Learning Outcomes

This article explains liability-driven and goal-based asset allocation in an exam-focused manner, including:

- understanding the rationale for shifting from asset-only optimization to liability-relative and goal-based frameworks, and identifying when each approach is most appropriate for institutional and private clients;

- constructing, interpreting, and comparing surplus efficient frontiers, including how surplus risk, surplus return, and asset–liability correlations jointly determine optimal portfolios;

- distinguishing surplus optimization from traditional mean–variance optimization in terms of objectives, constraints, risk measures, and practical implications for funding stability and contribution policy;

- analyzing the structure of liability-driven investing, with emphasis on designing and funding hedging and return-seeking portfolios that reflect liability characteristics, funding status, and risk tolerance;

- applying goal-based allocation to multi-goal individual clients, including mapping goals to sub-portfolios, setting risk tolerances and horizons by goal, and recognizing trade-offs versus a single efficient portfolio;

- evaluating the advantages and limitations of surplus optimization, LDI, and goal-based approaches, and recognizing common pitfalls tested at CFA Level 3, such as ignoring liability behavior, mismeasuring risk, or misaligning portfolio design with stated objectives.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are expected to understand the application of liability-driven approaches such as LDI, surplus optimization, and goal-based allocation, with a focus on the following syllabus points:

- Recognizing the difference between asset-only and liability-relative allocation

- Applying surplus optimization methodology in ALM

- Constructing hedging and return-seeking portfolios for liability-driven investing

- Explaining surplus efficient frontiers and evaluating surplus risk

- Applying goal-based asset allocation for individuals with multiple objectives

- Evaluating the strengths and limitations of LDI/goal-based approaches for the exam

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What are the main differences between traditional mean-variance optimization and surplus optimization in ALM?

- In the context of LDI, explain how the hedging and return-seeking portfolio structure aligns with liability characteristics.

- For a client with multiple goals, how does goal-based allocation differ from a single risk–return efficient portfolio?

Introduction

Liability-driven and goal-based investing approaches are central to CFA Level 3 exam topics in asset-liability management (ALM) and private wealth. These frameworks shift the focus from maximizing asset returns alone to meeting specific liabilities or prioritized financial goals. Surplus optimization adapts classic mean-variance analysis to account for both assets and liabilities, aiming to maximize the surplus of assets over obligations, with risk measured by the volatility of that surplus. For both institutional and individual clients, understanding surplus optimization and the structure of liability-driven investing (LDI) is essential for both practical implementation and exam success.

Key Term: Surplus Optimization

Surplus optimization is an asset allocation process that maximizes expected surplus (assets minus liabilities) for a given level of surplus risk, rather than maximizing asset return alone. Key Term: Liability-Driven Investing (LDI)

LDI is a strategy that allocates assets with the goal of meeting liabilities, focusing on asset-liability matching, hedging relevant risks, and surplus volatility management.Test Tip: When revising ALM surplus optimization and LDI, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

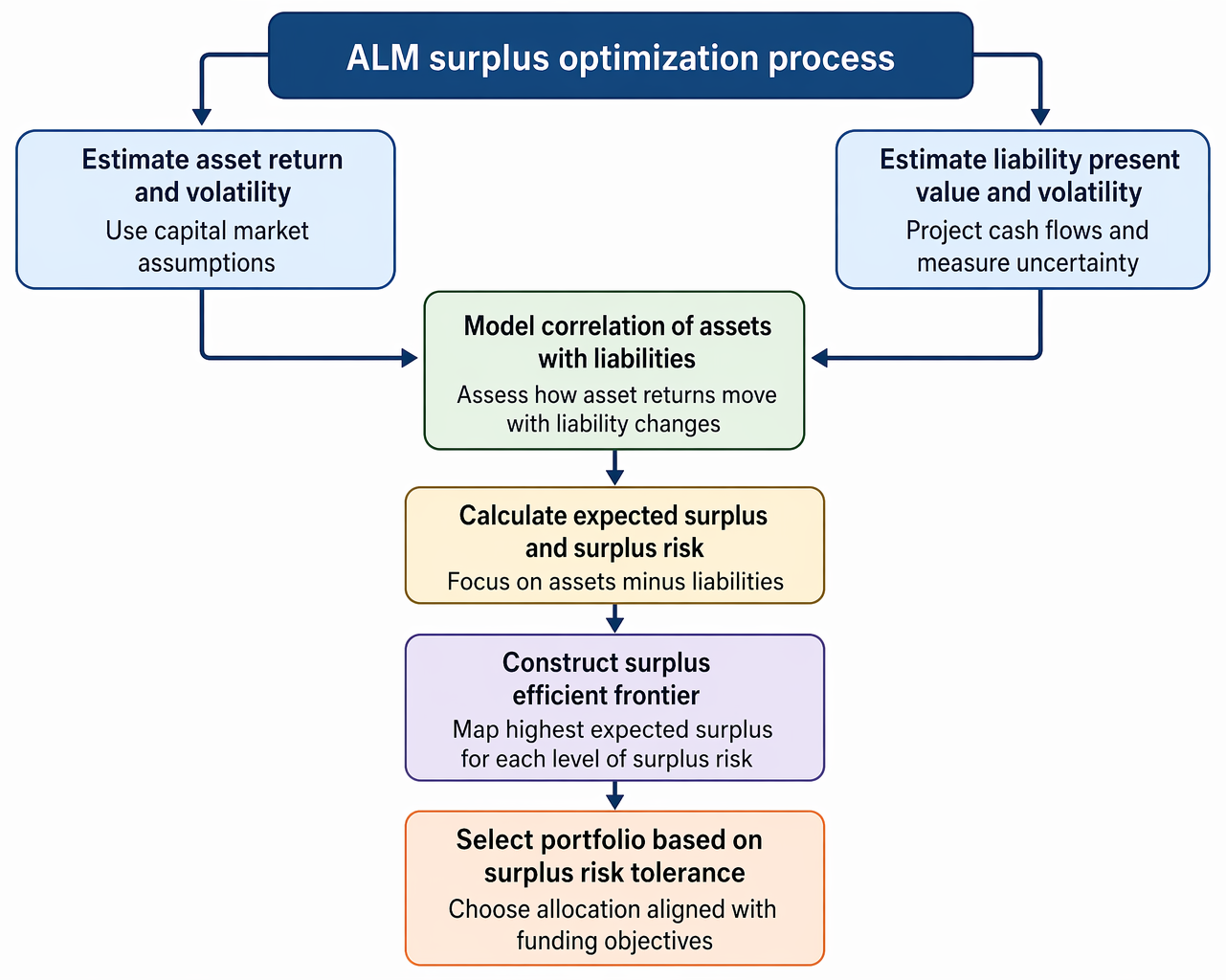

Surplus Optimization and the Surplus Efficient Frontier

Surplus optimization extends traditional mean-variance optimization by including the present value of liabilities in the analysis. Risk is measured using the volatility of the surplus (assets minus liabilities), not just the volatility of assets. By using a surplus efficient frontier, the objective is to select portfolios that maximize expected surplus return for acceptable surplus risk, considering the correlation between assets and liabilities.

ALM surplus optimization integrates asset and liability estimates to derive expected surplus, construct the surplus efficient frontier, and select portfolios.

Key Term: Surplus Efficient Frontier

The surplus efficient frontier is the set of portfolios that offer the maximum expected surplus return for each level of surplus risk, considering both asset and liability behaviors.

Worked Example 1.1

A pension plan’s projected benefit obligation has a present value of $100 million. You model several asset portfolios and find that their expected returns and correlations with the plan liabilities differ substantially. How does selecting a portfolio based solely on asset return differ from selecting along the surplus efficient frontier?

Answer:

Asset-only optimization will select the highest expected return for a given level of asset volatility, with no regard for liability behavior or funding risk. Surplus optimization, by contrast, will account for how portfolio returns and volatilities interact with changes in the liability value and choose the allocation that offers the most favorable expected surplus return for a selected surplus risk, directly addressing plan solvency.

Structure of LDI Asset Allocation: Hedging and Return-Seeking Portfolios

LDI typically divides the allocation into a ‘hedging portfolio’ designed to hedge liability cash flows and related risk factors (duration, inflation, etc.), and a ‘return-seeking portfolio’ to increase surplus by capturing risk premia.

Key Term: Hedging Portfolio

A hedging portfolio is constructed to offset changes in the value of liabilities, generally using duration-matched high-quality fixed income or derivatives. Key Term: Return-Seeking Portfolio

Return-seeking portfolios invest in equities, alternatives, or other growth assets to add surplus beyond what is needed for liability matching.

The classic two-portfolio LDI structure allocates assets first to the hedging portfolio (to match the present value and volatility of liabilities), then allocates any surplus to the return-seeking portfolio, maximizing the likelihood of asset sufficiency.

Worked Example 1.2

A pension fund is 110% funded and wishes to minimize contribution volatility. It builds a bond portfolio that closely matches the interest rate sensitivity of plan liabilities and invests all remaining assets in a diversified return-seeking portfolio. What is the benefit of this approach compared to a 60/40 fixed-mix allocation?

Answer:

Matching liability duration hedges interest rate risk, helping ensure asset values change in tandem with liabilities, therefore reducing surplus volatility and required contributions. Allocating surplus to return-seeking assets seeks to grow funding status efficiently. This approach is likely to offer better solvency risk control than a fixed-mix asset-only strategy that ignores liability behavior.

Surplus Optimization versus Traditional Mean-Variance Optimization

Traditional MVO maximizes asset return for a specified level of portfolio risk, while ignoring liabilities. In surplus optimization, the risk and return characteristics of both assets and liabilities (and their correlation) are modeled together. Risk is measured by surplus volatility (or shortfall risk) and not just by asset volatility. This distinction is especially important for investors with long-duration or inflation-sensitive liabilities.

Key Term: Shortfall Risk

Shortfall risk is the probability that asset values will fall below liability values, resulting in a funding deficit.Exam Warning: Omitting the impact of asset-liability correlations or failing to recognize that asset volatility alone is not an adequate risk measure for liability-driven mandates is a common error. Always model surplus or asset-liability volatility, not assets in isolation.

Goal-Based Allocation for Individual Clients

Goal-based investing addresses the multiple and often competing objectives of individuals or families by allocating assets to distinct sub-portfolios, each matched to a specific financial goal, risk level, and time horizon. Each goal receives its own optimized allocation. The overall portfolio is then the combination of the allocations to each goal, typically sacrificing some theoretical global efficiency in favor of client adherence and clarity of purpose.

Key Term: Goal-Based Asset Allocation

Goal-based asset allocation is an investment approach that creates distinct portfolios for prioritized client goals, setting portfolio risk and return based on each goal’s needs.

Worked Example 1.3

A client wants to fund their retirement, pay for a child’s university expenses in 8 years, and provide a charitable bequest. How can the goal-based approach improve client suitability compared to a mean-variance-optimized portfolio?

Answer:

Each goal receives a dedicated sub-portfolio, with its own risk profile and constraints (e.g., a more conservative allocation for the university goal and a higher-risk allocation for the bequest). This enhances the probability of achieving each goal and helps manage behavioral risks by allowing separate monitoring and rebalancing.

Advantages and Limitations of Surplus Optimization and LDI

Advantages:

- Focuses directly on the investor's fundamental objective: meeting liabilities or goals.

- Explicitly models surplus risk, enabling control of solvency risk.

- Improves monitoring and alignment of investment strategy to client needs.

Limitations:

- Requires sophisticated modeling of assets, liabilities, and correlations.

- May be sensitive to input assumptions and stressed scenarios.

- Transaction and implementation complexity (especially for LDI-like private mandates).

Key Point Checklist

This article has covered the following key knowledge points:

- Differences between asset-only and surplus (liability-relative) optimization

- Construction and interpretation of the surplus efficient frontier

- Role of hedging and return-seeking portfolios in LDI asset allocation

- Practical structure of LDI for DB pension plans and individual clients with competing goals

- Goal-based asset allocation as applied to individual objectives

- Key strengths and limitations of LDI and surplus optimization in institutional and private wealth contexts

Key Terms and Concepts

- Surplus Optimization

- Liability-Driven Investing (LDI)

- Surplus Efficient Frontier

- Hedging Portfolio

- Return-Seeking Portfolio

- Shortfall Risk

- Goal-Based Asset Allocation