Learning Outcomes

This article explains liability-driven and goal-based portfolio approaches, including:

- Defining funding ratio, surplus, and funding ratio risk, and contrasting these measures with traditional asset-only volatility.

- Measuring and interpreting surplus volatility, funding status, and changes in the funding ratio across different market and liability scenarios.

- Explaining the mechanics and purpose of asset‑liability management (ALM) for both institutional investors (such as defined benefit pension plans) and individual, goal‑based portfolios.

- Describing the structure and intuition of funding ratio and time‑based glidepaths, and how they systematically adjust allocations between growth and defensive assets.

- Analyzing how portfolio risk exposure should adjust as funding ratios, time horizons, and objectives change, with emphasis on dynamic, rules‑based rebalancing.

- Applying glidepath and funding ratio concepts to exam‑style numerical and qualitative questions, including surplus tracking, risk budgeting, and interpretation of scenario analysis.

- Evaluating the strengths, weaknesses, and practical implementation challenges of glidepath‑driven and funding ratio‑driven asset allocation frameworks in both institutional and individual settings.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand liability‑driven and goal‑based investment approaches, with a focus on the following syllabus points:

- Evaluating and measuring funding ratio risk in institutional (e.g., pension) and goal‑based (e.g., individual) portfolios, including surplus volatility and shortfall probabilities.

- Analyzing asset‑liability management (ALM) strategies, including surplus optimization, hedging/return‑seeking structures, and immunization concepts.

- Designing and applying funding ratio glidepaths and time‑based glidepaths, and understanding their impact on dynamic risk positioning over time.

- Comparing the strengths, weaknesses, and implementation challenges of glidepath‑based and funding ratio‑based asset allocation frameworks.

- Applying these concepts via quantitative and qualitative exam questions involving surplus tracking, scenario analysis, and dynamic allocation rules.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

For a defined benefit pension plan, which measure best captures funding ratio risk?

- a) The standard deviation of plan asset returns

- b) The probability distribution of the plan’s funding ratio over time

- c) The tracking error of plan asset returns versus an equity index

- d) The duration of the plan’s bond portfolio

-

In a funding ratio glidepath, which policy is most consistent with liability‑driven investing?

- a) Increase equity exposure as the funding ratio rises above 1.2

- b) Maintain a constant 60/40 equity/bond mix regardless of funding status

- c) Reduce growth exposure as the funding ratio improves above full funding

- d) Switch entirely to cash whenever the funding ratio falls below 1.0

-

For a pension fund that adopts surplus volatility as its risk metric rather than asset‑only volatility, which portfolio change is most likely?

- a) Increase allocations to long‑duration bonds that covary with liability values

- b) Reduce liability duration to minimize interest rate sensitivity

- c) Replace bonds with equities because they have higher expected returns

- d) Ignore changes in discount rates because they affect only liabilities

-

In a goal‑based framework for an individual investor, what is the main purpose of a dynamic glidepath?

- a) To maximize terminal wealth regardless of interim risk

- b) To shift risk exposure systematically as time to the goal and funding status change

- c) To maintain a constant portfolio beta over the investor’s life cycle

- d) To ensure the portfolio always tracks a broad market index

Introduction

Meeting future commitments—whether pension payments or individual financial goals—often requires more than maximizing returns or minimizing simple portfolio volatility. Modern asset allocation frameworks incorporate the interplay between assets, liabilities, and specific funding objectives. Approaches that account for the risk of failing to meet future obligations include funding ratio management, liability‑driven investing, and glidepath design. These methods are central for institutional investors like defined benefit pension plans and increasingly applied in goal‑based frameworks for individuals. This article explains funding ratio risk, surplus volatility, and the rationale for risk‑adjusted asset allocation over time, equipping you with assessment‑ready understanding for the CFA Level 3 exam.

Key Term: liability‑driven investing (LDI)

An investment approach that defines risk relative to a set of explicit liabilities, seeking to structure assets so that they track or hedge the value and cash flows of those liabilities rather than maximizing asset‑only returns. Key Term: liability

The present value of promised or expected future payments, discounted at an appropriate rate that reflects timing, risk, and any contractual features (such as indexation).

LDI reframes the central question from “How volatile are my assets?” to “How volatile is my ability to meet promised payments?” That distinction is central to funding ratio risk and glidepaths.

FUNDING RATIO RISK: CONCEPTS AND MEASUREMENT

The funding ratio is a core metric for liability‑driven and goal‑based investors. It measures the relationship between the current value of assets and the present value of liabilities or future goals.

Key Term: funding ratio

The ratio of the current market value of plan or goal‑funding assets to the present value of plan liabilities or targeted future outflows.

Formally, at time ,

where is the market value of assets and is the present value of remaining liabilities or goals.

A related concept is the surplus.

Key Term: surplus

The difference between the market value of assets and the present value of liabilities:

which can be positive (surplus) or negative (deficit). Key Term: funding status

A qualitative description of the relationship between assets and liabilities, often expressed as underfunded (funding ratio < 1, negative surplus), fully funded (≈1, surplus ≈ 0), or overfunded (> 1, positive surplus).

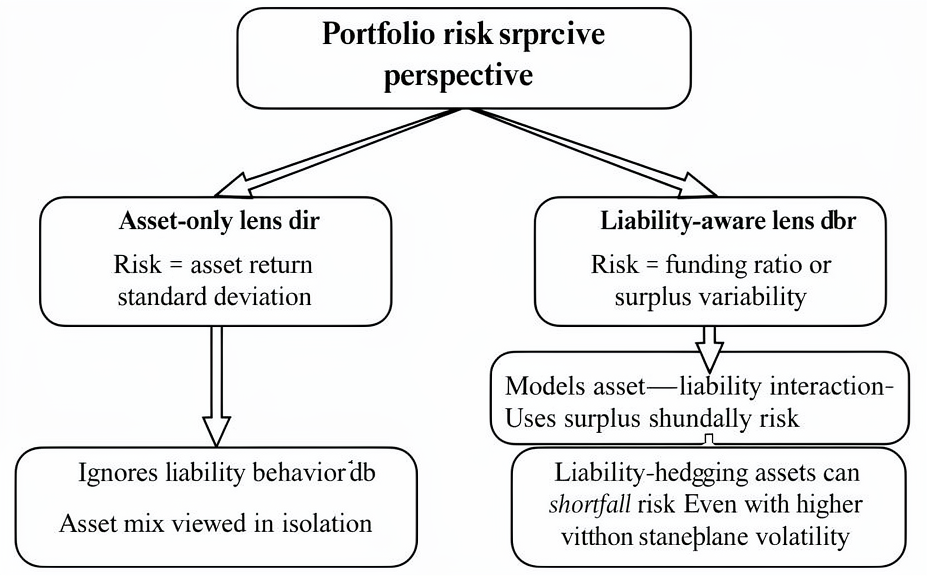

Funding ratio risk refers to the uncertainty in this measure over time—how volatile the ratio is due to movements in both asset and liability values. Unlike traditional risk measures, which typically focus on the portfolio's standard deviation, funding ratio risk focuses on the sufficiency of assets relative to future commitments.

Key Term: funding ratio risk

The potential for the funding ratio to change adversely, leading to a shortfall of assets relative to required liabilities or goals over the relevant horizon. Key Term: surplus volatility

The standard deviation of surplus returns, defined as asset returns minus liability returns, measuring risk in terms of changes to the net funding position.

Surplus return over a period is often defined as:

where and are changes in asset and liability values. Surplus volatility is then .

Increasing funding ratio risk means a greater likelihood of a shortfall and higher uncertainty in meeting obligations—central considerations for institutional portfolio design and, by analogy, for goal‑based portfolios.

Funding Ratio Risk vs. Asset‑Only Volatility

Traditional mean–variance analysis treats risk as the variability of asset returns. In a liability‑driven context, this is incomplete because:

- Liabilities themselves are sensitive to interest rates, inflation, salary growth (for pensions), or cost inflation (for goals such as education or healthcare).

- Assets and liabilities may move in offsetting or mutually amplifying ways. The correlation between asset returns and liability “returns” is critical.

- An asset strategy that appears risky in an asset‑only sense may actually reduce funding ratio risk if it hedges liability sensitivity.

For example, long‑duration bonds may increase asset‑only volatility but reduce surplus volatility if plan liabilities are also long‑duration and discounted at yields that covary with bond yields.

For exam purposes, always ask:

- How do asset values move?

- How do liability values move under the same scenario?

- What happens to surplus and the funding ratio?

A strategy that reduces surplus volatility, even at the cost of higher asset‑only volatility, can be more appropriate for an LDI investor.

Measuring Changes in the Funding Ratio

Changes in the funding ratio over a short horizon can be approximated by:

where is the asset return and is the liability return (percentage change in ). This highlights:

- Funding ratio improves if assets outperform liabilities ().

- Funding ratio deteriorates if liabilities “out‑earn” assets (), which can occur when discount rates fall and liability present values rise faster than asset values.

Exam questions may present scenarios with interest rate changes that move significantly, even when asset values are unchanged. Recognize that:

- A fall in discount rates increases and thus can reduce the funding ratio, even if asset returns are neutral.

- Strategies that lengthen asset duration can help mitigate this effect by increasing asset values when rates fall.

LIABILITY-DRIVEN INVESTING AND THE ROLE OF THE GLIDEPATH

The Liability‑Driven Mindset

Liability‑driven investing (LDI) explicitly accounts for how assets and liabilities interact. Here, risk is defined as the chance that assets will be insufficient at key future dates given liability payments or goal cash flows. Asset‑liability management strategies use metrics such as surplus volatility and funding status rather than simple asset volatility.

Key Term: asset‑liability management (ALM)

The coordinated management of assets and liabilities to optimize funding status and ensure the timely payment of obligations, typically using surplus volatility, funding ratio, and shortfall probability as core metrics.

ALM for a pension plan, insurer, or even an individual’s retirement portfolio typically involves:

- Identifying the term structure and nature of liabilities (timing, currency, inflation linkage, optionality).

- Constructing asset portfolios that hedge key risk exposures (e.g., interest rates, inflation) while seeking additional returns where appropriate.

- Monitoring funding status and adjusting exposures as conditions and objectives change.

From the curriculum’s asset allocation reading, three broad liability‑relative approaches are relevant conceptually:

- Surplus optimization: Extends mean–variance optimization by using surplus return and surplus volatility rather than asset return and asset volatility.

- Hedging/return‑seeking portfolios: Splits assets into a hedging portfolio and a return‑seeking portfolio.

- Integrated asset–liability approach: Jointly optimizes both sides of the balance sheet (more relevant for banks and insurers).

Key Term: hedging portfolio

A portfolio of assets designed to match the sensitivity of liabilities to key risk factors (e.g., interest rates, inflation), thereby stabilizing surplus or the funding ratio. Key Term: return‑seeking portfolio

The portion of assets invested primarily to generate growth in surplus and improve the funding ratio, typically with higher expected return and higher volatility.

Liability‑driven investors allocate between these two portfolios depending on funding status, risk tolerance, and sponsor support. Glidepaths formalize how this allocation changes over time.

Key Term: glidepath

A predetermined roadmap or rule set for altering portfolio risk exposure as funding status, time horizon, or other state variables change, typically by adjusting the mix between growth (return‑seeking) and defensive (hedging) assets.

A glidepath may be expressed as a formula (e.g., equity weight as a function of funding ratio), a table of asset mixes at different funding levels, or a set of dynamic rules.

Funding Ratio Glidepaths

A funding ratio glidepath provides a disciplined schedule or rule for adjusting portfolio risk exposure based on current funding status. It typically:

- Lowers allocation to risky assets as the funding ratio improves, locking in gains and increasing hedging assets.

- Increases risk tolerance if the funding ratio falls below target, using growth assets to restore adequate funding, subject to sponsor’s risk capacity.

Key Term: funding‑status glidepath

A glidepath in which the portfolio’s growth/defensive allocation is an explicit function of the current funding ratio or surplus level.

In a typical pension application:

- When severely underfunded, the plan may allocate a larger share to equities and other growth assets, accepting higher surplus volatility to seek higher expected returns.

- As it approaches full funding, the allocation gradually shifts towards long‑duration bonds and liability‑matching instruments.

- Once overfunded, the plan may mostly hedge liabilities to reduce the probability of falling back into deficit.

Why Glidepaths

Glidepaths aim to align risk exposure with the marginal value of additional surplus:

- When underfunded, an incremental unit of surplus is very valuable; the investor may rationally accept more risk.

- When strongly overfunded, the main objective becomes preserving the surplus; the investor should accept less risk and focus on hedging.

They also address governance and behavioral issues:

- Pre‑committed, rules‑based responses reduce the temptation for ad hoc, potentially pro‑cyclical decisions (e.g., “de‑risking at the bottom” after large losses).

- They provide a clear framework for stakeholders (sponsors, boards, beneficiaries) to understand how risk will be managed as conditions change.

Worked Example 1.1

A defined benefit pension scheme has an asset value of $1.1 billion and a present value of liabilities of $1 billion. The current funding ratio is thus 1.1. Its investment policy states: “If the funding ratio exceeds 1.1, reduce equity exposure from 60% to 40%. If the funding ratio falls below 1.0, increase equity allocation to 70%.” If market distress causes both assets and liabilities to fall by 10%, what action should the fund take?

Answer:

After a 10% asset fall: $1.1bn × 0.9 = $0.99bn. Liabilities fall to $0.9bn. New ratio = $0.99bn / $0.9bn ≈ 1.10. Since the ratio is at the threshold, maintain equity at 40%. If markets fell a bit further and the ratio dipped below 1.1, equity would be increased under the glidepath rule. Note that in this scenario, asset and liability values move together, so funding status is roughly preserved. An exam twist could involve liabilities falling by only 5% (if discount rates rise less than asset yields), in which case the funding ratio would deteriorate and might trigger an increase in growth exposure.

This example illustrates that funding ratio dynamics depend on both asset and liability behavior, not solely on asset returns.

MEASURING AND MANAGING FUNDING RATIO RISK

Liability-relative risk measurement evaluates asset-liability interaction through funding ratio variability, unlike asset-only risk based solely on return standard deviation.

Surplus Volatility vs. Portfolio Volatility

Funding status can deteriorate rapidly if asset and liability returns are weakly correlated or become uncorrelated under stress. Asset‑only volatility ignores shifts in liability values.

Surplus volatility captures “true” risk to funding objectives:

- Surplus return: where is asset return and is “liability return.”

- Surplus volatility:

A higher (more negative) correlation between assets and liabilities reduces surplus volatility, all else equal. This is why long‑duration bonds that covary with liability discount rates can be powerful hedging assets despite their own price volatility.

Exam Warning: The CFA exam often tests comprehension of surplus volatility. Many candidates mistakenly focus on portfolio standard deviation alone. Always assess risk in terms of asset–liability interaction and surplus behavior.

From the surplus optimization approach in the curriculum:

- An investor maximizes expected surplus return subject to a penalty on surplus return volatility .

- The risk aversion parameter governs the chosen point on the surplus efficient frontier, not the asset‑only frontier.

In practice, this requires an expanded covariance matrix including liabilities as another “asset class,” with their own expected return, volatility, and correlations with asset classes.

Sensitivity to Asset and Liability Moves

A key element of funding ratio risk management is to quantify, stress test, and simulate how the funding ratio changes given scenarios for both asset and liability valuations.

Key Term: dynamic glidepath

A rule or schedule that adjusts the portfolio’s asset mix or risk level over time in response to changing funding status, time remaining, or other state variables, often used in LDI and goal‑based frameworks.

Scenario analysis might consider:

- Parallel and non‑parallel shifts in the yield curve (affecting both bond prices and the discount rate for liabilities).

- Equity market shocks with different correlations to interest rates.

- Changes in inflation or salary assumptions (for salary‑linked pension plans).

- Demographic or longevity shifts that increase or decrease liability present values.

For example:

- A 100 bp decline in long‑term yields may increase the present value of liabilities by more than 10% if their duration is long, while the asset portfolio may appreciate by less if it has shorter duration. Funding ratio could fall sharply despite positive asset returns.

- If the asset portfolio includes a substantial allocation to long‑duration bonds or interest rate swaps, the asset appreciation may better match the liability increase, stabilizing the funding ratio.

Immunization and Structural Risk

Immunization is a classic ALM technique for interest rate risk.

Key Term: immunization

A fixed‑income strategy that constructs a bond portfolio whose value will be sufficient to meet a given liability (or set of liabilities) at a specified horizon, by matching the portfolio’s duration to the liability horizon and controlling convexity and dispersion.

Key conditions from the fixed‑income curriculum:

- Initial asset value at least equals the present value of the liability.

- Macaulay duration of the asset portfolio matches the liability horizon.

- Portfolio convexity (and thus cash‑flow dispersion) is minimized, reducing sensitivity to non‑parallel yield curve shifts.

Even with immunization:

- There is structural risk if yield curve twists cause asset cash flow yields to diverge from those that would perfectly hedge the liability.

- Regular rebalancing is required to maintain duration and convexity alignment as time passes and yields move.

From a funding ratio standpoint, immunization reduces interest rate‑driven volatility of surplus but may leave other risks (e.g., inflation, longevity, equity risk in return‑seeking assets) unmanaged. Glidepaths often combine partial immunization (for core liabilities) with dynamic allocation of surplus to growth assets.

GLIDEPATHS IN GOAL-BASED PORTFOLIOS

Glidepaths are also prominent in goal‑based investing for individuals. Here, the target funding level is set for a personal or household objective (e.g., retirement, education, legacy). The allocation to risky assets is systematically adjusted as:

- The goal date approaches (time‑based dimension).

- Assets accumulate relative to the required future sum (funding‑status dimension).

Key Term: goal‑based investing

An approach that structures portfolios around specific investor goals, measuring success and risk relative to the probability of meeting each goal rather than overall wealth or benchmark performance. Key Term: time‑based glidepath

A glidepath that adjusts the portfolio’s growth/defensive mix based primarily on time remaining to a target date, typically reducing equity exposure as the horizon shortens.

In practice, individual glidepaths often combine:

- A time‑based component: reflects declining human capital and risk capacity as retirement approaches.

- A funding‑status component: responds to whether the investor is ahead of or behind the required savings trajectory.

For example, many target‑date funds reduce the equity allocation steadily from, say, 90% several decades before retirement to 40–50% by the retirement date. More advanced designs incorporate funding level relative to the income replacement goal.

Key Term: economic balance sheet

A comprehensive view of an individual’s wealth that includes financial capital (investment assets), human capital (present value of future labor income), pension wealth, and other assets such as home equity.

From the human capital reading:

- Early in life, human capital is large relative to financial capital and often bond‑like (stable employment in safe sectors) or equity‑like (volatile earnings in cyclically sensitive sectors).

- As retirement nears, human capital declines and financial capital becomes relatively more important in sustaining consumption.

Time‑based glidepaths can be justified as:

- Holding more risky financial assets when human capital is large and stable (total wealth is less sensitive to financial market shocks).

- Gradually de‑risking financial assets as human capital is depleted and consumption depends increasingly on portfolio wealth.

Worked Example 1.2

Maria aims to fund her child's university tuition in 15 years, estimated at $200,000 in today's terms. She invests in a portfolio with a dynamic glidepath: 90% equity at wealth less than target (below $150,000 present value), cutting to 50% equity once assets reach $180,000 (present value of tuition at current date). How does this approach help?

Answer:

The glidepath increases upside potential when Maria lags her goal, by maintaining 90% equity to seek higher expected returns. Once assets are close to fully funding the goal (above $180,000 present value), the glidepath reduces equity exposure to 50%, emphasizing capital preservation. This lowers the chance that adverse markets late in the horizon will push the portfolio below the amount needed for tuition. For exam purposes, note that this is a funding‑status glidepath layered on a time horizon; it explicitly ties risk exposure to the distance between current wealth and the present value of the goal.

Worked Example 1.3

Consider two 45‑year‑old investors, both targeting retirement at 65. Each currently has $500,000 in financial assets. Investor A has human capital valued at $1 million (low job security), while Investor B has human capital valued at $3 million (stable, high‑earning profession). Both have similar risk tolerance. How might an optimal glidepath differ between them?

Answer:

Investor B, with larger and more stable human capital, can sustain more volatility in financial assets without jeopardizing expected consumption. A plausible glidepath could assign B a higher starting equity allocation (e.g., 80%) that declines more slowly, while A might start at 60–70% equity and de‑risk more aggressively as retirement approaches. This illustrates that time‑based glidepaths should be adapted to individual circumstances (economic balance sheets), not applied mechanically. On the exam, be prepared to argue for a less conservative glidepath for investors with higher human capital and longer, stable earnings prospects, even if they are the same age as others.

In retirement planning, glidepaths can also interact with annuity decisions:

- Purchasing life annuities converts part of financial capital into “bond‑like” lifetime income.

- This can allow the remaining portfolio to be invested more aggressively or, alternatively, maintain a low‑risk stance depending on risk preferences.

RISK BUDGETING AND GLIDEPATH DESIGN

Effective risk management requires explicit risk budgets—rules for how much surplus volatility or funding ratio risk is tolerable at different funding statuses and horizons.

Key Term: risk budget

A quantified limit on the amount of risk (e.g., surplus volatility, tracking error, probability of shortfall, or maximum drawdown) that an investor is willing to accept, often allocated across strategies, asset classes, or time.

Designing a funding ratio or time‑based glidepath typically involves:

-

Step 1: Define risk and success metrics.

- For a pension: surplus volatility, probability that the funding ratio falls below a critical threshold (e.g., 0.9) over 5–10 years, or expected contribution volatility for the sponsor.

- For an individual: probability of failing to meet a given goal, maximum acceptable drawdown in real consumption, or shortfall risk on the retirement income efficient frontier.

-

Step 2: Set risk budgets by state.

- Underfunded states may permit higher surplus volatility and greater allocation to return‑seeking assets.

- Near full funding, risk budgets become tighter; surplus volatility and shortfall probabilities should be constrained.

- Overfunded states often have the lowest risk budgets, aiming to lock in surplus.

-

Step 3: Map states to asset mixes (the glidepath). For instance, a simplified pension glidepath might be:

- Funding ratio < 0.9: 70% growth assets, 30% hedging assets.

- 0.9 ≤ funding ratio < 1.1: 50% growth, 50% hedging.

- Funding ratio ≥ 1.1: 20% growth, 80% hedging.

The specific percentages would be calibrated via surplus‑based simulations or optimization.

-

Step 4: Implement and monitor.

- Track funding ratio and surplus regularly (e.g., quarterly).

- Rebalance when thresholds are crossed or deviations exceed tolerance bands.

- Use derivatives (equity index futures, interest rate swaps) where appropriate to adjust exposures quickly and cost‑effectively.

From the derivatives reading:

- Interest rate swaps and bond futures can be used to adjust duration to match liability sensitivity without fully restructuring the bond portfolio.

- Equity futures can adjust equity exposure rapidly to follow a glidepath while keeping existing managers and mandates stable.

Revision Tip: Dynamic glidepaths are effective only if monitored and regularly enforced. In exam scenarios, always mention the need for ongoing tracking, governance support, and clear delegation of rebalancing authority.

Formal vs. Heuristic Risk Controls

The equity portfolio construction reading distinguishes between:

- Formal constraints: based on statistical risk measures such as volatility, tracking error, VaR, or CVaR.

- Heuristic constraints: rules on position size, sector limits, or style tilts.

In an LDI or goal‑based context:

- Formal risk budgets might cap surplus volatility at, say, 10% per year or limit the 5‑year probability of a funding ratio below 0.9 to 5%.

- Heuristic rules may restrict maximum equity weights, illiquid allocations, or leverage usage along the glidepath.

Examiners may expect you to:

- Recommend an appropriate risk metric (e.g., surplus volatility rather than asset volatility) given the investor’s objectives.

- Show how a proposed glidepath respects both formal risk limits (e.g., shortfall probability) and heuristic constraints (e.g., maximum equity allocation).

LIMITATIONS AND PRACTICAL CHALLENGES

While glidepaths provide rule‑based discipline, they are not foolproof. Key limitations include:

-

Model and parameter risk:

- Surplus optimization and glidepath calibration rely on capital market assumptions (expected returns, volatilities, correlations) and liability assumptions (discount rates, mortality, salary growth).

- Mis‑estimation can lead to glidepaths that are either too aggressive (underestimating risk) or too conservative (sacrificing unnecessary return).

-

Liability uncertainty:

- For pensions and retirement goals, longevity risk and changes in benefit formulas can significantly change liability levels.

- For individuals, changes in life circumstances (career, health, family) alter both human capital and required consumption, potentially invalidating previously calibrated glidepaths.

-

Sudden liability shifts: Regulatory or actuarial changes (e.g., in discount rate methodology, longevity tables) can cause abrupt increases in , triggering unexpected breaches of risk budgets or glidepath thresholds.

-

Asset–liability correlation instability:

- Historical correlations between assets and liability drivers may break down in stressed markets. For example, an equity sell‑off coinciding with a drop in yields can both reduce asset values and increase , severely harming funding ratios.

- LDI strategies heavily reliant on historical correlation structures may underperform in such environments.

-

Illiquidity and implementation frictions:

- Many institutional portfolios include illiquid assets (private equity, real estate, infrastructure). Rebalancing these to follow a glidepath is slow and costly.

- Adjustments may need to be implemented via liquid overlays (e.g., futures), introducing basis risk and collateral/margin management issues.

-

Governance and behavioral challenges:

- Sponsors or individuals may find it psychologically difficult to increase risk after losses (when funding ratios fall), even if the glidepath calls for it.

- Conversely, they may resist de‑risking in strong markets due to greed or performance‑chasing, undermining the discipline of the glidepath.

-

Overly rigid rules:

- A purely mechanical glidepath may fail to exploit unusually attractive or unattractive market conditions.

- Some discretion (within guardrails) may be beneficial, combining glidepath discipline with opportunistic tactical tilts.

For exam essays, it is often effective to:

- Acknowledge the conceptual benefits of glidepaths (discipline, alignment with funding objectives).

- Enumerate key implementation challenges.

- Suggest mitigants: regular review of assumptions, stress testing, clear governance, use of derivatives for fine‑tuning, and integrated consideration of human capital and sponsor support.

Summary

Liability‑driven and goal‑based investing shift the focus of risk measurement from asset volatility to the risk of not meeting future obligations—operationalized via funding ratio risk and surplus volatility. These approaches recognize that asset and liability values move together, and that the correlation between them is important.

Funding ratio risk is best understood through:

- Surplus returns and surplus volatility.

- Scenario analysis and stress testing of both assets and liabilities.

- Shortfall probabilities with respect to critical funding thresholds.

Dynamic glidepaths—whether based on funding status, time to horizon, or both—are practical tools for:

- Adjusting the mix between hedging and return‑seeking assets as conditions change.

- Aligning risk exposure with the marginal value of surplus across different funding states.

- Embedding pre‑committed, rules‑based discipline into asset allocation decisions.

Effective implementation requires:

- Thoughtful risk budgeting, using surplus‑relative metrics.

- Robust ALM processes that account for liability characteristics and human capital (for individuals).

- Ongoing monitoring, governance support, and recognition of limitations such as model risk, liability uncertainty, and implementation frictions.

Understanding these concepts—and being able to integrate them in institutional and individual contexts—is important for CFA Level 3 performance, especially in constructed‑response questions involving funding status, surplus management, and dynamic asset allocation.

Key Point Checklist

This article has covered the following key knowledge points:

- Define and explain funding ratio, surplus, funding status, and funding ratio risk in portfolio management.

- Distinguish surplus volatility from asset‑only volatility and explain why it is the relevant risk metric for LDI investors.

- Apply asset‑liability management concepts, including surplus optimization and immunization, to both institutional and goal‑based portfolios.

- Design and interpret funding‑status glidepaths and time‑based glidepaths, including their mapping from funding ratio states to growth/defensive allocations.

- Explain how human capital and the economic balance sheet inform glidepath design for individual investors.

- Manage surplus volatility within formal and heuristic risk budgets using dynamic rebalancing rules and derivative overlays.

- Assess limitations and practical implementation challenges for glidepath frameworks, including model risk, liability shocks, illiquidity, and governance issues.

Key Terms and Concepts

- liability‑driven investing (LDI)

- liability

- funding ratio

- surplus

- funding status

- funding ratio risk

- surplus volatility

- asset‑liability management (ALM)

- hedging portfolio

- return‑seeking portfolio

- glidepath

- funding‑status glidepath

- dynamic glidepath

- immunization

- goal‑based investing

- time‑based glidepath

- economic balance sheet

- risk budget