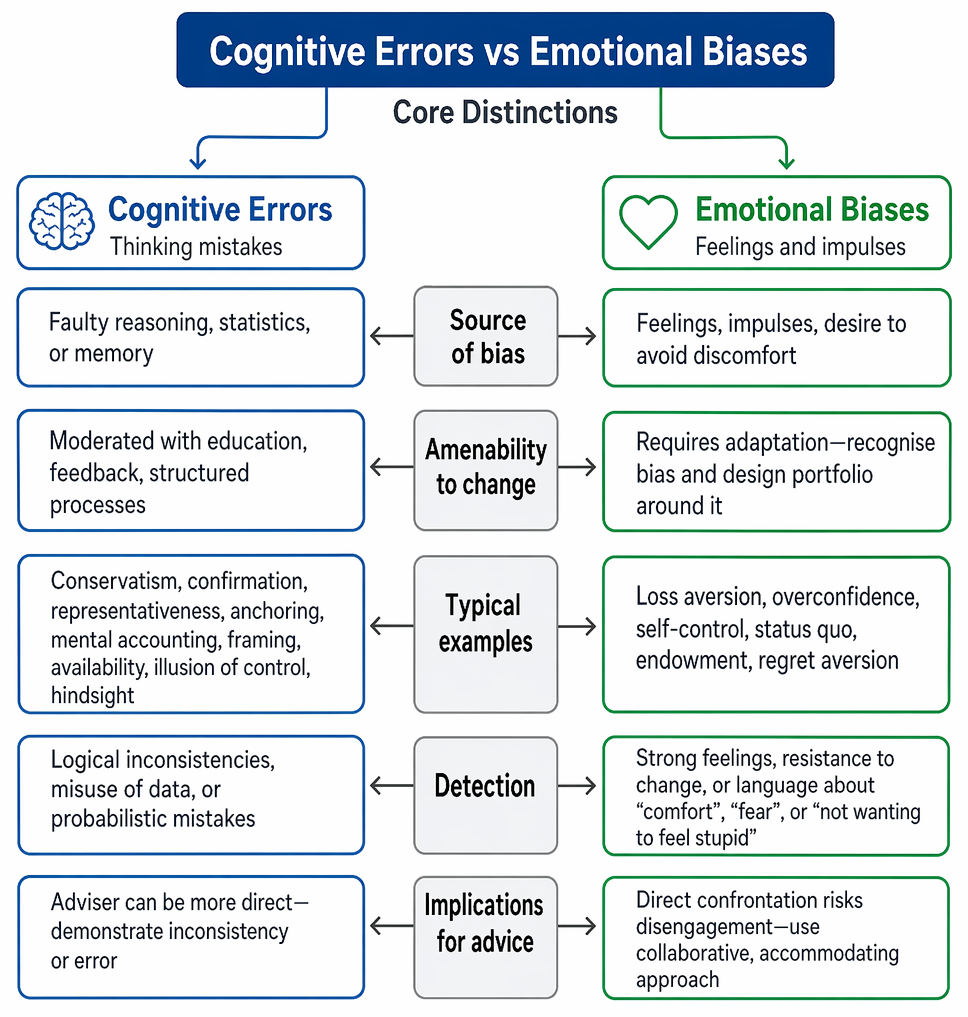

COGNITIVE ERRORS VS EMOTIONAL BIASES: CORE DISTINCTIONS

Understanding the differences between cognitive errors and emotional biases is critical for both exam questions and real-world advice.

Cognitive errors and emotional biases are compared by behavioural source, common manifestations, implications for risk tolerance, and appropriate adviser responses.

-

Source of bias:

- Cognitive errors arise from faulty reasoning, statistics, or memory — they are “thinking mistakes”.

- Emotional biases arise from feelings, impulses, and the desire to avoid psychological discomfort.

-

Amenability to change:

- Cognitive errors are often moderated with education, feedback, and structured decision processes.

- Emotional biases usually require adaptation — recognising the bias and designing the portfolio around it.

-

Typical examples:

- Cognitive: conservatism, confirmation, representativeness, anchoring, mental accounting, framing, availability, illusion of control, hindsight.

- Emotional: loss aversion, overconfidence, self-control, status quo, endowment, regret aversion.

-

Detection:

- Cognitive errors are revealed by logical inconsistencies, misuse of data, or probabilistic mistakes.

- Emotional biases are revealed by strong feelings, resistance to change, or language about “comfort”, “fear”, or “not wanting to feel stupid”.

-

Implications for advice:

- With cognitive errors, advisers can usually be more direct, demonstrating the inconsistency or error.

- With emotional biases, direct confrontation risks client disengagement; a more collaborative, accommodating approach is preferred.

Worked Example 1.1

A client refuses to update their portfolio despite evidence that former outperforming stocks now lag the benchmark. She says, “I feel comfortable with what I have; changing things makes me nervous.”

Answer:

The most applicable bias is status quo bias, an emotional bias where the investor prefers no change. The emotional language (“feel comfortable,” “nervous about change”) is a cue that this is not just a data-processing issue. Since emotional biases are harder to correct, the adviser should accommodate the bias: propose gradual changes, set rebalancing bands, and frame adjustments as risk-reduction rather than “changing everything,” rather than seek immediate, wholesale restructuring.

Worked Example 1.2

An investor only pays attention to new information that confirms their existing view that technology stocks will always outperform. They actively search for reports supporting this view and dismiss negative research as “noise”.

Answer:

This is confirmation bias, a belief perseverance cognitive error. The adviser should aim to moderate the bias by:

- Presenting evidence on cycles in sector performance and base rates of persistent outperformance.

- Explicitly reviewing disconfirming evidence in meetings.

- Using portfolio analytics to show concentration risk. The key is to show that ignoring contradictory information is logically inconsistent with the client’s stated objectives.

IMPACT ON WEALTH MANAGEMENT AND PORTFOLIO CONSTRUCTION

Understanding whether a client’s error is cognitive or emotional changes the adviser’s approach and, ultimately, the IPS and strategic asset allocation.

-

If the bias is a cognitive error:

- Encourage logical review with data. For example, for representativeness, show long-term performance dispersion of “hot” managers.

- Use education — explain probability, diversification benefits, and historical evidence.

- Build structured processes: investment policy statements, rebalancing rules, and checklists reduce room for ad hoc, biased decisions.

- In exam answers, verbs like “educate”, “demonstrate”, “quantify”, and “show” often signal moderation.

-

If the bias is an emotional bias:

-

Avoid direct confrontation; acknowledge the client’s feelings.

-

Accommodate the bias by incorporating the bias into portfolio design:

- For loss-averse clients, a higher allocation to low-volatility assets or explicit “safety buckets”.

- For endowment bias, allow a capped concentrated position and diversify around it.

-

Emphasise strategies that increase long-term adherence, even if they are slightly suboptimal in a mean–variance sense.

-

In exam answers, verbs like “accommodate”, “structure”, “segment”, and “build around” typically indicate adaptation.

-

Biases also influence manager selection and monitoring:

- Regret aversion and loss aversion can drive committees to focus excessively on avoiding Type I errors (hiring an underperformer), leading to trend-following and high manager turnover.

- Overconfidence may lead CIOs to overweight active strategies or allocate to complex alternatives without sufficient due diligence.

Relating biases to Type I/II errors and their costs shows synthesis-level understanding in essays.

Exam Warning: For CFA exam questions, mixing up cognitive errors with emotional biases, or treating all as equally amendable to logical correction, is a frequent source of error. Always check whether the bias described originates from faulty logic (cognitive) or feeling (emotional). Look for emotional language, family or legacy attachments, or fear of regret — these usually point to emotional biases requiring adaptation.

BIAS MITIGATION TECHNIQUES

Mitigation strategies must be matched to the type of bias.

-

For cognitive errors (moderation focus):

- Provide education on probability, diversification, and historical evidence.

- Highlight alternative data and base rates; use scenario and sensitivity analysis.

- Use checklists and documented decision processes to reduce ad hoc reasoning.

- Encourage review of past mistakes, maintaining a decision journal to counter hindsight and overconfidence.

-

For emotional biases (adaptation focus):

-

Accept that some biases cannot realistically be eliminated.

-

Structure portfolios to accommodate the bias:

- More cash or capital-protected products for highly loss-averse clients.

- Multi-bucket or layered portfolios that separate “safety” assets from “aspirational” assets, consistent with mental accounting but still globally coherent.

-

Use goal-based approaches rather than pure mean–variance optimisation, particularly for retail private wealth clients.

-

Employ gradual implementation and default options to work with status quo and regret-aversion biases.

-

Worked Example 1.3

A 53-year-old inheritor becomes emotionally attached to inherited stock and refuses to sell, despite heavy concentration risk and clear evidence that the company faces structural decline. The position is 40% of her liquid wealth, and she says, “This stock built my family’s fortune; selling it would feel like betraying my parents.”

Answer:

This is endowment bias, an emotional bias rooted in attachment to owned assets, reinforced by family legacy. The adviser should primarily accommodate the bias:

- Accept that full diversification may be unrealistic in the short term.

- Propose partial sales over time, perhaps linked to price triggers or life events.

- Build diversification around the holding, adding uncorrelated assets to reduce overall risk.

- Consider hedging strategies (e.g., collars) if available and suitable. Directly pressing for immediate sale is likely to fail and damage the relationship.

Worked Example 1.4

A 40-year-old entrepreneur insists on investing only in small-cap growth stocks similar to his own business. He has enjoyed strong returns in recent years and says, “I have a good feel for these companies; I know how to pick winners.”

Answer:

The dominant bias is overconfidence bias, an emotional bias, potentially reinforced by illusion of control (a cognitive error). The emotional self-belief suggests that complete moderation is unlikely. The adviser should:

- Partly moderate by reviewing the entrepreneur’s actual investment track record and demonstrating concentration risk.

- Partly accommodate the bias by allowing an “active sleeve” where the client can pick such stocks within limits, while ring-fencing a core diversified portfolio aligned with long-term goals. Recognising the mix of cognitive and emotional components and designing a hybrid response shows higher-level understanding.

Summary

Investment biases can be split into cognitive errors (from flawed logic) and emotional biases (from feelings and impulses). Cognitive errors can usually be moderated by explanation, structured processes, and education; emotional biases generally must be identified and accepted, adapting the advice and portfolio to client preferences.

At Level 3, the examiner expects you not only to label the bias correctly, but also to:

- Judge whether moderation or adaptation is more realistic.

- Explain specific portfolio and process implications (asset allocation, diversification, rebalancing, manager selection).

- Propose practical steps consistent with both behavioural finance and the client’s IPS.

Accurately mapping vignettes to this framework is a frequent differentiator between mid-level and top-level exam responses.

Key Point Checklist

This article has covered the following key knowledge points:

- Differences between cognitive errors and emotional biases in investment decision-making.

- Typical biases in each category, including conservatism, confirmation, representativeness, anchoring, mental accounting, framing, availability, loss aversion, overconfidence, self-control, status quo, endowment, and regret aversion.

- Diagnostic cues in vignettes for distinguishing logic-based errors from feeling-based biases.

- Implications for bias detection and correction (moderation) versus adaptation in IPS design and portfolio construction.

- Practical approaches to managing client biases, including education, process discipline, goal-based structures, and portfolio segmentation.

- Relevance of biases to manager selection and monitoring, especially through regret and loss aversion.

- Importance of matching mitigation technique to the bias type for both exam answers and real-world practice.

Key Terms and Concepts

- cognitive error

- emotional bias

- belief perseverance bias

- information-processing bias

- conservatism bias

- confirmation bias

- representativeness bias

- illusion of control bias

- hindsight bias

- anchoring and adjustment bias

- mental accounting bias

- framing bias

- availability bias

- bias adaptation

- loss-aversion bias

- overconfidence bias

- self-control bias

- status quo bias

- endowment bias

- regret-aversion bias